|

시장보고서

상품코드

1940796

미국의 시설 관리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

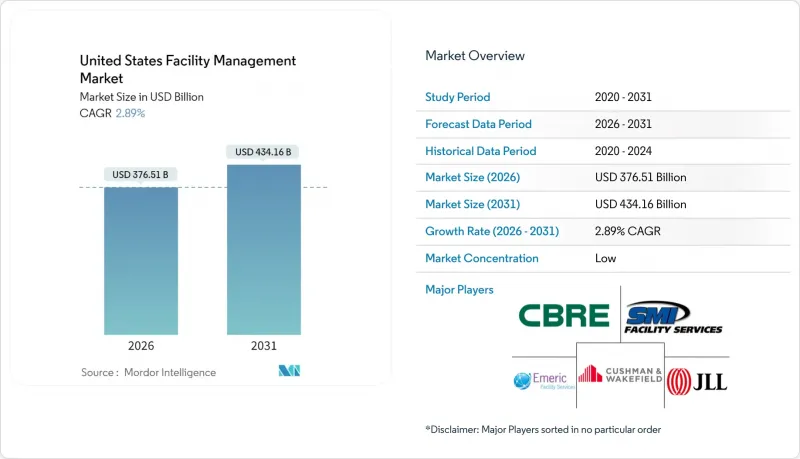

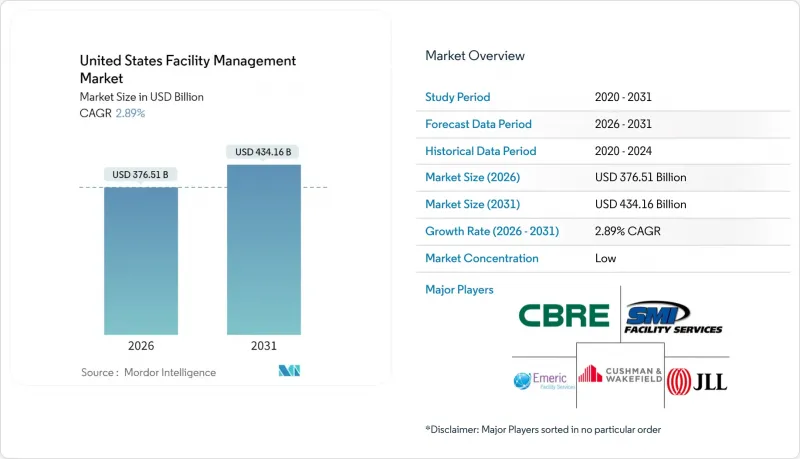

미국의 시설 관리 시장은 2025년에 3,659억 3,000만 달러로 평가되었고, 2026년 3,765억 1,000만 달러에서 2031년까지 4,341억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 2.89%로 예상됩니다.

상업용 부동산의 공실률은 오피스 자산의 경우 14.1%인 반면, 산업용 부동산의 경우 견조한 흡수가 진행되어 서비스 수요의 분기를 낳고 있습니다. 조직이 공조설비(HVAC), 소방설비, 인프라 유지보수를 미룰 수 없기 때문에 하드 서비스가 주도적인 위치에 있으며, 팬데믹 이후 업무 환경에서는 보안 및 웰빙 프로토콜을 강화해야 하기 때문에 소프트 서비스에 대한 수요도 증가하고 있습니다. 인플레이션 억제법에 따라 연방정부 건물 개보수에 9억 7,500만 달러가 배정되어 에너지 효율적 개보수 수요를 촉진하는 등 규제 역시 결정적입니다. IoT 센서에서 AI 기반 예지보전에 이르는 기술 통합은 다운타임을 줄이고 유틸리티를 최적화하여 운영 모델을 변화시키고 있습니다.

미국의 시설 관리 시장 동향 및 인사이트

주요 도시권의 도시화와 인구 증가

오스틴, 피닉스 등 선벨트 지역의 거점 도시들은 기업과 주민들을 계속 끌어들이고 있으며, 스마트 빌딩 플랫폼을 통합한 신규 시설과 리노베이션 공사에 대한 수요가 증가하고 있습니다. 이들 시장의 시설 관리자는 다양한 자산 포트폴리오에서 고도의 자동화와 레거시 인프라를 조화시켜야 합니다. 지식경제의 테넌트들은 유연한 공간을 중요시하며, 서비스 제공업체들은 실시간 점유율 분석을 제공해야 하는 상황에 직면해 있습니다. 잇따른 이상기후로 인해 기후 변화에 대한 내성이 필수적으로 요구되고 있으며, 긴급 유지보수 계획의 요구사항이 강화되고 있습니다. 이러한 복합적인 압력으로 인해 서비스의 복잡성과 비용이 증가하고 있습니다.

미국 인프라 법안의 부문별 투자 우선 순위

연방정부 지출로 9억 7,500만 달러가 4,000만 평방피트 규모의 공공건물 개보수에 사용되어 주정부 차원의 유사한 기준의 파급효과를 주도하고 있습니다. '미국 제품 우선' 조항과 '현행 임금' 조항은 인건비를 상승시켜 시설 관리자에게 조달 전략과 인력 전략의 정교화를 요구하고 있습니다. 전력망 현대화에 대한 지출은 EV 충전기 유지 관리 및 에너지 저장 시스템 통합에 대한 책임을 추가합니다. 소유주가 보조금 자격에 대한 보증을 요구함에 따라 FM 계약에서 컴플라이언스 추적은 중요한 요소가 되었습니다. 이렇게 공공 지출이 민간 서비스 설계를 형성하고 있습니다.

주요 FM 사업자의 수익성 지표

2024년에는 영업비용이 매출 성장률을 상회하여 이익률이 축소되고 기술 투자가 제한될 것으로 예측됩니다. ABM인더스트리는 3.3%의 매출 성장을 기록했지만, 임금 및 공공요금 인플레이션으로 인해 이익이 잠식되었습니다. 분산된 경쟁 환경은 가격 결정력을 제한하고 있으며, 특히 고비용의 사이버 보안 및 규제 대응 서비스에서 두드러지게 나타나고 있습니다. 공공요금에서 전기요금이 차지하는 비중이 58.9%로 상승하면서 전가된 가격 책정이나 서비스 품질 저하를 강요당하고 있습니다. 이러한 압박으로 인해 소규모 사업자들은 통합 또는 틈새 분야로 특화할 수밖에 없는 상황에 처해 있습니다.

부문 분석

하드 서비스는 고객이 비재량적 자산 유지보수에 우선순위를 두면서 2025년 미국의 시설 관리 시장의 58.45%를 차지할 것으로 예측됩니다. 예지보전 도구와 IoT 센서는 기존의 MEP 업무를 데이터 기반 루틴으로 전환하여 예기치 못한 다운타임을 억제하고 있습니다. 점점 더 엄격해지는 화재 예방 및 에너지 절약 기준에 대한 대응은 비용 압박 속에서도 수요를 지탱하고 있습니다. 규제 주도의 시설물 갱신으로 인해 미국의 시설 관리 시장의 하드 서비스 규모는 완만한 증가 추세를 유지할 것으로 예측됩니다. 소프트 서비스는 CAGR 3.74%로 확대되고 있으며, 현재 AI 지원 모니터링 시스템, 감염 방지 청소, 하이브리드 업무에 적응하는 유연한 케이터링 모델이 패키지로 제공되고 있습니다.

소프트 서비스 제공 기업은 ESG를 고려한 청소용 화학약품, 인력 배치를 적정화하는 실시간 점유 데이터로 차별화를 꾀하고 있습니다. 보안 계약에 출입통제 장비의 사이버 물리적 감시가 포함되는 경우가 증가하고 있습니다. 팬데믹 이후 직원 경험 개선 방안이 계속되는 가운데, 직장 지원 서비스의 중요성이 커지고 있습니다. 그러나 노동력 부족에 따른 임금 상승이 수익성을 압박하고 있습니다. 이러한 상황에서 미국의 시설 관리 시장 전체에서 하드웨어 자산의 건전성과 거주자의 웰빙 지표를 통합하는 플랫폼을 중심으로 생태계가 진화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United States facility management market was valued at USD 365.93 billion in 2025 and estimated to grow from USD 376.51 billion in 2026 to reach USD 434.16 billion by 2031, at a CAGR of 2.89% during the forecast period (2026-2031).

Commercial real-estate vacancy at 14.1% in office assets contrasts with robust industrial absorption, shaping divergent demand for services. Hard services hold sway because organizations cannot postpone HVAC, fire-safety or infrastructure upkeep, yet soft services gain ground as post-pandemic workplaces demand heightened security and wellness protocols. Regulation is equally decisive; the Inflation Reduction Act allocates USD 975 million to federal building upgrades, accelerating demand for energy-efficient retrofits. Technology integration-from IoT sensors to AI-based predictive maintenance-reshapes operating models by cutting downtime and optimizing utilities.

United States Facility Management Market Trends and Insights

Urbanization and Population Growth in Major Metros

Sun Belt hubs such as Austin and Phoenix continue to attract businesses and residents, increasing demand for both new facilities and retrofits that incorporate smart-building platforms. Facility managers in these markets must juggle advanced automation with legacy infrastructure across mixed portfolios. Knowledge-economy tenants emphasize flexible spaces, pushing service providers to offer real-time occupancy analytics. Climate resilience has become integral after successive extreme-weather events, intensifying requirements for emergency maintenance planning. These combined pressures elevate service complexity and costs.

Sector Investment Priorities in United States Infrastructure Bills

Federal outlays direct USD 975 million to upgrade 40 million sq ft of public buildings, anchoring a spill-over of similar standards at state level. Buy-American and prevailing-wage clauses inflate labor costs, compelling facility managers to refine procurement and workforce strategies. Grid-modernization spending adds responsibilities for EV-charger upkeep and energy-storage integration. Compliance tracking now factors prominently into FM contracts as owners seek assurance of bill eligibility. Thus, public spending shapes private service design.

Profitability Rates of Major FM Players

Operating expenses exceeded revenue growth in 2024, shrinking margins and constraining tech investment. ABM Industries posted 3.3% revenue expansion but faced wage and utility inflation that eroded gains. Fragmented competition limits pricing power, especially for costly cyber-security and regulatory services. Elevated electricity now equals 58.9% of utility spend, forcing either pass-through pricing or service downgrades. The squeeze pushes small providers toward consolidation or niche specialization.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Drivers Specific to Labour and Safety Standards

- Technology-Led Integrated FM (IoT, BMS, AI-Based Predictive Maintenance)

- Workforce Indicators - Labor Participation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services controlled 58.45% of the United States facility management market in 2025 as clients prioritized non-discretionary asset upkeep. Predictive maintenance tools and IoT sensors are turning legacy MEP tasks into data-driven routines that curb unplanned downtime. Compliance with ever-tighter fire-safety and energy codes bolsters demand even amid cost pressures. The United States facility management market size for hard services will continue to edge upward given regulation-driven upgrades. Soft services, expanding at a 3.74% CAGR, now bundle AI-enabled surveillance, infection-control cleaning, and flexible catering models aligning with hybrid work.

Soft-service providers differentiate through ESG-aligned cleaning chemicals and real-time occupancy data that right-size staffing. Security contracts increasingly incorporate cyber-physical monitoring of access-control devices. As post-pandemic employee-experience initiatives endure, workplace support offerings gain relevance. However, labour shortages inflate wages, challenging profitability. The ecosystem thus evolves around integrated platforms that merge hard-asset health with occupant wellness metrics across the broader United States facility management market.

The United States Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-House, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and More), and Geography (Northeast, Southeast, Midwest, Southwest, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABM Industries

- Emcor Group Inc.

- CBRE Group Inc.

- Jones Lang LaSalle IP, Inc.

- Cushman & Wakefield PLC

- Sodexo Inc.

- ISS Facility Services Inc.

- GDI Integrated Facility Services

- Kellermeyer Bergensons Services

- Guardian Service Industries Inc.

- AHI Facility Services Inc.

- Emeric Facility Services

- SMI Facility Services

- Shine Management and Facility Services

- Haworth Inc.

- Servicon Systems Inc.

- UG2 Facility Services

- Alpine Building Maintenance

- Aramark

- Broadway Building Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%) - by Service Type

- 4.1.5 Facility Management Market Share (%) - by Hard Services

- 4.1.6 Facility Management Market Share (%) - by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in US Infrastructure Bills

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Drivers

- 4.2.1 Urbanization and Population Growth in Major Metros

- 4.2.2 Sector Investment Priorities in US Infrastructure Bills

- 4.2.3 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2.4 Technology-Led Integrated FM (IoT, BMS, AI-Based Predictive Maintenance)

- 4.2.5 Building Performance Standards Mandates Driving Retro-Commissioning Services

- 4.2.6 Inflation Reduction Act Tax Incentives Accelerating Decarbonization Retrofit Demand

- 4.3 Restraints

- 4.3.1 Profitability Rates of Major FM Players

- 4.3.2 Workforce Indicators - Labor Participation

- 4.3.3 Rising Commercial Real Estate Vacancies in Urban Cores

- 4.3.4 Increasing Cybersecurity Liability Exposure in Connected Building Systems

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses, etc.)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABM Industries

- 6.4.2 Emcor Group Inc.

- 6.4.3 CBRE Group Inc.

- 6.4.4 Jones Lang LaSalle IP, Inc.

- 6.4.5 Cushman & Wakefield PLC

- 6.4.6 Sodexo Inc.

- 6.4.7 ISS Facility Services Inc.

- 6.4.8 GDI Integrated Facility Services

- 6.4.9 Kellermeyer Bergensons Services

- 6.4.10 Guardian Service Industries Inc.

- 6.4.11 AHI Facility Services Inc.

- 6.4.12 Emeric Facility Services

- 6.4.13 SMI Facility Services

- 6.4.14 Shine Management and Facility Services

- 6.4.15 Haworth Inc.

- 6.4.16 Servicon Systems Inc.

- 6.4.17 UG2 Facility Services

- 6.4.18 Alpine Building Maintenance

- 6.4.19 Aramark

- 6.4.20 Broadway Building Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)