|

시장보고서

상품코드

1940841

베트남의 비료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

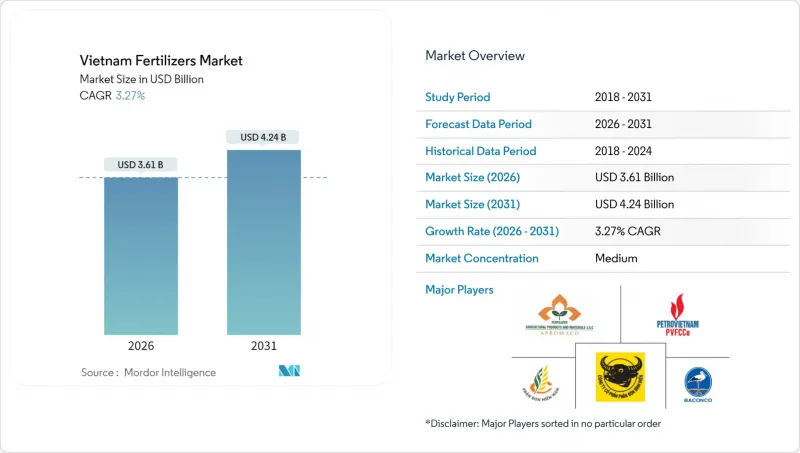

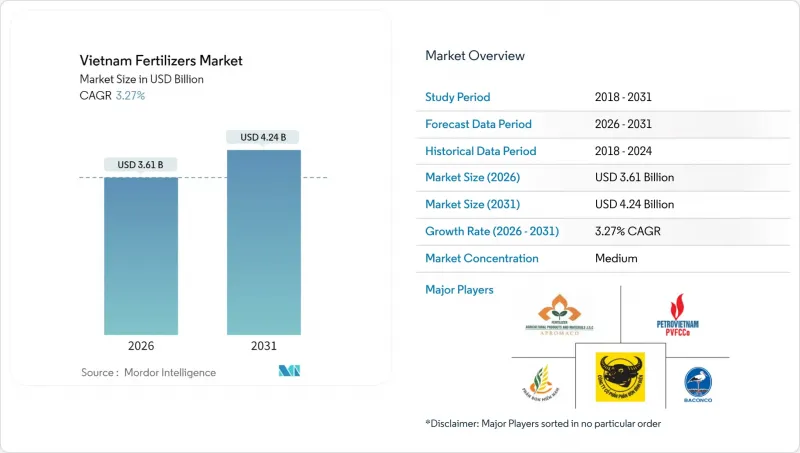

베트남의 비료 시장 규모는 2025년 35억 달러에서 2026년에 36억 1,000만 달러로 성장할 것으로 예측됩니다.

2031년에는 42억 4,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 3.27%의 성장률을 보일 것으로 전망됩니다.

베트남은 국내 우레아 잉여, 정부의 강력한 현대화 프로그램, 캄보디아, 한국, 필리핀으로의 수출 확대의 혜택을 누리고 있습니다. 물류비 상승과 5%의 부가가치세(VAT) 도입으로 인한 비용구조의 변화가 경쟁 압력으로 작용하고 있지만, 세액공제 제도는 궁극적으로 국내 생산자에게 유리하게 작용할 것입니다. 고부가가치 수출 작물용 정밀 시비 시스템 및 특수 비료에 대한 수요가 기술 투자를 견인하는 반면, 위조품 수입과 칼륨염, DAP에 대한 의존도가 수익률을 지속적으로 압박하고 있습니다. 한편, 국내 주요 기업들의 적극적인 생산능력 증설과 세계 유통업체와의 제휴를 통해 베트남은 지역 비료 허브로서의 역할을 강화하고 있습니다.

베트남의 비료 시장 동향 및 분석

국내 우레아 잉여가 수출 확대를 견인

베트남에서는 연간 약 120만 톤의 우레아가 잉여 생산되고 있으며, 2024년에는 173만 톤(7억 9,900만 달러 상당)을 수출하여 2023년 대비 11.7% 증가한 수량을 달성했습니다. 수출 대상국의 34.3%를 캄보디아가 차지하고 있으며, 한국이 12.7%, 필리핀이 6.3%로 그 뒤를 잇고 있습니다. 원가 우위는 후미 및 카마우 가스 통합 단지에서 비롯되며, 경쟁력 있는 원재료 가격을 확보하고 있습니다. 수출 확대는 운송 리스크를 분산시키고, 공장 가동률을 향상시켜 내수 수요 둔화에도 국내 수익을 지탱하고 있습니다.

5%의 부가가치세(VAT) 공제로 국내 생산 비용 감소

베트남의 비료 시장에서 5%의 부가가치세(VAT) 공제 시행은 국내 제조업체의 생산비용을 절감하고 수입품에 대한 경쟁력을 강화할 것입니다. 2025년 7월 1일부터 소비세 면세에서 5% 과세제도로 전환됨에 따라 생산자는 천연가스 및 설비에 대한 임베디드세액공제를 적용받을 수 있게 됩니다. 이번 세제 개정으로 완전 과세 대상인 수입 비료에 비해 순 생산비용이 감소합니다. 이번 조치로 인해 운전자금 수요는 증가하지만, 특히 인산이암모늄(DAP)과 칼륨 수입가격이 상승하는 성수기에 국내 기업의 수익률을 강화할 수 있습니다.

원거리 지역으로의 액체 비료 및 서방형 비료(CRF)의 높은 물류 비용

베트남의 외딴 지역으로 액체 비료 및 서방형 비료(CRF) 운송에 따른 높은 물류 비용이 시장 성장을 제약하고 있습니다. 이러한 비용은 최종 가격을 높이고, 채택률을 낮추며, 시장 침투를 저해합니다. 인프라의 제약, 공급망의 비효율성, 국제 운송에 대한 의존으로 인해 베트남의 물류 비용은 농업 관련 사업 수익에서 큰 비중을 차지하고 있습니다. 베트남의 비료 물류비용 중 운송비는 60%를 차지하며, 세계 평균 30%를 크게 상회하고 있습니다. 팬데믹 이전 컨테이너당 3,000달러였던 해상 운송비는 2024년 14,000달러로 상승했습니다. 또한, 산악지대인 북서부 지역으로의 도로 접근은 여전히 제한되어 있습니다. 액체 비료와 서방형 비료의 온도 관리 운송 요건은 배송 비용을 더욱 증가시켜 델타 지역 이외의 지역에서는 특수 비료의 도입을 제한하고 있습니다.

부문 분석

2025년 기준 단일 성분 비료는 베트남의 비료 시장 점유율의 76.65%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 3.42%로 가장 빠르게 성장할 것으로 예측됩니다. 이는 쌀, 옥수수, 사탕수수 생산에 있어 비용을 중시하는 소규모 농가의 이용이 주도하고 있습니다. 이 카테고리 내에서 요소는 국내 생산의 경제성 덕분에 혜택을 받고 있지만, DAP(인산암모늄)와 MAP(인산일암모늄)은 수입 의존도가 높아 가격 변동 요인이 되고 있습니다. 복합비료는 점유율은 작지만, 유황과 미량 영양소를 배합한 균형 잡힌 NPK 혼합비료를 원하는 농장주들 수요로 인해 더 빠른 속도로 성장하고 있습니다.

우레아의 가용성은 전통적인 살포 시비를 뒷받침하고 있지만, 휘발에 의한 질소 손실로 인해 억제제 및 코팅 기술에 대한 관심이 높아지고 있습니다. 복합 배합 비료는 수출용 수확량을 목표로 하는 커피 및 과수 재배자들의 지지를 받고 있습니다. 미량영양소 배합 제품은 초기 단계이지만, 라테라이트 토양에 많은 아연, 붕소 결핍을 해소하여 과실의 품질 프리미엄 향상에 기여하고 있습니다. 정부의 지속적인 영양 관리 교육으로 인해 2030년까지 균형 잡힌 배합 제품으로 수요 전환이 예상됩니다.

2025년 현재 베트남의 비료 시장의 94.85%는 재래식 과립형 비료가 차지할 것으로 예상되며, 이는 기존의 유통망과 살포 도구에 대한 익숙함이 반영된 것입니다. 특수형 비료는 시비 관개 및 온실 재배의 확대로 인해 2031년까지 연평균 복합 성장률(CAGR) 3.58%를 나타낼 것으로 예측됩니다. 수용성 결정 및 액체 현탁액은 점적 관개하는 열대 과수원에서 빠른 흡수를 실현하고 과립형 비료 살포에 비해 영양 효율을 향상시킵니다.

서방형 비료는 높은 가격대에 위치하며, 원거리로 운송 비용이 높지만, 대규모 커피 농장은 인건비 절감을 위해 높은 지출을 감수하고 있습니다. 미생물 접종제와 휴민산 강화 액비는 토양 건강 문제에 대응하고 유기농 인증 기준을 충족합니다. 디지털 플랫폼의 확장으로 특수 비료 제조업체는 틈새 수요에 효율적으로 대응할 수 있게 되었으며, 주요 생산업체의 제품 포트폴리오 다각화를 촉진하고 있습니다.

베트남의 비료 시장은 유형(복합비료와 단일비료), 형태(재래식 및 특수제품), 적용방법(관개, 엽면살포, 토양살포), 작물 유형(밭작물, 원예작물 등)에 따라 세분화되어 있습니다. 시장 예측은 금액(USD)과 수량(미터톤)으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 보고서 제공

제3장 주요 요약 주요 조사 결과

제4장 주요 산업 동향

제5장 시장 규모와 성장 예측(수량과 금액)

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

LSH 26.03.11Vietnam fertilizers market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.5 billion with 2031 projections showing USD 4.24 billion, growing at 3.27% CAGR over 2026-2031.

Vietnam benefits from surplus domestic urea, strong government modernization programs, and growing exports to Cambodia, South Korea, and the Philippines. Competitive pressure comes from logistics inflation and a new 5% VAT that changes cost dynamics, yet the tax credit mechanism ultimately favors local producers. Precision-fertigation systems and specialty fertilizer demand for high-value export crops are driving technology investment, while counterfeit imports and dependence on potash and DAP continue to weigh on margins. Meanwhile, aggressive capacity additions by domestic leaders and alliances with global distributors strengthen Vietnam's role as a regional fertilizer hub.

Vietnam Fertilizers Market Trends and Insights

Surplus Domestic Urea Driving Export Push

Vietnam produces a urea surplus of about 1.2 million metric tons annually, enabling 2024 exports of 1.73 million metric tons valued at USD 709.91 million, a 11.7% volume jump over 2023. Cambodia absorbed 34.3% of shipments, followed by South Korea at 12.7% and the Philippines at 6.3%. Cost advantages stem from integrated gas-based complexes in Phu My and Ca Mau that secure competitive feedstock pricing. The export momentum spreads freight risk and lifts plant utilization, thus buoying domestic earnings even when local demand moderates.

Pending 5% VAT Credit Lowers Local Production Cost

The implementation of 5% VAT credits in Vietnam's fertilizer market reduces production costs for domestic manufacturers, enhancing their competitiveness against imports. The transition from VAT exemption to a 5% VAT regime, effective July 1, 2025, enables producers to reclaim input VAT on natural gas and equipment. This tax adjustment decreases net production costs compared to imported fertilizers subject to full taxation. While the measure increases working capital requirements, it strengthens profit margins for domestic companies, particularly during peak seasons when diammonium phosphate (DAP) and potash import prices increase.

High Logistics Cost for Liquids and CRF to Remote Provinces

The high logistics costs associated with transporting liquid fertilizers and Controlled-Release Fertilizers (CRFs) to Vietnam's remote provinces constrain market growth. These costs increase final prices, reduce adoption rates, and restrict market penetration. Vietnam's logistics expenses constitute a significant portion of agricultural business revenue due to infrastructure limitations, supply chain inefficiencies, and dependence on international shipping. Transportation represents 60% of fertilizer logistics costs in Vietnam, compared to the global average of 30%. Ocean freight costs increased from USD 3,000 per container before the pandemic to USD 14,000 in 2024 . Additionally, road accessibility to the mountainous Northwest region remains restricted. The temperature-controlled shipping requirements for liquid and controlled-release fertilizers further increase delivery costs, limiting specialty fertilizer adoption beyond the delta regions.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Fertigation Adoption in Mekong and Red River Deltas

- Government Organic Fertilizer Targets

- Potash and DAP Import Dependence - Exposed to Price Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers captured 76.65% of the Vietnam fertilizers market share in 2025 and show the fastest growth of CAGR 3.42% by 2031, driven by cost-sensitive smallholder practices in rice, corn, and sugarcane production. Within this group, urea benefits from strong domestic production economics, whereas DAP and MAP remain import-dependent, adding price volatility. Complex fertilizers account for a smaller slice yet expand faster as plantation operators seek balanced NPK blends with sulfur and micronutrients.

Urea's accessibility underpins traditional broadcast application, but nitrogen losses through volatilization spur interest in inhibitors and coating technologies. Complex blends find traction with coffee and fruit growers targeting export-grade yields. Micronutrient formulations, though nascent, address zinc and boron deficiencies common in lateritic soils, lifting fruit quality premiums. Continued government education on nutrient stewardship is anticipated to shift volumes toward balanced formulas by decade-end.

Conventional granules dominated 94.85% of the Vietnamese fertilizers market in 2025, reflecting entrenched distribution networks and familiarity with broadcasting tools. Specialty forms posted a 3.58% CAGR through 2031 due to fertigation and greenhouse growth. Water-soluble crystals and liquid suspensions generate rapid uptake in drip-irrigated tropical fruit orchards, improving nutrient efficiency relative to granular top-dressing.

Controlled-release fertilizers command premium pricing and face steep freight costs to remote provinces, but large coffee estates accept higher outlays to cut labor costs. Microbial inoculants and humic-enriched liquids address soil health concerns and meet organic certification criteria. As digital platforms expand, specialty suppliers can serve niche demand efficiently, encouraging portfolio diversification among major producers.

The Vietnam Fertilizers Market is Segmented by Type (Complex and Straight), Form (Conventional and Specialty), Application Mode (Fertigation, Foliar, and Soil), and Crop Type (Field Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- PetroVietnam Fertilizer and Chemical Corporation

- PetroVietnam Ca Mau Fertilizer Joint Stock Company

- Baconco Company Limited

- Binh Dien Fertilizer Joint Stock Company

- Duc Giang Chemical Group Joint Stock Company

- Southern Fertilizer Joint Stock Company

- Ninh Binh Phosphate Fertilizer Joint Stock Company

- Agricultural Products and Materials Joint Stock Company

- Haifa Chemicals Ltd.

- Yara International ASA

- Grupa Azoty S.A.

- Lam Thao Fertilizers and Chemicals Joint Stock Company

- Song Gianh Corporation

- Que Lam Group Joint Stock Company

- Israel Chemicals Ltd.

- Nutrien Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surplus domestic urea driving export push

- 4.6.2 Pending 5 % VAT credit lowers local production cost

- 4.6.3 Shift to specialty grades for high-value export crops

- 4.6.4 Precision-fertigation adoption in Mekong & Red River deltas

- 4.6.5 Government organic-fertilizer targets (50 % area by 2050)

- 4.6.6 E-commerce distribution platforms reaching smallholders

- 4.7 Market Restraints

- 4.7.1 High logistics cost for liquids & CRF to remote provinces

- 4.7.2 Counterfeit & sub-standard imports eroding farmer trust

- 4.7.3 Potash & DAP import dependence exposed to price shocks

- 4.7.4 Seasonal inventory glut depressing producer margins

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 TSP

- 5.1.2.3.4 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 PetroVietnam Fertilizer and Chemical Corporation

- 6.4.2 PetroVietnam Ca Mau Fertilizer Joint Stock Company

- 6.4.3 Baconco Company Limited

- 6.4.4 Binh Dien Fertilizer Joint Stock Company

- 6.4.5 Duc Giang Chemical Group Joint Stock Company

- 6.4.6 Southern Fertilizer Joint Stock Company

- 6.4.7 Ninh Binh Phosphate Fertilizer Joint Stock Company

- 6.4.8 Agricultural Products and Materials Joint Stock Company

- 6.4.9 Haifa Chemicals Ltd.

- 6.4.10 Yara International ASA

- 6.4.11 Grupa Azoty S.A.

- 6.4.12 Lam Thao Fertilizers and Chemicals Joint Stock Company

- 6.4.13 Song Gianh Corporation

- 6.4.14 Que Lam Group Joint Stock Company

- 6.4.15 Israel Chemicals Ltd.

- 6.4.16 Nutrien Ltd.