|

시장보고서

상품코드

1940850

유럽의 드라이 믹스 모르타르 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Dry Mix Mortar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

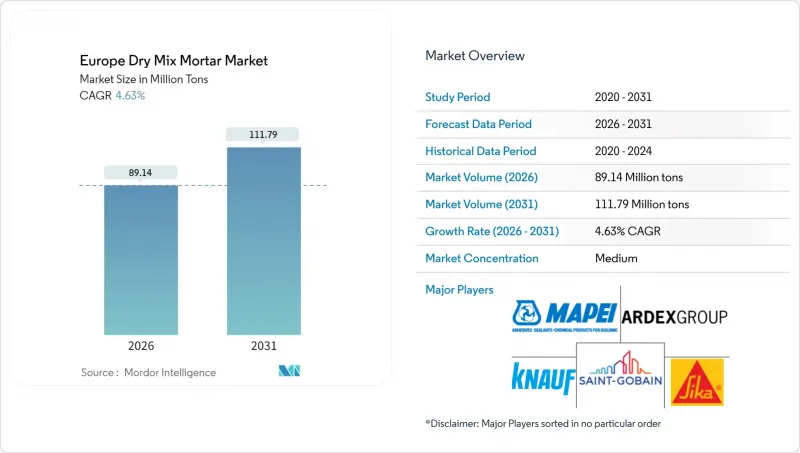

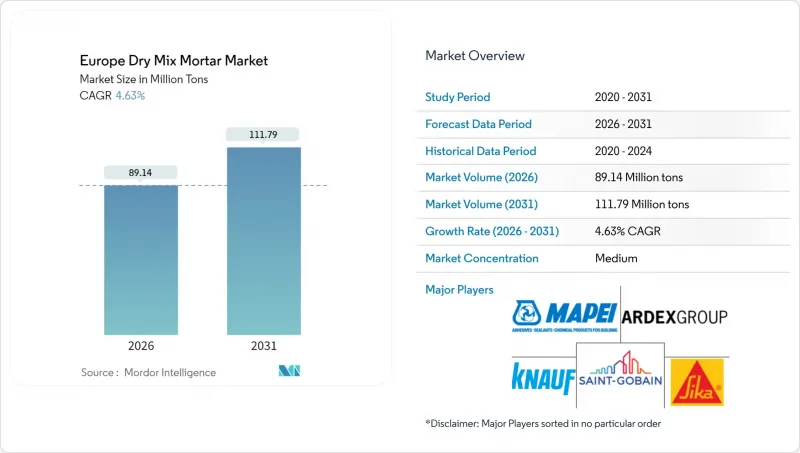

유럽의 드라이 믹스 모르타르 시장은 2025년 8,519만 톤에서 2026년에는 8,914만 톤으로 성장하여 2026년부터 2031년까지 CAGR 4.63%를 기록하며 2031년까지 1억 1,179만 톤에 달할 것으로 예측됩니다.

이러한 성장 궤적은 이 지역의 저탄소 건설로의 결정적인 전환, 공공 부문의 대규모 개조 예산, 유럽 그린딜에 따른 규제 정합성에서 비롯된 것입니다. 노후화된 주택 재고의 개보수 활동, 자동 사일로 배칭의 보급 확대, 재활용 재료 배합에 대한 급속한 제품 혁신이 모두 수요를 촉진하고 있습니다. 경쟁 전략은 원재료 가격 변동을 완화하는 수직적 통합과 엄격한 VOC(휘발성 유기화합물) 및 실리카 분진 기준치를 충족하는 지속적인 제품 연구개발에 초점을 맞추고 있습니다. 전체 경쟁 환경에서는 디지털화된 공장과 순환 경제 첨가제에 대한 투자가 새로운 시장 기회를 개척하는 동시에 지속가능성 인증에서 차별화를 가능하게 하고 있습니다.

유럽 드라이 믹스 모르타르 시장 동향과 인사이트

노후화된 건축 재고가 개보수 수요를 견인합니다.

유럽 건축물의 4분의 3 이상이 1990년 이전에 지어져 현재의 에너지 성능 기준을 충족하지 못하고 있습니다. 독일 연방정부의 보조금 제도와 프랑스의 MaPrimeRenov 프로그램은 미장용 모르타르, 단열 모르타르, 보수용 모르타르에 대한 안정적인 수요를 창출하고 있습니다. 이러한 개보수 수요가 높은 환경에서는 접착력 향상, 저분진, 섬유 혼입 등의 특수 배합이 경쟁우위를 가지고 있으며, 소규모 시공업체도 현장 시공이 용이한 배합의 확대가 제조업체에 요구되고 있습니다. 동시에, 자동 사일로 시스템은 숙련된 미장공의 부족을 완화하고, 밀집된 도시 지역 현장에서도 안정적인 혼합 품질을 제공합니다.

EU 탈탄소화 및 에너지 효율화 지침

개정된 건축물 에너지 성능 지침(EPBD)은 2030년까지 모든 신축 건물이 거의 제로 에너지 상태를 달성하고 기존 건물의 대규모 개보수를 의무화하고 있습니다. 이러한 규제로 인해 제품 개발자들은 재생 미분말이나 시멘트계 보조 재료를 배합한 저탄소 함유 레시피를 채택할 수밖에 없는 상황입니다. 개정된 건설제품 규정에 따라 환경제품신고(EPD)가 의무화될 전망인 가운데, 톤당 250kg CO2e 미만의 제조 공정 배출량을 인증할 수 있는 선행기업은 공공입찰에서 규격 우선권을 획득할 가능성이 높습니다.

원자재 가격 변동성

2024년에는 EU 배출권거래제(EU ETS)에 따른 에너지 인플레이션과 탄소배출권 비용으로 인해 시멘트 가격이 상승할 것으로 예상됩니다. 한편, 골재는 물류 병목현상과 채굴 허가 강화로 인해 가격이 상승했습니다. 원자재 비용은 생산 비용의 최대 70%를 차지하기 때문에 헤지 조치를 취하지 않은 제조업체는 수익률 압박과 계약 가격 조정 지연에 직면했습니다. 독일과 네덜란드 일부 지역의 모래 부족은 특수 미분말의 가격 상승으로 이어졌고, 생산자들은 재생 유리와 쇄석 콘크리트를 대체 충전재로 인정할 수밖에 없었습니다. 이러한 원자재 비용의 변동은 전가 메커니즘이나 대체 원자재가 안정화될 때까지 생산량 증가를 억제하는 요인으로 작용합니다.

부문 분석

2025년 유럽 드라이 믹스 모르타르 시장에서 주택 프로젝트가 52.00%를 차지했습니다. 이는 가속화되는 에너지 절약형 개보수 의무화로 인해 단열재, 렌더링, 스크 리드에 대한 수요가 증가했기 때문입니다. 상업시설은 규모는 작지만, 하이브리드 오피스 리노베이션과 소매점 포맷 업데이트가 활발해지면서 2031년까지 CAGR 6.2%로 가장 높은 성장률을 보일 것으로 예측됩니다. 산업 및 공공시설의 수요는 항균 타일 접착제를 선호하는 제약용 클린룸 건설에 의해 뒷받침되고 있습니다. TEN-T(유럽횡단교통망)에 기반한 인프라 갱신으로 앵커재, 보수용 그라우트, 방수 슬러리에 대한 수요가 꾸준히 증가하고 있습니다.

주택 부문의 우위는 2024년 독일에서 120만 가구의 리노베이션 실적이 기록된 점, 프랑스가 연간 50만 가구의 대규모 리노베이션을 목표로 하고 있는 점 등에 기인합니다. 바이오 기반 섬유와 상변화 마이크로캡슐을 통합한 고성능 렌더링 시스템은 엄격한 U값 기준을 충족시키면서 프리미엄 가격을 보장합니다. 상업 분야의 성장은 사무실 레이아웃을 공동 작업 구역으로 재구성하려는 소유주의 의지에 의해 뒷받침되어 빠른 경화 레벨링 재료에 대한 수요를 촉진하고 있습니다. 산업 분야의 활동은 청정 제조 공장을 의무화하는 법규에 의한 인센티브에 의존하고 있으며, 저 VOC 바닥용 모르타르가 필수적입니다. 시공업체들은 자동 사일로 배칭이 노동력 부족(특히 주택 개보수에서 심각)을 완화하고, 지연 방지와 마감 품질 향상에 기여한다고 지적합니다.

유럽 드라이 믹스 모르타르 시장 보고서는 최종 용도별(상업, 산업 및 공공시설, 인프라, 주거), 용도별(석고, 렌더링, 타일 접착제, 그라우팅, 방수 슬러리, 콘크리트 보호 및 개보수 등), 지역별(프랑스, 독일, 이탈리아, 러시아, 스페인, 영국, 기타 유럽 국가)로 분류되어 있습니다. 별도로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO의 모아 두어의 주요 전략적 과제

KSM 26.03.10The Europe Dry Mix Mortar Market is expected to grow from 85.19 million tons in 2025 to 89.14 million tons in 2026 and is forecast to reach 111.79 million tons by 2031 at 4.63% CAGR over 2026-2031.

This growth trajectory stems from the region's decisive shift toward lower-carbon construction, substantial public-sector renovation budgets, and regulatory alignment under the European Green Deal. Renovation activity in the aging housing stock, the wider adoption of automated silo batching, and rapid product innovation around recycled content formulations are all reinforcing demand. Competitive strategies center on vertical integration to buffer raw material volatility and on continuous product research and development that meets strict VOC and silica dust thresholds. Across the competitive landscape, investments in digitalized plants and circular economy additives are unlocking new market opportunities while enabling differentiation in sustainability credentials.

Europe Dry Mix Mortar Market Trends and Insights

Ageing Building Stock Drives Renovation Demand

More than three-quarters of Europe's buildings were erected before 1990 and fail to meet today's energy-performance thresholds. Germany's federal incentives and France's MaPrimeRenov programs channel steady demand toward render, insulation, and repair mortars. Specialized blends with improved adhesion, low dust, and embedded fibers hold a competitive advantage in this retrofit-heavy environment, encouraging manufacturers to scale formulations that ease site application for smaller contractor crews. At the same time, automated silo systems are mitigating skilled-plasterer shortages and delivering consistent mix quality on dense urban job sites.

EU Decarbonisation and Energy-Efficiency Directives

The recast Energy Performance of Buildings Directive (EPBD) requires all new buildings to achieve nearly zero-energy status by 2030 and mandates the deep renovation of the existing stock. These mandates are prompting product developers to adopt lower-carbon-embodied recipes that incorporate recycled fines and supplementary cementitious materials. With environmental product declarations (EPDs) set to become compulsory under the revised Construction Products Regulation, early movers that can certify cradle-to-gate emissions under 250 kg CO2e per ton are likely to seize specification priority across public tenders.

Raw-Material Price Volatility

Cement prices rose in 2024, driven by energy inflation and carbon allowance costs under the EU ETS, while aggregates increased amid logistical bottlenecks and tighter mining permits. Raw inputs represent up to 70% of production expenses, so unhedged manufacturers faced margin compression and adjustment lags in contract pricing. Sand scarcity in parts of Germany and the Netherlands added a premium on specialty fines, compelling producers to qualify recycled glass and crushed concrete as substitute fillers. Fluctuating input costs thereby temper volume growth until pass-through mechanisms or alternative raw materials stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Prefabricated/Off-Site Construction

- Post-Pandemic Green Infrastructure Stimulus

- Stringent VOC and Silica-Dust Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential projects accounted for 52.00% of the European dry mix mortar market in 2025, as accelerating energy-retrofit mandates drove increased demand for insulation, render, and screed volumes. Commercial premises, although smaller in scale, are projected to post the fastest 6.2% CAGR through 2031 as hybrid office refurbishments and retail format updates intensify. Industrial and institutional demand is fueled by pharmaceutical cleanroom builds that favor antimicrobial tile adhesives. Infrastructure upgrades under TEN-T add steady volumes in anchoring, repair grout, and waterproofing slurries.

The residential segment's primacy stems from Germany's 1.2 million-unit retrofit record in 2024 and France's target of 500,000 deep renovations annually. High-performance render systems integrating bio-based fibers and phase-change microcapsules secure premium pricing while meeting stringent U-value thresholds. Commercial growth benefits from owners' drive to repurpose office layouts into collaborative work zones, boosting demand for rapid-set leveling compounds. Industrial activity leans on legislative incentives for cleaner manufacturing plants, which mandate low-VOC flooring mortars. Contractors note that automated silo batching mitigates labor shortages, particularly those that are acute in residential refurbishment, thereby preventing delays and improving finishing quality.

The Europe Dry Mix Mortar Market Report is Segmented by End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), Application (Plaster, Render, Tile Adhesive, Grout, Waterproofing Slurry, Concrete Protection and Renovation, and More), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Ardex Group

- Baumit Group

- Cemex S.A.B DE C.V.

- Fassa Bortolo

- Holcim

- Kerakoll Spa

- Knauf Group

- LATICRETE International, Inc.

- MAPEI S.p.A.

- Murexin GmbH

- Saint-Gobain

- Sika AG

- SOPREMA International

- Terraco Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing building stock drives renovation demand

- 4.2.2 EU decarbonisation and energy-efficiency directives

- 4.2.3 Growth in prefabricated/off-site construction

- 4.2.4 Post-pandemic green infrastructure stimulus

- 4.2.5 Automated silo batching adoption

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Stringent VOC and silica-dust regulations

- 4.3.3 Skilled spray-plaster labour shortage

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 By Application

- 5.2.1 Plaster

- 5.2.2 Render

- 5.2.3 Tile Adhesive

- 5.2.4 Grout

- 5.2.5 Waterproofing Slurry

- 5.2.6 Concrete Protection and Renovation

- 5.2.7 Insulation and Finishing Systems

- 5.2.8 Other Applications

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardex Group

- 6.4.2 Baumit Group

- 6.4.3 Cemex S.A.B DE C.V.

- 6.4.4 Fassa Bortolo

- 6.4.5 Holcim

- 6.4.6 Kerakoll Spa

- 6.4.7 Knauf Group

- 6.4.8 LATICRETE International, Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Murexin GmbH

- 6.4.11 Saint-Gobain

- 6.4.12 Sika AG

- 6.4.13 SOPREMA International

- 6.4.14 Terraco Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment