|

시장보고서

상품코드

1940857

스테퍼 모터 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Stepper Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

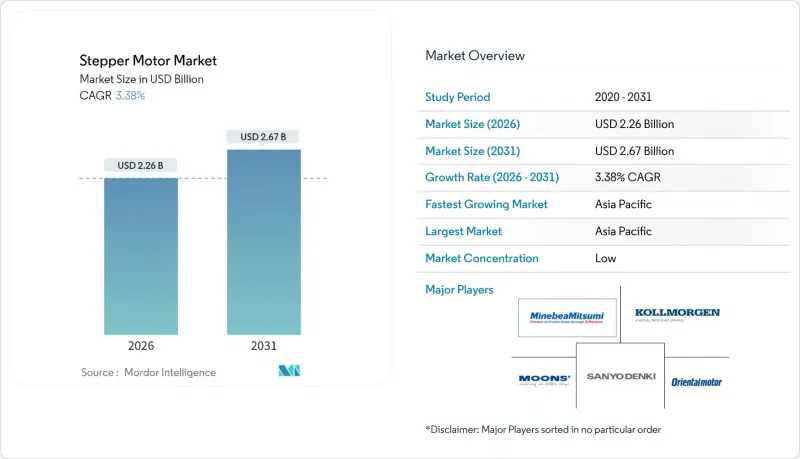

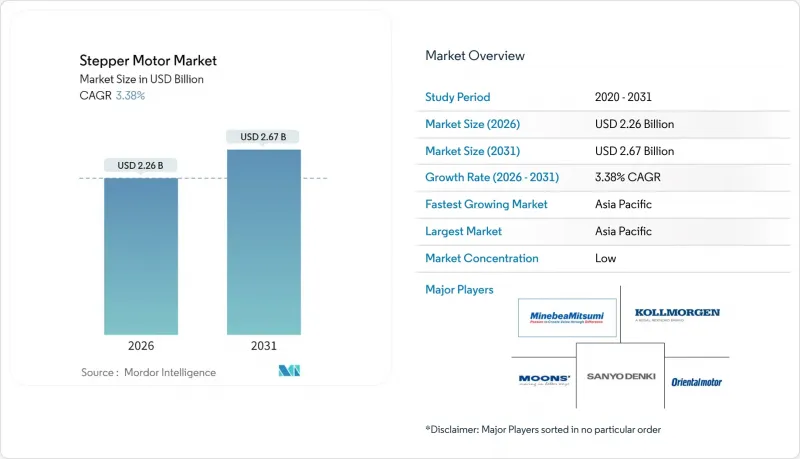

스테퍼 모터 시장은 2025년 21억 9,000만 달러에서 2026년에는 22억 6,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 3.38%를 기록하며 2031년까지 26억 7,000만 달러에 달할 것으로 예측됩니다.

로봇, 의료기기, 반도체 제조 장비 제조업체들이 고가의 서보 플랫폼을 피하기 위해 정밀한 개방형 루프 위치 결정 기술로 스테퍼 기술을 계속 선택함에 따라 수요는 안정적으로 유지되고 있습니다. 협동 로봇은 조립 셀에서 점점 더 많이 사용되고 있으며, 예측 가능한 토크와 간소화된 프로그래밍을 제공하는 소형 NEMA 표준 유닛의 도입이 가속화되고 있습니다. 반도체 설비 투자, 특히 패키징 및 리소그래피 라인에 대한 투자는 클린룸 환경에서 신뢰성 높은 동작을 구현하는 하이브리드 및 선형 제품 수주를 뒷받침하고 있습니다. 또한, 실험실 자동화, 데스크톱 3D 프린터, 배터리 제조 라인에서도 유지보수가 적고 반복성이 높은 액추에이터에 대한 수요가 증가하고 있습니다. 2024년에는 재고 조정으로 인해 모션 제어 분야 전체가 축소되었지만, 2025년 공장 자동화 투자 재개는 안정적인 구매 주기로의 회귀를 의미합니다.

세계 스테퍼 모터 시장 동향 및 인사이트

로봇공학 및 협동 로봇 보급 확대

협동 로봇을 도입하는 제조 공장에서는 예측 가능한 스텝 증분으로 토크 제한이 내재되어 있어 사람과 기계의 안전성을 높이기 위해 스테퍼 구동을 선호합니다. 미국의 리쇼어링 계획과 유럽의 생산성 향상 방안은 마이크로 스테핑 컨트롤러가 장착된 저전압 2상 하이브리드에 대응하는 모듈식 모션 플랫폼이 표준화되고 있습니다. 인코더가 장착된 폐쇄형 루프 모델은 서보에 필적하는 부드러움을 실현하여 픽앤플레이스 시스템의 작업 범위를 확장합니다. 이더넷 기반 프로토콜을 통해 모터는 공장 네트워크에 통합되어 상태 모니터링이 가능하여 예기치 않은 다운타임을 최소화할 수 있습니다. 소량 생산이 위탁 생산을 지배하는 가운데, 쉬운 전환과 빠른 프로그래밍으로 인해 스테퍼 솔루션은 시스템 통합업체에게 매력적인 선택이 되고 있습니다.

의료기기의 정밀 모션 제어에 대한 수요 증가

수술용 로봇, 혈액 분석기, 약물전달 펌프는 컴팩트한 설치 공간 내에서 서브마이크론 단위의 정밀도를 요구합니다. 이 사양은 고해상도 인코더와 결합된 현대식 하이브리드 스테퍼 모터가 충족합니다. 설계자는 전원 차단 시에도 기구 위치를 유지하는 재현성 있는 유지 토크를 중시하여 모터를 선정합니다. 이는 환자 안전에 매우 중요한 안전 조치입니다. 조용한 작동은 공진을 가청주파수 대역으로부터 멀어지게 하는 감쇠 알고리즘을 통해 실현되어 병원 소음 기준을 충족합니다. FDA 및 CE 규정은 추적성을 중요시하며, ISO 13485 인증을 획득하고 설계 이력 파일을 검증한 벤더를 우대합니다. 의료 분야의 긴 교체 주기는 부품 공급업체에게 수익 전망이 밝다는 것을 의미합니다.

서보/BLDC 모터와의 성능 비교

단계적인 성능 향상에도 불구하고 스테퍼 스택의 토크는 1,000RPM을 넘어서면 급격히 감소하여 고속 픽앤플레이스 및 컨베이어 드라이브에 적용하는 데 한계가 있습니다. 엔트리 레벨 서보의 가격 하락으로 중정밀 작업에서 스테퍼가 우세했던 기존의 비용 차이가 줄어들었습니다. 통합형 서보 패키지에는 자동 조정 기능과 필드 버스 옵션이 표준으로 장착되어 있어 설치 작업이 간소화되고 총 설치 비용 차이가 줄어듭니다. 따라서 마케팅 담당자는 밸브 구동 및 마이크로플레이트 인덱스와 같이 정적 위치 유지 토크가 동적 요구 사항을 능가하는 사용 사례를 강조합니다.

부문 분석

하이브리드형은 토크 밀도와 1.8도 스텝 분해능의 균형으로 인해 2025년 스테퍼 모터 시장의 54.65%를 차지했습니다. 영구자석형과 가변리액턴스형보다 3.95%의 CAGR로 확대될 것으로 예상됩니다. 이러한 장점은 프레임 크기를 확대하지 않고도 자속 밀도를 높이는 정밀 자기 회로에 대한 지속적인 연구개발 투자로 이어지고 있습니다. 현재 각 업체들은 고충진율 권선을 채택하여 I2R 손실을 줄이고 저전류 동작을 가능하게함으로써 발열량 억제에 따른 베어링 수명 연장을 실현하고 있습니다.

하이브리드 기술의 개선은 IEC 60034-30-1 표준 클래스를 충족하는 데 필요한 에너지 효율 향상도 지원합니다. 네오디뮴 철 붕소 자석 블랭크는 레이저 가공을 통해 조립 후 왜곡을 최소화하여 광학 부품 테스트 단계에 필수적인 마이크로 스텝 선형성을 향상시켰습니다. 영구자석 유닛은 여전히 비용 중심의 자동판매기용으로 채택되고 있으며, 가변 릴럭턴스 설계는 자석의 열화가 우려되는 극한 온도 환경의 펌프 분야에서 틈새 시장을 유지하고 있습니다. 전반적으로 스테퍼 모터 시장은 비용 우위를 잃지 않고 저렴한 서보와의 성능 차이를 메울 수 있는 하이브리드 기술 개선을 중심으로 한 기술 로드맵의 혜택을 누리고 있습니다.

지역별 분석

2025년에도 아시아태평양은 35.74%의 점유율로 매출 1위를 유지했습니다. 이는 자석, 샤프트, 드라이버의 조달을 효율화하는 중국의 부품 생태계가 기반이 되고 있습니다. MOONS'&Electric 등 지역 대기업들은 연간 100만대 이상의 규모 경제를 바탕으로 공격적인 가격 책정으로 세계 수출 채널을 지원하고 있습니다. 일본은 양산과 더불어 특허를 획득한 폐쇄형 루프 펌웨어, 고진공 설계 등의 기술력으로 지역 반도체 장비 수출을 주도하고 있습니다. 한국과 동남아시아는 위탁생산 거점으로 부상하고 있으며, 수입 하이브리드 제품을 프린터 및 로봇 완제품 서브어셈블리에 통합하여 역내 가치사슬을 강화하고 있습니다.

북미는 3.76%의 CAGR이 예상되며, 연방정부의 자동화 갱신 지원책과 국내 반도체 공장 입지에 따른 수혜를 받고 있습니다. 미국의 시스템 통합업체들은 신규 EV 배터리 공장 건설 시 리드타임 단축을 위해 커스텀 서보보다 표준화된 NEMA 표준 프레임을 지정하는 경향이 강해지고 있습니다. 캐나다의 생명과학 및 식품 포장 시설에서 세척에 강한 IP65 사양에 대한 수요가 증가하고 있으며, 멕시코에서는 비용 최적화된 오픈 루프 스테퍼 모터를 사용하여 자동차 하네스 생산 라인을 지원하고 있습니다.

유럽에서는 공장의 폐쇄 루프 개조를 촉진하는 규정 2019/1781 등 에너지 절약 지침으로 인해 꾸준한 성장세를 보이고 있습니다. 독일 OEM 업체는 고진공 사양의 제품을 세계 웨이퍼 가공 장비 시장에 공급하기 위해 현지의 정밀 가공 기술을 활용하고 있습니다. 한편, 중동 및 아프리카의 신흥 경제권에서는 해수 담수화, 섬유 및 포장 프로젝트에 스테퍼 드라이브가 채택되기 시작했지만, 그 수량은 여전히 성숙 지역에 비해 극히 일부에 불과합니다. 전반적으로, 지리적 다양화는 스테퍼 모터 시장을 국부적 인 불황으로부터 보호하고 강력한 다 지역 수요 기반을 뒷받침합니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.10The stepper motor market is expected to grow from USD 2.19 billion in 2025 to USD 2.26 billion in 2026 and is forecast to reach USD 2.67 billion by 2031 at 3.38% CAGR over 2026-2031.

Demand holds steady as manufacturers in robotics, medical devices, and semiconductor equipment continue choosing stepper technology for precise open-loop positioning that avoids the higher system cost of servo platforms. Collaborative robots are gaining traction in assembly cells and are accelerating the adoption of compact NEMA-frame units that deliver predictable torque and simplified programming.Semiconductor capital spending, particularly in packaging and lithography lines, sustains orders for hybrid and linear variants that operate reliably in clean-room environments. Growth also stems from laboratory automation, desktop 3-D printers, and battery-manufacturing lines seeking low-maintenance actuators with tight repeatability. While the overall motion-control sector contracted in 2024 because of inventory corrections, renewed factory-automation investment in 2025 signals a return to steady purchasing cycles.

Global Stepper Motor Market Trends and Insights

Growing adoption of robotics and collaborative automation

Manufacturing plants deploying collaborative robots favor stepper drives because predictable step increments allow intrinsic torque limiting that enhances human-machine safety. U.S. reshoring programs and European productivity upgrades are standardizing on modular motion platforms that accept low-voltage, two-phase hybrids with microstepping controllers. Encoder-equipped closed-loop models are now achieving near-servo smoothness, broadening the feasible working envelope for pick-and-place systems. Ethernet-based protocols integrate the motors into plant networks, enabling condition monitoring that minimizes unplanned downtime. As small-lot production dominates contract manufacturing, easy changeover and fast programming keep stepper solutions attractive for integrators.

Rising demand for precision motion control in medical devices

Surgical robots, hematology analyzers, and drug-delivery pumps require sub-micron accuracy within compact footprints, a specification matched by modern hybrid steppers coupled to high-resolution encoders. Designers select the motors for repeatable holding torque that maintains instrument position even when power is cut, a critical patient-safety safeguard. Quiet operation is delivered by damping algorithms that shift resonance away from audible frequencies, meeting hospital noise norms. FDA and CE rules highlight traceability, favoring vendors with ISO 13485 certificates and validated design-history files. Long replacement cycles in healthcare extend revenue visibility for component suppliers.

Performance limits versus servo / BLDC motors

Despite incremental gains, torque in stepper stacks declines sharply above 1,000 RPM, capping suitability in high-speed pick-and-place or conveyor drives. Price erosion in entry-level servos reduces the historical cost gap that once favored steppers for medium-precision work. Integrated servo packages now include automatic tuning and fieldbus options, simplifying commissioning and reducing the total installed cost delta. Marketers, therefore, emphasize use cases where positional holding torque at standstill outweighs dynamic requirements, such as valve actuation or microplate indexing.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of 3-D printing and desktop manufacturing ecosystems

- Surge in semiconductor packaging-equipment investments

- Integrated smart-actuators cannibalizing discrete motors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid variants commanded 54.65% stepper motor market share in 2025 due to their balance of torque density and 1.8-degree step resolution, and they are forecast to expand at a 3.95% CAGR, outpacing permanent-magnet and variable-reluctance formats. This dominance translates into sustained research and development allocations for finer magnetic circuits that raise flux density without enlarging frame size. Vendors now deploy high-fill-factor windings that shave I2R losses and allow operation at reduced current, extending bearing life through lower heat generation.

Hybrid improvements also underpin energy-efficiency upgrades needed to comply with IEC 60034-30-1 classes. Neodymium-iron-boron magnet blanks are laser-machined to minimize post-assembly skew, improving microstep linearity essential for photonics test stages. Permanent-magnet units still serve cost-sensitive vending machines, while variable-reluctance designs retain niches in extreme-temperature pumps where magnet decay is a concern. Overall, the stepper motor market benefits from a technology roadmap centered on hybrid refinements that close the performance gap with inexpensive servos without surrendering the cost advantage.

The Stepper Motor Market Report is Segmented by Motor Type (Hybrid, Permanent Magnet, and Variable Reluctance), Drive Technique (Open-Loop, and Closed-Loop), Application (Industrial Equipment, Robotics and Cobots, Medical and Laboratory Devices, Computing / 3-D Printing, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remained the 2025 revenue leader with a 35.74% share, anchored by Chinese component ecosystems that streamline magnet, shaft, and driver sourcing. Regional titans such as MOONS' Electric leverage scale economies above 1 million units per year, supporting aggressive pricing that feeds global export channels. Japan complements volume with technology, patented closed-loop firmware, and high-vacuum designs that power the region's semiconductor equipment exports. South Korea and Southeast Asia have emerged as contract-manufacturing hubs that integrate imported hybrids into finished printer and robot sub-assemblies, reinforcing intra-regional value chains.

North America, projected at a 3.76% CAGR, benefits from federal incentives that reimburse automation upgrades and onshore semiconductor fabs. U.S. integrators increasingly specify standardized NEMA frames over custom servos to shorten lead times during green-field EV battery-plant construction. Canadian facilities in life sciences and food packaging drive demand for wash-down IP65 variants, while Mexico supports automotive harness production lines using cost-optimized open-loop steppers.

Europe experiences steady gains under energy-efficiency directives such as Regulation 2019/1781 that push factories toward closed-loop retrofits. German OEMs exploit local precision-machining expertise to supply high-vacuum variants to the global wafer-tool sector. Meanwhile, emerging Middle-East and African economies begin specifying stepper drives in desalination, textile, and packaging projects, though volumes remain a fraction of mature regions. Altogether, geographic diversification shields the stepper motor market from isolated downturns and underscores a resilient multi-regional demand base.

- AMETEK, Inc.

- Anaheim Automation, Inc.

- Arcus Technology Inc.

- Changzhou Fulling Motor Co., Ltd.

- Changzhou Leili Intelligent Drive Systems Co., Ltd.

- ElectroCraft, Inc.

- Faulhaber Group

- JVL Industri Elektronik A/S

- Kollmorgen (Regal Rexnord Corp.)

- Lin Engineering, Inc.

- MinebeaMitsumi Inc.

- MOONS' Electric Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- Nidec Servo Corporation

- Nippon Pulse America, Inc.

- Oriental Motor Co., Ltd.

- Parker-Hannifin Corp.

- Performance Motion Devices, Inc.

- Phytron GmbH

- Schneider Electric SE

- Sanyo Denki Co., Ltd.

- Sonceboz SA

- STMicroelectronics N.V.

- Tamagawa Seiki Co., Ltd.

- Texas Instruments Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of robotics and collaborative automation

- 4.2.2 Rising demand for precision motion control in medical devices

- 4.2.3 Expansion of 3-D printing and desktop manufacturing ecosystems

- 4.2.4 Surge in semiconductor packaging-equipment investments

- 4.2.5 Shift to energy-efficient closed-loop stepper solutions

- 4.2.6 Government incentives for localised motion-component production

- 4.3 Market Restraints

- 4.3.1 Performance limits versus servo / BLDC motors

- 4.3.2 Price pressure from low-cost Asian manufacturers

- 4.3.3 Integrated smart-actuators cannibalising discrete motors

- 4.3.4 Thermal-management challenges in compact designs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Hybrid

- 5.1.2 Permanent Magnet

- 5.1.3 Variable Reluctance

- 5.2 By Drive Technique

- 5.2.1 Open-Loop

- 5.2.2 Closed-Loop

- 5.3 By Application

- 5.3.1 Industrial Equipment

- 5.3.2 Robotics and Cobots

- 5.3.3 Medical and Laboratory Devices

- 5.3.4 Computing / 3-D Printing

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMETEK, Inc.

- 6.4.2 Anaheim Automation, Inc.

- 6.4.3 Arcus Technology Inc.

- 6.4.4 Changzhou Fulling Motor Co., Ltd.

- 6.4.5 Changzhou Leili Intelligent Drive Systems Co., Ltd.

- 6.4.6 ElectroCraft, Inc.

- 6.4.7 Faulhaber Group

- 6.4.8 JVL Industri Elektronik A/S

- 6.4.9 Kollmorgen (Regal Rexnord Corp.)

- 6.4.10 Lin Engineering, Inc.

- 6.4.11 MinebeaMitsumi Inc.

- 6.4.12 MOONS' Electric Co., Ltd.

- 6.4.13 Nanotec Electronic GmbH & Co. KG

- 6.4.14 Nidec Servo Corporation

- 6.4.15 Nippon Pulse America, Inc.

- 6.4.16 Oriental Motor Co., Ltd.

- 6.4.17 Parker-Hannifin Corp.

- 6.4.18 Performance Motion Devices, Inc.

- 6.4.19 Phytron GmbH

- 6.4.20 Schneider Electric SE

- 6.4.21 Sanyo Denki Co., Ltd.

- 6.4.22 Sonceboz SA

- 6.4.23 STMicroelectronics N.V.

- 6.4.24 Tamagawa Seiki Co., Ltd.

- 6.4.25 Texas Instruments Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment