|

시장보고서

상품코드

1940871

아프리카의 데이터센터 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Africa Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

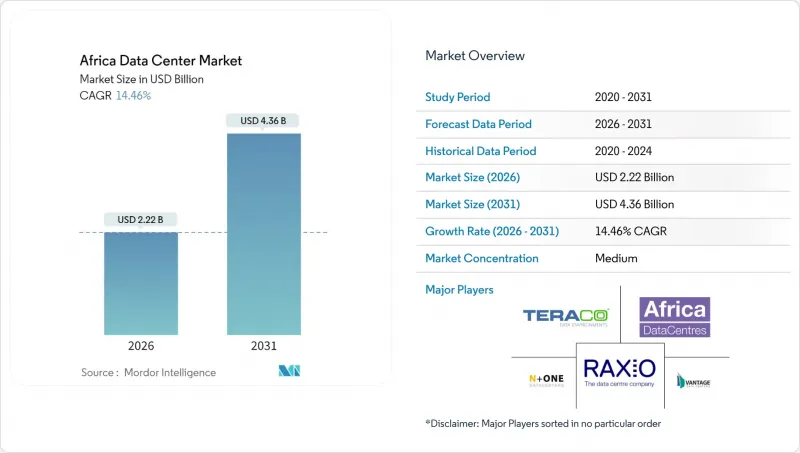

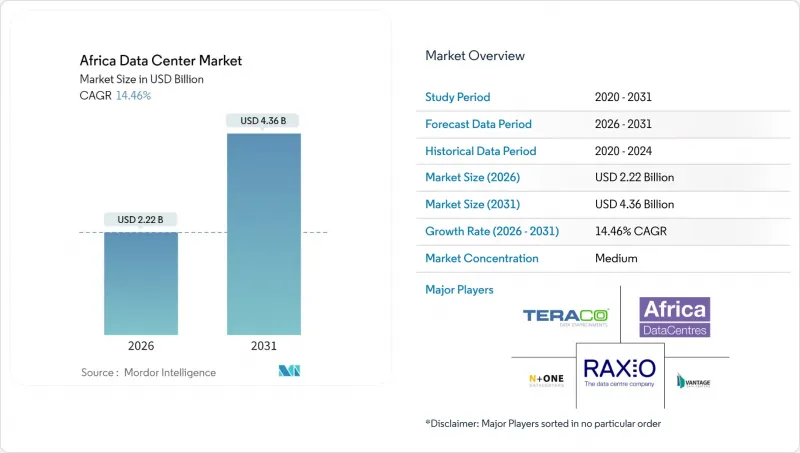

아프리카의 데이터센터 시장은 2025년에 19억 4,000만 달러로 평가되었고, 2026년 22억 2,000만 달러에서 2031년까지 43억 6,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 14.46%로 예상됩니다.

IT 부하 용량 측면에서 시장 규모는 2025년 1,170MW에서 2030년까지 3,460MW로 확대될 것이며, 예측 기간(2025-2030년) 동안 연평균 24.29%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 시장 세분화에서의 점유율 및 추정치는 MW 단위로 계산되어 보고되고 있습니다. 이러한 급격한 성장은 해저 케이블 증설, 5G 구축, 적극적인 데이터 거주 규정, 기업 및 정부의 소버린 호스팅으로의 전략적 전환을 반영하고 있으며, 이 모든 것이 아프리카의 데이터센터 시장의 선도 기업들에게 지연시간 감소와 컴플라이언스 경제성 향상으로 이어집니다. 지연시간 감소와 컴플라이언스 경제성 향상을 가져옵니다. 투자 선순환이 가속화되고 있는 배경에는 과거에는 장벽으로 작용했던 전력망 제약이 재생에너지와 컴플라이언스 전문성을 결합할 수 있는 사업자에게 유리하게 작용하고 있기 때문으로 분석됩니다. 또한, 클라우드 우선 정책, 성장하는 핀테크 생태계, 총소유비용을 절감하는 재생에너지 활용 캠퍼스도 수요를 촉진하고 있습니다. 경쟁은 단순한 상면적이 아닌 에너지 조달, 숙련된 인력, 규제 대응에 초점을 맞추고 있으며, 이로 인해 합병과 제휴가 진행되고, 분산된 현지 용량을 아프리카의 데이터센터 시장 전체에 걸친 지역 간 플랫폼으로 통합하고 있습니다.

아프리카의 데이터센터 시장 동향과 인사이트

급성장하는 클라우드 퍼스트의 디지털 전환

아프리카의 기업 클라우드 지출은 매년 25-30%씩 증가하고 있으며, 저지연 워크로드를 처리하기 위해 국제적인 하이퍼스케일 용량과 현지 코로케이션을 결합해야 할 필요성이 대두되고 있습니다. 나이지리아의 40% 기준 등 최소한의 현지 조달을 의무화하는 정부의 IT 규제는 On-Premise 환경에서 캐리어 중립 시설로의 전환을 가속화하고 있습니다. 금융기관은 거래의 60% 이상을 클라우드 네이티브 코어에서 처리하고 있지만, 오프쇼어 스토리지에 대한 규제 제한으로 인해 컴플라이언스를 충족하는 국내 인프라가 요구되고 있습니다. 이러한 하이브리드화의 필요성은 퍼블릭 클라우드 노드와 기업 케이지가 유럽이나 북미를 경유하는 헤어핀 연결 없이 연결될 수 있는 상호연결성이 뛰어난 데이터센터의 중요성을 높이고 있습니다. 이에 따른 수요 급증은 여러 클라우드 온램프에 다크 파이버를 갖춘 캠퍼스를 갖추고 BFSI 고객이 요구하는 감사받은 데이터 보호 관리를 제공할 수 있는 사업자에게 유리합니다.

정부의 데이터 주권 관련 법규

나이지리아의 '2023년 데이터 보호법', 남아프리카공화국의 '개인정보보호법', 케냐의 '데이터 보호법'은 공동으로 기밀 데이터를 국내 유보를 의무화하고 있습니다. 중요 데이터 관리자로 분류되는 다국적 기업은 개인 기록을 현지에서 처리해야 하며, 위반 시 연간 매출액의 최대 2%의 벌금이 부과되기 때문에 입지 선정 기준이 전력 가격에서 법적 컴플라이언스로 전환되고 있습니다. 금융 규제 당국은 고객의 은행 데이터를 국내에 보관하도록 규정하고 있으며, 이를 통해 Tier 3 및 Tier 4 데이터센터의 최소 가동률을 보장합니다. 국경 간 전송 제한으로 인해 기존의 중앙집중식 아키텍처가 분열되어 클라우드 제공 업체는 여러 아프리카 시장에 여러 구역을 복제해야 합니다. 법적 대응, 사이버 보안, 감사에 대한 전문성과 더불어 강력한 가동률을 보장할 수 있는 사업자는 데이터 거주지의 복잡성 증가에 따라 우선순위 파트너가 될 수 있습니다.

만성적인 전력망 불안정성

남아공 이외의 지역에서는 전력망 신뢰도가 60% 이하로 떨어지기 때문에 디젤 발전 설비를 예비용이 아닌 상시 가동용으로 설계할 수밖에 없습니다. 나이지리아 현장에서는 몇 주간의 정전에 대비하여 디젤 연료를 예산으로 책정하고 있으며, 에너지 비용이 운영 비용의 55-65%(성숙한 시장에서는 35-45%)를 차지합니다. 잦은 발전기 가동 중단은 유지보수 비용과 배출량을 증가시키고, 지속가능성 주장에 의문을 제기하며, 재생에너지가 대중화될 때까지 하이퍼스케일 기업의 진입을 제한하고 있습니다. 남아공의 계획된 정전 일정은 예측 가능하지만, 여전히 전력망과 백업 전원의 1:1 중복성을 요구하고 있으며, 전력 인프라에 대한 자본 지출을 두 배로 늘리고 있습니다. 자체 태양광, 풍력, 지열 자산을 보유한 사업자는 축전지 비용 하락에 따라 구조적인 비용 우위를 확보하고 있습니다.

부문 분석

2025년 기준 대규모 시설은 아프리카의 데이터센터 시장 규모의 30.92%를 차지할 것으로 예상되며, 컴플라이언스 감사 및 상호연결 설계를 효율화하는 통합형 홀에 대한 고객 지향이 두드러집니다. 규모의 경제를 통해 우수한 전력 사용 효율, 장애에 강한 전기 토폴로지, 현장 재생 에너지 통합을 통해 랙당 총 소유비용을 절감할 수 있습니다. 엄격한 데이터 보호 심사에 직면한 기업들은 실사 주기를 단축하기 위해 ISO 27001 준수와 다층적인 물리적 보안을 입증할 수 있는 캠퍼스에서 중요한 워크로드를 호스팅하는 것을 선호합니다. 또한, 인프라 펀드의 자본 조달을 통해 대규모 사업자는 쉘을 사전 정비하고, 주요 테넌트 계약이 체결될 때까지 내부 공사를 지연시켜 아프리카의 데이터센터 시장 수요 급증에 맞추어 가동률을 조정할 수 있습니다.

성장 궤도는 여전히 가파른 성장세를 유지하고 있으며, CAGR 24.12%를 유지하고 있습니다. 이는 요하네스버그, 라고스, 나이로비에 건설 중인 신규 메가와트급 시설이 대규모 홀에 직접 공급되기 때문입니다. 중간 규모의 사이트는 메가 와트 규모의 약속을 수반하지 않는 맞춤형 스위트를 원하는 지역 기업들에게 여전히 매력적입니다. 소규모 사이트는 지방정부의 전자정부 및 지점 업무 워크로드에는 여전히 유효하지만, 가동 시간 및 보안 표준을 강화하는 규제로 인해 업그레이드 압력에 직면하고 있습니다. 주로 남아공의 대규모 및 초대형 건설은 다국적 클라우드 컨텐츠 제공업체의 트래픽을 수용하고 대륙간 상호연결 기반의 착륙지 역할을 할 것입니다.

2025년 기준, 아프리카의 데이터센터 시장의 57.92%는 Tier 3 시설이 차지하고 있으며, 이중화와 자본 집약도 사이에서 실용적인 균형을 이루고 있습니다. 99.982%의 가용성 기준은 BFSI(은행, 금융, 보험), 통신, 정부 조달의 대부분의 요건을 충족시키면서 현지 투자자의 프로젝트 예산 범위 내에서 유지됩니다. 또한 Tier 3 인증은 전력 품질 현실에 부합하며, 많은 아프리카 도시 지역에서는 이중 전력 공급과 다양한 변전소 설치가 현실적이지 않기 때문입니다. 그 결과, 사업자들은 N+1 토폴로지와 모듈형 전원 블록을 도입하여 전력망의 내결함성이 향상되면 Tier 4로 진화할 수 있는 여지를 남겨두고 있습니다.

그러나 티어4의 채택은 24.05%의 연평균 복합 성장률(CAGR)로 가속화되고 있으며, 주로 하이퍼스케일 확장에 의해 주도되고 있습니다. 이를 위해서는 동시 유지보수가 가능한 시스템과 장애에 강한 전력 경로가 필요합니다. 이러한 시설은 지역 클라우드 가용성 영역의 핵심이 되어 저 지연 및 국내 처리가 필요한 핀테크 및 전자상거래 플랫폼을 유치하고 있습니다. Tier 1 및 Tier 2 사이트는 컨텐츠 캐싱 및 재해복구 이용 사례로 살아남고 있지만, 규제 당국의 감시가 강화되고 있으며, 소유자는 추가 중복성을 추가하도록 권장하고 있습니다. 따라서 계층 구성은 아프리카의 디지털 경제가 성숙함에 따라 고객의 기대치가 점차 높아지는 것을 반영하고 있습니다.

아프리카의 데이터센터 시장 보고서는 데이터센터 규모(대규모, 초대형, 중대형, 중형, 메가, 소형), 계층 기준(Tier 1 및 2, Tier 3, Tier 4), 데이터센터 유형(하이퍼스케일/자체 구축, 엔터프라이즈/엣지, 코로케이션), 최종사용자 산업(IT, ITES, E-커머스, 미디어 및 엔터테인먼트 등), 국가(남아프리카 등) 별로 분류됩니다. 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 ITES, E-커머스, 미디어 및 엔터테인먼트 등), 국가(남아공 등) 별로 분류되어 있습니다. 시장 예측은 IT 부하 용량(MW) 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(MW)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.11The Africa Data Center Market was valued at USD 1.94 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 4.36 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031).

In terms of IT load capacity, the market is expected to grow from 1.17 thousand megawatt in 2025 to 3.46 thousand megawatt by 2030, at a CAGR of 24.29% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. The surge reflects a strategic pivot by enterprises and governments toward sovereign hosting, backed by subsea cable additions, 5G rollouts, and assertive data-residency rules, all of which lower latency and improve compliance economics for early movers in the Africa data center market. The investment up-cycle accelerates because grid constraints, once a deterrent, now favor operators that can bundle renewable power and compliance expertise. Demand also benefits from cloud-first mandates, growing fintech ecosystems, and renewable-powered campuses that lower total cost of ownership. Competition centers on energy sourcing, skilled labor, and regulatory navigation rather than sheer floor space, driving mergers and partnerships that consolidate fragmented local capacity into region-spanning platforms across the Africa data center market.

Africa Data Center Market Trends and Insights

Spiralling Cloud-First Digital Transformation

Corporate cloud spending in Africa is growing 25-30% each year, forcing enterprises to blend international hyperscale capacity with local colocation for low-latency workloads. Government IT mandates that stipulate minimum local sourcing, such as Nigeria's 40% threshold, accelerate migrations from on-premise rooms to carrier-neutral facilities. Financial institutions process more than 60% of transactions via cloud-native cores, yet regulatory ceilings on offshore storage require compliant in-country infrastructure. This hybrid imperative elevates interconnection rich data centers that can knit public cloud nodes to enterprise cages without hair-pinning traffic through Europe or North America. The resulting demand spike benefits operators whose campuses incorporate dark fiber to multiple cloud on-ramps and who can offer audited data-protection controls sought by BFSI clients.

Government Data-Sovereignty Legislation

Nigeria's Data Protection Act 2023, South Africa's Protection of Personal Information Act, and Kenya's Data Protection Act collectively obligate sensitive data to remain within national borders. Multinationals categorised as Data Controllers of Major Importance must process personal records locally or risk penalties up to 2% of annual turnover, reshaping site-selection criteria from power price to legal compliance. Financial regulators stipulate that customer banking data reside domestically, guaranteeing a baseline load for Tier 3 and Tier 4 halls. Cross-border transfer restrictions fragment previously centralised architectures, compelling cloud providers to replicate zones across multiple African markets. Operators that can marshal legal, cybersecurity, and audit expertise alongside robust uptime become preferred partners as data-residency complexity deepens.

Chronic Grid Instability

Outside South Africa, grid reliability hovers below 60%, compelling facilities to size diesel plants for continuous rather than standby use. Nigerian sites budget diesel for weeks-long power gaps, elevating energy to 55-65% of operating expense compared with 35-45% in mature markets. Frequent genset cycling escalates maintenance and emissions, challenging sustainability narratives and limiting hyperscale commitment until renewables scale. South Africa's load-shedding schedule, although predictable, still obliges a 1:1 redundancy between grid and backup sources, doubling capital outlay for electrical infrastructure. Operators with captive solar, wind, or geothermal assets gain a structural cost edge as battery storage costs decline.

Other drivers and restraints analyzed in the detailed report include:

- Rapid 5G and National Backbone Fibre Projects

- Rising Subsea Cable Landings

- Limited Skilled Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large facilities commanded 30.92% of the Africa data center market size in 2025, evidencing customer preference for consolidated halls that streamline compliance audits and interconnection design. Economies of scale allow superior power usage efficiency, more fault-tolerant electrical topologies, and onsite renewable integration, lowering per-rack total cost of ownership. Enterprises facing stringent data-protection reviews prefer hosting critical workloads in campuses that can demonstrate ISO 27001 adherence and layered physical security, reducing due-diligence cycles. Moreover, capital availability from infrastructure funds enables large operators to pre-fit shells and delay internal build until anchor tenants sign, keeping utilisation aligned with demand spikes in the Africa data center market.

The growth trajectory remains steep, 24.12% CAGR, because greenfield megawatts under construction in Johannesburg, Lagos, and Nairobi pipeline directly into large-format halls. Medium-sized sites continue to appeal to regional enterprises that desire customised suites without megawatt-scale commitments. Small footprints, though still relevant for municipal e-government and branch office workloads, face upgrade pressure as regulations tighten uptime and security benchmarks. Massive and mega-scale builds, predominantly in South Africa, serve spill-over traffic from multinational cloud and content providers and act as landing pads for cross-continent interconnection fabrics.

Tier 3 halls made up 57.92% of the Africa data center market size in 2025, striking a pragmatic balance between redundancy and capital intensity. The 99.982% availability threshold satisfies most BFSI, telecom, and government procurement checklists while keeping project budgets within reach for local investors. Tier 3 certification also aligns with power-quality realities, as dual utility feeds or diverse substations remain impractical in many African metros. As a result, operators deploy N+1 topologies with modular power blocks that can evolve toward Tier 4 if grid resilience improves.

Tier 4 adoption is nevertheless accelerating at 24.05% CAGR, predominantly through hyperscale expansions that require concurrently maintainable systems and fault-tolerant electrical paths. Such facilities anchor regional cloud availability zones, attracting fintech and e-commerce platforms that need low-latency, in-country processing. Tier 1 and Tier 2 sites persist for content caching and disaster-recovery use cases but increasingly attract scrutiny from regulators, nudging owners to retrofit additional redundancy. The tier mix therefore mirrors a gradual up-shift in customer expectations as African digital economies mature.

The Africa Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Standard (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), End User Industry (BFSI, IT and ITES, E-Commerce, Media and Entertainment, and More), and Country (South Africa and More). The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Teraco Data Environments Proprietary Limited

- Medallion Communications Limited

- Africa Data Centers

- Paratus Group Holdings Limited

- Vantage Data Centers LLC

- Telecom Egypt

- Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- N+ONE Data Centers

- Open Access Data Centres Limited

- ONIX Data Centre Limited

- Icolo Data Centres Kenya Limited

- Interxion Holding N.V. (a Digital Realty company)

- Wana Corporate S.A. (INWI Business)

- Raxio Data Centre Holdings Pte. Ltd.

- MainOne Cable Company Limited (an Equinix company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of 5G and national backbone fibre projects

- 4.2.2 Spiralling cloud-first digital transformation among African enterprises

- 4.2.3 Rising subsea cable landings boosting international bandwidth supply

- 4.2.4 Government data-sovereignty legislation driving in-country hosting

- 4.2.5 Surging venture capital and infrastructure fund inflows into African data centers

- 4.2.6 Emergence of green hydrogen and renewable-powered campuses

- 4.3 Market Restraints

- 4.3.1 Chronic grid instability and reliance on diesel generators

- 4.3.2 Limited domestic skilled workforce for critical facility operations

- 4.3.3 High import tariffs and logistics costs for mission-critical equipment

- 4.3.4 Political and security risks in key growth corridors

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 South Africa

- 4.5.6.2 Israel

- 4.5.6.3 Nigeria

- 4.5.6.4 Rest of Africa

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MW)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Standard

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Israel

- 5.5.3 Nigeria

- 5.5.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Teraco Data Environments Proprietary Limited

- 6.4.2 Medallion Communications Limited

- 6.4.3 Africa Data Centers

- 6.4.4 Paratus Group Holdings Limited

- 6.4.5 Vantage Data Centers LLC

- 6.4.6 Telecom Egypt

- 6.4.7 Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- 6.4.8 N+ONE Data Centers

- 6.4.9 Open Access Data Centres Limited

- 6.4.10 ONIX Data Centre Limited

- 6.4.11 Icolo Data Centres Kenya Limited

- 6.4.12 Interxion Holding N.V. (a Digital Realty company)

- 6.4.13 Wana Corporate S.A. (INWI Business)

- 6.4.14 Raxio Data Centre Holdings Pte. Ltd.

- 6.4.15 MainOne Cable Company Limited (an Equinix company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment