|

시장보고서

상품코드

1940909

미국의 지붕 공사 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

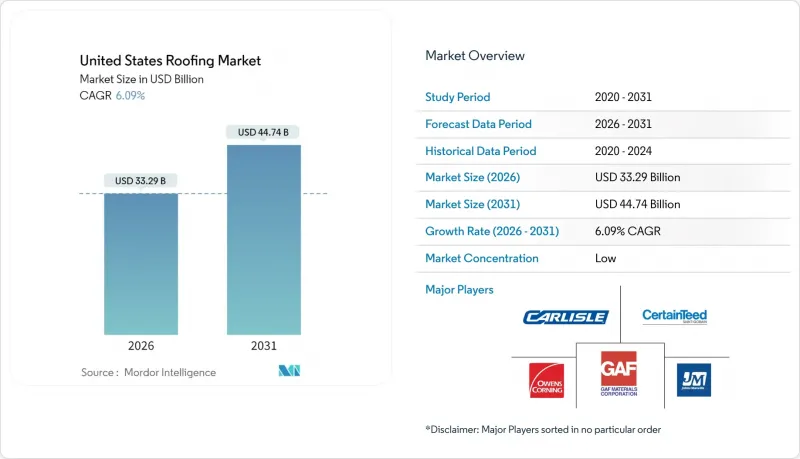

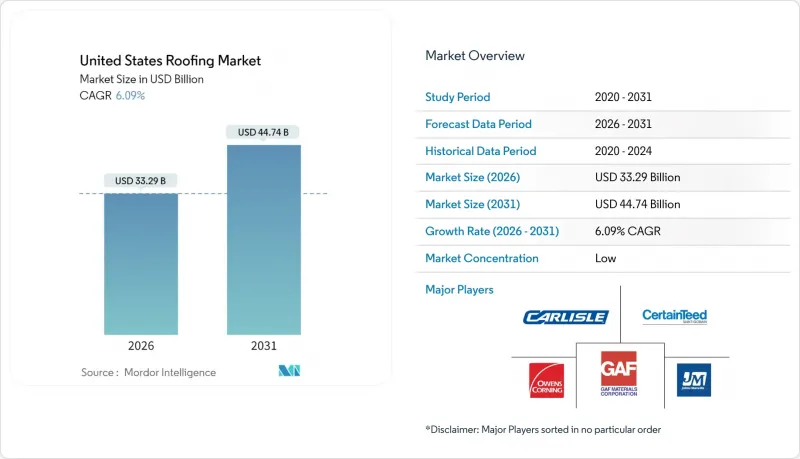

미국 지붕 시장은 2026년 시장 규모가 332억 9,000만 달러로 추정되며, 2025년 313억 8,000만 달러에서 성장이 전망됩니다.

2031년까지의 예측에서는 447억 4,000만 달러에 달하며, 2026-2031년에 CAGR 6.09%로 확대할 전망입니다.

국내 주택 재고의 노후화, 심각한 기상현상의 빈번한 발생, 연방정부의 에너지 절약 대책에 따른 인센티브가 이러한 꾸준한 확장을 지원하고 있습니다. 지붕 교체 공사는 연간 설치량의 5분의 4 이상을 차지하고 있으며, 신축 건설이 둔화되더라도 업계는 예측 가능한 수요 기반을 확보할 수 있습니다. 상업 프로젝트에서는 멤브레인 기술이 현대 건축 기준의 에너지 성능 요구 사항을 충족시키기 때문에 평평한 지붕과 낮은 경사 지붕 시스템이 주류입니다. 한편, 내구성과 태양광발전이 가능한 표면을 원하는 소유자 수요로 인해 금속 및 TPO 제품이 다른 소재를 능가하는 성장세를 보이고 있습니다. 홈디포와 QXO가 수십억 달러 규모의 거래를 주도하는 유통 통합은 공급망에 인공지능 툴을 도입하여 대규모 플랫폼이 계약업체에 신속한 배송과 맞춤형 상품을 제공할 수 있는 토대를 마련하고 있습니다.

미국 지붕재 시장 동향 및 분석

주택 재고의 지붕 개보수 주기가 지속적인 수요를 주도

연간 지붕 수요의 80% 이상이 지붕 교체 공사로 인한 것이며, 미국 주택의 평균 건축 연한은 40년에 육박하고 있습니다. 강풍에 대한 노출이 증가하면 아스팔트 슁글재의 열화가 가속화되며, 실지 조사에서 내구연한 10년 만에 고장이 발생한 사례도 확인되었습니다. 북동부 및 중서부 지역에는 전후 건설된 주택이 집중되어 있으며, 현재 이들 주택이 동시에 개보수 시기를 맞이하고 있으며, 경기 변동에 관계없이 계약자에게는 안정적인 수주량을 기대할 수 있습니다. 주택담보대출 금리가 하락하면 이 사이클은 더욱 활성화되고, 소유자는 자산 가치를 리노베이션 예산으로 사용할 수 있게 됩니다. 드론을 통한 상태 평가는 점검 시간을 단축하고, 객관적인 데이터세트를 생성하여 보험금 청구를 신속하게 처리하고, 프로젝트 파이프라인을 더욱 원활하게 합니다.

기후 변화에 따른 태풍 피해 복구가 시장 역학 재조합

2024년 미국의 지붕 관련 보험 청구액은 300억 달러를 넘어섰습니다. 대류성 폭풍으로 인한 재산 피해는 570억 달러에 달하고, 전년 대비 거의 두 배에 달했습니다. 텍사스, 콜로라도 및 인접한 토네이도 얼라이언스 지역의 주에서 발생하는 사건의 비율이 증가하고 있으며, 비재난 등급의 풍수해 및 우박 피해 청구는 2022년 17%에서 2024년 25%로 상승할 것으로 예측됩니다. 이러한 반복되는 재해로 인해 지붕 교체 주기가 단축되고, 가뜩이나 어려운 노동 시장에 수요가 급증하게 됩니다. 보험사들은 현재 15-20년 이상된 지붕의 보상금액을 줄이고, 4등급 내충격 기준의 시스템에 대해 보험료 할인을 제공함으로써 고객을 고가의 금속이나 합성소재 제품으로 유도하고 있습니다.

숙련된 인력 부족으로 성장 잠재력 제약

건설 업계는 2025년까지 50만1천명의 추가 인력이 필요하지만, 루퍼 5명 중 1명은 이미 55세 이상입니다. 열악한 현장 환경이 다른 직종에 비해 높은 이직률을 초래하고, NRCA(전미 지붕공사업협회)의 TRAC 커리큘럼 확대와 크렘슨대학의 100만 달러 규모의 '지붕산업센터' 설립에도 불구하고 견습생 수료자가 수요를 따라잡지 못하고 있습니다. 노동력 부족은 건설 비용 상승, 프로젝트 지연, 그리고 건설업체가 태풍 피해 지역으로 진출할 수 있는 속도 제한으로 이어지고 있습니다. 사모펀드 지원 플랫폼은 적극적으로 인재를 모집하고 있지만, 소규모 업체는 임금과 복리후생 측면에서 경쟁력이 부족해 능력 격차가 확대되고 있습니다.

부문 분석

주거용 용도는 2025년 미국 지붕 시장 매출의 59.12%를 차지할 것으로 예상되며, 노후화된 주택과 폭풍우로 인한 교체 수요가 겹치면서 2031년까지 연평균 복합 성장률(CAGR) 7.18%를 나타낼 것으로 전망됩니다. 예측 가능한 갱신 주기는 시산업체에게 안정적인 기반을 제공하는 한편, 섹션 25C 세액공제는 소유주에게 에너지 절약형 지붕재와 금속 패널로 업그레이드하도록 유도하여 자산 가치 향상에 기여합니다. 보험사는 내충격 시스템을 장려하여 교체 주기를 더욱 단축하고 있습니다.

상업적 수요는 기업의 넷제로 목표와 E-Commerce 확대에 따른 창고 건설 붐으로 인해 탄력을 받고 있습니다. 태양광 대응 표면을 갖춘 저경사 타포린은 운영비 절감을 원하는 시설 관리자의 관심을 끌고 있으며, 연방 인프라 자금은 학교, 교통 거점 및 공공시설에 투입되고 있습니다. 주택 시장이 여전히 미국 지붕재 시장의 근간을 이루고 있는 가운데, 대형 전국 건설업체들은 지역별 단독주택 수요 변동을 헤지하기 위해 다양한 상업용 프로젝트를 통해 사업 포트폴리오의 균형 조정을 강화하고 있습니다.

2025년 현재 미국 지붕 시장 규모의 81.65%는 개보수 공사가 차지하고 있으며, 이는 성숙한 건축 재고와 잦은 폭풍우 피해에 대한 보험금 지급을 반영하고 있습니다. 드론 영상, AI를 통한 상태 평가, 효율화된 보험 포털을 통해 보험금 청구 주기가 단축되고, 기상재해 발생 후 지붕 철거가 빨라지고 있습니다. 따라서 시산업체는 지붕 교체 공사를 전문으로 하는 즉시 대응팀에 인력과 자재를 집중 배치하고 있습니다.

신규 설치는 점유율은 작지만, 선벨트 지역의 주택 착공 증가와 데이터센터 건설이 지방 도시를 휩쓸면서 CAGR 7.52%의 성장이 예상됩니다. 현대의 건축 기준은 반사재와 내화재를 의무적으로 사용하도록 하고 있으며, 이는 단가 상승의 한 요인이 되고 있습니다. 건설사와 유통업체가 협력하여 현장의 자재 보관 체계가 정비되고, 도난이나 날씨 지연을 최소화할 수 있으며, 인력난이 지속되는 상황에서도 도입이 진행되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액, 단위 : 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06United States Roofing Market market size in 2026 is estimated at USD 33.29 billion, growing from 2025 value of USD 31.38 billion with 2031 projections showing USD 44.74 billion, growing at 6.09% CAGR over 2026-2031.

Renewals triggered by the nation's aging housing stock, the growing frequency of severe weather events, and federal energy-efficiency incentives underpin this steady expansion. Re-roofing activities account for more than four-fifths of annual installation volume, giving the industry a predictable demand foundation even when new construction moderates. Flat and low-slope systems dominate commercial projects because their membrane technologies satisfy modern building-code requirements for energy performance, while metal and TPO products outpace other materials as owners seek durability and solar-ready surfaces. Distribution consolidation, led by Home Depot's and QXO's multibillion-dollar deals, ushers artificial-intelligence tools into supply chains and positions large platforms to offer contractors faster deliveries and tailored assortments.

United States Roofing Market Trends and Insights

Housing-Stock Re-Roofing Cycle Drives Sustained Demand

More than four-fifths of annual roofing demand comes from re-roofing, and the median U.S. home age is nearing 40 years. Elevated wind exposure accelerates asphalt-shingle degradation, with field studies showing failures as early as 10 years into service life. Concentrated cohorts of post-war homes in the Northeast and Midwest are now simultaneously entering their renewal windows, giving contractors consistent volume regardless of macroeconomic swings. The cycle intensifies when mortgage rates dip, allowing owners to convert equity into upgrade budgets. Drone-based condition assessments shorten inspection times and create objective datasets that speed insurance claims, further smoothing project pipelines.

Climate-Driven Storm Repairs Reshape Market Dynamics

U.S. roof-related claims exceeded USD 30 billion in 2024 as convective storms produced USD 57 billion in property damage, almost double the prior year. Texas, Colorado, and adjacent Tornado Alley states account for a rising share of events, with non-catastrophic wind and hail claims climbing from 17% in 2022 to 25% in 2024. This recurring hazard compresses replacement cycles and pushes demand spikes into already tight labor markets. Insurers now depreciate coverage for roofs older than 15-20 years and offer premium credits for Class 4 impact-rated systems, nudging customers toward higher-cost metal and synthetic products.

Skilled-Labor Shortages Constrain Growth Potential

The construction sector needs 501,000 more workers in 2025, yet 1 in 5 roofers is already over 55 years old. Harsh job-site conditions drive higher turnover than in other trades, and apprenticeship completions lag demand despite NRCA's expanded TRAC curriculum and Clemson's USD 1 million Roofing Industry Center commitment. Labor shortfalls inflate installation costs, extend project backlogs, and limit the pace at which contractors can scale into storm-damaged regions. Private equity-backed platforms recruit aggressively, but smaller shops struggle to match wage offers and benefit packages, widening capacity gaps.

Other drivers and restraints analyzed in the detailed report include:

- Federal Energy Efficiency Incentives Accelerate Premium Adoption

- Retail Distribution Consolidation Transforms Market Access

- Material Price Volatility Pressures Margin Stability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential applications generated 59.12% of 2025 revenue for the United States roofing market and are on track for a 7.18% CAGR through 2031 as aging homes collide with storm-driven replacements. Predictable renewal cycles give installers steady baselines, while Section 25C credits persuade owners to upgrade to energy-efficient shingles or metal panels that boost property values. Insurers incentivize impact-rated systems, compressing replacement timelines even further.

Commercial demand gains momentum from corporate net-zero commitments and an e-commerce-fueled warehouse boom. Low-slope membranes with solar-ready surfaces attract facility managers seeking lower operating costs, and federal infrastructure funding channels work to schools, transit centers, and public offices. Although residential still anchors the United States roofing market, large national contractors increasingly balance their portfolios with diversified commercial projects to hedge regional single-family swings.

Replacement undertakings represented 81.65% of the United States roofing market size in 2025, reflecting a mature building inventory and frequent storm damage settlements. Drone imagery, AI-assisted condition scoring, and streamlined insurance portals shorten claim cycles, driving faster roof tear-offs once weather events hit. Contractors, therefore, allocate personnel and inventory toward ready-response teams that specialize in reroof projects.

New installations account for a smaller share yet are forecast to grow 7.52% CAGR as migration pushes housing starts in the Sun Belt and data-center builds sweep secondary metros. Modern codes mandate reflective or fire-rated coverings, often elevating unit costs. Partnerships between builders and distributors enable job-site staging that minimizes theft and weather delays, reinforcing adoption even when labor remains tight.

The United States Roofing Market Report is Segmented by Sector (Residential, Commercial, Infrastructure), by Installation Type (New Installation, Replacement/Renovation), by Roofing Type (Slope Roof, Flat/Low-Slope Roof), by Material Type (Modified Bitumen, EPDM Rubber, TPO, PVC Membrane, and More), and by Geography (Northeast, Midwest, Southeast, West, Southwest). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- GAF Materials Corporation

- Owens Corning

- CertainTeed (Saint-Gobain)

- Carlisle Companies Inc.

- Johns Manville (Berkshire Hathaway)

- IKO Industries

- TAMKO Building Products

- Atlas Roofing Corporation

- Beacon Building Products

- ABC Supply Co.

- Holcim Elevate (Firestone Building Products)

- Duro-Last Inc.

- Malarkey Roofing Products

- CentiMark Corporation

- Tecta America

- Flynn Group

- Baker Roofing Company

- IronHead Roofing

- Sika Sarnafil

- MFM Building Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Housing-stock re-roofing cycle (>=80 % of demand)

- 4.2.2 Climate-driven storm repairs & insurance spend

- 4.2.3 Federal/State energy-efficiency incentives (IRA tax credits, Title 24)

- 4.2.4 Retail giant entry into specialty distribution (Home Depot-SRS deal)

- 4.2.5 AI-enabled aerial data pricing/claims (Verisk, EagleView)

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortages elevating installation costs

- 4.3.2 Volatility in asphalt & polymer feedstock prices

- 4.3.3 Proliferation of counterfeit/sub-spec materials

- 4.3.4 Insurance tightening: higher deductibles & roof-age exclusions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.2.1 Offices and Retail

- 5.1.2.2 Industrial and Logistics

- 5.1.2.3 Others

- 5.1.3 Infrastructure

- 5.2 By Installation Type

- 5.2.1 New Installation

- 5.2.2 Replacement / Renovation (Re-Roofing)

- 5.3 By Roofing Type

- 5.3.1 Slope Roof

- 5.3.2 Flat / Low-Slope Roof

- 5.4 By Material Type

- 5.4.1 Modified Bitumen

- 5.4.2 EPDM Rubber

- 5.4.3 Thermoplastic Polyolefin

- 5.4.4 PVC Membrane

- 5.4.5 Metals

- 5.4.6 Tiles

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 Southeast

- 5.5.4 West

- 5.5.5 Southwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 GAF Materials Corporation

- 6.4.2 Owens Corning

- 6.4.3 CertainTeed (Saint-Gobain)

- 6.4.4 Carlisle Companies Inc.

- 6.4.5 Johns Manville (Berkshire Hathaway)

- 6.4.6 IKO Industries

- 6.4.7 TAMKO Building Products

- 6.4.8 Atlas Roofing Corporation

- 6.4.9 Beacon Building Products

- 6.4.10 ABC Supply Co.

- 6.4.11 Holcim Elevate (Firestone Building Products)

- 6.4.12 Duro-Last Inc.

- 6.4.13 Malarkey Roofing Products

- 6.4.14 CentiMark Corporation

- 6.4.15 Tecta America

- 6.4.16 Flynn Group

- 6.4.17 Baker Roofing Company

- 6.4.18 IronHead Roofing

- 6.4.19 Sika Sarnafil

- 6.4.20 MFM Building Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment