|

시장보고서

상품코드

2034975

반도체 웨이퍼 연마 및 연삭 장비 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Semiconductor Wafer Polishing And Grinding Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

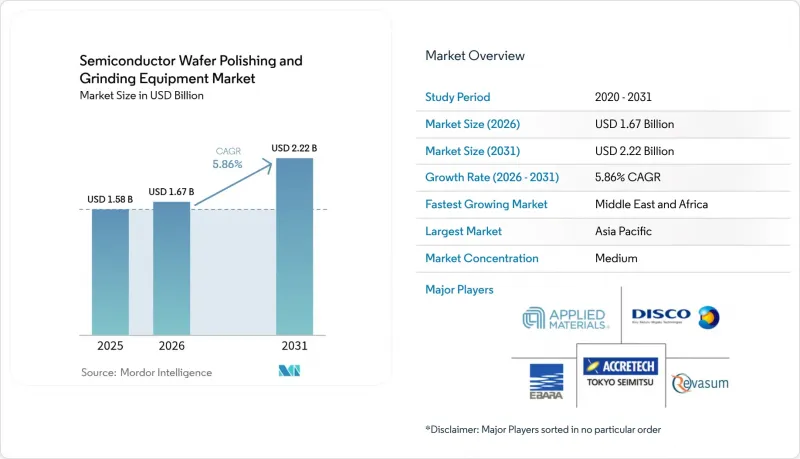

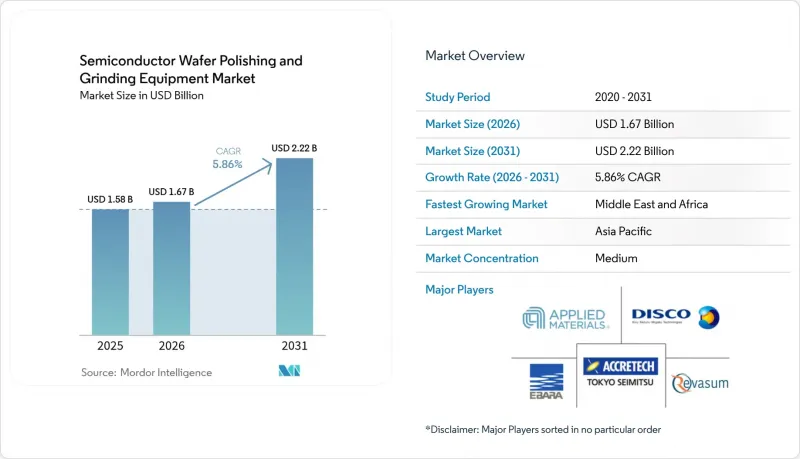

반도체 웨이퍼 연마 및 연삭 장비 시장 규모는 2025년 15억 8,000만 달러에서 2026년에는 16억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.86%로 성장을 지속하여, 2031년에는 22억 2,000만 달러에 이를 것으로 예측됩니다.

이 기간 동안 대형 웨이퍼, 와이드 밴드갭 재료 및 자동화 툴에 대한 설비투자가 정밀 재료 제거 시스템 주문량을 지속적으로 증가시켰습니다. 장비 공급업체는 원자 수준의 공차를 관리하기 위해 실시간 공정 제어 기능을 확장하는 한편, AI를 활용한 진단 기능을 통해 기술자 부족을 보완하고 수율을 향상시켰습니다. 수출관리 규제로 인해 조달 전략을 재검토하고 북미와 유럽에 대한 병행 투자를 촉진한 결과, 아시아에 대한 과도한 의존도를 줄이고 지역별 서비스 체제를 강화했습니다. 또한, 지속가능성 관련 규제 또한 장비 선택에 영향을 미쳐 슬러리를 사용하지 않는 CMP 패드와 소모품이 적은 연삭 기술로의 전환을 가속화했습니다.

세계 반도체 웨이퍼 연마 및 연삭 장비 시장 동향과 인사이트

아시아에서 첨단 노드 칩을 탑재한 가전제품 소비 확대

중국, 인도, 동남아시아 전역에서 플래그십 스마트폰과 AI 기반 웨어러블 기기의 급속한 보급으로 원자 단위의 매끄러운 웨이퍼 표면과 10억분의 1 단위로 측정되는 결함 밀도를 요구하는 3nm 이하 디바이스에 대한 수요가 가속화되고 있습니다. 현지 파운더리는 수출 허가의 불확실성에도 불구하고 CMP 및 미세 연삭의 생산 능력을 확대하는 한편, 장비 제조업체는 평탄도를 손상시키지 않고 엄격한 환경 기준을 충족하는 무염소 패드를 도입했습니다. 멀티코어 SoC의 보급과 함께 다양한 재료 스택의 공정 균일성이 중요해지면서 이종 레이어에 특화된 적응형 제어 CMP 시스템에 대한 투자가 촉진되었습니다.

300mm 및 450mm CMP 장비에 대한 수요를 주도하는 미세화 추세

비용 효율적인 다이 밀도 추구로 인해 300mm가 주류 포맷으로 자리 잡았지만, 더 큰 블랭크에서 2.25배의 다이 면적을 얻을 수 있기 때문에 450mm의 시험적 개발이 다시 등장했습니다. 공구 제조업체들은 플래튼을 강화하고, 슬러리 분포를 최적화하고, 인사이트 측정 기능을 통합하여 더 넓은 표면에서 나노미터 수준의 제거 균일성을 유지하면서 스케일업이라는 과제를 해결해 왔습니다. TSMC의 510mmX515mm 직사각형 기판 프로토타입은 기존 툴 아키텍처를 전면적으로 재검토하지 않고도 사용 가능한 면적을 3배로 늘릴 수 있는 또 다른 길을 제시했습니다.

300mm 장비의 높은 설비 투자 비용과 긴 ROI 주기

2024년 기준 300mm CMP 플랫폼 1대당 가격은 300만-500만 달러에 달했고, 설비 업그레이드에 100만-200만 달러가 추가되기 때문에 생산량이 적은 팹의 경우 투자회수 기간이 4년 이상 소요됩니다. 중소규모의 제조업체는 확장을 연기하고 리퍼브 및 공유 용량 모델을 선택했기 때문에 규모 확대에 따른 다이당 비용 측면에서 명백한 이점이 있음에도 불구하고 전체 장비 도입이 둔화되었습니다.

부문 분석

CMP 장비는 2025년 매출의 55.92%를 차지했으며, 0.1nm 미만의 제거 정밀도가 요구되는 첨단 노드의 평탄도 목표를 달성하는 데 있어 여전히 핵심적인 역할을 하고 있습니다. 반도체 웨이퍼 연마 및 연삭 장비 시장은 팹이 3nm 이하 수율 향상을 위해 연마제 없는 슬러리 및 AI를 활용한 엔드포인트 검출을 채택하면서 수혜를 입었습니다. 연삭 및 연마 일체형 플랫폼은 웨이퍼 이송 횟수를 줄이고, 파티클 리스크를 줄이며, 대기 시간을 단축시켰습니다.

고객이 공정 공정을 통합하여 클린룸 공간을 확보함에 따라 통합 시스템의 CAGR은 2031년까지 7.55%로 단일 그라인더를 능가하는 7.55%를 나타낼 것으로 예측됩니다. 각 벤더들은 폐쇄 루프 온도 제어, 예지보전, 소모품 수명 분석 기능을 번들로 제공하여 다품종 생산에서 OEE(종합 설비 가동률)를 향상시켰습니다. 다이아몬드 및 기타 초경질 기판에 대응하는 새로운 래핑 및 슬라이싱 툴은 반도체 웨이퍼 연마 및 연삭 장비 시장의 범위를 틈새 광전자 및 양자 소자 분야로 확장했습니다.

2025년 시장 수익의 61.88%를 300mm 노드가 차지할 것으로 예상됐으며, 이는 수십 년에 걸친 공정 성숙도, 최적화된 소모품, 그리고 충분히 상각된 팹 자산이 그 배경이 됩니다. CMP 패드의 텍스처와 백그라인딩 휠의 형상을 지속적으로 개선하여 처리량을 더욱 향상시킴으로써 반도체 웨이퍼 연마 및 연삭 장비 시장에서 이 부문의 경제적 우위를 더욱 강화했습니다.

반면, 450mm 이상 카테고리는 웨이퍼 당 다이 수를 3배로 늘릴 수 있는 직사각형 포맷을 모색하는 파일럿 라인에 힘입어 10.84%의 가장 높은 CAGR을 기록했습니다. 각 장비 업체들은 확대된 플래튼, 로봇 핸들러 및 여러 직경에 대응 가능한 대용량 슬러리 공급 시스템의 프로토타입을 개발하여 반도체 웨이퍼 연마 및 연삭 장비 업계가 대규모 ROI 평가를 진행하고 있는 가운데, 2028년 이후 대량 도입을 목표로 체제를 정비하고 있습니다.

반도체 웨이퍼 연마 및 연삭 장비 시장은 장비 유형(웨이퍼 연삭기 등), 웨이퍼 크기(150mm 이하, 200mm, 300mm, 450mm 이상), 기술(백그라인딩 등), 반도체 유형(메모리, 로직 및 SoC 등), 최종 사용자(반도체 제조업체 등), 그리고 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)으로 분류됩니다.

지역별 분석

2025년 아시아태평양은 세계 전체 매출의 67.94%를 차지할 것으로 예상됐으며, 대만, 한국, 일본, 중국, 일본, 중국이 견인차 역할을 할 것입니다. 이들 지역에서는 집적 디바이스 로드맵과 파운드리의 확장이 장비 조달을 지원했습니다. TSMC의 무염소 패드 도입과 일본의 보조금 지원으로 인한 팹 클러스터 형성은 친환경 장비에 대한 지역적 선호를 강화했습니다. 수출 관리의 불확실성으로 인해 중국 팹은 현지 공급업체에 대한 의존도가 높아졌지만, 라이선스 예외 조치를 통해 하이엔드 CMP 장비의 수입은 지속되어 반도체 웨이퍼 연마 및 연삭 장비 시장 수요는 견고하게 유지되었습니다.

북미에서는 2022년 'CHIPS and Science Act'를 계기로 투자가 회복세를 보이고 있습니다. 이 법은 520억 달러의 인센티브를 동원하여 2025년까지 총 4,500억 달러에 육박하는 90개 이상의 팹 건설을 발표하도록 유도했습니다. 생산능력 증설로 장비 수주는 증가했지만, 2030년까지 6만 7,000명에 달할 것으로 예상되는 기술자 부족으로 인해 자동화의 우선순위를 높이고 인재 파이프라인을 가속화하기 위해 학술 컨소시엄과의 제휴를 추진했습니다.

유럽에서는 2030년까지 세계 생산 점유율 20%를 목표로 하는 430억 유로(498억 3,000만 달러) 규모의 '칩스법'이 그 뒤를 이었습니다. 독일의 정밀 엔지니어링 기업, 프랑스의 첨단 패키징 기지, 북유럽의 재료 과학 연구소는 에너지 회수 펌프와 물 재활용 루프를 갖춘 CMP 시스템을 요구하여 EU 그린딜의 목표와 조달을 일치시키고 차별화된 반도체 웨이퍼 연마 및 연삭 장비 시장 솔루션을 촉진했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The semiconductor wafer polishing and grinding equipment market size is expected to grow from USD 1.58 billion in 2025 to USD 1.67 billion in 2026 and is forecast to reach USD 2.22 billion by 2031 at 5.86% CAGR over 2026-2031.

During the period, capital spending on larger wafers, wide-bandgap materials, and automation tools has driven sustained order volumes for precision material-removal systems. Equipment suppliers scaled real-time process-control features to manage atomic-level tolerances, while AI-enabled diagnostics offset technician shortages and improved yield. Export-control rules reshaped sourcing strategies, prompting parallel investments in North America and Europe that reduced over-reliance on Asia and strengthened regional service footprints. Sustainability mandates also influenced tool selection, accelerating the shift toward slurry-free CMP pads and low-consumable grinding technologies.

Global Semiconductor Wafer Polishing And Grinding Equipment Market Trends and Insights

Growing consumption of consumer electronics with advanced-node chips in Asia

Rapid uptake of flagship smartphones and AI-enabled wearables across China, India, and Southeast Asia accelerated demand for sub-3 nm devices that require atomically smooth wafer surfaces and defect densities measured in parts per billion. Local foundries expanded CMP and fine-grinding capacity despite export-license uncertainty, while tool makers introduced chlorine-free pads that met strict environmental codes without compromising planarity. As multi-core SoCs proliferated, process uniformity across diverse material stacks became critical, spurring investment in adaptive-control CMP systems tailored for heterogeneous layers.

Miniaturization push driving demand for 300 mm and 450 mm CMP tools

The search for cost-effective die density sustained 300 mm as the mainstream format, yet exploratory 450 mm development resurfaced because a larger blank yields 2.25 times more die area. Tool makers tackled the scale-up challenge by reinforcing platens, optimizing slurry distribution, and embedding in-situ metrology to maintain nanometer-level removal uniformity across wider surfaces. TSMC's prototype 510 mm X 515 mm rectangular substrate hinted at an alternate path that could triple usable area without fully overhauling legacy tool architectures.

High capital cost and long ROI cycle for 300 mm tools

A single 300 mm CMP platform carried a USD 3-5 million price tag in 2024, with facility upgrades adding USD 1-2 million, stretching payback beyond 4 years in lower-volume fabs. Smaller players delayed expansion and opted for refurbished or shared-capacity models, slowing overall tool uptake despite clear cost-per-die advantages at scale.

Other drivers and restraints analyzed in the detailed report include:

- Foundry capacity investments in the U.S. and Europe under the CHIPS Act

- Transition to SiC/GaN power devices requires ultra-precision grinding

- Export controls and IP barriers limiting shipments to China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CMP tools generated 55.92% of 2025 revenue and remained central to advanced-node planarity targets that mandate removal accuracy below 0.1 nm. The semiconductor wafer polishing and grinding equipment market benefited as fabs adopted abrasive-free slurries and AI-assisted endpoint detection to push sub-3 nm yields upward. Integrated grinder-polisher platforms reduced wafer transfers, trimming particle risks, and cutting queue time.

Integrated systems' 7.55% CAGR through 2031 outpaced standalone grinders as customers consolidated process steps to free cleanroom space. Vendors bundled closed-loop temperature control, predictive maintenance, and consumable-life analytics, enhancing OEE for high-mix production. Emerging lapping and slicing tools addressed diamond and other ultra-hard substrates, extending the semiconductor wafer polishing and grinding equipment market reach into niche photonics and quantum-device lines.

The 300 mm node held 61.88% of 2025 market revenue, underlining decades of process maturity, optimized consumables, and well-depreciated fab assets. Continuous enhancements in CMP pad texture and back-grinding wheel geometry further raised throughput, reinforcing the segment's economic moat within the semiconductor wafer polishing and grinding equipment market.

Conversely, the 450 mm and above category registered the fastest 10.84% CAGR, driven by pilot lines exploring rectangular formats that promise 3X more die per wafer. Equipment makers prototyped enlarged platens, robotic handlers, and high-capacity slurry-delivery systems adaptable to multiple diameters, positioning themselves for potential mass adoption beyond 2028 as the semiconductor wafer polishing and grinding equipment industry evaluates ROI at scale.

Semiconductor Wafer Polishing and Grinding Equipment Market is Segmented by Equipment Type (Wafer Grinding Machines, and More), Wafer Size (<=150 Mm, 200 Mm, 300 Mm, and 450 Mm and Above), Technology (Back-Grinding, and More), Semiconductor Type (Memory, Logic and SoC, and More), End-User (Integrated Device Manufacturers, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific retained 67.94% of global revenue in 2025, anchored by Taiwan, South Korea, Japan, and China, where integrated device roadmaps and foundry expansions sustained tool procurements. TSMC's chlorine-free pad rollout and Japan's subsidy-backed fab clusters reinforced a regional preference for environmentally optimized equipment. Export-control uncertainties nudged Chinese fabs to local suppliers, yet high-end CMP imports persisted via license exceptions, preserving baseline semiconductor wafer polishing and grinding equipment market demand.

North America experienced an investment renaissance following the 2022 CHIPS and Science Act, which mobilized USD 52 billion in incentives and prompted over 90 fab announcements worth nearly USD 450 billion through 2025. Capacity additions raised tool orders, although technician gaps of 67,000 positions by 2030 drove automation priorities and partnerships with academic consortia to accelerate workforce pipelines.

Europe followed with the EUR 43 billion (USD 49.83 billion) Chips Act that targeted a 20% global output share by 2030. Germany's precision-engineering firms, France's advanced-packaging hubs, and Nordic material-science institutes demanded CMP systems featuring energy-recovery pumps and water-recycling loops, aligning procurement with EU Green Deal objectives and fostering differentiated semiconductor wafer polishing and grinding equipment market solutions.

- Applied Materials Inc.

- Ebara Corporation

- DISCO Corporation

- Tokyo Seimitsu Co. Ltd (ACCRETECH)

- Revasum Inc.

- Komatsu NTC Ltd.

- Okamoto Machine Tool Works Co. Ltd.

- Lapmaster Wolters GmbH (Precision Surfacing Solutions)

- Logitech Ltd.

- Entrepix Inc. (Amtech Systems)

- G&N Genauigkeits Maschinenbau Nurnberg GmbH

- Hantop Intelligence Tech Co. Ltd.

- CMP-Tec Inc.

- Koyo Machinery Co. Ltd.

- Shanghai ShinEne Technology Co. Ltd.

- Qingdao Lapping & Polishing Equipment Co. Ltd.

- Nagase Integrex Co. Ltd.

- Strausbaugh Inc. (S-Cubed)

- Pureon AG

- Vibrantz Technologies Inc.

- Axus Technology

- SHANGHAI FAMOUS TRADE CO.,LTD (ZMSH)

- Huahai Machinery Group

- Hansung Engineering Co. Ltd.

- GPMT Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Consumption of Consumer Electronics with Advanced-Node Chips in Asia

- 4.2.2 Miniaturization Push Driving Demand for 300 mm and 450 mm CMP Tools

- 4.2.3 Foundry Capacity Investments in U.S. and Europe under CHIPS Acts

- 4.2.4 Transition to SiC/GaN Power Devices Requiring Ultra-Precision Grinding

- 4.2.5 Yield-Enhancement Needs for 3D-IC and Heterogeneous Integration

- 4.2.6 Sustainability Mandates Advancing Slurry-Free Polishing Technologies

- 4.3 Market Restraints

- 4.3.1 High Capital Cost and Long ROI Cycle for 300 mm Tools

- 4.3.2 Consumables Cost Inflation (Pads, Slurries, Diamond Wheels)

- 4.3.3 Export-Control and IP Barriers Limiting Shipments to China

- 4.3.4 Skilled-Technician Shortage for Process Set-up and Maintenance

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value Chain Analysis

- 4.8 Secondary Equipment Market Dynamics

- 4.9 Investment Analysis

- 4.10 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Wafer Grinding Machines

- 5.1.2 Wafer Polishing (CMP) Equipment

- 5.1.3 Integrated Grinder-Polisher Tools

- 5.1.4 Others (Lapping, Slicing Thinners)

- 5.2 By Wafer Size

- 5.2.1 <=150 mm

- 5.2.2 200 mm

- 5.2.3 300 mm

- 5.2.4 450 mm and Above

- 5.3 By Technology

- 5.3.1 Back-Grinding

- 5.3.2 Double-Side Grinding

- 5.3.3 Chemical Mechanical Polishing (CMP)

- 5.3.4 Edge-Grinding / Bevel Polishing

- 5.4 By Semiconductor Type

- 5.4.1 Memory (DRAM, NAND)

- 5.4.2 Logic and SoC

- 5.4.3 Power and Analog (Si, SiC, GaN)

- 5.4.4 MEMS and Sensors

- 5.4.5 CMOS Image Sensors

- 5.4.6 LED and Optoelectronics

- 5.5 By End-User

- 5.5.1 Foundries

- 5.5.2 Integrated Device Manufacturers (IDMs)

- 5.5.3 OSAT / Advanced Packaging Facilities

- 5.5.4 Research and Development Institutes and Pilot Lines

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Taiwan

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 India

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Applied Materials Inc.

- 6.4.2 Ebara Corporation

- 6.4.3 DISCO Corporation

- 6.4.4 Tokyo Seimitsu Co. Ltd (ACCRETECH)

- 6.4.5 Revasum Inc.

- 6.4.6 Komatsu NTC Ltd.

- 6.4.7 Okamoto Machine Tool Works Co. Ltd.

- 6.4.8 Lapmaster Wolters GmbH (Precision Surfacing Solutions)

- 6.4.9 Logitech Ltd.

- 6.4.10 Entrepix Inc. (Amtech Systems)

- 6.4.11 G&N Genauigkeits Maschinenbau Nurnberg GmbH

- 6.4.12 Hantop Intelligence Tech Co. Ltd.

- 6.4.13 CMP-Tec Inc.

- 6.4.14 Koyo Machinery Co. Ltd.

- 6.4.15 Shanghai ShinEne Technology Co. Ltd.

- 6.4.16 Qingdao Lapping & Polishing Equipment Co. Ltd.

- 6.4.17 Nagase Integrex Co. Ltd.

- 6.4.18 Strausbaugh Inc. (S-Cubed)

- 6.4.19 Pureon AG

- 6.4.20 Vibrantz Technologies Inc.

- 6.4.21 Axus Technology

- 6.4.22 SHANGHAI FAMOUS TRADE CO.,LTD (ZMSH)

- 6.4.23 Huahai Machinery Group

- 6.4.24 Hansung Engineering Co. Ltd.

- 6.4.25 GPMT Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment