|

시장보고서

상품코드

2034991

GRC 소프트웨어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GRC Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

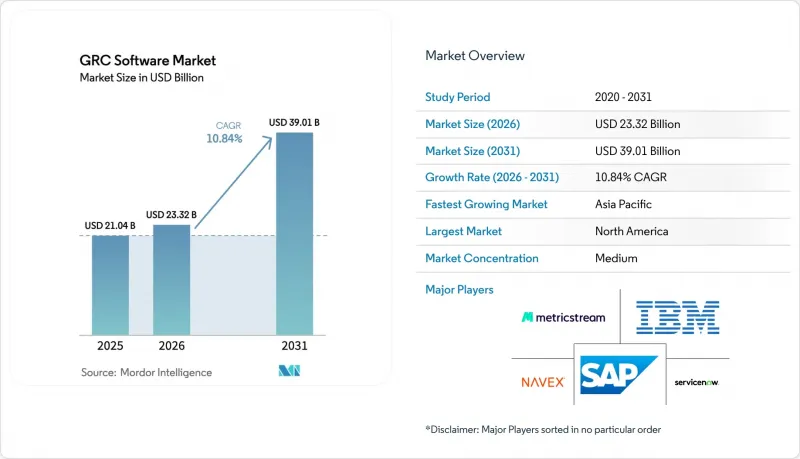

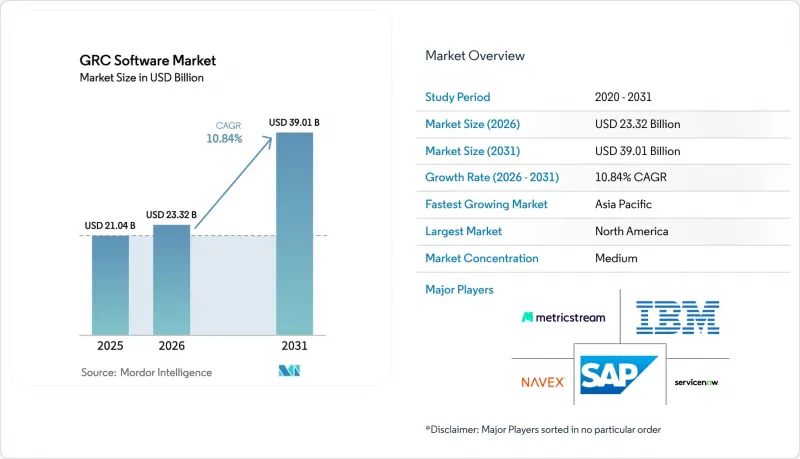

GRC 소프트웨어 시장 규모는 2025년에 210억 4,000만 달러로 평가되었고 2026년 233억 2,000만 달러에서 2031년까지 390억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.84%를 나타낼 전망입니다.

규제 차이의 확대, 사이버 공격의 표적이 되는 영역의 확대, 이사회 차원의 지속적인 통제 모니터링에 대한 요구가 증가함에 따라 기업들은 정책, 리스크, 감사 워크플로우를 실시간으로 통합하는 통합된 클라우드 네이티브 플랫폼으로 전환하고 있습니다. 소프트웨어 컴포넌트가 여전히 주류를 이루고 있지만, 매니지드 서비스의 두 자릿수 성장은 사내 기술 부족을 보완할 수 있는 전문가 주도의 도입이 선호되고 있음을 보여줍니다. 기업이 전 세계에 분산된 사업 운영 전반에 대한 통합적인 모니터링을 원하면서 클라우드 도입이 가속화되고 있습니다. 한편, AI를 활용한 분석을 통해 GRC 소프트웨어 시장은 사후 대응적인 컴플라이언스 비용에서 미래지향적인 리스크 인텔리전스에 대한 투자로 전환하고 있습니다. ESG, 프라이버시, 비즈니스 연속성 요구사항의 통합은 플랫폼 로드맵을 재구성하고 있으며, 벤더들은 탄소 회계, AI 거버넌스, 사이버 보험 증거 수집 기능을 단일 관리 화면에 통합한 모듈형 제품군을 제공하는 방향으로 나아가고 있습니다.

세계 GRC 소프트웨어 시장 동향 및 인사이트

전 세계 데이터 프라이버시 규제 강화

국경 간 데이터 프라이버시 규제가 급증하고 있으며, 엄격한 금전적 처벌로 인해 다국적 기업들은 증거 수집 및 정보 유출 알림을 자동화하는 엔드투엔드 플랫폼으로 기존의 단편적인 도구 세트를 대체해야만 합니다. "디지털 운영 탄력성 법(Digital Operational Resilience Act)과 같은 새로운 규제는 보고 대상 인시던트의 범위를 확대하고 엄격한 제3자 감시를 부과하며, 기업은 데이터 매핑, 동의 관리, 벤더 리스크 관리 워크플로우를 단일 GRC 소프트웨어 시장 플랫폼 내에 통합해야 합니다. 벤더 리스크 관리 워크플로우를 단일 GRC 소프트웨어 시장 플랫폼으로 통합하도록 촉구하고 있습니다. 한 관할 구역의 미비점이 다른 관할 구역의 동시 조사를 유발할 수 있는 연쇄적인 컴플라이언스 위반의 특성으로 인해, 지역별 관리 격차를 가시화하는 실시간 대시보드의 가치가 높아지고 있습니다. 각 벤더들은 400개 이상의 전 세계 법령에 따라 매일 업데이트되는 정책 라이브러리를 제공함으로써 이에 대응하고 있으며, 통합된 워크플로우 엔진이 각 사업부서의 책임자에게 시정 작업을 할당하고 있습니다. 기계 판독이 가능한 감사 추적을 제공하는 플랫폼은 규제 당국의 승인을 신속하게 처리하고 외부 감사 비용을 절감하며, 수동 스프레드시트에서 AI 기반 컴플라이언스 허브로의 예산 재분배 주기를 강화합니다.

클라우드 네이티브 애플리케이션의 확산

마이크로서비스, 컨테이너, 서버리스 아키텍처는 기존의 감사 스냅샷으로는 포착할 수 없는 일시적인 리소스를 생성하기 때문에 지속적인 제어 모니터링이 필수적입니다. 최신 플랫폼에는 배포 시 정책을 검증하는 쿠버네티스 어드미션 컨트롤러의 후크가 내장되어 있으며, 텔레메트리 데이터를 위험 모델에 스트리밍하여 몇 초마다 히트맵을 재계산합니다. 이러한 동적 모니터링은 디지털 퍼스트 스타트업이 하루에 수백 번씩 코드를 배포하고, 규제 당국이 운영 탄력성 공개를 의무화하고 있는 아시아태평양에서 특히 중요합니다. 구성 드리프트, 취약점 현황, 컴플라이언스 상황의 실시간 상관관계 분석을 통해 정책 위반을 감지하는 데 걸리는 평균 시간을 몇 주에서 몇 분으로 단축하여 이사회가 GRC 소프트웨어 시장에 대한 추가 투자를 정당화할 수 있도록 돕습니다. 클라우드 서비스 제공업체들은 GRC 벤더와 협력하여 에이전트 설치가 필요 없는 컴플라이언스 API를 공개함으로써 소규모 팀의 도입 장벽을 낮추고 있습니다. 그 결과, 클라우드 네이티브 통합을 통해 평가 기준은 프레임워크에 대한 체크박스 형태의 대응에서 지연시간, 확장성, 자동 복구의 깊이로 이동했습니다.

여러 관할권에 걸친 컴플라이언스의 복잡성과 비용 절감 효과

단편화된 규정집으로 인해 중복된 문서 작성 업무가 발생하여 총 컴플라이언스 비용이 연간 7,800억 달러에 달하고 있습니다. 보고 기준, 보존 기간, 위험 평가 빈도 등 모든 차이가 도구, 프로세스 및 인력에 대한 수요를 증가시키고 있습니다. 통제된 GRC 소프트웨어 기반이 부족한 다국적 기업들은 부패방지, 개인정보 보호, 비즈니스 연속성 프로그램을 위해 개별 시스템을 운영하고 있으며, 이는 데이터 사일로화 및 감사 피로를 유발하고 있습니다. 플랫폼 통합은 초기 라이선스 비용을 증가시키지만, 외부 컨설턴트에 대한 지출 감소와 규제 위반으로 인한 벌금 감소를 통해 투자 회수를 가져옵니다. 바젤 III와 같은 지역적 조화 노력은 부분적인 수렴을 가져왔지만, 프랑스의 사판 II법, 독일공급망법 등 새로운 국가별 규제가 잇따라 도입되고 있어 장기적으로 비용 압박은 여전히 심각합니다.

부문 분석

2025년 소프트웨어는 리스크, 감사, 프라이버시, ESG 모듈을 통합한 제품군에 대한 기업의 선호로 인해 매출 점유율 71.65%를 유지했습니다. 그러나 서비스 부문은 2031년까지 연평균 복합 성장률(CAGR) 12.98%로 가장 빠르게 성장할 것으로 예상되며, 이는 기술적 실현과 전문적 가이드를 결합한 성과 중심 계약으로 시장이 이동하고 있음을 보여줍니다. 매니지드 서비스 제공업체는 플랫폼 액셀러레이터를 도입하고, 지역 규제에 비추어 통제를 매핑하고, 내부 자원이 부족한 고객을 대신하여 지속적인 모니터링 센터를 운영하고 있습니다. 이러한 하이브리드 제공 방식은 중간 규모의 구매 기업에게는 가치 실현 시간을 단축하고, 수십 개의 관할권에 동시에 진출해야 하는 대규모 다국적 기업에게는 투자 회수 기간을 단축할 수 있습니다. GRC 소프트웨어 서비스 시장 규모는 벤더들이 자문, 설정, 운영 서비스를 구독 번들에 포함시킴에 따라 꾸준히 확대될 것으로 예측됩니다. 동종업계 그룹 간 통제 성숙도를 벤치마킹하고, 도입 후 고도화된 분석 기능은 시정조치 로드맵을 통해 인사이트를 수익화하고자 하는 컨설팅 부서에 크로스셀링의 기회를 창출하고 있습니다.

플랫폼 제공업체들은 AI를 활용한 컨트롤 매핑과 자연어 기반의 정책 수집 기능을 통해 소프트웨어를 강화하여 베이스라인 도입에 필요한 수작업의 부담을 줄이고 있습니다. 또한, 사이버 범위 테스트, e디스커버리, 로우코드 워크플로우 툴과의 생태계 통합을 촉진하기 위해 오픈 API를 공개하고 있습니다. 이러한 확장성은 핵심 기능을 확장하는 파트너를 유치하여 간접적인 수익원을 활성화합니다. 자동화의 발전에도 불구하고, 다중 원장을 통한 업무 분담과 세밀한 데이터 주권 분할과 같은 복잡한 설정 작업에는 여전히 전문가의 참여가 필요하며, 이를 통해 서비스 수익의 기반은 견고하게 유지됩니다. 예측 기간 동안 기업 구매자들은 전체 프로그램 예산 중 관리형 기능에 할당하는 비율을 늘릴 것으로 예상되며, 이는 GRC 소프트웨어 시장에서 소프트웨어 및 서비스의 양대 축인 소프트웨어 및 서비스 부문의 성장을 가속할 것으로 보입니다.

2025년에는 클라우드 도입이 매출의 62.90%를 차지하며 CAGR 13.85%를 나타낼 것으로 예측됐습니다. 이는 기업이 탄력적인 확장성과 협력적 모니터링을 강력하게 요구하고 있음을 반영합니다. 서비스로 제공되는 지속적인 제어 모니터링을 통해 리스크 관리팀은 SaaS, IaaS(Infrastructure-as-a-Service), On-Premise 커넥터에서 수집한 실시간 텔레메트리 데이터를 분석할 수 있으며, On-Premise 하드웨어 설치에 대한 CAPEX 부담을 줄일 수 있습니다. On-Premise 하드웨어 도입에 따른 설비투자(CAPEX) 부담을 피할 수 있습니다. 이 아키텍처는 신속한 정책 업데이트, 컴플라이언스 증거의 자동 수집 및 원격 감사 액세스를 지원하며, 분산된 인력으로부터 높은 평가를 받고 있습니다. 통합 청사진이 성숙해지고, 벤더들이 지역별 테넌트 구성을 통해 엄격한 데이터 거주지 규정 준수를 달성함에 따라, 클라우드 솔루션의 GRC 소프트웨어 시장 규모는 On-Premise 솔루션을 능가할 것으로 예측됩니다.

에어갭 환경이 여전히 필수적인 국방, 공공 안전, 중요 인프라 등의 분야에서는 On-Premise 구축이 지속될 것입니다. 이러한 구매자들은 강력한 어플라이언스, 내부 API 게이트웨이, 오프라인 보고 기능을 원합니다. 그럼에도 불구하고 벤더들은 고객의 데이터센터나 소버린 클라우드에서 실행할 수 있는 컨테이너화 에디션을 도입하여 도입의 경계를 모호하게 만들고 있습니다. 마이그레이션 로드맵은 종종 호스트형 샌드박스 내 비본격적인 워크로드에서 시작하여 암호화, 키 관리 및 액세스 분리 기준을 검증한 후 규제 대상 데이터 세트로 확장되는 경우가 많습니다. 하이브리드 오케스트레이션 콘솔은 두 가지 모드를 모두 아우르는 통합 대시보드를 제공하여 이기종 환경 전반에서 정책 일관성과 감사 추적성을 보장합니다. 그 결과, GRC 소프트웨어 시장은 성능, 주권, 비용의 균형을 맞추는 '가능하면 클라우드, 필요하면 On-Premise'라는 패러다임으로 변화하고 있습니다.

GRC 소프트웨어 시장 보고서는 구성요소(소프트웨어 및 서비스), 구축 모드(클라우드 및 On-Premise), 조직 규모(대기업, 중소기업), 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 제조, IT 및 통신 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카) 별로 분류되어 있습니다.

지역별 분석

북미는 2025년 매출의 39.55%를 차지할 것으로 예상됐으며, 그 배경에는 성숙한 규제 프레임워크, 높은 사이버 보험 보급률, 그리고 이사회의 책임성을 촉구하는 주주 소송이 많이 발생했기 때문입니다. 연방 정부 기관은 현재 거의 실시간으로 정보 유출 알림을 요구하고 있으며, 기업들은 주요 GRC 소프트웨어 시장 플랫폼에 내장된 지속적인 모니터링 및 자동화된 증거 관리 기능을 도입해야 합니다. 또한, 기술 및 컨설팅 제공업체 간의 통합은 조달 주기를 간소화하는 자문 서비스 및 SaaS 구독 번들 제공을 통해 지역 내 도입을 가속화하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정), 알고리즘의 투명성 및 라이프사이클 모니터링까지 책임성을 확대할 예정인 EU AI법 등 선구적인 법규로 인해 구조적으로 대규모 사용자 기반을 유지하고 있습니다. 은행, 보험사, 에너지 사업자는 현재 디지털 운영 탄력성 법에 따라 자체 평가를 제출해야 하며, ICT 장애의 연쇄를 모델링하는 시나리오 테스트 엔진에 대한 새로운 수요가 생겨나고 있습니다. 따라서 유럽 구매자와 관련된 GRC 소프트웨어 시장 점유율은 소비자 보호와 시스템 안정성을 모두 중시하는 정책적 움직임에 의해 강화되고 있습니다. 각 벤더들은 지역별 데이터 처리 구역, 다국어 정책 라이브러리, 슐렘스 II 판결의 요구사항을 준수하는 플랫폼 내 국경 간 데이터 전송 점검 등을 통해 차별화를 꾀하고 있습니다.

아시아태평양은 급속한 디지털화, 핀테크 혁신, 탄소 거래제 확대에 힘입어 15.1%의 연평균 복합 성장률(CAGR)로 세계 최고치를 기록할 것으로 예측됩니다. 중국, 일본, 한국, 싱가포르 정부는 유럽의 규정을 반영하면서도 서로 다른 지속가능성 공시 기준을 도입하고 있으며, 다국적 기업들은 여러 프레임워크를 동시에 대응할 수 있는 설정 가능한 플랫폼을 선호하고 있습니다. 지역 중소기업들은 세계 브랜드의 엄격한 공급업체 인증 기준을 충족하기 위해 '성장에 따른 종량제' 방식을 점점 더 많이 채택하고 있으며, 이는 GRC 소프트웨어 시장에 대한 수요를 확대시키고 있습니다. 한편, 라틴아메리카, 중동 및 아프리카에서는 도입이 초기 단계이지만, 외국인 직접투자자가 자본을 투입하기 전에 문서화된 거버넌스 관리 체계를 요구하고 있어 관심이 높아지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Governance, Risk, and Compliance (GRC) Software market size was valued at USD 21.04 billion in 2025 and estimated to grow from USD 23.32 billion in 2026 to reach USD 39.01 billion by 2031, at a CAGR of 10.84% during the forecast period (2026-2031).

Heightened regulatory divergence, growing cyber-attack surfaces, and board-level demand for continuous controls monitoring are steering enterprises toward unified, cloud-native platforms that integrate policy, risk, and audit workflows in real time. Software components continue to dominate, yet double-digit expansion of managed services signals a preference for expert-led implementations that offset internal skills shortages. Cloud deployment is accelerating as firms seek collaborative oversight across globally distributed operations, while AI-driven analytics are turning the Governance, Risk, and Compliance (GRC) Software market from a reactive compliance outlay into a proactive risk-intelligence investment. Convergence of ESG, privacy, and operational-resilience mandates is also reshaping platform roadmaps, pushing vendors toward modular suites that embed carbon accounting, AI governance, and cyber-insurance evidence collection within a single pane of glass.

Global GRC Software Market Trends and Insights

Intensifying Global Data-Privacy Regulations

Cross-border data privacy mandates are multiplying, and stiff financial penalties are forcing multinationals to replace patchwork toolsets with end-to-end platforms that automate evidence gathering and breach notification. New regimes such as the Digital Operational Resilience Act enlarge the scope of reportable incidents and impose strict third-party oversight, prompting enterprises to consolidate data-mapping, consent management, and vendor-risk workflows inside a single Governance, Risk, and Compliance (GRC) Software market platform. The cascading nature of non-compliance-where a lapse in one jurisdiction can trigger parallel investigations elsewhere-elevates the value of real-time dashboards that surface control gaps by geography. Vendors are responding with policy libraries updated daily against more than 400 global statutes, while integrated workflow engines route remediation tasks to line-of-business owners. Platforms that deliver machine-readable audit trails are achieving faster regulator sign-offs and lowering external-audit fees, reinforcing a cycle of budget reallocation from manual spreadsheets to AI-augmented compliance hubs.

Proliferation of Cloud-Native Applications

Microservices, containers, and serverless architectures generate ephemeral resources that evade traditional audit snapshots, making continuous controls monitoring indispensable. Modern platforms now embed Kubernetes admission-controller hooks that validate policy at deploy time, streaming telemetry into risk models that recalculate heat maps every few seconds. This dynamic oversight is especially critical in Asia-Pacific, where digital-first start-ups deploy code hundreds of times per day and regulators are mandating operational-resilience disclosures. Real-time correlation of configuration drift, vulnerability posture, and compliance posture cuts mean-time-to-detect for policy violations from weeks to minutes, helping boards justify additional investment in the Governance, Risk, and Compliance (GRC) Software market. Cloud service providers are partnering with GRC vendors to publish compliance APIs that remove the need for agent installation, reducing onboarding friction for small teams. As a result, cloud-native integration has shifted evaluation criteria from checkbox support for a framework to latency, scale, and automated remediation depth.

Complexity and Cost of Multi-Jurisdictional Compliance

Fragmented rulebooks add overlapping documentation duties that inflate the total cost of compliance by USD 780 billion annually. Each divergence-be it reporting thresholds, retention periods, or risk-assessment cadences-multiplies tooling, process, and staffing demands. Multinationals that lack an orchestrated Governance, Risk, and Compliance (GRC) Software market backbone juggle separate instances for anti-corruption, privacy, and operational-resilience programs, creating data silos and audit fatigue. Platform unification drives up-front licensing fees yet delivers payback through reduced external-consultant spend and fewer regulatory fines. While regional harmonization efforts such as Basel III offer partial convergence, new country-specific regimes like France's Sapin II or Germany's Supply-Chain Act continue to proliferate, keeping cost pressures acute over the long term.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Cyber-Insurance Underwriting Requirements

- Expansion of ESG Reporting Mandates

- Shortage of In-House GRC Domain Expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained a 71.65% revenue share in 2025 thanks to enterprise preference for integrated suites that consolidate risk, audit, privacy, and ESG modules. Yet services posted the fastest expected expansion at a 12.98% CAGR through 2031, underscoring a market shift toward outcome-based engagements that fuse technology enablement with subject-matter guidance. Managed service providers deploy platform accelerators, map controls to regional regulations, and operate continuous monitoring centers on behalf of clients with limited in-house staff. This hybrid delivery approach improves time-to-value for mid-sized buyers and shortens payback periods for large multinationals that must roll out across dozens of jurisdictions simultaneously. The Governance, Risk, and Compliance (GRC) Software market size for services is projected to climb steadily as vendors package advisory, configuration, and run-time operations into subscription bundles. Enhanced post-deployment analytics that benchmark control maturity across peer cohorts create cross-sell pathways for consulting arms eager to monetize insights through remediation roadmaps.

Platform suppliers are enriching software with AI-aided control mapping and natural-language policy ingestion, decreasing the manual effort requirement for baseline deployment. They also expose open APIs to facilitate ecosystem integrations with cyber range testing, e-discovery, and low-code workflow tools. This extensibility attracts partners that extend core capabilities, stimulating indirect revenue streams. Despite automation advances, complex configuration tasks-such as multi-ledger segregation of duties or fine-grained data-sovereignty partitioning-still require specialist input, ensuring that the services revenue pool remains buoyant. Over the forecast window, enterprise buyers are expected to allocate an increasing share of total program budgets to managed capabilities, reinforcing the dual-track expansion of software and services within the Governance, Risk, and Compliance (GRC) Software market.

Cloud deployments accounted for 62.90% of revenue in 2025 and are on course to register a 13.85% CAGR, reflecting enterprise appetite for elastic scalability and collaborative oversight. Continuous controls monitoring delivered as a service allows risk teams to interrogate real-time telemetry drawn from SaaS, infrastructure-as-a-service, and on-premises connectors without the capex burden of local hardware. This architecture underpins faster policy updates, automated compliance evidence collection, and remote audit access, qualities valued by distributed workforces. The Governance, Risk, and Compliance (GRC) Software market size for cloud solutions is forecast to outpace on-premises equivalents as integration blueprints mature and as vendors achieve compliance with stringent data-residency statutes through region-specific tenancy.

On-premises deployments will persist in segments such as defense, public safety, and critical infrastructure, where air-gapped environments remain mandatory. These buyers demand hardened appliances, internal API gateways, and offline reporting capabilities. Nonetheless, vendors are introducing containerized editions that can run either in customer data centers or sovereign clouds, blurring the deployment boundary. Migration roadmaps often begin with non-production workloads in hosted sandboxes before extending to regulated data sets once encryption, key management, and access-segregation standards are validated. Hybrid orchestration consoles provide unified dashboards spanning both modes, ensuring policy consistency and audit traceability across heterogeneous estates. Consequently, the Governance, Risk, and Compliance (GRC) Software market continues its transformation toward a "cloud when possible, on-prem where required" paradigm that balances performance, sovereignty, and cost.

Governance, Risk, and Compliance (GRC) Software Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Vertical (BFSI, Healthcare and Life Sciences, Manufacturing, IT and Telecommunications, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

North America commanded 39.55% of 2025 revenue, underpinned by mature regulatory frameworks, deep cyber-insurance penetration, and a high incidence of shareholder litigation that drives board accountability. Federal agencies now expect near-real-time breach notification, compelling firms to adopt continuous monitoring and automated evidence management embedded in leading Governance, Risk, and Compliance (GRC) Software market platforms. Consolidation among technology and consulting providers has also accelerated regional uptake by offering bundled advisory plus SaaS subscriptions that streamline procurement cycles.

Europe maintains a structurally large user base due to pioneering legislation such as GDPR and the upcoming EU AI Act, which extends accountability to algorithmic transparency and lifecycle monitoring. Banks, insurers, and energy operators must now submit Digital Operational Resilience Act self-assessments, creating fresh demand for scenario-testing engines that model ICT failure propagation. The Governance, Risk, and Compliance (GRC) Software market share associated with European buyers is therefore reinforced by policy activism that stresses both consumer protection and systemic stability. Vendors differentiate through localized data-processing zones, multilingual policy libraries, and in-platform cross-border data transfer checks that align with Schrems II requirements.

Asia-Pacific is projected to achieve a 15.1% CAGR, the highest globally, fueled by rapid digitization, fintech innovation, and expanding carbon-trading schemes. Governments across China, Japan, Korea, and Singapore have launched sustainability disclosure standards that mirror, yet diverge from, European rules, prompting multinationals to favor configurable platforms capable of addressing multiple frameworks in parallel. Regional SMEs increasingly adopt pay-as-you-grow pricing to meet stringent supplier-qualification metrics imposed by global brands, funneling incremental volume into the Governance, Risk, and Compliance (GRC) Software market. Meanwhile, Latin America, the Middle East, and Africa are at earlier stages of adoption but display rising interest as foreign direct investors require documented governance controls before releasing capital.

- IBM Corporation

- SAP SE

- Oracle Corporation

- SAS Institute Inc.

- ServiceNow, Inc.

- Wolters Kluwer N.V. (Enablon)

- Thomson Reuters Corporation

- NAVEX Global, Inc.

- MetricStream, Inc.

- Diligent Corporation

- Riskonnect, Inc.

- Archer Technologies LLC (RSA)

- LogicGate, Inc.

- OneTrust, LLC

- Workiva Inc.

- Galvanize (A Diligent Company)

- Mitratech Holdings Inc.

- Ideagen PLC

- Sword GRC Limited

- SAI Global Pty Limited

- LogicManager, Inc.

- Quantivate, LLC

- ProcessGene Ltd.

- Continuity Logic, LLC

- RiskWatch International, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying global data-privacy regulations

- 4.2.2 Proliferation of cloud-native applications

- 4.2.3 Surge in cyber-insurance underwriting requirements

- 4.2.4 Expansion of ESG reporting mandates

- 4.2.5 AI-driven predictive analytics adoption in risk management

- 4.2.6 Board-level demand for "continuous controls monitoring"

- 4.3 Market Restraints

- 4.3.1 Complexity and cost of multi-jurisdictional compliance

- 4.3.2 Shortage of in-house GRC domain expertise

- 4.3.3 Regulatory uncertainty around AI governance

- 4.3.4 Vendor lock-in concerns in integrated suites

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises (SMEs)

- 5.4 By Vertical

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 IT and Telecommunications

- 5.4.5 Government and Public Sector

- 5.4.6 Energy and Utilities

- 5.4.7 Retail and Consumer Goods

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 SAS Institute Inc.

- 6.4.5 ServiceNow, Inc.

- 6.4.6 Wolters Kluwer N.V. (Enablon)

- 6.4.7 Thomson Reuters Corporation

- 6.4.8 NAVEX Global, Inc.

- 6.4.9 MetricStream, Inc.

- 6.4.10 Diligent Corporation

- 6.4.11 Riskonnect, Inc.

- 6.4.12 Archer Technologies LLC (RSA)

- 6.4.13 LogicGate, Inc.

- 6.4.14 OneTrust, LLC

- 6.4.15 Workiva Inc.

- 6.4.16 Galvanize (A Diligent Company)

- 6.4.17 Mitratech Holdings Inc.

- 6.4.18 Ideagen PLC

- 6.4.19 Sword GRC Limited

- 6.4.20 SAI Global Pty Limited

- 6.4.21 LogicManager, Inc.

- 6.4.22 Quantivate, LLC

- 6.4.23 ProcessGene Ltd.

- 6.4.24 Continuity Logic, LLC

- 6.4.25 RiskWatch International, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment