|

시장보고서

상품코드

2035003

마케팅 에이전시 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Marketing Agencies Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

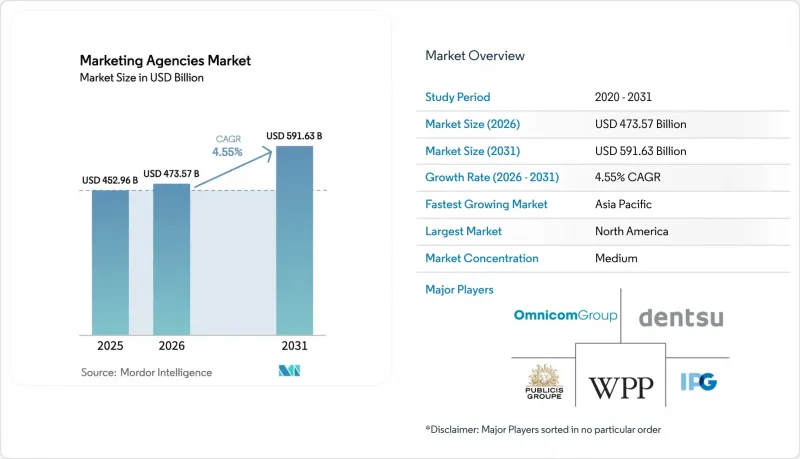

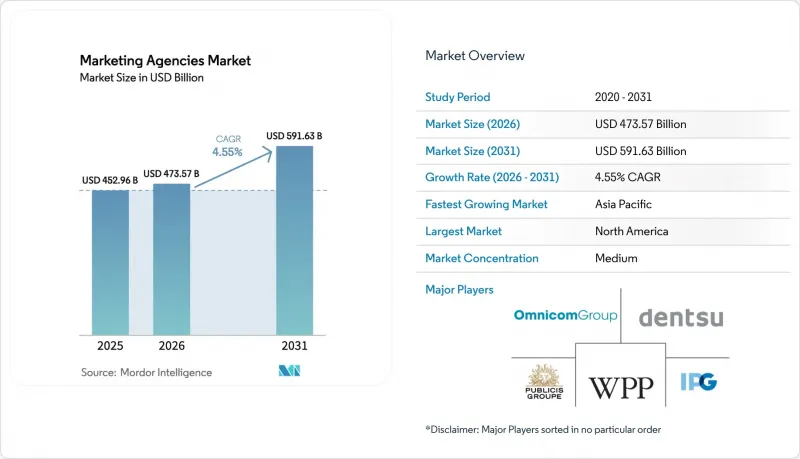

2026년 마케팅 에이전시 시장 규모는 4,735억 7,000만 달러로 추정되며 2025년 4,529억 6,000만 달러에서 성장하여 2031년에는 5,916억 3,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지 CAGR 4.55%로 성장할 전망입니다.

크리에이티브 개발에서의 인공지능 도입 확대, 성과 연동형 계약의 급속한 확대, 쿠키를 사용하지 않는 개인화 기술의 확산으로 인해 브랜드가 에이전시 제휴를 평가하는 방식이 재편되고 있습니다. 독자적인 데이터 활용 능력과 성과 연동형 보상 모델을 결합한 에이전시는 장기 계약을 체결할 수 있는 반면, 고도의 분석 역량을 갖추지 못한 에이전시는 내부 팀 확대에 따른 수익률 압박에 직면하고 있습니다. 또한 규모의 경제를 추구하는 지주회사들의 통합이 진행됨에 따라 경쟁의 격화도 두드러지고 있습니다. 옴니콤이 인터퍼블릭 그룹을 130억 달러에 인수하여 연간 7억 5,000만 달러의 비용 시너지를 기대할 수 있게 된 것이 그 좋은 예입니다.

세계 마케팅 에이전시 시장 동향과 인사이트

AI를 활용한 캠페인 최적화

인공지능(AI)은 미디어 플래닝의 개념을 재정의하고 있습니다. 실시간 알고리즘이 광고 비용 대비 효과(ROAS)를 극대화하기 위해 채널을 넘나들며 크리에이티브, 게재 위치, 입찰가를 동적으로 조정하기 때문입니다. 구글과 Smartly의 제휴는 이러한 변화를 여실히 보여주고 있습니다. 매주 수십억 개의 크리에이티브 시그널을 생성하는 이 플랫폼은 디스플레이, 소셜, 동영상 포맷을 위한 자산 선택을 자동화하고 있습니다. 유사한 시스템을 도입한 에이전시들은 두 자릿수의 효율성이 향상되었다고 보고하고 있으며, 이를 통해 전략가들은 스토리텔링과 측정 방법의 혁신에 집중할 수 있게 되었다고 합니다. 대규모 언어 모델의 급속한 발전으로 복사, 음성, 모션 그래픽은 며칠이 아닌 몇 분 만에 버전 관리가 가능해졌습니다. 지주회사들이 외부 벤더에 대한 의존도를 낮추기 위해 자체 AI 스튜디오를 설립하면서 경쟁은 더욱 치열해지고 있습니다. 중기적으로는 AI를 활용한 워크플로우와 수동 워크플로우의 성능 격차가 확대될 것으로 예상되며, 뒤처진 기업은 투자를할 것인지, 아니면 상품화의 위험을 감수할 것인지를 선택해야할 것입니다.

성과연동형 요금제 도입

성과 연동형 수수료 체계는 에이전시의 수익을 클라이언트의 비즈니스 성과와 연동하여, 노동 시간 기반 청구 대신 리드 수, 증분 매출 또는 브랜드 리프트 지표에 연계된 모델로 전환하고 있습니다. 브랜드는 이러한 계약의 투명성과 책임성을 중요하게 여기고 있으며, 성과를 증명할 수 있는 에이전시일수록 계약 갱신율이 높습니다. 그러나 성과가 부진할 경우 수익률이 직접적으로 압박을 받기 때문에 에이전시는 더 큰 재무적 리스크를 떠안게 되므로 고도의 예측 및 어트리뷰션 프레임워크가 필수적입니다. 이커머스, SaaS, 앱 마케팅 등 데이터가 풍부한 업계에서는 전환 이벤트의 귀속이 용이하기 때문에 이 방식의 도입이 가장 빠르게 진행되고 있습니다. 시장 관측통에 따르면, 성과급 수수료는 이미 인플루언서, 제휴사, DRT(Direct Response Television)에서 표준이 되었으며, 현재 주류 브랜드 캠페인으로 옮겨가고 있다고 합니다. 단기적인 성장은 북미 광고주들이 주도하고 있지만, 유럽 조달팀도 기본료와 수익 분배를 결합한 하이브리드 리테이너 계약을 시험적으로 도입하는 사례가 늘고 있습니다.

포춘지 선정 500대 기업의 인하우스 에이전시 확대

현재 대형 광고주의 82%가 어떤 형태로든 사내 에이전시를 운영하고 있으며, 2015년 이후 거의 두 배로 증가했습니다. 비용 절감, 신속한 대응, 그리고 퍼스트 파티 데이터에 대한 근접성이 이러한 변화의 원동력이 되고 있습니다. 외부 파트너는 풀패널 형태의 리테이너 계약보다는 프로젝트 기반이나 전문적 업무를 맡는 경우가 많아지고 있으며, 이로 인해 기존 에이전시의 수익 예측이 어려워지고 있습니다. 존재의 의미를 유지하기 위해, 지주 그룹은 고객사 사무실 내에 부서 간 팀을 배치하고 전략적 감독과 현장 제작을 결합하고 있습니다. 하이브리드 모델은 엄격한 규정 준수 요건을 보완하는 외부 전문 지식이 엄격한 규정 준수 요건을 보완하는 규제 산업에서 번성하고 있습니다. 중기적으로는 내부 팀과 외부 팀의 경계가 모호해지면서 브랜드 거버넌스를 유지하면서 리소스를 유연하게 운용할 수 있는 에이전시가 우위를 점할 것입니다.

부문 분석

디지털 마케팅 서비스는 2025년 매출의 61.58%를 차지할 것으로 예상됐으며, 지출과 전환 이벤트를 연결하고 측정 가능한 옴니채널 참여 모델에 대한 브랜드의 선호도를 보여줍니다. 이러한 우위가 마케팅 에이전시 시장 규모 확대의 기반이 되고 있지만, 클라이언트가 미디어, 컨텐츠, 커머스 워크플로우 전반에 걸친 통합적인 거버넌스를 요구함에 따라 풀서비스 에이전시가 CAGR 11.32%로 가장 빠른 성장세를 보이고 있습니다. 통합의 이점은 통합 데이터 레이크에서 나타나며, 크로스 채널 어트리뷰션이 명확하고 종합적인 최적화를 가능하게 합니다. 한편, 전통적인 마케팅 서비스는 체험형 액티베이션, 스폰서십 컨설팅, 그리고 물리적 접점이 프리미엄 브랜드 자산을 가져다주는 인쇄 매체를 많이 사용하는 럭셔리 분야에서 여전히 존재감을 유지하고 있습니다. AI를 활용한 풀서비스 모델이 규모를 확대하면 디지털 전문 에이전시 시장 점유율이 급상승할 가능성이 높습니다.

예측 분석에 대한 수요가 증가함에 따라 성과 중심 계약으로의 전환이 가속화되고 있으며, 크리에이티브의 가시성, 구매 경로, 평생 가치를 포괄하는 자체 대시보드에 투자하는 에이전시들이 그 혜택을 누리고 있습니다. 반대로 타사 광고 서버에만 의존하는 기업은 플랫폼이 네이티브 최적화 기능을 제공함에 따라 우위를 잃어가고 있습니다. 주요 그룹들은 이에 대응하여 기술력 향상을 위한 예산을 머신러닝 연구실과 로우코드를 통한 컨텐츠 자동화에 투입하고 있습니다. 예측 기간 동안 마케팅 에이전시 업계는 미디어 바잉과 커머스 인에이블먼트의 융합이 진행될 것으로 예상되며, 전통적인 크리에이티브 전문 부티크는 자신의 존재 의미를 지키기 위해 퍼포먼스형 에이전시와 제휴 및 합병을 할 수 밖에 없을 것입니다.할 것입니다.

지역별 분석

북미는 견조한 기업 지출과 성숙한 애드테크 인프라를 바탕으로 2025년 전 세계 매출의 36.05%를 차지할 것으로 예측됐습니다. 미국 고객들은 AI를 활용한 크리에이티브 최적화를 우선시하고 있으며, 캐나다의 구글에 대한 반독점법 조치는 다양한 광고 생태계를 향한 규제 움직임을 부각시키고 있습니다. 멕시코의 급성장하는 전자상거래 시장은 국경을 초월한 인플루언서 프로그램과 현지화된 크리에이티브 스튜디오를 결합한 네트워크 에이전시를 끌어들이고 있습니다. 유럽은 GDPR(EU 개인정보보호규정)로 인한 엄격한 개인정보 보호 규제로 인해 쿠키리스 솔루션과 퍼스트파티 데이터 제휴에 대한 투자를 촉진하고 있습니다. 특히 독일과 북유럽 국가들에서 ESG 기대에 부합하는 에이전시들은 지속가능성에 초점을 맞춘 캠페인 경쟁 입찰에서 우위를 점하고 있습니다. 언어의 다양성은 중앙 집중식 분석 허브와 각 국가별 크리에이티브 팀을 결합한 하이브리드형 인재 모델을 유리하게 만듭니다.

아시아태평양은 모바일 중심 소비, 소셜 커머스 확산, 중산층의 자유재량지출 증가에 힘입어 연평균 14.24%라는 놀라운 성장세를 보이고 있습니다. 중국 마케터들은 알리바바, 텐센트, 두잉에 걸친 플랫폼의 세분화에 대응하기 위해 브랜드당 평균 12.7개의 에이전시를 활용하고 있습니다. '디지털 인디아' 프로그램에 따라 인도의 중소기업이 급증함에 따라 현지어 컨텐츠와 저용량 동영상 포맷에 대한 수요가 증가하고 있습니다. 동남아시아 시장에서는 인플루언서 중심의 라이브 커머스가 정착되고 있으며, 에이전시는 현지 사투리에 정통한 크리에이터 네트워크를 구축해야 하는 상황입니다. 일본 에이전시 업계에서는 담합 조사로 인해 컴플라이언스 감시가 강화되고 거버넌스 강화가 요구되고 있으며, 이는 세계 광고주들에게 호의적으로 받아들여지고 있습니다. 호주의 리테일 미디어 붐은 미국의 지주회사가 부티크형 커머스 컨설팅 회사를 인수하는 계기가 되어 국경을 초월한 M&:A가 지속되고 있음을 보여주고 있습니다.

중동 및 아프리카는 규모는 작지만 새로운 기회가 싹트고 있습니다. 소버린 펀드가 관광, 스마트시티 인재 유치, 문화유산 진흥을 위한 통합적 마케팅이 필요한 메가 프로젝트에 자금을 지원하고 있기 때문입니다. 아랍어 현지화 능력과 이슬람 금융에 대한 전문성을 갖춘 에이전시는 카타르와 사우디아라비아에서 경쟁사보다 앞서 있습니다. 라틴아메리카의 디지털 결제 혁명은 브라질, 아르헨티나, 콜롬비아 전역에서 소셜 커머스 캠페인을 가속화하고 있지만, 거시 경제의 변동성으로 인해 유연한 계약 조건이 요구되고 있습니다. 이러한 지역적 특성은 마케팅 에이전시 시장에서 다국어 지원과 문화적 유연성을 갖춘 서비스 제공이 요구된다는 것을 뒷받침하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Marketing Agencies Market size in 2026 is estimated at USD 473.57 billion, growing from 2025 value of USD 452.96 billion with 2031 projections showing USD 591.63 billion, growing at 4.55% CAGR over 2026-2031.

Heightened adoption of artificial intelligence in creative development, rapid scaling of performance-based pricing contracts, and cookie-less personalization technologies are reshaping how brands evaluate agency partnerships . Agencies that combine proprietary data capabilities with outcome-linked remuneration models secure longer-term contracts, while those lacking advanced analytics face margin pressure as in-house teams expand. Competitive intensity also rises as holding companies consolidate to capture scale efficiencies, exemplified by Omnicom's USD 13 billion acquisition of Interpublic Group that promises USD 750 million in annual cost synergies.

Global Marketing Agencies Market Trends and Insights

AI-driven campaign optimization

Artificial intelligence is redefining media planning as real-time algorithms dynamically vary creative, placement, and bidding across channels to maximize return on ad spend. Google's collaboration with Smartly illustrates this pivot: weekly generation of billions of creative signals enables the platform to automate asset selection for display, social, and video formats. Agencies deploying similar systems report double-digit efficiency gains, freeing strategists to focus on storytelling and measurement innovation. Rapid advances in large language models now allow copy, audio, and motion graphics to be versioned in minutes rather than days. Competitive stakes escalate as holding groups develop in-house AI studios to avoid reliance on external vendors. Over the medium term, performance differentials between AI-enabled and manual workflows are expected to widen, pressuring laggards to invest or risk commoditization.

Performance-based pricing adoption

Outcome-linked fee structures align agency revenue with client business results, replacing labor-hour billing with models tied to lead volume, incremental sales, or brand-lift metrics. Brands value the transparency and accountability of these contracts, leading to higher renewal rates for agencies able to prove impact. However, agencies assume greater financial risk because under-performance directly erodes margins, necessitating sophisticated forecasting and attribution frameworks. Data-rich verticals such as e-commerce, SaaS, and app marketing are quickest to adopt because conversion events are easily attributable. Market observers note that performance fees are already standard in influencer, affiliate, and direct-response television, and they are now moving into mainstream brand campaigns. Short-term growth stems from North American advertisers, yet European procurement teams increasingly pilot hybrid retainers that blend base fees with shared upside.

In-house agency expansion among Fortune 500 companies

Eighty-two percent of large advertisers now operate some form of internal agency, nearly doubling since 2015. Cost savings, faster turnaround, and closer proximity to first-party data motivate this shift. External partners increasingly win project-based or specialist assignments rather than full-funnel retainers, eroding revenue visibility for traditional shops. To defend relevance, holding groups embed cross-functional pods inside client offices, pairing strategic oversight with on-site production. Hybrid models flourish in highly regulated sectors where external expertise complements strict compliance mandates. Over the medium term, the boundary between in-house and external teams blurs, rewarding agencies that can flex resources while maintaining brand governance.

Other drivers and restraints analyzed in the detailed report include:

- Cookieless personalization technologies

- Retail media network proliferation

- Talent attrition to big-tech product teams

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital marketing services retained 61.58% of 2025 revenue, underscoring brands' preference for measurable, omnichannel engagement models that link spend to conversion events. This dominance anchors the marketing agencies' market size baseline, yet full-service agencies exhibit the fastest growth at 11.32% CAGR because clients seek unified governance across media, content, and commerce workflows. Integration advantages manifest in consolidated data lakes that reveal cross-channel attribution, allowing holistic optimization. Meanwhile, traditional marketing services persist in experiential activations, sponsorship consulting, and print-heavy luxury verticals where physical touchpoints carry premium brand equity. The marketing agencies' market share of digital specialists is likely to plateau once AI-augmented full-service models reach scale.

Demand for predictive analytics accelerates migration toward outcome-oriented contracts, benefiting agencies that invest in proprietary dashboards covering creative viewability, path-to-purchase, and lifetime value. Conversely, firms that depend solely on third-party ad servers lose leverage as platforms offer native optimization. Leading groups respond by funneling up-skilling budgets into machine-learning labs and low-code content automation. Over the forecast horizon, the marketing agencies industry expects greater convergence between media buying and commerce enablement, compelling legacy creative boutiques to partner or merge with performance shops to safeguard relevance.

The Marketing Agencies Market Report is Segmented by Service Type (Digital Marketing Services, Traditional Marketing Services, Full-Service Agencies), Application (Large Enterprises, Small and Mid-Sized Enterprises), End User (BFSI, IT and Telecom, Retail and Consumer Goods, Public Services, Manufacturing and Logistics), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.05% of global 2025 revenue amid robust enterprise spending and mature ad-tech infrastructure. U.S. clients prioritize AI-enabled creative optimization, while Canada's antitrust action against Google underscores regulatory momentum toward diversified ad ecosystems. Mexico's accelerating e-commerce market attracts network agencies that pair cross-border influencer programs with localized creative studios. Europe follows as the second-largest region, with GDPR-driven privacy rigor catalyzing investment in cookieless solutions and first-party data alliances. Agencies that align with regional ESG expectations win competitive bids for sustainability-focused campaigns, especially within Germany and the Nordic states. Linguistic diversity favors hybrid talent models that combine centralized analytics hubs with country-specific creative pods.

Asia-Pacific stands out with a 14.24% forecast CAGR, propelled by mobile-centric consumption, social commerce proliferation, and rising middle-class discretionary spend. China's marketers employ an average of 12.7 agencies per brand to navigate platform fragmentation across Alibaba, Tencent, and Douyin. India's SME surge under the Digital India program spurs demand for vernacular content and low-data video formats. Southeast Asian markets embrace influencer-driven live-commerce, prompting agencies to cultivate creator networks fluent in local dialects. Japan's agency landscape experiences heightened compliance scrutiny following bid-rigging investigations, forcing governance enhancements that global advertisers view favorably. Australia's retail media boom entices U.S. holding companies to acquire boutique commerce consultancies, signaling ongoing cross-border M&A.

The Middle East and Africa represent smaller but nascent opportunities as sovereign funds finance megaprojects requiring integrated marketing for tourism, smart-city recruitment, and cultural heritage promotion. Agencies with Arabic localization capabilities and Islamic finance expertise position ahead of rivals in Qatar and Saudi Arabia. Latin America's digital-payment revolution accelerates social-commerce campaigns across Brazil, Argentina, and Colombia, although macroeconomic volatility mandates flexible contract terms. Collectively, regional nuances reinforce the marketing agencies market's requirement for multilingual, culturally agile service delivery.

List of Companies Covered in this Report:

- WPP

- Omnicom Group

- Publicis Groupe

- Interpublic Group

- Dentsu Group

- Accenture Song

- Havas Group

- Deloitte Digital

- Cognizant Interactive

- IBM iX

- Cheil Worldwide

- Hakuhodo DY Holdings

- BBDO

- Ogilvy

- Grey Group

- Saatchi & Saatchi

- R/GA

- VMLY&R

- Leo Burnett

- TBWA Worldwide

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven campaign optimization

- 4.2.2 Performance-based pricing adoption

- 4.2.3 Cookieless personalization technologies

- 4.2.4 Accelerated shift of B2B budgets to ABM platforms

- 4.2.5 SME-friendly self-serve ad portals

- 4.2.6 Retail media network proliferation

- 4.3 Market Restraints

- 4.3.1 In-house agency expansion among Fortune 500

- 4.3.2 Talent attrition to big-tech product teams

- 4.3.3 Data-privacy-driven campaign compliance costs

- 4.3.4 Fragmented measurement standards

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Digital Marketing Services

- 5.1.2 Traditional Marketing Services

- 5.1.3 Full-Service Agencies

- 5.2 By Application

- 5.2.1 Large Enterprises

- 5.2.2 Small and Mid-Sized Enterprises (SMEs)

- 5.3 By End User

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Retail and Consumer Goods

- 5.3.4 Public Services

- 5.3.5 Manufacturing and Logistics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 WPP

- 6.4.2 Omnicom Group

- 6.4.3 Publicis Groupe

- 6.4.4 Interpublic Group

- 6.4.5 Dentsu Group

- 6.4.6 Accenture Song

- 6.4.7 Havas Group

- 6.4.8 Deloitte Digital

- 6.4.9 Cognizant Interactive

- 6.4.10 IBM iX

- 6.4.11 Cheil Worldwide

- 6.4.12 Hakuhodo DY Holdings

- 6.4.13 BBDO

- 6.4.14 Ogilvy

- 6.4.15 Grey Group

- 6.4.16 Saatchi & Saatchi

- 6.4.17 R/GA

- 6.4.18 VMLY&R

- 6.4.19 Leo Burnett

- 6.4.20 TBWA Worldwide

7 Market Opportunities & Future Outlook

- 7.1 Generative-AI-enabled hyper-personalized creative studios

- 7.2 Brand commerce integration with live-stream shopping platforms