|

시장보고서

상품코드

2035028

전자 실험실 노트(ELN) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Electronic Laboratory Notebook (ELN) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

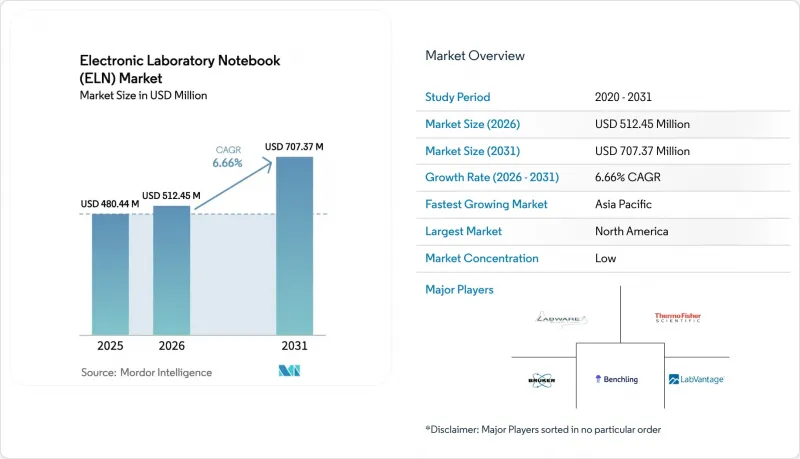

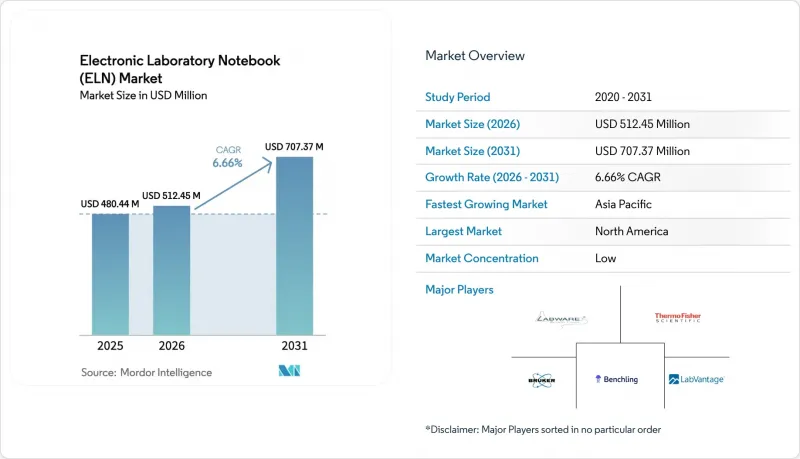

2026년 전자 실험실 노트(ELN) 시장 규모는 5억 1,245만 달러로 추정되며 2025년 4억 8,044만 달러에서 성장하여 2031년에는 7억 737만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 6.66%를 나타낼 것으로 예측됩니다.

이러한 강력한 성장의 원동력은 생명과학 분야 연구소의 디지털화, 데이터 무결성에 대한 규제 압력 증가, 그리고 ELN을 수동적인 기록 시스템에서 능동적인 연구 보조 도구로 전환하는 인공지능(AI) 기능의 등장에 기인합니다. 과거 오프프레미스 컴퓨팅에 신중한 태도를 보였던 이 분야에서 웹 기반 도입이 빠르게 받아들여지고 있는 점은 특히 주목할 만합니다. 사이버 보안 대책에 대한 감시가 강화되고 있음에도 불구하고, 2024년에는 이미 클라우드 플랫폼이 67.92%의 점유율을 차지했습니다. 다학제 솔루션은 55.45%의 점유율로 여전히 주요 제품 카테고리로, 단일 플랫폼에서 화학, 생물학, 분석 기능을 지원하는 통합 데이터 모델에 대한 요구를 반영하고 있습니다. 이러한 광범위한 기능과 21 CFR Part 11 준수 기능을 결합하여 제공하는 벤더는 미국과 유럽에서 데이터 무결성 위반이 지속적으로 증가하고 있다는 검사 결과에 따라 전략적 우위를 점할 수 있습니다. 수요 측면에서는 아시아태평양의 계약 연구 기관(CRO)이 빠르게 성장하고 있으며, 규제 조화가 아직 진행 중인 아시아태평양에서 전자 실험실 노트(ELN) 시장을 높은 성장 궤도에 올려놓았습니다.

세계 전자 실험실 노트(ELN) 시장 동향과 인사이트

생명과학 분야 연구 개발의 디지털화 급성장

생명과학 연구소는 2025년까지 연간 약 40 엑사바이트의 데이터가 생성될 것으로 예상했으며, 탐색적 연구와 GxP 프레임워크가 결합된 구조화되고 검색 가능한 리포지토리에 대한 요구가 증가하고 있습니다. 다학제적 ELN은 현재 실험실의 운영체제로서 역할을 하며, 장비의 데이터를 실시간으로 수집하고, 표준화된 메타데이터를 적용하고, 감사인이 기대하는 감사 추적을 생성합니다. 머신러닝 모델에는 깨끗하고 리니어지(데이터 흐름)가 명확한 데이터 세트가 필요하고, ELN이 주요 집약 노드로 빠르게 자리를 잡아가고 있기 때문에 이러한 환경은 전자 실험실 노트 시장을 활성화시킬 것입니다. 제약사들은 아웃소싱 계약에서 디지털 데이터 수집을 의무화함으로써 도입을 더욱 가속화하고 있으며, 도입이 늦었던 CRO(의약품 개발 수탁기관)를 빠른 도입 주기로 몰아넣고 있습니다. 이러한 추세는 광범위한 사용자 커뮤니티가 더 많은 공유 템플릿, 모범 사례 워크플로우, 사전 학습된 AI 모델을 생성하는 네트워크 효과로 이어져 플랫폼의 가치를 강화하고 있습니다.

데이터 무결성에 대한 규제 당국의 추진(21 CFR Part 11)

2024년, 데이터 무결성 부족이 제약회사에 대한 FDA의 경고서에서 가장 중요한 지적사항으로 지적된 이후, 규제 당국은 전자 기록에 대한 단속을 강화했습니다. 최신 ELN은 변조 불가능한 감사 추적, 세분화된 권한 설정, 검증된 종이 기록과 유사한 전자 서명 프로토콜을 통해 이러한 모니터링을 지원합니다. 완전 준수 시스템을 도입하는 기업은 시정 비용을 절감하고, 심사 기간을 단축하며, EU, 중국, 인도가 유사한 요구사항으로 수렴하는 가운데 국경 간 신청에 대한 신뢰성을 높일 수 있습니다. 현재 검증 패키지와 지속적인 패치 문서를 제공할 수 있는 벤더가 경쟁 우위를 점하고 있으며, 이미 품질 관리 업무로 바쁜 IT 부서의 부담을 상당 부분 덜어주고 있습니다.

뿌리 깊은 데이터 보안에 대한 우려

위탁개발생산기관(CDMO)에서 발생한 정보 유출 사건으로 인해 지적재산권 유출과 환자 데이터 노출에 대한 우려가 커지고 있다(Pharma-Focus-America). 의사결정권자들은 규제 당국으로부터의 벌금이나 평판 훼손을 우려해 클라우드 전환을 미루는 경우가 많은데, 이는 효율성의 이점을 훨씬 능가할 수 있는 잠재적 위험 요소입니다. 다단계 인증, 행동 기반 이상 징후 감지, 지속적인 침입 테스트와 같은 효과적인 대책은 특히 정보 보안 담당자가 한정된 중견기업에 있어 비용과 복잡성을 증가시킵니다. 그 결과, 일부 구매자는 미션 크리티컬한 워크플로우를 On-Premise로 유지하고 있으며, 이는 단기적으로 전자 실험실 노트 시장의 총 잠재 시장 규모를 감소시키는 요인으로 작용하고 있습니다.

부문 분석

다학제간 솔루션은 2025년 매출의 54.93%를 차지했으며, 기업들이 화학 합성, 분자생물학, 분석 워크플로우를 아우르는 단일 인터페이스를 선호하는 경향을 보이고 있습니다. 이 부문의 CAGR 6.41%는 조직이 종이 노트와 독립형 전문 앱을 폐지함에 따라 통합이 계속 진행될 것임을 시사합니다. 머신러닝 모델은 통합 데이터 세트에서 더 많은 인사이트를 얻기 위해 광범위한 기능을 갖춘 플랫폼은 알고리즘의 성능을 향상시키고 구매자의 선호도를 높이고 전자 실험실 노트(ELN) 시장에서 이 부문의 점유율을 더욱 확대할 수 있습니다. 학술 연구실에서도 비슷한 추세를 볼 수 있습니다. 384명의 학생을 대상으로 한 사용자 설문 조사에서 수기 기록장 대비 가독성, 실시간 협업, 구조화된 검색 기능이 결정적인 장점으로 꼽혔습니다. 예측 기간 동안 스펙트럼 분석 위젯이나 세포 배양 대시보드와 같은 보다 전문적인 기능들은 틈새 도구로 남지 않고 이러한 종합적인 시스템에 통합될 가능성이 높으며, 이로 인해 통합의 움직임이 가속화될 것으로 보입니다.

합성화학 최적화나 미생물 균주 엔지니어링과 같이 전문용어와 단위 조작이 매우 독특한 심층 수직 시장에서는 전문 ELN이 여전히 중요하게 작용하고 있습니다. 이러한 틈새 시장을 공략하는 업체들은 내장된 계산기, 화학량론적 균형 조정 기능, 분야별 규제 조항에 맞춘 템플릿 라이브러리를 기반으로 프리미엄 가격을 책정하고 있습니다. 그러나 통합 요구 사항으로 인해 대기업은 종종 혼합형 도입을 선택하는 경향이 있습니다. 즉, 전문 기능을 내장한 플러그인으로 강화된 다학제적 핵심 시스템입니다. 이러한 하이브리드 도입 패턴은 애플리케이션 프로그래밍 인터페이스(API) 생태계를 확장하고, 데이터를 구조화된 ELN 항목으로 직접 전송하고자 하는 계측기 벤더를 지원할 수 있습니다.

2025년에는 독점 플랫폼이 전 세계 매출의 78.15%를 차지했습니다. 이러한 장점은 번들로 제공되는 검증 결과물, 24시간 365일 지원 체제, 그리고 적극적인 제품 로드맵 배포 속도에 기반하고 있습니다. 벤더가 기성품 설치적격성평가(IQ) 및 운영적격성평가(OQ) 문서를 제공함으로써 컴플라이언스에 대한 부담을 줄일 수 있기 때문에 기업 구매 담당자들은 이를 높이 평가했습니다. 그러나 전자 실험실 노트(ELN) 업계에서는 뚜렷한 전환을 볼 수 있습니다. 오픈소스 대체 솔루션은 벤더 종속과 높은 라이선스 비용을 피하고자 하는 대학과 중소기업에 힘입어 CAGR 7.31%를 나타낼 것으로 예측됩니다. 커뮤니티 프로젝트는 현재 모듈식 아키텍처, 컨테이너화된 배포, 그리고 기존의 기능적 격차를 메우는 광범위한 플러그인 생태계를 제공합니다.

하이브리드 모델들이 점점 더 많은 인기를 얻고 있습니다. 조직은 오픈 코어형 ELN 기반을 통합하고, 그 위에 분석, 바코드 통합, 전자서명 등을 위한 독자적인 확장 기능을 얹고 있습니다. 이러한 접근 방식을 통해 사용자 정의성을 유지하면서 규제상의 체크포인트를 확실히 충족할 수 있습니다. 앞으로 오픈소스 기여자들이 품질 관리 프로세스를 체계화하고, 컴플라이언스 컨설팅 회사와의 제휴를 통해 신뢰성의 장벽이 해소되고 건전한 경쟁이 촉진될 것입니다. 그 결과, 혁신 주기의 가속화와 가격의 적정화를 통해 최종 사용자에게 혜택이 돌아갈 수 있습니다.

"전자 실험실 노트(ELN) 보고서는 제품 유형(학제형 ELN, 특정 분야형 ELN), 라이선스 유형(독점, 오픈소스), 도입 형태(웹/클라우드 기반, On-Premise), 최종 사용자(제약/바이오 기업, 수탁 연구기관, 학술/연구기관 등), 지역(북미, 유럽 등)별로 분류하여 분석하였습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

북미는 여전히 가장 큰 시장이며, 보스턴-캠브리지, 샌프란시스코 베이 지역, 롤리-더럼 회랑의 생명공학 집적화가 2025년 전 세계 매출의 37.65%를 것으로 예측됐습니다. FDA의 잦은 점검으로 인해 기업들은 검증이 완료된 플랫폼을 조기에 채택할 수밖에 없었고, 이러한 관행은 대형 제약사들 시장 포화에도 불구하고 조달 주기를 계속 연장시키고 있습니다. 인공지능(AI) 확장 기능에 대한 투자로 도입 기반이 더욱 확대되고 있습니다. 예를 들어, 미국의 한 대형 바이오 제약사는 프로토콜 작성 및 품질 보증(QA) 검토를 효율화하기 위해 전자 실험실 노트(ELN)에 내장된 생성 모델을 시범적으로 도입하고 있습니다.

유럽은 두 번째로 큰 시장 규모를 자랑하며, 독일의 화학 분야 전문성, 영국의 유전체학에 대한 집중, 그리고 '호라이즌 유럽'의 국경 간 공동연구에 대한 지속적인 자금 지원으로 뒷받침되고 있습니다. 브렉시트에 따른 데이터 주권에 대한 논의로 일부 영국 연구소는 벤더 계약을 재검토했지만, 영국의 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)에 따른 적합성을 확인한 후 대부분 기존 클라우드 제공업체를 유지하기로 했습니다. EU의 부속서 11 준수는 FDA의 요구사항과 병행하여 다국적 기업은 지역별 맞춤화를 최소화하고 세계 ELN 템플릿을 배포할 수 있습니다. 그 결과, 유럽의 전자 실험실 노트 시장 규모는 2031년까지 1억 8,410만 달러 이상에 달할 것으로 예측됩니다.

아시아태평양은 중국의 IND 신청 급증과 인도의 생물학적 제제 제조 의욕에 힘입어 8.71%의 가장 높은 CAGR을 기록했습니다. 지역 CRO 업체들은 현지 규제 당국과 동기화된 데이터 액세스를 원하는 유럽 및 미국 고객 모두를 만족시키기 위해 확장성이 높은 ELN 플랫폼에 적극적으로 투자하고 있습니다. 싱가포르의 '국가 AI 전략'이나 한국의 '바이오 디지털 이니셔티브'와 같은 정부 주도의 이니셔티브는 디지털 실험실로의 전환을 위한 보조금을 제공하여 잠재적 구매자를 확대되고 있습니다. 세포치료 및 합성생물학 틈새 분야의 스타트업 기업들도 수요를 더욱 확대시키고 있습니다. 이러한 비즈니스 모델은 최신 ELN을 통해 가장 적절하게 관리되는 촘촘한 아이덴티티 체인(Chain of Identity) 문서화에 의존하고 있기 때문입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 백만 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The electronic lab notebooks market size in 2026 is estimated at USD 512.45 million, growing from 2025 value of USD 480.44 million with 2031 projections showing USD 707.37 million, growing at 6.66% CAGR over 2026-2031.

Strong momentum stems from ongoing digitization across life-sciences laboratories, growing regulatory pressure for data integrity, and the emergence of artificial-intelligence features that convert ELNs from passive record systems into active research assistants. Rapid acceptance of web-based deployments is especially striking in a sector once wary of off-premise computing, with cloud platforms already holding 67.92% share in 2024 despite heightened scrutiny of cybersecurity safeguards. Cross-disciplinary solutions remain the dominant product category at 55.45% share, mirroring the need for unified data models that support chemistry, biology, and analytical functions on a single platform. Vendors that pair these broad capabilities with built-in 21 CFR Part 11 compliance have gained a strategic edge as inspection findings show data-integrity violations continuing to rise in the United States and Europe. On the demand side, contract research organizations (CROs) in Asia-Pacific are scaling rapidly, propelling the electronic lab notebooks market toward high-growth territories where harmonized regulations are still evolving.

Global Electronic Laboratory Notebook (ELN) Market Trends and Insights

Surge in Life-Sciences R&D Digitization

Life-sciences laboratories are producing roughly 40 exabytes of data annually by 2025, intensifying the need for structured, searchable repositories that marry exploratory research with GxP frameworks. Cross-disciplinary ELNs now function as laboratory operating systems that capture instrument feeds in real time, enforce standardized metadata, and create the audit trails auditors expect. This environment elevates the electronic lab notebooks market because machine-learning models require clean, lineage-rich datasets, and the ELN is fast becoming the principal aggregation node. Pharmaceutical sponsors further accelerate adoption by mandating digital data capture in outsourcing contracts, pushing late-adopting CROs into rapid implementation cycles. Collectively, these developments foster a network effect in which broader user communities generate more shared templates, best-practice workflows, and pre-trained AI models, reinforcing platform value.

Regulatory Push for Data Integrity (21 CFR Part 11)

Regulators intensified electronic-record enforcement in 2024 as data-integrity failures topped FDA warning-letter findings for pharmaceutical manufacturers. Modern ELNs answer this scrutiny through immutable audit trails, granular permission sets, and electronic-signature protocols that mirror those of validated paper records. Companies that adopt fully compliant systems reduce remediation costs, shorten inspection timelines, and improve confidence in cross-border submissions as the EU, China, and India converge on similar requirements. Competitive advantage now accrues to vendors able to deliver validation packages and ongoing patch documentation, removing a sizeable burden from IT groups already stretched thin by quality-management tasks.

Persistent Data-Security Concerns

High-profile breaches at contract development and manufacturing organizations (CDMOs) have raised fears over intellectual-property leakage and patient-data exposure Pharma-Focus-America. Decision-makers often delay cloud migrations, fearing regulatory fines and reputational harm that could dwarf efficiency gains. Effective countermeasures-multi-factor authentication, behavior-based anomaly detection, and continuous penetration testing-add cost and complexity, particularly for midsize firms with limited infosec headcount. Consequently, some buyers keep mission-critical workflows on-premise, diluting the total addressable slice of the electronic lab notebooks market in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Cloud-Native Lab Ecosystems

- CRO Outsourcing Boom in Asia-Pacific

- Legacy LIMS/ERP Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cross-disciplinary offerings captured 54.93% of 2025 revenue, illustrating how enterprises prefer a single interface that spans chemistry synthesis, molecular biology, and analytical workflows. The segment's 6.41% CAGR signals continued convergence as organizations dismantle paper notebooks and standalone specialty apps. Because machine-learning models derive more insight from blended datasets, wide-spectrum platforms improve algorithmic performance, reinforcing buyer preference and further enlarging this slice of the electronic lab notebooks market. Academic labs echo the trend; user studies involving 384 students cited readability, real-time collaboration, and structured search as decisive advantages over hand-written logs. Over the forecast horizon, more domain-specific features-spectral-analysis widgets, cell-culture dashboards-will likely be folded into these umbrella systems rather than remain in niche tools, accelerating consolidation.

Specialized ELNs keep relevance in deep verticals such as synthetic chemistry optimization or microbial-strain engineering, where domain vocabularies and unit operations are highly idiosyncratic. Vendors catering to these niches command premium pricing justified by built-in calculators, stoichiometric balancers, and template libraries attuned to field-specific regulatory clauses. Nevertheless, integration demands often steer large enterprises toward mixed deployments: a central cross-disciplinary backbone augmented by plug-ins that embed specialty functions. This hybrid adoption pattern enlarges the ecosystem for application-programming interfaces, supporting instrumentation vendors that wish to push data directly into structured ELN entries.

Proprietary platforms contributed 78.15% of global sales in 2025, a dominance rooted in bundled validation artifacts, 24/7 support commitments, and aggressive product-road-map velocity. Enterprise buyers appreciate the reduced compliance overhead when vendors supply ready-made installation qualification (IQ) and operational qualification (OQ) documentation. Yet the electronic lab notebooks industry is witnessing a clear pivot: open-source alternatives are forecast to grow at 7.31% CAGR, fueled by universities and SMEs keen to avoid vendor lock-in and steep seat fees. Community projects now deliver modular architectures, containerized deployments, and extensive plugin ecosystems that narrow historic feature gaps.

Hybrid models are gathering steam. Organizations integrate an open-core ELN foundation and layer proprietary extensions for analytics, barcode integration, or electronic signatures. This approach preserves customizability while ensuring regulatory checkpoints remain intact. Over time, as open-source contributors formalize quality-management processes and partner with compliance consultancies, the trust barrier will erode, fostering healthy competition that benefits end users through faster innovation cycles and price discipline.

The Electronic Lab Notebooks Report is Segmented by Product Type (Cross-Disciplinary ELN, Specific/Domain ELN), License Type (Proprietary, Open-Source), Deployment Mode (Web/Cloud-based, On-Premise), End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, Academic & Research Institutes, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the single-largest contributor, capturing 37.65% of global revenue in 2025 thanks to intensive biotech clustering in Boston-Cambridge, the San Francisco Bay Area, and the Raleigh-Durham corridor. Frequent FDA inspections oblige firms to adopt fully validated platforms early, a practice that continues to propel procurement cycles even as top-tier pharma saturation grows. Investments in artificial-intelligence extensions further deepen the installed base; for example, US biopharma leaders are piloting ELN-embedded generative models to streamline protocol authoring and QA review.

Europe constitutes the second-largest region, supported by Germany's chemicals expertise, the United Kingdom's genomics focus, and sustained Horizon Europe funding for cross-border collaborations. Brexit-induced data-sovereignty debates caused some UK labs to reevaluate vendor contracts; however, most elected to maintain existing cloud providers after verifying adequacy under UK GDPR. EU Annex 11 compliance parallels FDA requirements, allowing multinational companies to roll out global ELN templates with minimal regional customization. As a result, the electronic lab notebooks market size in Europe is projected to exceed USD 184.1 million by 2031.

Asia-Pacific posts the fastest 8.71% CAGR, fueled by China's surge in IND filings and India's biologics manufacturing ambitions. Regional CRO giants invest aggressively in scalable ELN platforms to satisfy both local regulators and Western clients demanding synchronized data access. Government initiatives-Singapore's National AI Strategy, Korea's Bio-Digital initiative-offer grants that subsidize digital-lab conversions, widening the addressable buyer pool. Start-ups in cell-therapy and synthetic-biology niches further amplify demand, as these business models depend on meticulous chain-of-identity documentation best managed via modern ELNs.

- Benchling

- LabWare

- PerkinElmer (E-Notebook)

- Dassault Systemes BIOVIA

- Thermo Fisher Scientific

- Agilent Technologies

- Abbott Informatics

- LabVantage Solutions

- Dotmatics

- SciNote

- LabArchives

- Labguru (BioData)

- RSpace

- IDBS

- Arxspan

- Khemia Software

- Scispot

- Labii

- Sapio Sciences

- eLabNext

- MaterialsZone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in life-sciences R&D digitisation

- 4.2.2 Regulatory push for data integrity (e.g., 21 CFR Part 11)

- 4.2.3 Shift toward cloud-native lab ecosystems

- 4.2.4 CRO outsourcing boom in Asia-Pacific

- 4.2.5 AI-ready ELNs enabling predictive analytics (under-reported)

- 4.2.6 Venture capital funding for ELN start-ups (under-reported)

- 4.3 Market Restraints

- 4.3.1 Persistent data-security concerns

- 4.3.2 Legacy LIMS/ERP integration complexity

- 4.3.3 Talent gap in lab informatics (under-reported)

- 4.3.4 Plateauing ELN adoption in academia post-COVID (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product Type

- 5.1.1 Cross-disciplinary ELN

- 5.1.2 Specific/Domain ELN

- 5.2 By License Type

- 5.2.1 Proprietary

- 5.2.2 Open-source

- 5.3 By Deployment Mode

- 5.3.1 Web/ Cloud-based

- 5.3.2 On-premise

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organisations (CROs)

- 5.4.3 Academic & Research Institutes

- 5.4.4 Food & Beverage Industry

- 5.4.5 Petrochemical, Oil & Gas Industry

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Benchling

- 6.3.2 LabWare

- 6.3.3 PerkinElmer (E-Notebook)

- 6.3.4 Dassault Systemes BIOVIA

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Agilent Technologies

- 6.3.7 Abbott Informatics

- 6.3.8 LabVantage Solutions

- 6.3.9 Dotmatics

- 6.3.10 SciNote

- 6.3.11 LabArchives

- 6.3.12 Labguru (BioData)

- 6.3.13 RSpace

- 6.3.14 IDBS

- 6.3.15 Arxspan

- 6.3.16 Khemia Software

- 6.3.17 Scispot

- 6.3.18 Labii

- 6.3.19 Sapio Sciences

- 6.3.20 eLabNext

- 6.3.21 MaterialsZone

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment