|

시장보고서

상품코드

2035032

레거시 현대화 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Legacy Modernization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

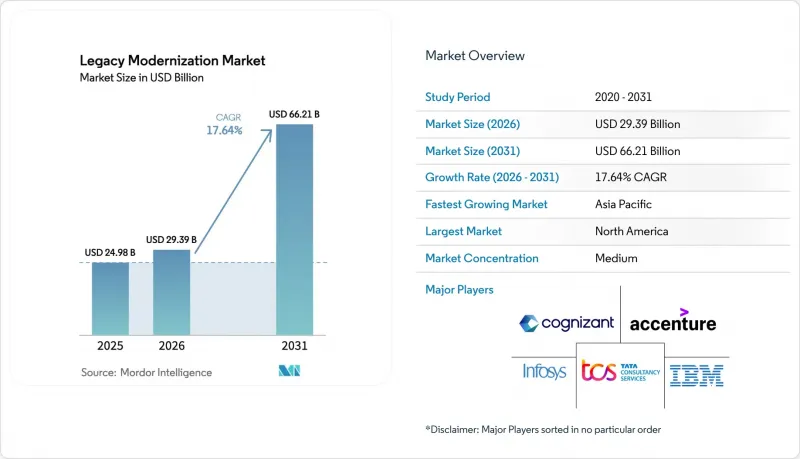

2026년 레거시 현대화 시장 규모는 293억 9,000만 달러로 추정되며 2025년 249억 8,000만 달러에서 성장하여 2031년에는 662억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 17.64%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

이러한 급격한 증가는 증가하는 기술적 부채를 해결하면서 클라우드 네이티브의 민첩성과 인공지능(AI)을 통한 효율화를 실현하는 것이 시급하다는 점을 강조합니다. 장애에 강한 실시간 디지털 보고에 대한 규제 요건이 조직에 행동을 촉구하는 한편, 경쟁 압력으로 인해 사후 대응적 유지보수에서 사전 예방적 재구축으로 전환하는 기업이 우위를 점하고 있습니다. 클라우드 도입의 대중화, GenAI를 활용한 코드 변환의 급속한 발전, 그리고 재구축 접근 방식에 대한 꾸준한 자본 유입이 결합되어 모든 주요 산업에서 투자 우선순위를 재구성하고 있습니다. 현대화가 가속화되는 가운데, 복잡한 전환 기간 동안 비즈니스 리스크를 줄이기 위한 전문 지식이 기업에게 요구되는 상황에서 서비스 중심의 접근은 여전히 매우 중요합니다. 시스템 통합사업자와 하이퍼스케일 클라우드 제공업체와의 파트너십은 깊은 업계 지식과 확장 가능한 플랫폼 기능을 결합하여 이러한 모멘텀을 더욱 강화하고 있습니다.

세계 레거시 현대화 시장 동향 및 인사이트

클라우드 네이티브를 통한 민첩성의 필요성

기업들은 모놀리식 아키텍처에서 꾸준히 탈피하고 있습니다. 이러한 시스템으로는 현재 고객용 디지털 제품이 요구하는 탄력적인 확장성, 마이크로서비스 지향성, API 우선의 상호운용성 등을 구현할 수 없기 때문입니다. 마이크로소프트와 코카콜라가 체결한 11억 달러 규모의 멀티 클라우드 계약은 세계 브랜드가 지속적인 배포 파이프라인과 세계 도달 범위를 지원하기 위해 적극적으로 현대화에 자금을 투자하고 있는 좋은 예입니다. 컨테이너 오케스트레이션과 서버리스 실행을 통해 기업은 출시 주기를 몇 개월에서 며칠로 단축하고, 거의 실시간으로 개인화 및 데이터 기반 의사결정을 내릴 수 있게 되었습니다. 디지털 스타트업이 더 빠른 제품 반복을 통해 기존 기업 시장 지위를 잠식함에 따라 이러한 추세는 더욱 강화되고 있습니다. 그 결과, 레거시 현대화 시장에서는 단계적인 리프트 앤 시프트보다 완전한 아키텍처 재구축이 계속 선호되고 있습니다.

COBOL 및 메인프레임 자산의 기술적 부채 증가

노후화된 COBOL 환경의 연간 유지보수 비용은 현재 많은 대형 은행과 보험사에서 현대화에 대한 투자비용을 능가하고 있습니다. 이러한 경향은 베테랑 개발자들의 은퇴에 따른 시스템 리스크를 경고하는 일본의 '2025년 문제'로 인해 더욱 선명하게 부각되고 있습니다. 후지쯔가 도요타와 공동으로 실시한 GenAI를 활용한 혁신으로 시스템 업데이트 기간을 50% 단축한 사례는 취약한 코드베이스를 계속 유지하는 것보다 교체하는 것이 훨씬 더 비용 효율적이라는 것을 증명하고 있습니다. 구성 요소와 기술 모두 부족한 상황에서 대응을 1년 미룰 때마다 운영 위험과 비용 곡선이 복합적으로 증가합니다. 그 결과, 이사회는 현대화를 단순한 IT 프로젝트가 아닌, 레거시 시스템 현대화를 회복탄력성의 핵심 우선순위로 인식하고 있으며, 이에 따라 레거시 시스템 현대화 시장에 대한 장기적인 수요가 증가하고 있습니다.

마이그레이션에 따른 초기 비용과 비즈니스 리스크

현대화 예산에는 일반적으로 새로운 인프라, 도구, 통합, 직원 기술 재교육 및 세부적인 변경 관리 프로그램이 포함됩니다. 리걸앤제너럴은 Kyndryl과 7년간의 데이터센터 철수 계획을 수립하고 있으며, 그린에너지로 인한 이익이 운영비용을 상쇄하는 경우에도 자본 지출이 필요하다는 점을 강조하고 있습니다. 전환 기간 동안 급여, 보험금 청구, 거래 등 미션 크리티컬한 용도에 장애가 발생하면 금전적 손실과 브랜드 가치 하락으로 이어질 수 있습니다. 그 결과, 레거시 현대화 시장은 주저하는 이사회를 안심시키기 위해 위험 완화 프레임워크, 단계적 도입 계획, 성과 기반 계약 조건을 지속적으로 패키지화해야 합니다.

부문 분석

2025년 기준, 서비스 부문은 레거시 현대화 시장의 58.05%를 차지했으며, 이러한 우위는 다년간에 걸쳐 진행되는 맞춤형 혁신 프로그램의 특화된 특성에 기인합니다. 자문 로드맵 수립, ROI 모델링, 시스템 통합, 매니지드 트랜스포메이션을 통해 재무 원장, 환자 기록 또는 국가 세금 시스템과 관련된 마이그레이션 리스크를 줄일 수 있습니다. 자동화 도구는 생산성을 향상시키지만, 기업은 여전히 비즈니스 연속성을 보장하기 위해 단계별 전환을 조정하기 위해 도메인 전문가에게 의존하고 있습니다.

소프트웨어 분야는 규모는 작지만 CAGR 16.09%로 빠르게 성장하고 있습니다. AI를 활용한 코드 분석기, 종속성 감지 도구, 자동 파이프라인 생성 도구는 현재 PaaS(Platform-as-a-Service) 제품군에 통합되어 있습니다. 구독 모델을 통해 고가의 라이선스 비용이 필요 없어지고 부분적인 도입이 가능해짐에 따라 소프트웨어 분야의 레거시 현대화 시장 규모가 확대될 것으로 예측됩니다. 이러한 추세는 패키지화된 결과물을 공동으로 제공하는 SI 파트너와 ISV(독립 소프트웨어 벤더)와의 협력을 강화하는 요인으로 작용하고 있습니다.

2025년 기준, 클라우드 모델은 레거시 현대화 시장에서 67.10%의 점유율을 차지했습니다. 기업들은 설비투자(CAPEX)의 부담 없이 탄력성, 세계 확장성, 관리형 보안 서비스를 제공하는 퍼블릭 클라우드 또는 멀티 클라우드 환경을 선호하고 있습니다. 민감한 워크로드에 대한 지역적 요구 사항으로 인해 하이브리드 패턴이 발생하지만, 이러한 아키텍처에서도 원격 측정 데이터를 퍼블릭 클라우드의 분석 엔진으로 전송하여 데이터 인사이트를 도출하고 있습니다.

순수 퍼블릭 클라우드 도입과 관련된 레거시 현대화 시장 규모는 17.98%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 이는 계속 확장되고 있는 하이퍼스케일 리전 및 현재 15개 세계 존으로 확장된 마이크로소프트와 Oracle의 'Database on Azure' 확장 같은 상호 연결 계약에 의해 뒷받침되고 있습니다. 금융, 게임, 의료 등 각 산업별 제공업체들은 계절적 워크로드에 대한 버스트 용량을 활용하고, 소버린 리전 및 기밀 컴퓨팅 인클로저를 통해 규제 준수를 보장하고 있습니다.

'레거시 현대화 시장 보고서'는 컴포넌트(소프트웨어 및 서비스), 도입 유형(On-Premise 및 클라우드), 현대화 방식(리호스팅, 리플랫폼, 리아키텍처, 리팩토링, 리플레이스먼트 및 COTS), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 제조, 헬스케어, IT, 통신, 기타), 조직 규모(대기업 및 중소기업(중소기업)), 최종 사용자 산업(제조, 금융, 의료, IT, 통신 및 기타), 조직 규모(대기업 및 중소기업)로 구분하여 분석합니다. COTS), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 제조, 헬스케어, IT 및 통신, 기타), 조직 규모(대기업 및 중소기업(SME)), 지역별로 분류됩니다.

지역별 분석

북미는 2025년 37.05%의 압도적인 매출 점유율을 차지했습니다. 이는 메인프레임의 도입 기반, 클라우드의 조기 도입, 그리고 장애에 강한 아키텍처를 중시하는 연방정부의 엄격한 감독을 반영한 것입니다. 미국 증권거래위원회(SEC)와 같은 규제 당국은 현재 자본 시장에 거의 실시간 보고를 요구하고 있으며, 클라우드 네이티브 데이터 웨어하우징과 분석을 전면에 내세우고 있습니다. 그 결과, 이 지역 전체 레거시 현대화 시장은 높은 평균 계약 금액과 장기 매니지드 서비스 갱신 계약을 유지하고 있습니다. 아시아태평양은 일본의 심각한 기술 부족, 인도의 국가적 디지털 공공 플랫폼 구상, 동남아시아의 핀테크 도입 확대에 힘입어 CAGR 15.71%로 성장하고 있습니다. NTT 데이터의 15억 달러 규모의 데이터센터 확장이나 후지쯔의 GenAI를 활용한 도요타와의 협력은 자국에서 시작된 혁신이 세계 베스트 프랙티스와 융합하고 있음을 보여줍니다. 스마트 제조 및 디지털 무역 통로를 둘러싼 정부의 경제 부양책은 레거시 현대화 시장에 더 많은 자본을 투입하고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정), 디지털 시장법, 지속가능성 지침이 겹치면서 강력한 모멘텀을 유지하고 있습니다. EU의 에너지 효율화 지침에 따라 데이터센터는 전력 사용 효율과 이산화탄소 배출량을 기록해야 하는데, 이는 최신 원격 측정 시스템 없이는 달성할 수 없는 과제입니다. 독일, 프랑스, 스페인의 소버린 클라우드 프레임워크는 공공 클라우드의 분석 기능을 대규모로 활용하면서 기밀 데이터를 영역 내에 유지하면서 하이브리드 설계로 많은 현대화 로드맵을 이끌고 있습니다. 중동 및 아프리카는 현재 규모는 작지만 디지털 정부 및 현금 없는 상거래를 우선시하는 각국의 다각화 정책으로 인해 빠르게 성장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 세분화

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

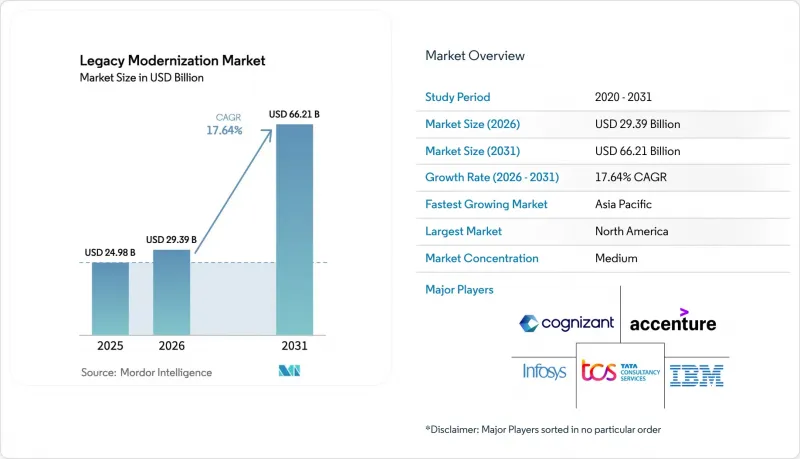

JHS 26.05.20Legacy modernization market size in 2026 is estimated at USD 29.39 billion, growing from 2025 value of USD 24.98 billion with 2031 projections showing USD 66.21 billion, growing at 17.64% CAGR over 2026-2031.

The sharp rise underscores the urgency to resolve mounting technical debt while unlocking cloud-native agility and artificial-intelligence-driven efficiencies. Regulatory mandates that demand resilient, real-time digital reporting push organizations to act, while competitive pressures reward firms that shift from reactive maintenance to proactive re-architecting. The dominance of cloud deployment, rapid progress in GenAI-assisted code conversion, and the steady inflow of capital toward re-architecting approaches together reshape investment priorities across every major vertical. As modernization accelerates, services-led engagements remain pivotal because enterprises require domain expertise that mitigates business-risk exposure during complex cut-over windows. Partnerships between systems integrators and hyperscale cloud providers further reinforce the momentum by coupling deep industry knowledge with scalable platform capabilities.

Global Legacy Modernization Market Trends and Insights

Cloud-Native Agility Imperative

Enterprises are steadily abandoning monolithic architectures because such systems cannot deliver the elastic scaling, microservices orientation, or API-first interoperability that customer-facing digital products now demand. A USD 1.1 billion multi-cloud agreement between Microsoft and Coca-Cola exemplifies how global brands fund aggressive modernization to support continuous deployment pipelines and worldwide reach. By adopting container orchestration and serverless execution, firms reduce release cycles from months to days, enabling near real-time personalization and data-driven decision-making. The trajectory intensifies as digital challengers erode incumbent market positions with faster product iteration. Consequently, the Legacy modernization market observes sustained preference for full re-architecting over incremental lift-and-shift movements.

Rising Technical Debt of COBOL and Mainframe Estates

Annual maintenance spending on aging COBOL estates now eclipses modernization investment in many large banks and insurers, a pattern vividly highlighted by Japan's "2025 cliff" that flags systemic risk as veteran developers retire. Fujitsu's work with Toyota, which cut system update time by 50% through GenAI-enabled transformation, proves that replacing brittle code bases is far cheaper than perpetuating them. With components and skills both scarce, each year of deferred action compounds operational risk and cost curves. As a result, boards increasingly treat modernization as a core resilience priority rather than an IT project, thereby boosting long-term demand for the Legacy modernization market.

Up-Front Migration Cost and Business Risk

Modernization budgets typically cover new infrastructure, tooling, integration, workforce reskilling, and detailed change-management programs. Legal and General committed to a seven-year data-center exit with Kyndryl, underlining capital outlays required even when green energy gains offset operational expense. Any disruption to mission-critical payroll, claims, or trading applications during cut-over can translate into financial penalties or brand erosion. Consequently, the Legacy modernization market must continually package risk-mitigation frameworks, phased deployment blueprints, and outcome-based commercial terms to reassure hesitant boards.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Digital Reporting and Resiliency

- Surge in GenAI-Assisted Code Conversion Tools

- Scarcity of Legacy-Language Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services controlled 58.05% of the Legacy modernization market in 2025, a lead rooted in the bespoke nature of multi-year transformation programs. Advisory road-mapping, ROI modeling, system integration, and managed transformation all converge to de-risk migrations that touch financial ledgers, patient records, or national tax systems. Automated tooling boosts productivity, yet enterprises still rely on domain specialists to orchestrate phased cutovers that safeguard business continuity.

Software, while smaller, is accelerating at a 16.09% CAGR. AI-augmented code analyzers, dependency discoverers, and automated pipeline generators are now embedded in platform-as-a-service suites. The Legacy modernization market size for software is predicted to broaden as subscription models eliminate large license fees and allow piecemeal adoption. The dynamic fosters tighter bonds between SI partners and ISVs who jointly offer packaged outcomes.

Cloud models captured 67.10% Legacy modernization market share in 2025. Enterprises favor public or multi-cloud footprints that deliver elasticity, global reach, and managed security services without capex overhead. Regional requirements for sensitive workloads produce hybrid patterns, but even these architectures pipe telemetry into public-cloud analytics engines to unlock data insights.

The Legacy modernization market size associated with pure public-cloud deployments is expanding at an 17.98% CAGR, helped by ever-growing hyperscale regions and interconnect agreements such as the Microsoft-Oracle "database-on-Azure" expansion that now spans 15 global zones. Financial, gaming, and healthcare providers leverage burst capacity for seasonal workloads while ensuring regulatory compliance via sovereign regions or confidential computing enclaves.

The Legacy Modernization Market Report is Segmented by Component (Software and Services), Deployment Type (On-Premises, and Cloud), Modernization Approach (Re-Hosting, Re-Platforming, Re-Architecting, Re-Factoring, and Replacement / COTS), End-User Industry (BFSI, Manufacturing, Healthcare, IT and Telecommunications, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), and Geography.

Geography Analysis

North America held a commanding 37.05% revenue share in 2025, reflecting an installed base of mainframes, early cloud adoption, and strict federal oversight that rewards resilient architecture. US regulators such as the Securities and Exchange Commission now impose near real-time reporting for capital markets, forcing cloud-native data warehousing and analytics to the foreground. As a result, the Legacy modernization market continues to enjoy high average contract values and long-term managed-services renewals across the region. Asia-Pacific is advancing at 15.71% CAGR, propelled by Japan's looming skills cliff, India's national digital-public-platform initiatives, and Southeast Asia's greenfield FinTech adoption. NTT DATA's USD 1.5 billion data-center expansion and Fujitsu's GenAI-assisted Toyota engagement illustrate home-grown innovation meeting global best practice. Government stimulus around smart manufacturing and digital trade corridors further injects capital into the Legacy modernization market. Europe maintains strong momentum as GDPR, the Digital Markets Act, and sustainability directives overlap. The EU Energy Efficiency Directive obliges datacenters to document power usage effectiveness and carbon emissions, a task achievable only with modern telemetry systems. Sovereign-cloud frameworks in Germany, France, and Spain steer many modernization roadmaps toward hybrid designs that keep sensitive data in-region while exploiting public-cloud analytics at scale. The Middle East and Africa, though smaller today, are accelerating thanks to national diversification agendas that prioritize digital government and cashless commerce.

- International Business Machines Corporation (IBM)

- Accenture plc

- Cognizant Technology Solutions Corporation

- Infosys Limited

- Tata Consultancy Services Limited

- Atos SE (Eviden SAS)

- Capgemini SE

- HCL Technologies Limited

- Wipro Limited

- DXC Technology Company

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC (Google Cloud)

- Oracle Corporation

- NTT DATA Corporation

- CGI Inc.

- Kyndryl Holdings, Inc.

- Tech Mahindra Limited

- Hexaware Technologies Limited

- OpenText Corporation (incl. Micro Focus)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native agility imperative

- 4.2.2 Rising technical debt of COBOL and mainframe estates

- 4.2.3 Regulatory push for digital reporting and resiliency

- 4.2.4 Surge in GenAI-assisted code conversion tools

- 4.2.5 Carbon-reduction mandates on datacenters

- 4.2.6 Mand A-driven system harmonisation deadlines

- 4.3 Market Restraints

- 4.3.1 Up-front migration cost and business risk

- 4.3.2 Scarcity of legacy-language specialists

- 4.3.3 Sovereign-cloud and data-residency restrictions

- 4.3.4 Licence-lock-in of niche ISV workloads

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Impact Assessment of Key Stakeholders

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Type

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Modernization Approach

- 5.3.1 Re-hosting

- 5.3.2 Re-platforming

- 5.3.3 Re-architecting

- 5.3.4 Re-factoring

- 5.3.5 Replacement / COTS

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Healthcare

- 5.4.4 IT and Telecommunications

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Others

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises (SMEs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Nigeria

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 Asia-Pacific

- 5.6.5.1 China

- 5.6.5.2 India

- 5.6.5.3 Japan

- 5.6.5.4 South Korea

- 5.6.5.5 ASEAN

- 5.6.5.6 Australia

- 5.6.5.7 New Zealand

- 5.6.5.8 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Business Machines Corporation (IBM)

- 6.4.2 Accenture plc

- 6.4.3 Cognizant Technology Solutions Corporation

- 6.4.4 Infosys Limited

- 6.4.5 Tata Consultancy Services Limited

- 6.4.6 Atos SE (Eviden SAS)

- 6.4.7 Capgemini SE

- 6.4.8 HCL Technologies Limited

- 6.4.9 Wipro Limited

- 6.4.10 DXC Technology Company

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Google LLC (Google Cloud)

- 6.4.14 Oracle Corporation

- 6.4.15 NTT DATA Corporation

- 6.4.16 CGI Inc.

- 6.4.17 Kyndryl Holdings, Inc.

- 6.4.18 Tech Mahindra Limited

- 6.4.19 Hexaware Technologies Limited

- 6.4.20 OpenText Corporation (incl. Micro Focus)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment