|

시장보고서

상품코드

2035039

데이터센터 서비스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2032년)Data Center Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032) |

||||||

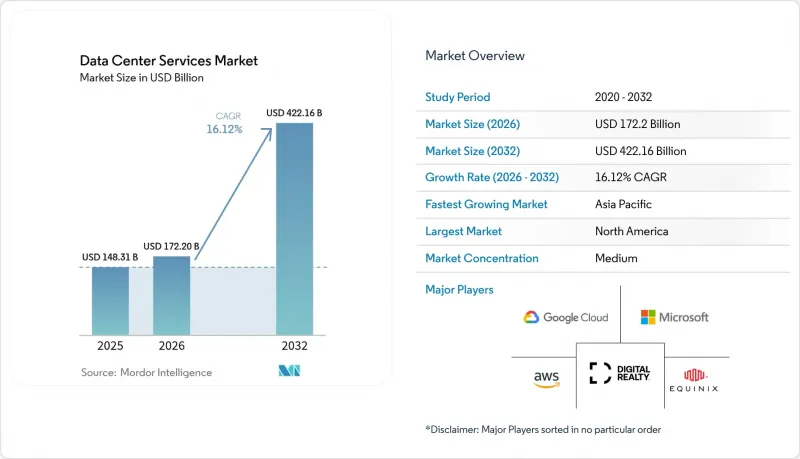

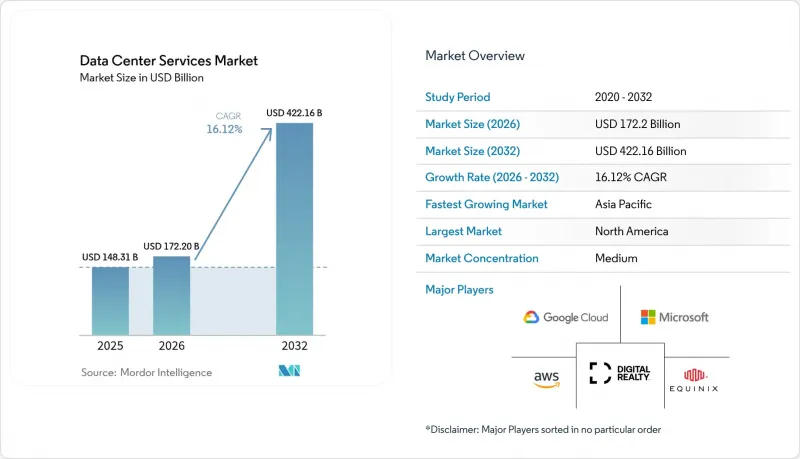

데이터센터 서비스 시장 규모는 2025년 1,483억 1,000만 달러에서 2026년에는 1,722억 달러로 확대되어 2026-2032년 CAGR 16.12%로 성장을 지속하여, 2032년에는 4,221억 6,000만 달러에 이를 것으로 예측됩니다.

기업들은 자본 집약적인 소유 모델에서 빠른 확장성을 제공하는 서비스 이용 모델로 전환하고 있습니다. 특히 인공지능(AI) 워크로드에는 기존 On-Premise 환경의 용량을 넘어서는 특수한 냉각 시스템과 전력 밀도가 필요하기 때문입니다. 코로케이션은 여전히 데이터센터 서비스 시장의 근간을 이루고 있지만, 조직이 민첩성을 위해 클라우드 네이티브 아키텍처를 채택함에 따라 클라우드 및 가상 데이터센터 서비스의 성장세는 더욱 가속화되고 있습니다. 코로케이션 전문업체와 하이퍼스케일 클라우드 제공업체들이 하이브리드 솔루션에 집중하면서 경쟁은 더욱 치열해지고 있습니다. 한편, 고전력 부품공급망 제약과 숙련된 인력 부족으로 인해 운영상의 마찰이 발생하고 있습니다. 규제 현지화 및 물 사용량 제한으로 인해 공급업체들은 시설 설계를 재검토하고 있으며, 이로 인해 더 높은 랙 밀도와 에너지 효율을 향상시킬 수 있는 액체 냉각 기술을 채택하고 있습니다.

세계 데이터센터 서비스 시장 동향 및 인사이트

데이터센터 기술에 대한 지출 증가

기업들은 이제 인프라에 대한 지출을 단순한 비용 센터가 아닌 경쟁 차별화 요소로 인식하고 있으며, 즉각적인 확장성을 제공하는 아웃소싱 모델에 더 많은 예산을 할당하고 있습니다. 이러한 추세는 마이크로소프트가 블랙록과 제휴하여 AI 인프라에 300억 달러를 투자한다고 발표한 후 두드러지게 나타났으며, 하이퍼스케일러가 외부 자본을 활용하여 도입을 가속화하고 있음을 강조하고 있습니다. 지출 수준 증가로 인해 기존 조달 주기에서 제약이 있었던 엣지 노드 및 AI 추론 엔진 도입이 가속화되고 있습니다. 고객은 도입 시간을 단축하고 최신 기술을 확보할 수 있는 관리형 환경을 선호하기 때문에 서비스 제공업체는 혜택을 누리고 있습니다. 그 결과, 데이터센터 서비스 시장에서는 최첨단 GPU 클러스터와 첨단 냉각 기술을 통합한 코로케이션 및 매니지드 호스팅에 대한 수요가 지속되고 있습니다.

클라우드와 하이퍼스케일 확장의 급격한 증가

클라우드 제공업체들은 지연시간 요건과 주권 데이터 규제를 충족하기 위해 지역 구역을 구축하고 있으며, 이로 인해 현지 서비스 파트너가 수익을 창출할 수 있는 수요가 넘쳐나고 있습니다. Oracle이 일본에 80억 달러를 투자한 것은 세계 도달 범위를 유지하면서 컴플라이언스를 충족하는 주권적 클라우드 역량에 대한 Oracle의 추진을 상징합니다. 이 확장을 통해 용량이 거대한 팜에 집중되지 않고 여러 도시에 분산되어 기업은 멀티 리전 내결함성 전략을 구축할 수 있게 됩니다. 하이퍼스케일러와의 제휴를 통해 데이터센터 서비스 시장을 클라우드 온램프와 로컬 인터커넥트를 결합한 통합 하이브리드 서비스로 전환할 수 있는 기회를 제공함으로써, 하이퍼스케일러는 새로운 수익원을 확보할 수 있습니다.

데이터 프라이버시 및 보안에 대한 우려

최근 정보 유출 사건으로 인해 기업들은 기밀성이 높은 워크로드를 외부에 위탁하는 것에 대해 신중을 기하고 있습니다. 특히 처벌이 엄격한 금융, 의료 분야에서는 이러한 경향이 두드러집니다. 공급자는 제로 트러스트 아키텍처와 투명한 사고 대응 프로세스에 투자해야 하며, 그 결과 운영 비용이 증가하여 수익률을 압박할 수 있습니다. 소규모 사업자들은 세계 동종업계와 동등한 수준의 보안 수준을 유지하기 위해 고군분투하고 있으며, 그 결과 일부 고객들은 인증된 환경을 제공하는 대형 브랜드에 통합을 추진하고 있습니다. 이 문제는 전환을 지연시키는 동시에 데이터센터 서비스 시장을 인프라 구독에 포함된 고부가가치 보안 서비스로 전환하는 요인으로 작용하고 있습니다.

부문 분석

2025년 코로케이션 서비스는 데이터센터 서비스 시장 규모의 44.72%를 차지했으며, 이는 클라우드에 직접 연결하거나 풍부한 상호 연결을 제공하는 캐리어 중립적인사이트에 대한 수요를 반영합니다. 그러나 운영 비용(OPEX)과 탄력적인 확장을 선호하는 조직에 힘입어 클라우드 및 가상 데이터센터 서비스는 CAGR 16.94%를 나타낼 것으로 예측됩니다. 코로케이션은 지연에 민감한 워크로드나 컴플라이언스 중심의 도입에 있어 여전히 매력적이며, 클라우드의 확산이 가속화되고 있는 상황에서도 안정적인 계약을 유지하고 있습니다. 매니지드 호스팅은 중견기업들이 일상적인 인프라 업무를 아웃소싱하면서 안정세를 보이고 있으며, 재해복구 및 백업은 데이터 보호에 대한 규제가 강화되면서 틈새 시장으로 성장하고 있습니다.

데이터센터 인프라 관리 도구는 전력, 냉각, 자산 활용률에 대한 실시간 인사이트를 제공하며, 모든 서비스 유형에 필수적인 요소로 자리 잡았습니다. 전문 서비스 및 컨설팅 서비스는 마이그레이션 로드맵 및 규제 감사 지도를 통해 고객과의 관계를 심화시키고 있습니다. 따라서 서비스 포트폴리오는 단일 랙 임대에서 물리적 실적, 가상 머신 및 자문 지원을 통합한 통합 제품군으로 진화하고 있습니다. 이러한 복합적인 접근 방식은 고객 유지율을 높이고, 데이터센터 서비스 시장을 향후 몇 년 동안 확장 궤도에 올려놓을 수 있도록 돕습니다.

2025년 기준, Tier III 시설은 데이터센터 서비스 시장 점유율의 54.73%를 차지했으며, 비용 효율성과 내결함성 사이에서 실용적인 균형을 유지하고 있습니다. 이러한 시설은 다운타임을 최소화하면서 Tier IV의 높은 비용을 피할 수 있는 주류 기업 워크로드를 호스팅하고 있습니다. 금융 거래 및 중요 의료 시스템을 대상으로 하는 Tier IV 사이트는 무중단 아키텍처가 인기를 끌면서 CAGR 16.02%를 나타낼 것으로 예측됩니다. Tier I과 Tier II 시설은 테스트 랩과 아카이브 스토리지를 제외하고는 점유율이 감소하고 있습니다.

사업자는 캠퍼스를 계층별로 구분하고 있으며, 이를 통해 고객은 용도의 내결함성과 예산을 일치시킬 수 있습니다. 사이트 전체를 Tier IV로 업그레이드하지 않고도 AI 클러스터에 대응하기 위해 수냉식 기술이 Tier III 홀에도 도입되고 있습니다. 이 모듈식 계층화는 가동률을 극대화하고 혼합 계층 캠퍼스의 매력을 높여 시장의 다양성을 강화하는 동시에 고객에게 세심한 가성비 절충안을 제공합니다.

'데이터센터 서비스 시장 보고서'는 서비스 유형(매니지드 호스팅 서비스, 코로케이션 서비스 등), 계층 기준(Tier I 및 II, Tier IV 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어 등), 구축 모델(On-Premise 데이터센터, 하이퍼스케일 등), 지역(북미, 아시아태평양 등)별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

지역별 분석

북미는 마이크로소프트와 블랙록의 300억 달러 규모의 AI 인프라 프로그램 등 하이퍼스케일 투자에 힘입어 2025년에도 데이터센터 서비스 시장에서 가장 큰 점유율을 유지했습니다. 잘 구축된 연결 허브, 풍부한 자본, 그리고 성숙한 규제 프레임워크가 이 지역의 리더십을 뒷받침하고 있습니다. 남서부 지역의 물 사용 제한으로 인해 액체 냉각 및 건식 냉각 솔루션의 도입이 가속화되고 있습니다. 캐나다는 지속적인 메가와트급 전력 부하를 필요로 하는 AI 트레이닝 클러스터를 유치하기 위해 재생에너지를 이용한 대안을 제공합니다.

아시아태평양은 광범위한 디지털화와 주권 데이터 정책에 힘입어 가장 빠른 성장을 기록했습니다. Oracle의 일본 내 80억 달러 규모의 주권 클라우드 구축과 NTT의 인도 내 15억 달러 규모의 확장 등은 이 지역의 모멘텀을 뒷받침하고 있습니다. 중국은 보안상의 이유로 국내 처리를 중시하고 있으며, 현지 업체를 우대하고 있습니다. 인도는 대규모 컴퓨팅을 필요로 하는 정부의 결제 시스템 및 생체 인식 프로그램의 혜택을 누리고 있으며, 동남아시아는 세계 기업과 현지 소비자를 연결하는 가교 역할을 하고 있습니다.

유럽의 동향은 GDPR(EU 개인정보보호규정)과 강화되는 지속가능성 요구사항의 영향을 받고 있습니다. 사업자들은 재생에너지 할당 목표를 달성하는 동시에 분절된 각국의 규제에 대응해야 하며, 이로 인해 컴플라이언스에 특화된 호스팅 서비스에 대한 수요가 발생하고 있습니다. 중동 및 아프리카는 새로운 개척지로 부상하고 있으며, UAE, 사우디아라비아, 케냐에서는 5억 4,400만 달러 규모의 마이크로소프트와 du의 시설과 지열발전을 이용한 캠퍼스 등 대규모 프로젝트가 발표되고 있습니다. 대륙 간 전략적 위치로 인해 이들 시장은 지역 간 허브 역할을 하고 있으며, 데이터센터 서비스 시장의 지리적 확장을 더욱 확장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The data center service market size is expected to grow from USD 148.31 billion in 2025 to USD 172.2 billion in 2026 and is forecast to reach USD 422.16 billion by 2032 at 16.12% CAGR over 2026-2032.

Enterprises are shifting from capital-heavy ownership toward service consumption models that provide rapid scalability, especially as artificial intelligence workloads require specialized cooling and power densities that outstrip traditional on-premise capabilities. Colocation remains the anchor of the data center service market, yet cloud and virtual data center services are gaining momentum as organizations embrace cloud-native architectures for agility. Competitive intensity is rising as colocation specialists and hyperscale cloud providers converge on hybrid solutions, while supply-chain constraints for high-power components and skilled labor shortages create operational friction. Regulatory localization and water-usage limitations are forcing providers to re-engineer facility designs, driving the uptake of liquid-cooling technologies that enable higher rack densities and improved energy efficiency.

Global Data Center Services Market Trends and Insights

Increase in Expenditure on Data Center Technology

Organizations now view infrastructure spending as a competitive differentiator rather than a pure cost center, allocating larger budgets to outsourced models that unlock instant scalability. The trend gained prominence after Microsoft committed USD 30 billion to AI infrastructure in partnership with BlackRock, underscoring how hyperscalers leverage external capital to accelerate deployments. Higher spending levels accelerate adoption of edge nodes and AI inference engines that would otherwise be constrained by traditional procurement cycles. Service providers benefit because clients prefer managed environments that reduce deployment time while ensuring technology currency. Consequently, the data center service market experiences sustained demand for colocation and managed hosting that integrate cutting-edge GPU clusters with advanced cooling.

Surge in Cloud and Hyperscale Expansion

Cloud providers are building regional zones to satisfy latency expectations and sovereign data rules, creating overflow demand that local service partners can monetize. Oracle's USD 8 billion investment in Japan exemplifies the push toward sovereign cloud capacity that meets compliance while maintaining global reach. The expansion diffuses capacity across multiple cities rather than concentrating it in mega-farms, allowing enterprises to architect multi-region resiliency strategies. For service vendors, partnering with hyperscalers opens cross-connect revenue streams and drives the data center service market toward integrated hybrid offerings that bundle cloud on-ramps with local interconnection.

Data Privacy and Security Concerns

High-profile breaches make enterprises cautious about outsourcing sensitive workloads, particularly in finance and healthcare where penalties are severe. Providers must invest in zero-trust architectures and transparent incident-response processes, raising operating costs that can erode margins. Smaller operators struggle to match the security depth of global peers, leading some customers to consolidate with larger brands that offer certified environments. The issue slows migrations yet also pushes the data center service market toward higher-value security services embedded within infrastructure subscriptions.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Workload Orchestration and Optimization

- Data-Sovereignty Regulations Driving Local Facilities

- Skilled Workforce Shortage in Advanced Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Colocation services generated 44.72% of the data center service market size in 2025, reflecting demand for carrier-neutral sites that offer direct cloud on-ramps and rich interconnection. Cloud and virtual data center services, however, are forecast to expand at a 16.94% CAGR, supported by organizations that prefer operational expenditure and elastic scaling. Colocation retains appeal for latency-sensitive workloads and compliance-driven deployments, sustaining steady contracts even as cloud uptake accelerates. Managed hosting stabilizes as mid-market enterprises offload routine infrastructure tasks, while disaster recovery and backup enjoy niche growth amid stricter data-protection mandates.

Data center infrastructure management tools have become essential across all service types, providing real-time insight into power, cooling, and asset utilization. Professional and consulting services deepen client relationships by guiding migration roadmaps and regulatory audits. Service portfolios therefore evolve from single-rack leasing to integrated suites that blend physical footprint, virtual machines, and advisory support. This composite approach anchors customer stickiness and keeps the data center service market positioned for multi-year expansion.

Tier III facilities accounted for 54.73% of the data center service market share in 2025, striking a pragmatic middle ground between cost efficiency and fault tolerance. They host mainstream corporate workloads that tolerate minimal downtime yet avoid Tier IV premiums. Tier IV sites, targeting financial trading and critical healthcare systems, are expected to post a 16.02% CAGR as zero-interrupt architectures gain favor. Tier I and Tier II facilities lose share except for test labs and archival storage.

Operators are segmenting campuses by tier, enabling clients to align application resilience with budget. Liquid cooling is filtering into Tier III halls to accommodate AI clusters without upgrading the entire site to Tier IV. This modular tiering maximizes utilization and broadens the appeal of mixed-tier campuses, reinforcing market diversity while offering customers granular cost-performance trade-offs.

The Data Center Service Market Report is Segmented Type of Service (Managed Hosting Service, Colocation Service and More), Tier Standard (Tier I and II, Tier IV and More), End-User Industry (BFSI, Healthcare and More), Deployment Model (On-Premise Data Centers, Hyperscale and More), and Geography (North America, Asia-Pacific and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the largest portion of the data center service market in 2025, buoyed by hyperscale investments like Microsoft and BlackRock's USD 30 billion AI-infrastructure program. Established connectivity hubs, abundant capital, and mature regulatory frameworks sustain regional leadership. Challenges arise from water-use restrictions in the southwest, spurring adoption of liquid or dry-cooling solutions. Canada offers renewably powered alternatives, attracting AI training clusters that demand continuous megawatt loads.

Asia-Pacific recorded the fastest growth, driven by widespread digitization and sovereign data policies. Oracle's USD 8 billion sovereign cloud build in Japan and NTT's USD 1.5 billion expansion in India underscore the region's momentum. China emphasizes domestic processing for security reasons, favoring local providers. India benefits from government payment systems and biometric identity programs that necessitate compute at scale, while Southeast Asia positions itself as a bridge between global enterprises and local consumers.

Europe's trajectory is influenced by GDPR and escalating sustainability mandates. Operators must navigate fragmented national regulations while meeting renewable-energy quotas, creating scope for specialized compliance hosting. Middle East and Africa emerge as new frontiers, with the UAE, Saudi Arabia, and Kenya unveiling large-scale projects like the USD 544 million Microsoft-du facility and geothermal-powered campuses. Strategic positioning between continents enables these markets to serve as inter-regional hubs, further broadening the geographical footprint of the data center service market.

- Equinix Inc.

- Digital Realty Trust Inc.

- Amazon Web Services (AWS)

- Microsoft Corporation (Azure)

- Google LLC (Google Cloud)

- Alibaba Cloud

- Tencent Cloud

- IBM Corporation

- Fujitsu Limited

- NTT Communications

- Hewlett Packard Enterprise Company

- Dell Inc.

- Cisco Systems Inc.

- Vertiv Co.

- Singapore Telecommunications Limited (Singtel)

- Iron Mountain Inc.

- Cyxtera Technologies

- CoreSite Realty Corporation

- Capgemini SE

- Kyndryl Holdings Inc.

- Rackspace Technology

- OVHcloud

- ATandT Inc.

- Switch Inc.

- EdgeConneX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Expenditure on Data Center Technology

- 4.2.2 Rising Data Center Complexities Due to Scalability

- 4.2.3 Surge in Cloud and Hyperscale Expansion

- 4.2.4 Data-Sovereignty Regulations Driving Local Facilities

- 4.2.5 Liquid Cooling Adoption Enabling Higher Rack Densities

- 4.2.6 AI-Driven Workload Orchestration and Optimization

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Security Concerns

- 4.3.2 Skilled Workforce Shortage in Advanced Operations

- 4.3.3 Water-Usage Restrictions for Cooling

- 4.3.4 Supply-Chain Bottlenecks for High-Power Components

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Investment and Fund-Raising Trends

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Type of Service

- 5.1.1 Managed Hosting Service

- 5.1.2 Colocation Service

- 5.1.3 Cloud / Virtual Data Center Services

- 5.1.4 Disaster Recovery and Backup Services

- 5.1.5 Data Center Infrastructure Management (DCIM) Services

- 5.1.6 Professional and Consulting Services

- 5.2 By Tier Standard

- 5.2.1 Tier I and II

- 5.2.2 Tier III

- 5.2.3 Tier IV

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 Retail and E-commerce

- 5.3.4 Manufacturing

- 5.3.5 IT and Telecom

- 5.3.6 Government and Public Sector

- 5.3.7 Media and Entertainment

- 5.3.8 Others

- 5.4 By Deployment Model

- 5.4.1 On-Premise Facilities

- 5.4.2 Colocation Facilities

- 5.4.3 Hyperscale/Self-built Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacifc

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacifc

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Equinix Inc.

- 6.2.2 Digital Realty Trust Inc.

- 6.2.3 Amazon Web Services (AWS)

- 6.2.4 Microsoft Corporation (Azure)

- 6.2.5 Google LLC (Google Cloud)

- 6.2.6 Alibaba Cloud

- 6.2.7 Tencent Cloud

- 6.2.8 IBM Corporation

- 6.2.9 Fujitsu Limited

- 6.2.10 NTT Communications

- 6.2.11 Hewlett Packard Enterprise Company

- 6.2.12 Dell Inc.

- 6.2.13 Cisco Systems Inc.

- 6.2.14 Vertiv Co.

- 6.2.15 Singapore Telecommunications Limited (Singtel)

- 6.2.16 Iron Mountain Inc.

- 6.2.17 Cyxtera Technologies

- 6.2.18 CoreSite Realty Corporation

- 6.2.19 Capgemini SE

- 6.2.20 Kyndryl Holdings Inc.

- 6.2.21 Rackspace Technology

- 6.2.22 OVHcloud

- 6.2.23 ATandT Inc.

- 6.2.24 Switch Inc.

- 6.2.25 EdgeConneX

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment