|

시장보고서

상품코드

2035078

위탁연구기관 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Contract Research Organization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

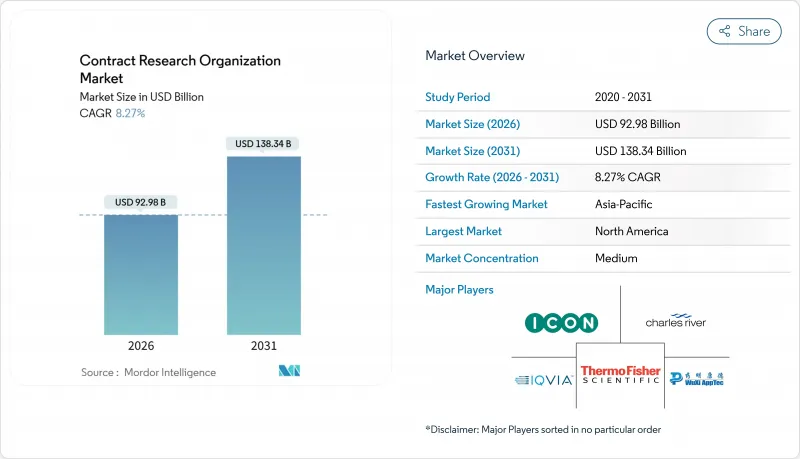

위탁연구기관(CRO) 시장 규모는 2026년에 929억 8,000만 달러로 추계되며 예측 기간(2026-2031년)에 CAGR 8.27%로 성장을 지속하여, 2031년까지 1,383억 4,000만 달러에 이를 전망입니다.

수익 확대는 개발 주기 단축, 전 세계 환자 접근성 확보, 점점 더 복잡해지는 규제 프로세스 준수에 대한 스폰서들의 요구가 증가함에 따라 주도되고 있습니다. 생물학적 제제 및 세포-유전자 치료에 대한 투자로 인해 임상시험 포트폴리오는 스폰서가 거의 없는 고도로 복잡한 프로토콜로 전환되고 있습니다. 규제 당국은 계속해서 신속 심사 지정을 부여하고 있으며, 이는 심사 기간을 단축하고 중요한 기능의 아웃소싱을 더욱 촉진하고 있습니다. 초기 단계의 생명공학 기업에 대한 벤처 캐피탈의 유입은 초기 임상시험에 대한 전문 지식에 대한 수요를 뒷받침하고 있으며, 기술을 활용한 임상시험기관 선정 도구는 임상 시작까지의 기간을 단축하고 스크리닝 실패율을 낮추고 있습니다.

세계 CRO 시장 동향 및 인사이트

바이오 의약품 및 첨단 치료법 개발 건수 증가

바이오의약품 및 세포-유전자치료제 파이프라인은 바이러스 벡터 제조, 체외 세포 조작, 장기적인 환자 모니터링이 필요하지만, 이를 자체적으로 보유하고 있는 스폰서는 거의 없습니다. FDA의 '재생의학 첨단치료제(Regenerative Medicine Advanced Therapy)' 지정은 제품 적격성 심사를 신속히 처리하고, 적응형 설계와 분산형 샘플 물류를 관리할 수 있는 CRO에 이점을 제공합니다. 새로운 CMC 가이드라인은 IND 신청의 불확실성을 줄이고, 저분자 의약품 포트폴리오에서 바이오 의약품으로 자본을 재분배하고 있습니다. 바이오시밀러가 기존 제품의 수익을 압박하는 가운데, 스폰서들은 장기적인 유전자 편집 임상시험에 필요한 고도로 전문화된 인프라를 제공하기 위해 CRO 파트너에 의존하고 있습니다.

신흥 시장에서의 환자 풀 및 임상시험 시설 확대

중국의 다지역 임상시험 프레임워크는 현재 해외 데이터를 승인하고 있으며, 다국적 프로그램의 임상시험 시설 설립을 가속화하고 있습니다. 인도 중앙의약품표준관리기구(CDSCO)는 심사 주기를 단축하고, 치료 경험이 없는 환자 코호트를 원하는 종양학 및 대사성 질환 스폰서를 유치하고 있습니다. 브라질의 ANVISA는 ICH E6(R2)를 준수하여 행정적 마찰을 줄이고 라틴아메리카의 피험자 등록을 촉진하고 있습니다. 이들 지역의 광범위한 인구 구성은 신속한 피험자 등록을 가능하게 하고, 인종적으로 다양한 데이터 세트를 통해 규제 당국에 제출할 수 있도록 도와줍니다.

품질 감사 및 컴플라이언스 위반에 대한 처벌 강화

FDA는 임상시험 실시기준(GCP)을 철저히 준수하기 위해 임상시험 책임자, IRB, 임상시험 의뢰자를 검사하고 있으며, 이로 인해 CRO는 모니터링, 전자 감사 추적 및 제3자 검증에 더 많은 예산을 배정해야 합니다. EMA의 임상시험 정보시스템은 투명성을 높여 평판 리스크를 낮추기 위해 노력하고 있습니다. 컴플라이언스 비용이 상승하는 가운데, 소규모 제공업체들은 수익률 압박과 통합의 위험에 직면해 있습니다.

부문 분석

CRO 시장에서 가장 빠르게 성장하는 분야인 초기 단계 개발 서비스는 2031년까지 연평균 10.72%의 성장률을 보일 것으로 예측됩니다. 금액 기준으로 볼 때, CRO 시장 규모에서 이 부문이 차지하는 비중은 바이오테크 기업 스폰서들이 빠른 개념증명(PoC) 프로그램을 우선시함에 따라 증가할 것으로 예측됩니다. 임상연구서비스는 여전히 지배적인 지위를 유지하며 2025년 매출 점유율의 61.45%를 차지할 것으로 예상됐지만, 조달 심사의 강화로 인해 가격 상승이 억제되고 있습니다. 임상 1상 부문은 전용 시설, 숙련된 의료 모니터 요원 및 학술 기관에 대한 즉각적인 접근성을 갖추고 있으며, 이를 통해 첫 임상시험의 리스크를 줄일 수 있어 프리미엄 요금이 책정될 수 있습니다. 2단계 및 3단계 업무는 전자 데이터 수집(EDC)의 보급으로 차별화가 사라지고 상품화가 진행되고 있습니다. 한편, 검사 서비스는 정밀의학에 대한 수요에 따라 꾸준히 성장하고 있으며, 컨설팅 서비스는 복잡한 규제 전략에 대한 틈새 수요를 유지하고 있습니다.

스폰서들은 바이오마커 선별 코호트 도입을 확대하고 있으며, 이로 인해 피험자 수는 줄어들지만 분석의 복잡성은 증가하고 있습니다. 규제 당국이 승인 후 안전성 데이터 제출을 요구하면서 4상 감시가 점차 확대되고 있지만, 많은 대형 스폰서들은 실제 데이터에 대한 통제권을 유지하기 위해 이러한 연구를 자체적으로 수행하고 있습니다. 차별화의 초점은 기술 플랫폼, 적응형 설계에 대한 전문 지식, 분산형 테스트 요소의 원활한 통합으로 옮겨가고 있습니다. 이러한 양극화로 인해 초기 단계의 활동은 프리미엄 가격을 유지할 수 있는 반면, 성숙한 서비스는 운영 규모에 따라 경쟁하게 됩니다.

종양학은 면역치료, 표적 저분자 약물, 세포치료제 등 1,000개 이상의 진행 중인 임상 자산의 수혜를 받아 2025년 21.43%로 치료 분야 중 가장 큰 수익을 창출했습니다. 한편, 감염병 분야는 팬데믹 대응 투자 및 mRNA 백신 플랫폼에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 10.81%로 가장 빠른 성장세를 보이고 있습니다. 중추신경계 및 면역학 분야도 주관적인 평가의 필요성을 줄여주는 디지털 바이오마커의 보급에 힘입어 각각 많은 투자를 유치하고 있습니다. 심혈관계 및 호흡기 분야는 제네릭 의약품 시장 잠식으로 인해 희귀질환으로 R&D 자금이 이동하면서 후발주자로 밀려나고 있습니다.

항균제 개발에 대한 정부의 인센티브와 새롭게 개편된 백신 파이프라인이 감염병 분야의 모멘텀을 뒷받침하고 있습니다. 종양학 분야의 둔화는 쇠퇴가 아니라 성숙의 신호입니다. 이미 시판되고 있는 체크포인트 억제제는 후기 임상에서 시판 후 활동으로 전환되고 있습니다. 중추신경계(CNS) 프로그램은 여전히 높은 스크리닝 실패율과 장기간의 추적관찰 기간에 직면해 있으며, 신경학 전문가와 탄탄한 임상연구자 네트워크를 보유한 CRO와의 협력이 필수적입니다. 희귀질환의 식별은 여전히 병목현상으로 남아있으며, 자체 환자 등록 데이터베이스를 보유한 CRO가 경쟁 우위를 점할 수 있습니다.

본 'CRO(위탁연구기관) 시장 보고서'는 서비스 유형(초기단계 개발 등), 치료영역(종양학, 감염질환 등), 최종 사용자(제약/바이오의약품, 의료기기, 기타), 제공모델(풀서비스, FSP, 하이브리드), 지역(북미, 유럽, 아시아, 아시아태평양, 중동, 아프리카, 남미) 별로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

북미는 2025년 매출의 38.92%를 차지했고, 미국 내 35만 개의 연구 인프라와 FDA의 세계 규제 영향력이 그 기반이 되고 있습니다. 스폰서들이 비용 절감과 다양한 환자층에 대한 접근을 위해 다각화를 추진하는 가운데, 성장률은 CRO 시장 평균을 밑돌고 있습니다. 캐나다와 멕시코는 신속한 윤리 심사 승인을 통해 심혈관 질환 및 당뇨병 코호트를 제공하고 있으며, 미국의 학술 연구 기관은 복잡한 종양학 및 유전자 치료 프로토콜을 유지하고 있습니다.

아시아태평양은 규제 현대화와 치료 경험이 없는 방대한 환자층에 힘입어 2031년까지 연평균 11.26%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, CRO 시장에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 중국에서는 IND 심사의 효율화와 다국가의 임상시험(MRCT)의 외국 데이터 승인으로 세계 프로그램 참여가 촉진되고 있습니다. 인도에서는 심사 주기의 단축으로 종양학 분야의 피험자 등록이 가속화되고 있으며, 일본에서는 ICH 준수를 통해 다국가 신청이 용이해졌습니다. 호주는 연구개발 세액공제 및 신속한 윤리심사를 활용하여 인체적용시험 유치에 주력하고 있습니다. 한국은 세포치료 인프라에 많은 투자를 하고 있으며, 첨단 치료법의 임상시험이 증가하고 있습니다.

유럽은 EMA(유럽의약품청)의 임상시험 정보 시스템을 통한 승인 조정을 통해 성숙한 임상 3상 시험 수행 능력을 유지하고 있습니다. 독일, 영국, 프랑스가 여전히 핵심 거점이지만, 브렉시트로 인해 현재 영국을 위한 병렬 프로토콜이 필요하게 되었습니다. 스페인과 이탈리아는 상대적 비용 우위를 가지고 있으며, 호흡기 및 순환기 계통의 임상시험을 점진적으로 획득하고 있습니다. 중동 및 아프리카는 규모는 작지만, 걸프 지역 국가들이 연구 다각화에 투자하면서 희귀질환 및 백신 임상시험을 수용하고 있습니다. 한편, 남미에서는 브라질과 아르헨티나를 중심으로 규제 조화가 진행되면서 감염병 조사 분야에서 존재감을 높이고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Contract Research Organization Market size is estimated at USD 92.98 billion in 2026, and is expected to reach USD 138.34 billion by 2031, at a CAGR of 8.27% during the forecast period (2026-2031).

Revenue expansion is driven by sponsors' increasing need to compress development cycles, secure global patient access, and comply with increasingly complex regulatory pathways. Investment in biologics and cell- and gene-therapies is shifting trial portfolios toward high-complexity protocols that few sponsors can execute in-house. Regulatory agencies continue to award expedited designations, which shorten review times and further encourage the outsourcing of critical functions. Venture capital inflows into early-stage biotechs sustain demand for first-in-human expertise, while technology-enabled site selection tools shorten startup timelines and lower screening failure rates.

Global Contract Research Organization Market Trends and Insights

Rising Volume of Biologics and Advanced Therapies Development

Biologics and cell- and gene-therapy pipelines require viral-vector production, ex vivo cell manipulation, and long-term patient monitoring, which most sponsors lack internally. The FDA's Regenerative Medicine Advanced Therapy designation expedites the qualification of products, rewarding CROs that can manage adaptive designs and decentralized sample logistics. New CMC guidelines have reduced IND uncertainties, prompting a reallocation of capital from small-molecule portfolios toward biologics. As biosimilars pressure legacy revenues, sponsors lean on CRO partners to supply the highly specialized infrastructure needed for durable gene-editing trials.

Expansion of Emerging Market Patient Pools and Investigator Sites

China's multi-regional clinical trial framework now accepts foreign data, accelerating site initiation for multinational programs. India's Central Drugs Standard Control Organisation has shortened review cycles, drawing oncology and metabolic sponsors seeking treatment-naive cohorts. Brazil's ANVISA aligned with ICH E6(R2), reducing administrative friction and promoting Latin American enrollment. The demographic breadth in these regions offers rapid accrual and strengthens regulatory submissions through ethnically diverse datasets.

Intensifying Quality Audits and Compliance Penalties

The FDA inspects investigators, IRBs, and sponsors to enforce Good Clinical Practice, pushing CROs to allocate larger budgets to monitoring, electronic audit trails, and third-party verification. The EMA's Clinical Trials Information System increases transparency, thereby raising the reputational stakes. Smaller providers face margin pressure and consolidation risk as compliance costs climb.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Regulatory Pathways for Orphan and Fast-Track Drugs

- Growing Venture Capital Funding for Early-Stage Biotech Firms

- High Capital Expenditure for Cutting-Edge Lab Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Early-phase development services, representing the fastest-growing segment of the Contract Research Organization market, are forecast to increase at a 10.72% annual rate through 2031. In value terms, this segment will account for a rising portion of the Contract Research Organization market size as biotech sponsors prioritize rapid proof-of-concept programs. Clinical Research Services remained dominant, with a 61.45% revenue share in 2025; however, heightened procurement scrutiny limits price escalation. Phase I units command premium rates because they have dedicated facilities, experienced medical monitors, and immediate access to academic centers, which mitigate the first-in-human risk. Phase II and Phase III work face commoditization as electronic data capture narrows differentiation. Laboratory Services grow steadily in response to the demand for precision medicine, while Consulting Services retain a niche appeal for complex regulatory strategies.

Sponsors are increasingly deploying biomarker-selected cohorts, which reduces enrollment numbers but increases analytical complexity. Phase IV surveillance expands modestly as agencies request post-approval safety evidence, yet many large sponsors internalize these studies to maintain control over real-world data. Differentiation shifts toward technology platforms, adaptive design expertise, and the seamless integration of decentralized trial components. This bifurcation keeps premium pricing in early-phase activities while mature services compete on operational scale.

Oncology generated the most considerable therapeutic-area revenue, at 21.43% in 2025, benefiting from over 1,000 active clinical assets that encompassed immunotherapies, targeted small molecules, and cell therapies. Infectious Diseases, however, exhibits the fastest expansion at 10.81% CAGR through 2031, reflecting pandemic-preparedness investment and mRNA vaccine platforms. Central Nervous System and Immunology each draw sizable spending, aided by the acceptance of digital biomarkers that reduce the need for subjective evaluations. Cardiovascular and Respiratory categories trail as generic erosion shifts R&D funding toward orphan conditions.

Government incentives for antimicrobial development, along with renewed vaccine pipelines, underpin infectious-disease momentum. Oncology's deceleration represents maturity rather than decline: commercialized checkpoint inhibitors transition activity from late-stage trials to post-marketing commitments. CNS programs still confront high screen-failure rates and lengthy follow-up periods, necessitating collaborations with CROs that include neurology specialists and robust investigator networks. Rare-disease identification remains a bottleneck, granting CROs with proprietary registries a competitive edge.

The Contract Research Organization Market Report is Segmented by Service Type (Early-Phase Development, and More), Therapeutic Area (Oncology, Infectious Diseases, and More), End User (Pharmaceutical & Biopharmaceutical, Medical Device, and Other), Delivery Model (Full-Service, FSP, and Hybrid), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). Market Forecasts are Provided in Value (USD).

Geography Analysis

North America contributed 38.92% revenue in 2025, anchored by the United States' 350,000-site research infrastructure and the FDA's global regulatory influence. Growth lags the Contract Research Organization market average as sponsors diversify to contain costs and access varied patient pools. Canada and Mexico supply cardiovascular and diabetes cohorts through swift ethics approvals, while U.S. academic centers sustain complex oncology and gene-therapy protocols.

The Asia-Pacific region is poised for an 11.26% CAGR to 2031, the Contract Research Organization market's fastest regional trajectory, driven by regulatory modernization and vast treatment-naive populations. China's streamlined IND reviews and acceptance of foreign data under MRCT promote inclusion in global programs. India accelerates oncology enrollment via shortened review cycles, and Japan's ICH alignment eases multinational submissions. Australia leverages R&D tax offsets and rapid ethics reviews to attract first-in-human studies. South Korea invests heavily in cell-therapy infrastructure, leading to an increase in advanced-therapy trials.

Europe maintains mature Phase III capacity with harmonized approvals via the EMA's Clinical Trials Information System. Germany, the United Kingdom, and France remain core hubs, although Brexit now requires parallel UK protocols. Spain and Italy offer relative cost advantages and are capturing incremental respiratory and cardiovascular studies. The Middle East and Africa remain small but are receiving rare-disease and vaccine trials as Gulf states invest in research diversification. Meanwhile, South America, led by Brazil and Argentina, is gaining ground in infectious-disease research amid regulatory harmonization.

- BioAgile Therapeutics Private Limited

- Charles River

- CRITERIUM, INC.

- Evotec

- Eurofins

- Fortrea

- ICON

- IQVIA

- Inotiv

- MedPace

- Parexel International (MA) Corporation

- Pharmaron

- PSI

- SGS

- Syneos Health

- Syngene International

- Thermo Fisher Scientific

- Tigermed

- Worldwide Clinical Trials

- WuXi AppTec (WuXi Clinical)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume of Biologics and Advanced Therapies Development

- 4.2.2 Expansion of Emerging Market Patient Pools and Investigator Sites

- 4.2.3 Accelerated Regulatory Pathways for Orphan and Fast-Track Drugs

- 4.2.4 Growing Venture Capital Funding for Early-Stage Biotech Firms

- 4.2.5 Adoption of Decentralized/Hybrid Clinical Trial Architectures

- 4.2.6 Integration of Real-World Evidence and Digital Biomarkers to Shorten Timelines

- 4.3 Market Restraints

- 4.3.1 Intensifying Quality Audits and Compliance Penalties

- 4.3.2 High Capital Expenditure for Cutting-Edge Lab Automation

- 4.3.3 Rising Geopolitical Risks Affecting Cross-Border Trials

- 4.3.4 Scarcity of GMP-Grade Viral Vector Manufacturing Capacity

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Suppliers

- 4.5.3 Bargaining Power Of Buyers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Early-Phase Development Services

- 5.1.2 Clinical Research Services

- 5.1.2.1 Phase I

- 5.1.2.2 Phase II

- 5.1.2.3 Phase III

- 5.1.2.4 Phase IV

- 5.1.3 Laboratory Services

- 5.1.4 Consulting Services

- 5.2 By Therapeutic Area

- 5.2.1 Oncology

- 5.2.2 Infectious Diseases

- 5.2.3 Central Nervous System (CNS) Disorders

- 5.2.4 Immunological Disorders

- 5.2.5 Cardiovascular Diseases

- 5.2.6 Respiratory Disorders

- 5.2.7 Diabetes

- 5.2.8 Other Therapeutic Areas

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biopharmaceutical Companies

- 5.3.2 Medical Device Companies

- 5.3.3 Other End Users (Academic / Government Institutes)

- 5.4 By Delivery Model

- 5.4.1 Full-Service / Integrated CRO

- 5.4.2 Functional Service Provider (FSP)

- 5.4.3 Hybrid / Modular Model

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest Of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest Of Asia-Pacific

- 5.5.4 Middle East And Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest Of Middle East And Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest Of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 BioAgile Therapeutics Private Limited

- 6.3.2 Charles River Laboratories

- 6.3.3 CRITERIUM, INC.

- 6.3.4 Evotec SE

- 6.3.5 Eurofins Scientific

- 6.3.6 Fortrea

- 6.3.7 ICON Plc

- 6.3.8 IQVIA Holdings Inc.

- 6.3.9 Inotiv

- 6.3.10 Medpace, Inc.

- 6.3.11 Parexel International (MA) Corporation

- 6.3.12 Pharmaron

- 6.3.13 PSI

- 6.3.14 SGS S.A.

- 6.3.15 Syneos Health

- 6.3.16 Syngene International Limited

- 6.3.17 Thermo Fisher Scientific Inc. (PPD Inc.)

- 6.3.18 Tigermed

- 6.3.19 Worldwide Clinical Trials

- 6.3.20 WuXi AppTec (WuXi Clinical)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment