|

시장보고서

상품코드

2035079

UV 경화형 인쇄 잉크 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)UV Cured Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

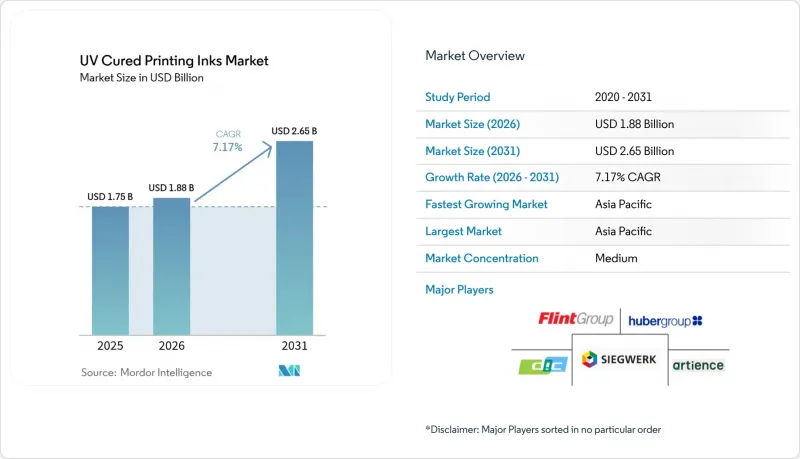

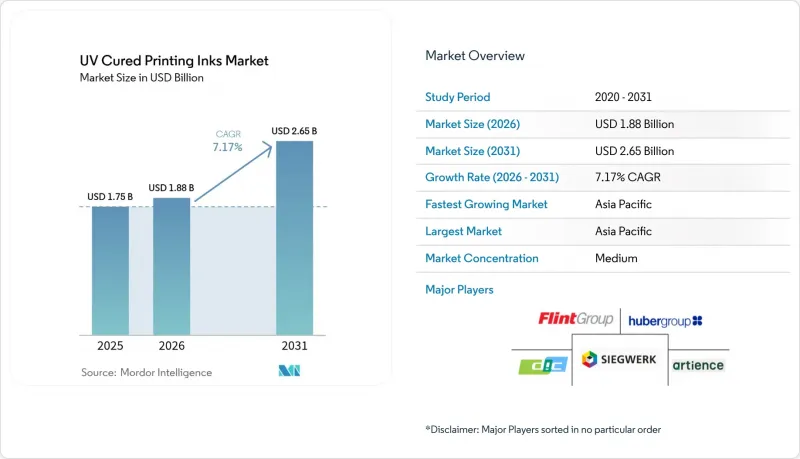

UV 경화형 인쇄 잉크 시장 규모는 2025년에 17억 5,000만 달러로 평가되었고 2026년 18억 8,000만 달러에서 2031년까지 26억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.17%를 나타낼 전망입니다.

수은 램프의 유지보수 및 VOC(휘발성 유기화합물) 배출을 없애고, 인쇄기의 소비전력을 60-65% 절감하는 에너지 절약형 LED 경화기술이 주요 성장 요인으로 작용하고 있습니다. 아시아태평양, 유럽연합(EU) 및 북미에서 식품 접촉에 대한 규제가 강화됨에 따라, 포장 컨버터 업체들은 이러한 요건을 충족시키기 위해 저전이성 잉크의 도입을 가속화하고 있습니다. OEM 업체들이 새로운 설비 투자 없이도 인쇄기 속도를 30-50% 향상시킬 수 있는 리트로핏용 LED 시스템을 출시함에 따라, 대상 기설치 설비의 저변이 확대되고 진입장벽이 낮아지고 있습니다. 동시에 광개시제 공급 위험과 수성 잉크 및 전자빔(EB) 경화형 잉크와 같은 대체 기술의 부상으로 인해 경쟁 압력이 발생하고 있으며, 공급업체는 혁신과 조달 체계의 유연성을 통해 이를 해결해야 합니다.

세계 UV 경화형 인쇄 잉크 시장 동향 및 인사이트

디지털 인쇄 및 잉크젯 인쇄 수요 증가

주문형 인쇄의 도입으로 출판사는 창고 보관 비용을 크게 절감하고 빠른 납기에 대한 기대에 부응할 수 있습니다. 또한, UV 경화형 잉크는 인쇄 후 건조 대기 시간 없이 코팅지 및 비코팅지 기판에 선명한 이미지를 구현할 수 있습니다. 브랜드가 디지털 캠페인에 촉각적 요소를 도입함에 따라 직접 메일의 취급량이 회복되고 있으며, 우편물 취급에 견딜 수 있고 내구성이 뛰어나며 마찰에 강한 UV 인쇄물에 대한 수요가 증가하고 있습니다. 후지필름의 특허는 계면활성제 개질 잉크젯 배합에 대한 연구 개발의 기세를 반영하여 색 간 번짐을 줄이고 광택의 균일성을 높이며, 고속 피에조 헤드와의 UV 호환성을 강화하는 기술입니다. Web-to-Print의 스토어 프론트를 도입한 상업용 인쇄업체들은 즉시 경화를 통해 작업 대기 시간을 단축할 수 있는 단발성, 개인화된 소량 주문 물량을 처리하고 있습니다. 전통적인 출판물의 발행 부수는 계속 줄어들고 있지만, 가변 데이터와 특수 소재로의 가치 전환은 UV 경화형 인쇄 잉크 시장의 성장에 긍정적인 견인차 역할을 하고 있습니다.

패키지 및 라벨 컨버터 확대

인도네시아, 인도, 베트남에서는 지역 내 FMCG(일용소비재) 수요 증가와 세계 브랜드공급망 니어쇼어링(Near-shoring)에 따라 컨버터 생산 능력이 확대되고 있습니다. 신규 인쇄 라인은 일반적으로 LED UV 또는 하이브리드 경화 방식을 채택하여 설치 시 낭비를 줄이고 공장의 ESG 표준을 충족합니다. 미라크론의 FLEXCEL NX 플랫폼으로 대표되는 플 렉소 인쇄기의 업그레이드를 통해 컨버터는 그라비아 인쇄와 동등한 미관을 구현하면서 UV 잉크 배합에 적합한 얇은 판과 낮은 잉크 도포량을 사용할 수 있게 됩니다. 브랜드 오너의 지속가능성 평가에서 UV LED 경화를 통한 에너지 절감 효과가 점점 더 중요해지면서 컨버터 업체들의 기술 혁신을 촉구하고 있습니다. 식품 접촉 규제 대응과 총소유비용(TCO) 절감이라는 두 가지 요구는 UV 경화형 인쇄 잉크 시장에서 포장 분야 수요를 확고히 하고 있습니다.

전통적인 상업 인쇄의 쇠퇴

광고주들이 예산을 디지털 플랫폼으로 전환함에 따라 신문과 잡지의 발행 부수는 지속적으로 감소하여 전통적인 UV 오프셋 잉크에 대한 수요를 약화시키고 있습니다. 포장, 라벨 또는 고부가가치 장식 인쇄로 전환하지 못한 상업용 인쇄 업체는 인쇄기 가동률 감소에 직면하여 잉크 소비가 직접적으로 감소합니다. 고수익률의 단납기, 소량 인쇄가 수익 감소를 완화하고 있지만, 인쇄량 감소는 계속되고 있으며, 이 억제요인은 구조적인 역풍으로 작용하고 있습니다.

부문 분석

LED 시스템은 2025년 UV 경화형 인쇄 잉크 시장 규모의 56.14%를 차지하고 2031년까지 연평균 복합 성장률(CAGR) 9.13%를 나타낼 것으로 예측됩니다. 이는 에너지 효율을 중시하는 컨버터들 사이에서 이 기술이 널리 받아들여지고 있음을 보여줍니다. 레트로핏(Retrofit) 옵션을 통해 설비 투자 장벽을 낮추고, 운영자는 기존 인쇄기 플랫폼을 유지하면서 다운타임을 크게 줄일 수 있습니다. 스택 온도를 낮추면 박막의 시트 왜곡이 해소되고 더 높은 닙 압력이 가능하여 18,000 sph 이상의 인쇄 속도에서도 조준 정확도를 유지할 수 있습니다. 이러한 특성이 결합되어 UV 경화형 인쇄 잉크 시장에서 LED의 선도적 지위를 뒷받침하고 있습니다.

아크 램프에 의한 경화는 양이온 광화학 반응을 일으키기 위해 광대역 스펙트럼이 필요한 특정 와이드 웹 및 스크린 인쇄 응용 분야에서 여전히 일정한 지위를 유지하고 있습니다. 그러나 최근 25W/cm2에 이르는 고출력 LED 다이오드로 인해 경화 깊이의 전통적인 차이가 줄어들고 있으며, 하이브리드 램프 하우징을 통해 사용자가 교대 근무 중에도 모드를 전환할 수 있기 때문에 전환 속도가 빨라지고 있습니다. 수은에 대한 정부 규제가 강화됨에 따라 아크 램프의 경제성은 더욱 낮아지고 LED의 우위는 더욱 강화될 것입니다.

"UV 경화형 인쇄 잉크 시장 보고서는 경화 공정(아크 경화 및 LED 경화), 잉크 유형(UV 플 렉소 잉크, UV 오프셋 잉크, UV 저에너지/LED 오프셋 잉크 등), 용도(포장, 상업/출판, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류되어 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

아시아태평양은 2025년 매출의 48.05%를 차지하고, 2031년까지 연평균 복합 성장률(CAGR) 9.08%를 나타낼 것으로 예측됩니다. 이는 중국의 전국적인 GB 4806.14-2023 준수 기한과 식품 포장용 잉크에 톨루엔 사용을 제한하는 인도 IS:15495의 시행에 의해 주도되고 있습니다. UFlex와 같은 지역 대기업들은 금속화 필름에 폴리에스테르 아크릴레이트를 접착하는 방식을 도입하여 컨버터가 한 번의 공정으로 배리어성과 전이성 두 가지 목표를 모두 달성할 수 있게 되었습니다. 에너지 절약 장비 비용의 최대 30%를 환급해주는 정부 인센티브는 새로운 그라비아 및 플 렉소 인쇄 공장의 LED UV 도입을 더욱 가속화하여 UV 경화형 인쇄 잉크 시장에서 이 지역의 견인력을 더욱 공고히 하고 있습니다.

북미는 기술 기반이 잘 갖춰진 지역으로, 일찍이 2016년부터 LED 장비를 도입한 기업이 많았습니다. 미국 환경보호청(EPA)의 권고와 인플레이션 감소법(Inflation Reduction Act)의 청정 제조 크레딧을 통해 2024년부터 2025년까지 수많은 설비 교체에 대한 자금 지원이 이루어졌습니다. 루브리졸사가 오하이오주에서 Solsperse 고분산제 생산량을 두 배로 늘린 사례에서 볼 수 있듯이, 수지 및 첨가제 생산능력 확대는 국내 잉크 제조업체에 대한 공급 안정화를 촉진하고 있습니다.

중동, 아프리카 및 남미는 현재 판매량 점유율이 낮지만, 수출 고객의 감사에 대응하기 위해 포장 가공 업체가 솔벤트 기반 라인에서 LED 플랫폼으로 전환함에 따라 잠재적인 성장 여지가 있습니다. 하이브리드 UV-EB 플렉소라인을 도입하고 있는 브라질 라벨 인쇄업체들의 동향은 거시 경제 상황이 안정되면 도입 일정을 단축할 수 있는 새로운 기술의 비약적인 발전을 뒷받침하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The UV Cured Printing Inks Market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.88 billion in 2026 to reach USD 2.65 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031).

Energy-efficient LED curing, which lowers press power consumption by 60-65% while removing mercury lamp maintenance and VOC emissions, is the primary growth driver. Packaging converters are accelerating adoption because low-migration formulations meet tightening food-contact rules in Asia-Pacific, the European Union, and North America. As OEMs release retrofit LED systems that raise press speeds 30-50% without new capital outlay, the addressable installed base widens and barriers to entry fall. At the same time, photoinitiator supply risks and emerging water-based or EB-curable alternatives inject competitive pressure that suppliers must manage through innovation and sourcing agility.

Global UV Cured Printing Inks Market Trends and Insights

Growing Demand from Digital and Inkjet Printing

Print-on-demand adoption lets publishers slash warehousing expenses and meet rapid turnaround expectations, and UV-cured inks enable crisp imagery on coated and uncoated substrates without post-press drying delays. Direct mail volumes are rebounding as brands integrate tactile pieces with digital campaigns, reinforcing demand for durable, scuff-resistant UV impressions that withstand postal handling. Research and development momentum is visible in FUJIFILM's patent covering surfactant-modified inkjet formulations that reduce inter-color bleeding and heighten gloss uniformity, an advance that strengthens UV compatibility with high-speed piezo heads. Commercial shops that add web-to-print storefronts tap short-run personalized jobs where instant curing shortens job queues. Although legacy publication volumes keep shrinking, the value shift to variable-data and specialty substrates produces a net positive pull on UV-cured printing inks market growth.

Expansion of Packaging and Label Converters

Converter capacity is rising across Indonesia, India, and Vietnam as regional FMCG demand climbs and global brands nearshore supply chains; each new press line typically specifies LED UV or hybrid curing to cut make-ready waste and satisfy factory ESG benchmarks. Flexographic press upgrades, exemplified by Miraclon's FLEXCEL NX platform, let converters match gravure aesthetics while using thinner plates and lower ink laydowns that suit UV formulations. Brand-owner sustainability scorecards increasingly credit energy savings from UV LED curing, nudging converters toward technology refresh. The dual need to meet food-contact rules and lower total cost of ownership cements packaging's pull on the UV-cured printing inks market.

Decline of Conventional Commercial Printing

Newspaper and magazine pagination keeps sliding as advertisers channel budgets into digital platforms, eroding legacy UV offset ink demand. Commercial printers that fail to pivot toward packaging, labels, or value-added embellishments face press under-utilization that directly reduces ink consumption. While high-margin short runs temper revenue loss, volume attrition persists, marking this restraint as a structural headwind.

Other drivers and restraints analyzed in the detailed report include:

- Stricter VOC/Sustainability Regulations

- Rapid Shift to Energy-Efficient LED UV Systems

- Competition from Water-Based and EB-Curable Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED systems accounted for 56.14% of the UV-cured printing inks market size in 2025 and are forecast to post a 9.13% CAGR to 2031, underlining the technology's broad acceptance among converters focused on energy metrics. The retrofit option lowers capital hurdles, letting operators preserve existing press platforms while sharply reducing downtime. Lower stack temperatures eliminate sheet distortion on thin films and enable higher nip pressures that maintain registration accuracy at press speeds above 18,000 sph. These attributes collectively sustain LED's leadership in the UV-cured printing inks market.

Arc-lamp curing retains a toehold in certain wide-web and screen-printing applications that need broadband spectra to trigger cationic photochemistry. However, recent high-output LED diodes reaching 25 W/cm2 narrow the former gap in cure depth, and hybrid lamp housings let users toggle modes mid-shift, hastening the migration curve. As government restrictions on mercury escalate, arc-lamp economics will further erode, reinforcing LED's dominant trajectory.

The UV-Cured Printing Inks Report is Segmented by Curing Process (Arc Curing and LED Curing), Ink Type (UV Flexo Inks, UV Offset Inks, UV Low Energy/LED Offset Inks, and More), Application (Packaging, Commercial and Publication, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 48.05% of 2025 revenue and is tracking a 9.08% CAGR to 2031, led by China's nationwide GB 4806.14-2023 compliance deadline and India's IS:15495 enforcement that restricts toluene in food packaging inks. Local leaders such as UFlex have introduced polyester acrylates that bond to metallized films, enabling converters to meet both barrier and migration goals in a single pass. Government incentives that refund up to 30% of energy-saving equipment costs further accelerate LED UV adoption across new gravure and flexo halls, cementing the region's pull on the UV-cured printing inks market.

North America holds a technology-rich base where early adopters embraced LED units as early as 2016. The U.S. EPA's endorsement and the Inflation Reduction Act's clean-manufacturing credits financed numerous retrofits during 2024-25. Resin and additive capacity expansions, exemplified by Lubrizol's doubling of Solsperse hyperdispersant output in Ohio, bolster supply assurance for domestic ink makers.

The Middle East and Africa, and South America contribute modest volume shares today, yet represent latent upside as packaging converters migrate from solvent lines to LED platforms to comply with export customer audits. Brazilian label printers installing hybrid UV-EB flexo lines attest to an emerging technology leapfrog that could compress adoption timelines once macroeconomic conditions stabilize.

- ALTANA

- APV Engineered Coatings

- artience Co. Ltd. (TOYO INK CO., LTD.)

- Avery Dennison Corporation

- DIC Corporation

- Flint Group

- FUJIFILM Corporation

- Huber Group

- Marabu GmbH & Co. KG

- MIMAKI ENGINEERING CO., LTD.

- Nazdar

- SAKATA INX CORPORATION

- Siegwerk Druckfarben AG & Co. KGaA

- T&K TOKA Corporation

- TOKYO PRINTING INK MFG. CO., LTD.

- Van Son Ink Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Digital and Inkjet Printing

- 4.2.2 Expansion of Packaging and Label Converters

- 4.2.3 Stricter VOC/Sustainability Regulations

- 4.2.4 Rapid Shift to Energy-Efficient LED UV Systems

- 4.2.5 Adoption of Low-Migration Inks in Food and Pharma Packs

- 4.3 Market Restraints

- 4.3.1 Decline of Conventional Commercial Printing

- 4.3.2 Competition from Water-Based and EB-Curable Systems

- 4.3.3 Photoinitiator Supply-Chain Volatility (China Clampdowns)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Curing Process

- 5.1.1 Arc Curing

- 5.1.2 LED Curing

- 5.2 By Ink Type

- 5.2.1 UV Flexo Inks

- 5.2.2 UV Offset Inks

- 5.2.3 UV Low Energy/LED Offset Inks (Except UV Offset Inks)

- 5.2.4 UV Screen Printing Inks

- 5.2.5 Other UV Cured Printing Inks Type

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JV, Partnerships)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ALTANA

- 6.4.2 APV Engineered Coatings

- 6.4.3 artience Co. Ltd. (TOYO INK CO., LTD.)

- 6.4.4 Avery Dennison Corporation

- 6.4.5 DIC Corporation

- 6.4.6 Flint Group

- 6.4.7 FUJIFILM Corporation

- 6.4.8 Huber Group

- 6.4.9 Marabu GmbH & Co. KG

- 6.4.10 MIMAKI ENGINEERING CO., LTD.

- 6.4.11 Nazdar

- 6.4.12 SAKATA INX CORPORATION

- 6.4.13 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.14 T&K TOKA Corporation

- 6.4.15 TOKYO PRINTING INK MFG. CO., LTD.

- 6.4.16 Van Son Ink Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment