|

시장보고서

상품코드

2035080

휴머노이드 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Humanoids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

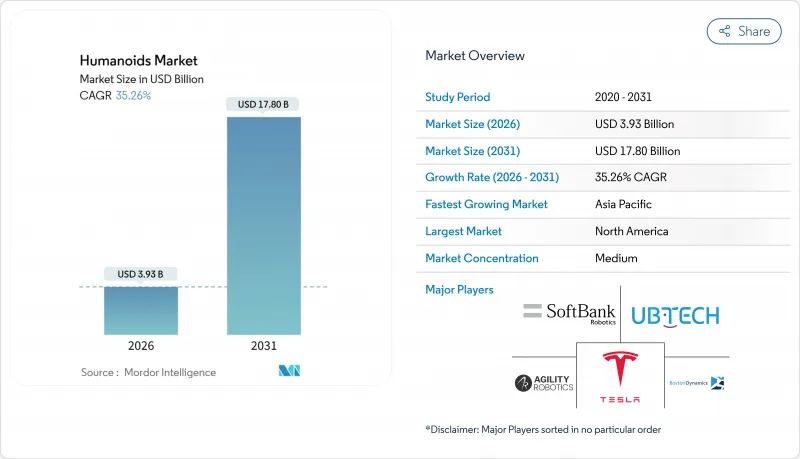

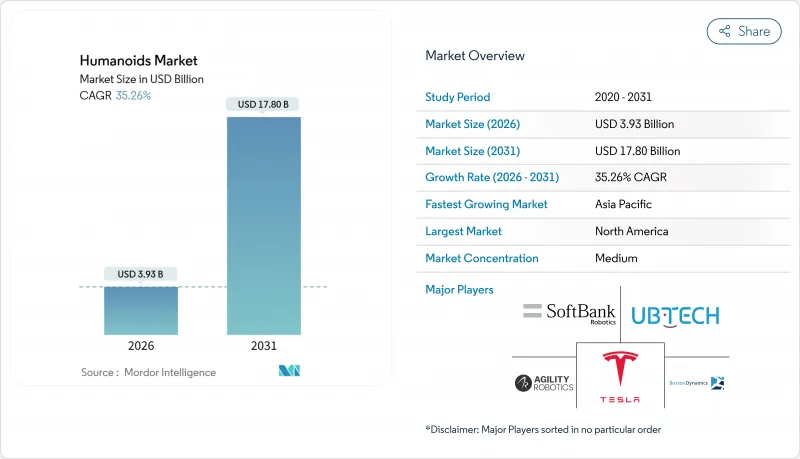

휴머노이드 시장 규모는 2026년에 39억 3,000만 달러 라고 추계되고 있어 예측 기간(2026-2031년)에서 CAGR 35.26%로 성장을 지속하여, 2031년까지 178억 달러에 이를 전망입니다.

인공지능(AI) 하드웨어의 급속한 비용 하락, G7 국가 및 중국의 인구 고령화, 산업 분야의 노동력 부족 현상과 맞물려 휴머노이드 로봇은 파일럿 프로젝트 단계에서 의료, 제조, 물류 분야의 핵심 운용 자산으로 전환하고 있습니다. 2024년부터 2025년까지 40억 달러 이상의 벤처투자가 유입되었으며, 중국과 한국의 '휴머노이드 2025' 정책과 맞물려 새로운 플랫폼 시장 출시 기간이 단축되고 있습니다. 기업들은 기존 도구와 인프라를 활용할 수 있는 인간 크기의 폼팩터를 선호하고 있으며, 소프트웨어의 발전으로 인해 정적이었던 기계가 적응형 동료로 변모하고 있습니다. 이러한 요소들이 상호보완적으로 작용하면서 휴머노이드 시장은 인력 확대 없이 생산성을 향상시키고자 하는 국가들에게 매우 중요한 솔루션이 되고 있습니다.

세계 휴머노이드 시장 동향과 인사이트

고령화에 따른 간병 공백으로 수요 증가 가속화

일본의 65세 이상 인구 비율은 2024년 29.1%에 달했고, 2030년까지 의료인력 부족 인원은 240만 명을 넘어설 것으로 예측됩니다. 병원에서는 환자의 지속적인 모니터링, 투약 업무, 사회적 교류를 위해 휴머노이드를 도입하여 품질을 유지하면서 운영비용을 30-40% 절감하고 있습니다. 혼다의 '할'은 현재 스페인의 노인 병동에서 간호사를 지원하며 국경을 초월한 유용성을 보여주고 있습니다. 비슷한 인력 부족에 직면한 소매업 및 서비스업 사업자들은 직원 수 감소에도 불구하고 고객 경험을 유지하기 위해 접수 및 서비스용 로봇을 도입하고 있습니다. 한국은 이미 직원 1만 명당 1,102대의 로봇이 가동되고 있으며, 이는 세계 최고 수준의 로봇 밀집도를 자랑합니다.

AI 비용 곡선, 대당 2만 5,000달러 이하로 떨어질 것

규모의 경제, 표준화된 액추에이터, 저가의 GPU로 인해 제조 비용은 2025년 35,000달러에서 2030년까지 목표인 13,000-17,000달러로 낮아집니다. 테슬라는 자동차 생산과 같은 대량 생산 체제를 반영해 대당 2만-3만 달러의 가격대로 '옵티머스'를 1만 대 생산할 것으로 예상하고 있습니다. 앱트로닉과 구글 딥마인드(Google DeepMind)의 제휴를 통해 대규모 언어 모델의 추론 능력과 Apollo의 운영 기술이 결합되어 과거에는 10만 달러 상당의 서버가 필요했던 처리를 엣지 프로세서에서 실행할 수 있게 되었습니다. 전기자동차 산업 덕분에 이미 2010년 대비 85% 하락한 배터리 팩 가격은 총소유비용을 더욱 낮추고 있습니다.

코봇 대비 높은 설비투자(Cap-ex)와 시간당 0.50달러 이상의 TCO를 제공합니다.

현재 휴머노이드의 가동 비용은 시간당 0.75-1.25달러이며, 6축 코봇의 경우 0.35-0.50달러입니다. 정밀한 기어박스, 25개 이상의 자유도, 그리고 첨단 센서 어레이로 인해 도입 비용과 유지보수 비용이 모두 치솟고 있습니다. 하지만 사람의 손길이 닿거나 탐색이 필요한 작업에서 코봇을 도입하기 위해서는 시설의 고비용 재설계가 필요하며, 시간당 비용 측면의 이점이 상쇄될 수 있습니다. 공장 평균 임금이 4만 5,000달러가 넘는 선진국에서는 휴머노이드의 연간 운영비용이 25,000-3만 5,000달러로 점점 더 경쟁력이 높아지고 있습니다.

부문 분석

2025년 매출 중 휠 구동형이 62.40%를 차지해 평평한 바닥을 가진 공장이나 풀필먼트 센터에서 에너지 효율이 높고 유지 보수가 적은 이동 수단이 현재 사용자들이 선호하고 있다는 것을 알 수 있습니다. 이러한 우위로 인해 같은 해에 바퀴 달린 휴머노이드 시장 점유율에서 가장 큰 비중을 차지했습니다. 그러나 이족보행 로봇 카테고리는 CAGR 57.1%로 확대되고 있으며, 이는 비용 하락에 따라 휴머노이드 시장이 인간과 환경의 완전한 호환성을 향해 나아가고 있음을 시사합니다.

개선된 모델 예측 제어, 적응형 발목 관절, 전신 협응 알고리즘을 통해 1.5m/s 이상의 정상 보행이 가능하며, 동시에 에너지 소비를 30% 절감할 수 있습니다. 하이브리드 로봇과 다관절 로봇은 잔해나 불규칙한 지형으로 인해 바퀴를 사용하기 어려운 재난 대응에 있어 여전히 틈새 솔루션이 되고 있습니다. AI 모션 플래너가 성숙해짐에 따라 구매자는 동일한 이족보행 유닛을 여러 지점에 재배치할 것으로 예상하고 있으며, 이는 평생 가치를 향상시키고 소프트웨어 업데이트와 운영 성과와의 연관성을 강화할 것으로 예측됩니다.

2025년 휴머노이드 시장 규모 중 하드웨어가 67.20%를 차지했으며, 이는 액추에이터, 복합재 프레임, 고해상도 센서 스택에 대한 막대한 설비투자를 반영합니다. 그러나 소프트웨어의 매출은 CAGR 55.9%를 기록하여 기계적인 업그레이드 주기를 능가하는 성장세를 보이고 있습니다.

클라우드 강화 비전, 자연어 처리 모델, 강화 학습 스택을 통해 동일한 섀시가 오전에는 키팅 작업을, 업무 시간 외에는 컨시어지 업무를 수행할 수 있습니다. 정기적인 라이선스 비용이 하드웨어의 일시적인 이익을 초과함에 따라, 벤더들은 가동 시간, 보안 패치, 기능 제공을 보장하는 서비스 수준 계약(SLA)으로 전환하고 있습니다. 스마트폰 생태계를 연상시키는 이러한 움직임은 물리적 제품 카테고리 내에서도 코드가 가장 큰 차별화 요소로 자리 잡고 있으며, 사이버 보안 및 데이터 소유권 조항에 대한 구매자의 관심이 높아지고 있습니다.

지역별 분석

북미는 20억 달러의 벤처 자금 조달과 도입 위험을 줄이는 초기 단계의 규제 샌드박스에 힘입어 2025년 전 세계 매출의 37.40%를 차지했습니다. 테슬라, 보스턴 다이내믹스, 애질리티 로보틱스(Agility Robotics) 등 미국 OEM 업체들은 2024년부터 2025년까지 총 12억 달러의 자금을 확보해 상용 툴과 시범 운영 자금으로 사용하기로 했습니다. 캐나다 대학은 컴플라이언스 액추에이터 연구를 전문으로 하고, 멕시코는 정밀 기어 케이싱을 공급함으로써 NAFTA공급망 통합을 휴머노이드 경제에 통합하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 시장으로 2031년까지 연평균 53.2%의 성장률을 보일 것으로 예측됩니다. 중국의 100억 달러 규모의 '국가 휴머노이드 계획'은 성(省)급 보조금, 군용 도입 및 구매 할당량을 통합하고 있으며, 6개 현지 기업은 2025년 생산량으로 각각 1,000대 이상을 목표로 하고 있습니다. 한국에서는 3조 5,000억 원 규모의 경기부양책으로 정책은행을 통해 민간 연구소에 자금이 공급되고, 연구개발 및 국내 조달 규정이 촉진되고 있습니다. 일본의 자동차 산업의 전통은 고정밀 스트럿과 조인트 모듈을 생산하고, 인도는 클라우드 제어용 미들웨어를 저렴한 비용으로 공급하고 있습니다. 이러한 요인들이 결합하여 생산 규모를 확대하고 단위 비용을 압축함으로써 아시아 신흥 경제권 전체에서 휴머노이드 시장을 촉진하고 있습니다.

유럽에서는 정책 주도의 꾸준한 성장세를 보이고 있습니다. 독일의 '인더스트리 4.0' 관련 시설에서는 다품종 소량 생산의 조립 공정을 해외로 이전하지 않고 국내에 유지하기 위해 휴머노이드를 도입하고 있습니다. EU의 AI 책임 지침은 엄격한 페일 세이프 설계를 의무화하여 인증 비용은 증가하지만 장기적인 평판 위험은 감소합니다. 프랑스와 영국은 첨단 햅틱센서 연구개발에 주력하고 있으며, 북유럽 국가에서는 노인요양 시범사업을 통해 장기요양 현장에서 로봇의 효용성을 검증하고 있습니다. 인증 일정으로 인해 일부 구매자는 도입을 늦출 수밖에 없는 상황이지만, 독일과 이탈리아의 전통 있는 자동차 부품 공급업체들이 서브 어셈블리 생산에 뛰어들면서 대서양을 가로지르는 경쟁이 심화되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Humanoids Market size is estimated at USD 3.93 billion in 2026, and is expected to reach USD 17.80 billion by 2031, at a CAGR of 35.26% during the forecast period (2026-2031).

Rapid cost declines in artificial intelligence hardware, demographic ageing in the G7 and China, and widening industrial labour gaps are converging to push humanoid robots from pilot projects to core operational assets across healthcare, manufacturing, and logistics. Venture investment flows exceeding USD 4 billion in 2024-2025, together with China's and South Korea's "Humanoid 2025" policies, are accelerating time-to-market for new platforms. Enterprises are prioritising human-scale form factors capable of using existing tools and infrastructure, while software advances turn once-static machines into adaptable co-workers. As these factors reinforce each other, the humanoids market is becoming a pivotal solution for countries seeking productivity gains without expanding their human workforce.

Global Humanoids Market Trends and Insights

Aging-Population Care Gap Intensifies Demand

Japan's population aged 65 years and older reached 29.1% in 2024, and healthcare worker deficits may exceed 2.4 million by 2030. Hospitals are turning to humanoids for continuous patient monitoring, medication rounds, and social interaction, trimming operating costs by 30-40% while keeping quality consistent. Honda's Haru units now assist nurses in Spanish geriatric wards, demonstrating cross-border relevance. Retail and hospitality operators facing similar labour gaps are introducing reception and service robots to protect customer experience despite shrinking staff levels. South Korea already operates 1,102 robots per 10,000 employees, the highest robot density worldwide.

AI Cost Curve Falling Below USD 25 k Per Unit

Economies of scale, standardised actuators, and low-cost GPUs are pushing manufactured costs down from USD 35,000 in 2025 to a targeted USD 13,000-17,000 by 2030. Tesla expects to build 10,000 Optimus units priced at USD 20,000-30,000 each, reflecting automotive-style throughput. Apptronik's partnership with Google DeepMind ties large-language-model reasoning to Apollo's manipulation skills, compressing what once required USD 100,000 servers onto edge processors. Battery pack prices, already 85% lower than 2010 levels thanks to the electric-vehicle industry, further erode total cost of ownership.

High Cap-ex & TCO Above USD 0.50/hr Compared with Cobots

Operating a humanoid costs USD 0.75-1.25 per hour today, versus USD 0.35-0.50 for six-axis cobots. Precision gearboxes, 25-plus degrees of freedom, and richer sensor arrays inflate both acquisition and maintenance outlays. Nevertheless, in tasks demanding human reach and navigation, cobots require costly re-engineering of facilities, offsetting their per-hour advantage. In developed economies where average factory wages top USD 45,000, a humanoid's USD 25,000-35,000 annual running cost is increasingly competitive.

Other drivers and restraints analyzed in the detailed report include:

- Factory Labour Shortages in G7 & China

- National "Humanoid 2025" Programmes (China, South Korea)

- Safety / Liability Regulation Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The wheel-drive class held 62.40% of 2025 revenues, underscoring current user preference for energy-efficient, low-maintenance mobility in flat-floored plants and fulfilment centres. This dominance meant the wheel cohort accounted for the largest slice of the humanoids market share that year. However, the biped category is expanding at a 57.1% CAGR, signalling that the humanoids market will pivot toward full human-environment compatibility as costs fall.

Improved model-predictive controllers, compliant ankle joints, and whole-body coordination algorithms are delivering steady-state walking above 1.5 m/s while cutting energy draw by 30%. Hybrid and multi-leg robots remain niche solutions for disaster response where debris or uneven terrain precludes wheels. As AI motion planners mature, buyers anticipate re-deploying the same biped unit across multiple sites, raising lifetime value and tightening the link between software updates and operational output.

Hardware captured 67.20% of the humanoids market size in 2025, reflecting large capital bills for actuators, composite frames, and high-resolution sensor stacks. Yet software revenue is tracking a 55.9% CAGR, outpacing any mechanical upgrade cycle.

Cloud-enhanced vision, natural-language models, and reinforcement-learning stacks enable the same chassis to perform kitting in the morning and concierge duties after hours. As recurring licence fees overtake one-off hardware margins, vendors are shifting to service-level agreements that guarantee uptime, security patches, and feature drops. This echo of the smartphone ecosystem positions code as the foremost differentiator even inside a physical-goods category, and heightens buyer focus on cybersecurity and data-ownership clauses.

The Humanoids Market Report is Segmented by Motion Type (Wheel-Drive, Biped, Hybrid/Multi-leg), Component (Hardware, Software, Services), End-User Industry (Healthcare Facilities, Retail & Shopping Centres, Manufacturing & Warehousing, and More), Form Factor (Full-Size Greater Than 140cm, Mid-Size 100-140cm, Small Less Than 100cm, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.40% of global 2025 revenue, catalysed by USD 2 billion in venture rounds and early regulatory sandboxes that cut deployment risk. United States OEMs such as Tesla, Boston Dynamics, and Agility Robotics collectively secured USD 1.2 billion during 2024-2025, bankrolling commercial tooling and pilot roll-outs. Canada's universities specialise in compliant-actuator research, and Mexico supplies precision gear casings, threading NAFTA supply-chain integration into humanoid economics.

Asia-Pacific is the fastest-growing theatre, advancing at a 53.2% CAGR to 2031. China's USD 10 billion National Humanoid programme aligns provincial grants, military adoption, and purchasing quotas, while six local firms target >= 1,000 units each for 2025 volume. South Korea's KRW 3.5 trillion stimulus channels funds through its policy bank to private labs, fostering R&D and domestic content rules. Japan's automotive heritage yields high-precision strut and joint modules, and India supplies cloud-control middleware at lower cost. Collectively, these forces scale output and compress unit costs, bolstering the humanoids market across emerging Asian economies.

Europe posts steady, policy-led growth. Germany's Industrie 4.0 facilities adopt humanoids to keep high-mix assembly at home rather than offshoring. The EU's draft AI liability directive compels rigorous fail-safe designs, adding qualification overhead but reducing long-run reputational risk. France and the United Kingdom emphasise advanced haptic-sensor R&D, while Nordic eldercare pilots validate robots in long-term-care settings. Although certification timelines push some buyers to slower roll-outs, established automotive suppliers in Germany and Italy are lining up to build sub-assemblies, reinforcing trans-Atlantic competition.

- Honda Motor Co., Ltd.

- Toyota Motor Corporation

- SoftBank Robotics Group Corp.

- UBTECH Robotics Inc.

- PAL Robotics SL

- Hanson Robotics Ltd.

- Kawada Robotics Corporation

- Promobot LLC

- Invento Robotics Pvt. Ltd.

- ROBOTIS Co., Ltd.

- Boston Dynamics Inc.

- Tesla, Inc. (Optimus)

- Agility Robotics LLC

- Figure AI, Inc.

- Engineered Arts Ltd.

- Unitree Robotics Co., Ltd.

- Fourier Intelligence Co., Ltd.

- Xiaomi Corp. - Robotics Lab

- Samsung Electronics Co., Ltd.

- Apptronik Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-population care gap intensifies demand

- 4.2.2 AI cost curve falling below USD 25k per unit

- 4.2.3 Factory labor shortages in G7 and China

- 4.2.4 National "Humanoid 2025" programs (China, S-Korea)

- 4.2.5 IEC/ISO elderly-care robot safety standards

- 4.2.6 EV motor and battery supply-chain spill-overs

- 4.3 Market Restraints

- 4.3.1 High cap-ex and TCO above USD 0.50 /hr compared with cobots

- 4.3.2 Safety / liability regulation uncertainty

- 4.3.3 Rare-earth magnet supply bottlenecks

- 4.3.4 Societal acceptance and labour-union pushback

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motion Type

- 5.1.1 Wheel-drive

- 5.1.2 Biped

- 5.1.3 Hybrid / Multi-leg

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By End-user Industry

- 5.3.1 Healthcare Facilities

- 5.3.2 Retail and Shopping Centres

- 5.3.3 Manufacturing and Warehousing

- 5.3.4 Hospitality (Hotels, Theme Parks)

- 5.3.5 Academic and Research Institutes

- 5.4 By Form Factor

- 5.4.1 Full-size (Greater than 140 cm)

- 5.4.2 Mid-size (100-140 cm)

- 5.4.3 Small (Less than 100 cm)

- 5.4.4 Upper-torso only

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honda Motor Co., Ltd.

- 6.4.2 Toyota Motor Corporation

- 6.4.3 SoftBank Robotics Group Corp.

- 6.4.4 UBTECH Robotics Inc.

- 6.4.5 PAL Robotics SL

- 6.4.6 Hanson Robotics Ltd.

- 6.4.7 Kawada Robotics Corporation

- 6.4.8 Promobot LLC

- 6.4.9 Invento Robotics Pvt. Ltd.

- 6.4.10 ROBOTIS Co., Ltd.

- 6.4.11 Boston Dynamics Inc.

- 6.4.12 Tesla, Inc. (Optimus)

- 6.4.13 Agility Robotics LLC

- 6.4.14 Figure AI, Inc.

- 6.4.15 Engineered Arts Ltd.

- 6.4.16 Unitree Robotics Co., Ltd.

- 6.4.17 Fourier Intelligence Co., Ltd.

- 6.4.18 Xiaomi Corp. - Robotics Lab

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Apptronik Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment