|

시장보고서

상품코드

2035082

데이터 마스킹 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Data Masking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

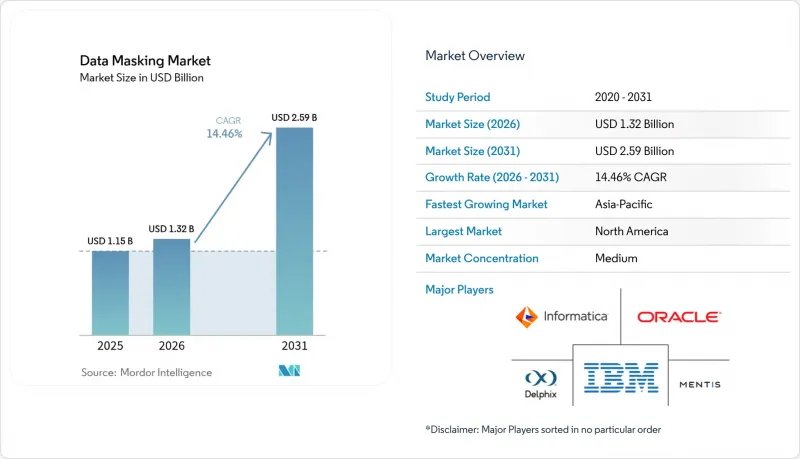

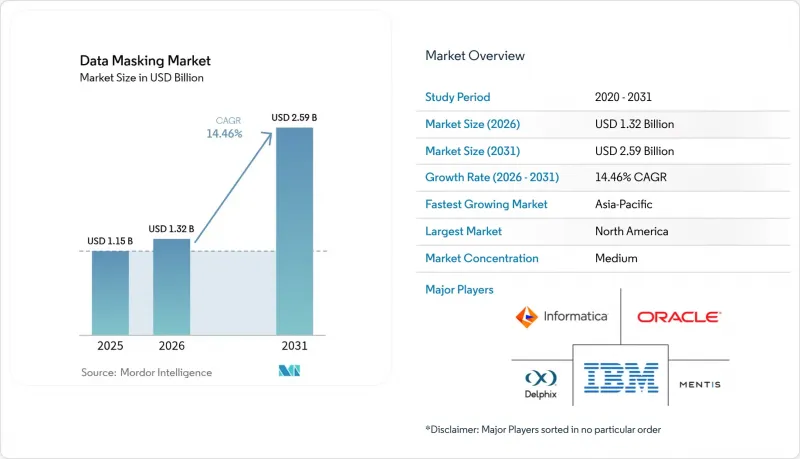

데이터 마스킹 시장 규모는 2025년에 11억 5,000만 달러로 평가되었고 2026년 13억 2,000만 달러에서 2031년까지 25억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 14.46%를 나타낼 전망입니다.

엄격한 규제, 클라우드 전환의 가속화, 랜섬웨어 피해의 급증으로 인해 조직은 임시방편적인 익명화에서 프로덕션 및 비프로덕션 환경의 데이터 자산을 보호하는 표준화된 마스킹 프로그램으로 전환해야 하는 상황에 직면해 있습니다. 각 벤더들은 마스킹 엔진에 AI를 내장하여 기밀 필드를 빠르게 발견할 수 있도록 하고 있으며, DevOps 팀은 지속적인 테스트의 기본값으로 포맷을 유지한 마스킹된 사본을 다루고 있습니다. 기존 기업들이 합성 데이터, 기밀 컴퓨팅, 비정형 데이터 보호의 제품 격차를 메우기 위해 틈새 전문 업체를 인수하려는 움직임이 나타나면서 업계 재편이 진행될 것으로 보입니다. 견조한 성장이 예상되지만, 도입의 복잡성, 라이선스 비용, 데이터 유용성에 대한 우려는 특히 중소기업(SME)에서 단기적인 도입 장벽으로 작용하고 있습니다.

세계 데이터 마스킹 시장 동향 및 인사이트

데이터 프라이버시 규제 강화로 컴플라이언스 투자 촉진

GDPR(EU 개인정보보호규정)을 필두로 수십억 유로의 벌금으로 뒷받침되는 개인정보 보호법의 확대로 인해 마스킹은 기업의 리스크 관리 과제의 중심에 자리 잡게 되었습니다. 현재 미국 13개 주에서는 GDPR(EU 개인정보보호규정)의 의무를 반영한 산업을 불문한 개인정보 보호법이 시행되고 있으며, 다국적 기업들은 수동 데이터 삭제에서 중앙에서 관리되는 마스킹 플랫폼으로 전환을 추진하고 있습니다. ISO/IEC 29100:2024에서는 마스킹이 공식적으로 인정된 프라이버시 강화 기술 중 하나로 꼽히고 있으며, 최고정보보안책임자(CISO)는 예산 승인을 위한 표준에 기반한 근거를 얻을 수 있습니다. 국경을 넘어 사업을 전개하는 은행, 소매업체, 의료 시스템에서는 관할권별 거주지 규칙을 준수하면서도 단일 관리 체계를 철저히 준수하는 정책 조정에 대한 요구가 증가하고 있습니다. 각 벤더들은 지역별로 정보 삭제 기준을 공식화한 템플릿을 제공함으로써 이에 대응하고 있으며, 이를 통해 도입의 신속성과 감사 비용 절감을 실현하고 있습니다.

클라우드 우선의 DevOps는 테스트 데이터 관리의 필요성을 가속화합니다.

DevOps 팀은 매일 코드를 배포하고 있으며, 기밀 정보를 노출하지 않고 프로덕션 환경과 유사한 모양과 동작을 가진 완전한 충실도의 테스트 데이터를 필요로 합니다. 마스킹된 데이터 세트는 현실적이지 않은 합성 데이터만 사용하는 대안에 비해 릴리스 주기를 73% 단축할 수 있기 때문에 마스킹은 지속적인 통합 파이프라인에 필수적인 요소입니다. 컨테이너화된 딜리버리 모델을 통해 팀은 기능 브랜치별로 마스킹된 사본을 실행할 수 있으며, 형식 보존형 토큰화를 통해 복잡한 마이크로서비스에서 참조 무결성을 유지할 수 있습니다. Oracle 데이터 세이프(Oracle Data Safe)와 IBM 인포스피어 옵티메이트(InfoSphere Optim)는 현재 개발자가 테라폼 스크립트에서 직접 호출할 수 있는 마스킹 API를 제공하고 있으며, 이를 통해 인프라-as-code 자동화를 간소화할 수 있습니다. 멀티 클라우드 도입률이 76%에 달하는 가운데, 플랫폼에 구애받지 않는 마스킹 브로커가 AWS, Azure, Google Cloud에서 일관된 정책을 보장합니다.

구현의 복잡성 때문에 기업 도입에 어려움을 겪고 있습니다.

메인프레임, ERP 스위트, 클라우드 데이터 웨어하우스에 각각 다른 커넥터가 필요하기 때문에 기업 전체에 마스킹을 적용하는 데 18개월이 소요되는 것으로 보고되고 있습니다. 수천 개의 테이블에 걸쳐 참조 무결성을 유지하려면 저장 프로시저의 리팩토링이 필요하며, 수개월에 걸친 QA 주기가 추가될 수 있습니다. 토큰화 볼트가 단일 장애점이 될 경우, 설계자는 액티브-액티브 클러스터를 설계해야 하며, 그 결과 설비투자가 증가하게 됩니다. 일부 기업들은 실시간 대응 범위를 희생하더라도 도입을 단순화하기 위해 동적 마스킹을 미루고 정적 스냅샷을 채택하고 있습니다.

부문 분석

정적 기법은 관계형 데이터베이스의 예측 가능한 처리량과 최소한의 쿼리 오버헤드로 인해 2025년 매출의 57.65%를 차지했습니다. 금융기관은 엄격한 키 관리 하에 계좌번호를 복원 가능한 상태로 유지하는 결정론적 토큰화를 중시하고 있으며, 이를 통해 스키마 변경 없이 마스킹된 데이터를 매칭 엔진에 공급할 수 있습니다. CAGR 14.92%로 성장하고 있는 동적 도구는 쿼리를 가로채고 그 자리에서 결과 집합을 재작성하여 프로덕션 환경의 분석 워크로드를 보호합니다. 초기 도입 기업에는 밀리초 단위의 실시간 개인화가 요구되는 온라인 소매업체들이 포함됩니다. 동적 솔루션의 데이터 마스킹 시장 규모는 2025년 4억 9,000만 달러로 추정되었으며, 고객 360과 오픈 뱅킹 API를 배경으로 2031년까지 11억 2,000만 달러 이상에 달할 것으로 예측됩니다. 포맷 보존 암호화는 이 두 가지를 연결하는 가교 역할을 하며, 아키텍트에게 즉각적인 컴플라이언스 준수와 인라인 마스킹 게이트웨이로의 점진적인 전환을 가능하게 하는 마이그레이션 경로를 제공합니다. 2024년 중반에 출시된 탈레스 보메트릭(Thales Vormetric)의 '볼트리스 토큰화(Vaultless Tokenization)'는 이러한 하이브리드 모델의 좋은 예입니다.

2026년부터 2031년까지 정적 마스킹은 QA, 교육 및 오프쇼어 지원을 위한 데이터베이스의 기본 선택이 될 것입니다. 그러나 조직이 이벤트 스트림 아키텍처로 현대화함에 따라 Kafka 주제와 GraphQL 응답을 마스킹할 수 있는 동적 마스킹이 지출 증가분을 차지하게 될 것입니다. 정책-코드 템플릿을 번들로 제공하고 머신러닝을 통해 필드를 자동 분류하는 벤더는 기술 장벽을 낮추고 규제 대상 산업에서 다이내믹 마스킹의 도입을 가속화할 수 있습니다. 그 결과, 데이터 마스킹 시장에서는 단일 기업 내에서 각기 다른 레이턴시 및 비용 요구사항에 맞게 최적화된 정적 및 동적 방식을 결합하여 도입하는 형태를 볼 수 있을 것입니다.

2025년에도 주권 요구 사항과 데이터센터에 대한 기존 투자로 인해 On-Premise 환경에서는 여전히 55.05%의 마스킹된 데이터가 처리되고 있었습니다. 그러나 클라우드 도입의 CAGR이 15.18%에 달하는 것은 특히 레거시 스택을 피하는 디지털화된 중소기업들 사이에서 빠른 점유율 전환이 이루어지고 있음을 보여줍니다. 클라우드 솔루션의 데이터 마스킹 시장 규모는 2025년 5억 2,000만 달러에 달하고, 멀티 클라우드 분석 프로그램의 발전에 따라 확대될 것으로 전망됩니다. 인텔 SGX와 같은 기밀 컴퓨팅 기능을 통해 마스킹 엔진은 계산 중에 키를 보호할 수 있어 공급자의 접근에 대한 우려를 줄일 수 있습니다. K2View의 패브릭은 Kubernetes 오퍼레이터로 배포되어 재코딩 없이 Redshift, Snowflake, BigQuery 전체에 규칙을 균일하게 적용합니다.

2031년까지 대부분의 대기업은 정책 엔진을 중앙에서 운영하며, On-Premise 및 클라우드 작업자 모두에게 적용 결정을 위임하게 될 것입니다. 이 페더레이티드 패턴은 데이터 전송 비용을 절감하고, 데이터 거주지 관련 법규를 준수할 수 있습니다. 2025년 하반기 공개 예정인 ISO/IEC 27701은 클라우드 PIA(프라이버시 영향 평가)를 위한 프라이버시 관리 방안을 규정하는 것으로, 마스킹 벤더들은 이미 초안 조항에 대한 관리 방안 대응을 진행하고 있습니다. 그 결과, 데이터 마스킹 시장에서는 모든 주요 하이퍼스케일러에 네이티브 커넥터를 갖추고, 클라우드 보안 포지셔닝 관리 도구와 데이터 리니지 메타데이터를 공유할 수 있는 플랫폼이 평가받게 될 것입니다.

지역별 분석

북미는 2025년 매출의 37.05%를 차지했습니다. 이는 클라우드의 조기 도입, 엄격한 주법, 그리고 랜섬웨어에 대한 높은 노출 위험에 기인합니다. 경영진의 예산에는 막대한 데이터 침해 벌금이 반영되어 있으며, 이로 인해 마스킹은 사이버 보안 로드맵의 최우선 순위가 되었습니다. 이 지역에 본사를 둔 다국적 기업들은 전 세계 자회사에 일관된 정책을 적용하는 통합 플랫폼을 도입하여 국경 간 감사를 간소화하고 있습니다.

유럽은 GDPR(EU 개인정보보호규정)의 시행과 AI법 등 새로운 법령의 시행에 힘입어 이를 따르고 있습니다. 메타에 대한 12억 유로의 벌금에서 볼 수 있듯이, 규제 당국이 거액의 벌금을 부과하는 태도는 마스킹 도입의 명확한 ROI(투자대비효과)를 뒷받침하고 있습니다. '디지털 유럽 프로그램'의 자금 지원으로 1억 4,200만 유로가 중소기업의 프라이버시 기술 도입에 사용되어 대기업과 중소기업 간의 역사적 격차가 줄어들고 있습니다.

아시아태평양은 2031년까지 15.44%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 싱가포르를 비롯한 각국은 OECD 프레임워크에 부합하도록 개인정보보호법을 개정하고 있으며, 중국은 PIPL(개인정보보호법)에 따라 데이터 로컬 처리를 의무화하고 있습니다. 이는 현지 마스킹 노드를 갖춘 지역 데이터센터 건설을 촉진하고 있습니다. 인도의 IT 아웃소싱 업체들은 오프쇼어 딜리버리 센터 내 고객 데이터를 보호하기 위해 기본적으로 마스킹을 채택하고 있으며, 국내 벤더에 대한 지출을 늘리고 있습니다. 남미, 중동, 아프리카는 절대적인 규모에서는 뒤쳐져 있지만, 디지털 ID, 핀테크, 스마트시티의 성숙도가 높아지면서 미개척 시장 기회가 창출되고 있습니다. 현지 대리점들은 마스킹을 컴플라이언스 대응 턴키 패키지에 포함시켜 초기 시장 침투를 가속화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The data masking market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031).

Strong legislation, accelerating cloud migration, and a surge in ransomware incidents are pushing organizations to replace ad-hoc anonymization with standardized masking programs that protect production and non-production data estates. Vendors are embedding AI in masking engines to speed discovery of sensitive fields, while DevOps teams treat masked, format-preserving copies as the default for continuous testing. Consolidation is likely as incumbents acquire niche specialists to fill product gaps in synthetic data, confidential computing, and unstructured data protection. Despite healthy growth, implementation complexity, licensing costs, and data-utility concerns remain short-term brakes on adoption, particularly for small and medium enterprises (SMEs).

Global Data Masking Market Trends and Insights

Rising Data-Privacy Regulations Drive Compliance Investment

Expanding privacy laws, led by GDPR and backed by multi-billion-euro fines, have pushed masking to the center of corporate risk agendas. Thirteen U.S. states now enforce sector-agnostic privacy statutes that mirror GDPR obligations, prompting multinationals to replace manual scrubbing with centrally governed masking platforms. ISO/IEC 29100:2024 lists masking among formally recognized privacy-enhancing technologies, giving chief information security officers (CISOs) a standards-based reference for budget approvals. Banks, retailers, and health systems with cross-border footprints increasingly demand policy orchestration that maps to jurisdiction-specific residency rules yet enforces a single control posture. Vendors respond with templates that codify region-specific redaction thresholds, accelerating rollouts and lowering audit costs.

Cloud-First DevOps Accelerates Test Data Management Needs

DevOps teams deploy code daily and require full-fidelity test data that looks and behaves like production without exposing secrets. Masked datasets shorten release cycles by 73% compared to less realistic synthetic-only alternatives, making masking integral to continuous integration pipelines. Containerized delivery models let teams spin up a masked copy per feature branch, while format-preserving tokenization keeps referential integrity for complex microservices. Oracle Data Safe and IBM InfoSphere Optim now ship masking APIs that developers call directly from Terraform scripts, which simplifies infrastructure-as-code automation. As multicloud adoption reaches 76%, platform-agnostic masking brokers ensure consistent policies across AWS, Azure, and Google Cloud.

Implementation Complexity Challenges Enterprise Adoption

Enterprises report 18-month timelines to roll out enterprise-wide masking because mainframes, ERP suites, and cloud data warehouses require different connectors. Maintaining referential integrity across thousands of tables can mean refactoring stored procedures, adding months of QA cycles. Where tokenization vaults become a single point of failure, architects must design active-active clusters, increasing capital expense. Some firms defer dynamic masking in favor of static snapshots, trading real-time coverage for simpler deployments.

Other drivers and restraints analyzed in the detailed report include:

- Synthetic Data Adoption Transforms AI Training Paradigms

- Surge in Ransomware Attacks Elevates Data Protection Priority

- High Total Cost of Ownership Constrains SME Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Static techniques delivered 57.65% of 2025 revenue, underpinned by predictable throughput and minimal query overhead in relational databases. Financial institutions value deterministic tokenization that keeps account numbers reversible under strict key control, allowing masked data to feed reconciliation engines without schema changes. Dynamic tools, growing at a 14.92% CAGR, shield production analytics workloads by intercepting queries and rewriting result sets on the fly. Early adopters include online retailers running real-time personalization where milliseconds matter. The data masking market size for dynamic solutions is estimated at USD 0.49 billion in 2025, projected to exceed USD 1.12 billion by 2031 on the back of customer-360 and open-banking APIs. Format-preserving encryption bridges both camps, giving architects a migration path that delivers immediate compliance while enabling a gradual move to in-line masking gateways. Thales Vormetric's vaultless tokenization, launched mid-2024, exemplifies the hybrid model.

Across 2026-2031, static masking will remain the default for QA, training, and offshore support databases. However, as organizations modernize to event-stream architectures, dynamic masking that can redact Kafka topics or GraphQL responses will capture incremental spend. Vendors that bundle policy-as-code templates and auto-classify fields using machine learning lower the skills barrier, accelerating dynamic adoption in regulated verticals. As a result, the data masking market will likely see a blending of static-plus-dynamic deployments within single enterprises, each optimized for distinct latency and cost envelopes.

On-premise environments still processed 55.05% of masked data in 2025, driven by sovereignty mandates and sunk investments in data centers. Yet a 15.18% CAGR in cloud deployments points to rapid share transfer, especially among digitized SMEs that bypass legacy stacks. The data masking market size for cloud solutions reached USD 0.52 billion in 2025 and will climb in line with multicloud analytics programs. Confidential-computing features such as Intel SGX allow masking engines to protect keys during computation, mitigating fears around provider access. K2View's fabric deploys as Kubernetes operators, applying rules uniformly across Redshift, Snowflake, and BigQuery without re-coding.

By 2031, most large enterprises will run policy engines centrally and push enforcement decisions to both local and cloud workers. This federated pattern reduces egress charges and complies with residency laws. ISO/IEC 27701, scheduled for late-2025 release, will codify privacy controls for cloud PIAs, and masking vendors are already mapping controls to draft clauses. Consequently, the data masking market will reward platforms with native connectors to all major hyperscalers and the ability to share lineage metadata with cloud security posture management tools.

The Data Masking Market Report is Segmented by Type (Static and Dynamic), Deployment Model (Cloud and On-Premise), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), Data Environment (Structured Data and Semi-Structured and Unstructured Data), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.05% of revenue in 2025, anchored by early cloud adoption, stringent state laws, and high ransomware exposure. C-suite budgets reflect sizable breach fines, pushing masking to the top of cybersecurity roadmaps. Multinationals headquartered in the region deploy unified platforms that apply policies consistently to subsidiaries worldwide, simplifying cross-border audits.

Europe follows with entrenched GDPR enforcement and emerging statutes such as the AI Act. Regulators' appetite for blockbuster fines, demonstrated by the EUR 1.2 billion Meta penalty, creates a clear ROI case for masking deployment. Funding from the Digital Europe Programme channels EUR 142 million toward SME privacy tech adoption, shrinking the historical gap between large enterprises and smaller firms.

Asia-Pacific posts the fastest 15.44% CAGR through 2031. Nations, including Singapore, update privacy laws to align with OECD frameworks, and China mandates data-local processing under PIPL, prompting regional data-center build-outs with local masking nodes. Indian IT outsourcers adopt masking by default to protect client data inside offshore delivery centers, boosting domestic vendor spend. South America, the Middle East, and Africa lag in absolute dollars but present green-field opportunities as digital ID, fintech, and smart-city initiatives mature. Local resellers bundle masking into turnkey compliance packages, accelerating initial penetration.

- IBM Corporation

- Oracle Corporation

- Informatica Inc.

- Delphix Corp.

- Mentis Inc.

- Innovative Routines International Inc.

- Solix Technologies Inc.

- K2View Ltd.

- Redgate Software Ltd.

- Broadcom Inc. (CA Technologies)

- Protegrity USA, Inc.

- TokenEx, LLC

- Ekobit d.o.o.

- Dataguise Inc. (PKWARE)

- Micro Focus International plc

- Informatica LLC

- Baffle, Inc.

- Very Good Security, Inc.

- Immuta, Inc.

- Spirion, LLC

- Camouflage Software Inc.

- ARCAD Software SA

- IRI Voracity (Innovative Routines International)

- Dataprotect S.A.

- TripleBlind, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in global data volume

- 4.2.2 Rising data-privacy regulations (GDPR, CCPA, etc.)

- 4.2.3 Cloud-first DevOps requiring masked test data

- 4.2.4 Surge in ransomware and cyber-attacks

- 4.2.5 Synthetic-data adoption to augment AI training

- 4.2.6 Data residency mandates in emerging economies

- 4.3 Market Restraints

- 4.3.1 Implementation complexity and legacy integration

- 4.3.2 High total cost of ownership for dynamic tools

- 4.3.3 Reduced data utility for advanced analytics

- 4.3.4 Regulatory uncertainty on cross-border synthetic datasets

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Key Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Static

- 5.1.2 Dynamic

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial and Defense

- 5.4.6 Energy and Utilities

- 5.4.7 Manufacturing

- 5.4.8 Other Industry Verticals

- 5.5 By Data Environment

- 5.5.1 Structured Data

- 5.5.2 Semi-structured and Unstructured Data

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Oracle Corporation

- 6.4.3 Informatica Inc.

- 6.4.4 Delphix Corp.

- 6.4.5 Mentis Inc.

- 6.4.6 Innovative Routines International Inc.

- 6.4.7 Solix Technologies Inc.

- 6.4.8 K2View Ltd.

- 6.4.9 Redgate Software Ltd.

- 6.4.10 Broadcom Inc. (CA Technologies)

- 6.4.11 Protegrity USA, Inc.

- 6.4.12 TokenEx, LLC

- 6.4.13 Ekobit d.o.o.

- 6.4.14 Dataguise Inc. (PKWARE)

- 6.4.15 Micro Focus International plc

- 6.4.16 Informatica LLC

- 6.4.17 Baffle, Inc.

- 6.4.18 Very Good Security, Inc.

- 6.4.19 Immuta, Inc.

- 6.4.20 Spirion, LLC

- 6.4.21 Camouflage Software Inc.

- 6.4.22 ARCAD Software SA

- 6.4.23 IRI Voracity (Innovative Routines International)

- 6.4.24 Dataprotect S.A.

- 6.4.25 TripleBlind, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment