|

시장보고서

상품코드

2035094

갈륨비소(GaAs) 웨이퍼 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Gallium Arsenide GaAs Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

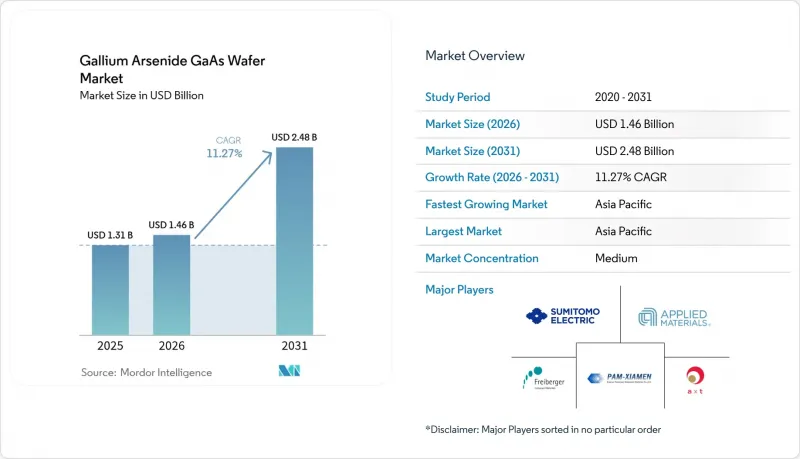

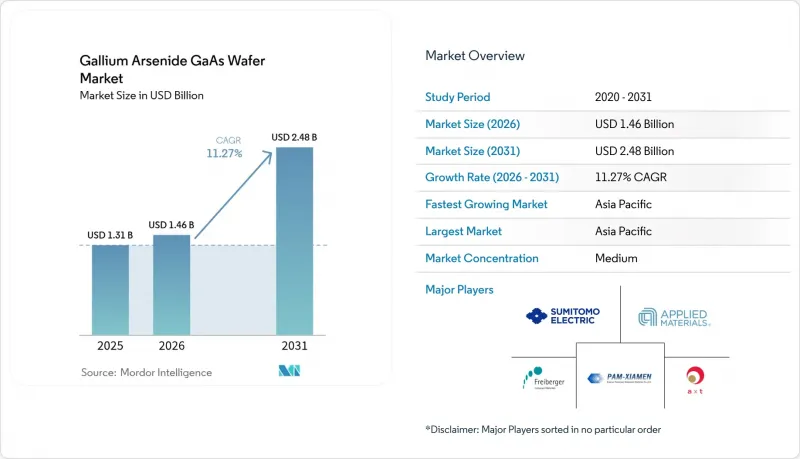

2026년 갈륨비소 웨이퍼 시장 규모는 14억 6,000만 달러로 추정되며 2025년 13억 1,000만 달러에서 성장하여 2031년에는 24억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 11.27%를 나타낼 것으로 예측됩니다.

고주파 무선 모듈, 광전자 이미터 및 국방용 레이더 장치에 대한 견고한 수요로 인해 갈륨비소 기판은 실리콘의 성능을 능가하는 분야에서 확고한 입지를 유지하고 있습니다. 주요 통신사업자들이 네트워크 하드웨어를 5G 표준으로 업데이트함에 따라, 프론트엔드 모듈 공급업체들은 mm파 대역에서 CMOS를 능가하는 성능을 발휘하는 GaAs 전력 증폭기를 채택할 수밖에 없는 상황입니다. 동시에 데이터센터 사업자들은 저지연으로 400G 및 800G 트래픽을 처리하기 위해 GaAs 기반 VCSEL 어레이를 채택하고 있으며, 마이크로 LED 혁신 기업들은 증강현실(AR) 헤드셋의 규모 확장을 위해 GaAs 에피택시 층의 균일성에 대한 기대감을 가지고 있습니다. 투자 동향을 살펴보면, 북미가 방사능 내성 웨이퍼에 대한 중요한 군사 수요를 포위하고 있는 반면, 아시아태평양의 팹은 수직 통합과 비용 우위를 활용하여 전 세계 고객에게 공급하고 있음을 확인할 수 있습니다. 원격 에피택시와 같은 획기적인 개념은 기판의 재활용을 가능하게 하고, 단기적인 수요를 둔화시키지 않으면서도 GaAs 소비 경제의 미래 변화를 시사합니다.

세계 갈륨비소(GaAs) 웨이퍼 시장 동향과 인사이트

5G 인프라 구축이 GaAs RF 수요를 견인할 것입니다.

통신 사업자들은 고밀도 5G 매크로셀 및 스몰셀 기지국을 배치하고 있으며, 이를 위해서는 28GHz 이상의 주파수 대역에서 선형 출력을 유지할 수 있는 전력 증폭기가 필요하지만, 실리콘 LDMOS는 이 영역에서 성능이 저하됩니다. 갈륨비소 웨이퍼는 약 8,500 cm2/V*s의 전자 이동도를 구현하여 도시 지역 커버리지를 보장하는 대규모 MIMO 어레이에서 신호 무결성을 유지하는 효율적인 프론트엔드 모듈을 가능하게 합니다. 네트워크 벤더들은 수직 통합형 GaAs 제조업체와 다년간공급 계약을 체결하여 4G 하드웨어 업데이트 주기를 2027년까지 예측 가능한 수요로 전환하고 있습니다.

광전자 소자 붐(VCSEL, 레이저)

하이퍼스케일 데이터센터는 저지연과 저전력을 실현하는 GaAs 기반 VCSEL 어레이를 채택한 400G 및 800G 광통신 장비로 전환하고 있습니다. 스마트폰 제조업체들은 생체 인식 모듈에 3D 센싱용 VCSEL을 내장하고, 자동차 제조업체들은 LiDAR에 GaAs 레이저를 채택하고 있습니다. 에피택셜 재성장 기술의 발전으로 방열성이 향상되고, 디바이스의 수명이 연장되며, 고품질 웨이퍼의 평균판매가격(ASP)이 유지되고 있습니다.

Si 및 SiC에 비해 높은 제조 비용

GaAs 결정을 끌어올리기 위해서는 가압 비소 분위기와 유독가스 취급이 필요하며, 이로 인해 실리콘보다 설비투자(CapEx)와 운영비용(Opex)이 더 많이 소요됩니다. 4인치나 6인치와 같은 소형 포맷에서는 300mm 실리콘 웨이퍼 당 다이 수에서 경제성이 떨어지기 때문에 가격에 민감한 소비자 가전제품에 GaAs를 적용하는 데 한계가 있습니다.

부문 분석

2025년에는 전력 증폭기 및 스위치가 5G 인프라 업그레이드의 핵심이 되어 RF 전자제품이 매출의 43.65%를 차지했습니다. 갈륨비소 웨이퍼 시장 규모의 이 부분은 스몰셀의 고밀도화 계획에 따라 꾸준히 확대될 것으로 예측됩니다. VCSEL 상호연결 및 AR/VR용 광학 소자가 주도하는 포토닉스 및 이미징 장치는 CAGR 13.25%로 다른 모든 응용 분야를 능가하는 성장률을 보일 것으로 예상되며, 이는 향후 갈륨비소 웨이퍼 시장공급량을 재구성할 것으로 보입니다.

휴대폰 제조업체들이 VCSEL 기반 얼굴 인식 모듈을 통합함에 따라, 부문 전반에 걸친 수요의 파급효과가 발생하여 일반적인 6인치 에피택셜 라인의 포토닉스 및 RF 생산량을 모두 증가시키고 있습니다. GaAs 태양전지는 여전히 우주선용 틈새 시장이지만, 새로운 이종집적 개념으로 인해 다중접합 설계가 지상의 집광 어레이에 도입될 가능성이 있습니다.

4인치 기판은 성숙한 제조 설비 덕분에 여전히 매출의 35.85%를 차지하고 있지만, 생산 능력 발표에 따르면 6인치 라인이 CAGR 12.85%로 증가분 수요의 대부분을 흡수할 것이라고 합니다. 이러한 전환으로 인해 1회 생산당 다이 수가 증가하고 고정비가 분산되어 전체 갈륨비소 웨이퍼 시장의 평균판매가격(ASP)이 하락하는 방향으로 가고 있습니다.

각 장비 업체들은 6인치 이상의 규모로 확대하기 위해 온도 구배 제어 및 비소 증기 관리에 힘쓰고 있습니다. 초기 8인치 파일럿 생산은 유망한 결과를 보여주었지만, 상업적 배포를 위해서는 결함률을 더 낮춰야 합니다.

지역별 분석

아태지역은 에피택셜 제조 라인의 집적화, 하도급 기반, 정부 주도의 5G 인프라 구축으로 2025년 갈륨비소 웨이퍼 시장의 60.10%를 차지했습니다. 정부의 인센티브에 힘입어 중국 본토에서는 화합물 반도체 팹의 확장이 진행되고 있으며, 대만과 한국은 파운드리 및 장비 시너지를 통해 공급의 다양성을 강화하고 있습니다.

북미는 안전한 국내 생산을 필요로 하는 항공우주 및 방위 분야 수요에 힘입어 2위를 차지했습니다. 최근 CHIPS법에 의한 인센티브로 레이더 및 위성 프로그램용 반절연 소재 전용의 새로운 결정성장로와 클린룸에 대한 자금이 투입되어 장기적인 국내 공급 체제가 구축되고 있습니다.

유럽은 자동차 및 산업 자동화 분야에서 강점을 보이고 있습니다. Tier 1 공급업체들은 ADAS 레이더 및 공장용 센싱을 지원하기 위해 GaAs 전력 소자를 조달하고 있으며, 엄격한 환경 규제로 인해 웨이퍼 재활용에 대한 순환 경제에 대한 조사가 활발히 진행되고 있습니다. EU의 협조적인 자금 지원으로 150mm 화합물 반도체 웨이퍼 파일럿 라인이 지원되고 있으며, 아시아 지역과의 생산 능력 격차를 줄이는 것을 목표로 하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20Gallium arsenide wafer market size in 2026 is estimated at USD 1.46 billion, growing from 2025 value of USD 1.31 billion with 2031 projections showing USD 2.48 billion, growing at 11.27% CAGR over 2026-2031.

Robust demand for high-frequency radio modules, optoelectronic emitters, and defense-grade radar devices keeps Gallium arsenide substrates firmly positioned where silicon performance plateaus. Large telecom operators are refreshing network hardware to 5G standards, compelling front-end module suppliers to specify GaAs power amplifiers that outperform CMOS at millimeter-wave bands. In parallel, data-center operators adopt VCSEL arrays on GaAs to move 400G and 800G traffic with lower latency, while micro-LED innovators count on GaAs epi uniformity to scale augmented-reality headsets. Investment patterns confirm that Asia-Pacific fabs leverage vertical integration and cost advantages to supply global customers, even as North America rings-fences critical military demand for radiation-hardened wafers. Breakthrough concepts such as remote epitaxy promise to recycle substrates, hinting at future shifts in GaAs consumption economics without dampening near-term demand.

Global Gallium Arsenide GaAs Wafer Market Trends and Insights

5G Infrastructure Roll-out Fuels GaAs RF Demand

Telecom operators are deploying dense 5G macro- and small-cell sites that require power amplifiers sustaining linear output well above 28 GHz, where silicon LDMOS falters. Gallium arsenide wafers deliver electron mobility around 8,500 cm2/V*s, enabling efficient front-end modules that preserve signal integrity in massive-MIMO arrays for urban coverage. Network vendors lock multiyear supply contracts with vertically integrated GaAs houses, converting 4G hardware refresh cycles into predictable demand through 2027.

Optoelectronic Device Boom (VCSELs, Lasers)

Hyperscale data centers move to 400G and 800G optics that rely on GaAs-based VCSEL arrays for lower latency and power draw. Smartphone makers embed 3D-sensing VCSELs in biometric modules, while automotive OEMs adopt GaAs lasers for LiDAR. Epitaxial regrowth advances improve thermal dissipation, extending device lifetimes and sustaining premium wafer ASPs.

High Production Cost vs Si and SiC

GaAs crystal pulling needs pressurized arsenic atmospheres and toxic-gas handling that raise CapEx and Opex above silicon. Smaller 4-inch and 6-inch formats cannot match the die-per-wafer economics of 300 mm silicon, limiting GaAs uptake in price-sensitive consumer gadgets.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace and Defense Uptake for High-Frequency Radar

- Asian Epitaxy Capacity Boosts Supply and Lowers ASP

- Gallium Supply Concentration and Export Controls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

RF electronics held 43.65% revenue in 2025 as power amplifiers and switches remain core to 5G infrastructure upgrades. This portion of the Gallium arsenide wafer market size is forecast to climb steadily alongside small-cell densification plans. Photonic and imaging devices, propelled by VCSEL interconnects and AR/VR optics, are set to outpace all other uses at 13.25% CAGR, thereby reshaping future volumes of the Gallium arsenide wafer market.

Cross-segment pull-through emerges as handset makers integrate VCSEL-based face ID modules, boosting both photonics and RF volume on common 6-inch epi lines. Solar cells on GaAs remain a niche for spacecraft, yet new heterointegration concepts could push multi-junction designs into terrestrial concentrator arrays.

Four-inch substrates still command 35.85% revenue thanks to mature tooling, but capacity announcements reveal that 6-inch lines will absorb most incremental demand at 12.85% CAGR. The shift improves die counts per run and spreads fixed costs, nudging the overall Gallium arsenide wafer market toward lower ASPs.

Equipment vendors tackle thermal-gradient control and arsenic vapor management to scale beyond 6 inches. Early 8-inch pilot runs show promise yet require further defect reduction before commercial deployment.

The Gallium Arsenide (GaAs) Wafer Market Report is Segmented by Application (Radio-Frequency Electronics, and More), Wafer Diameter (2 Inch, 3 Inch, 4 Inch, and More), Growth Technology (LEC, VGF, and More), End-Use Industry (Telecom and 5G Infrastructure, and More), Conductivity Type (Semi-Insulating GaAs, Semi-Conducting GaAs), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 60.10% of the Gallium arsenide wafer market in 2025 thanks to clustered epitaxial lines, a deep subcontract base, and state-backed 5G build-outs. Government incentives help mainland China expand compound-semiconductor fabs, while Taiwan and South Korea provide foundry and equipment synergies that reinforce supply diversity.

North America ranks second, anchored by aerospace and defense demand requiring secure on-shore production. Recent CHIPS Act incentives finance new crystal-growth reactors and cleanrooms dedicated to semi-insulating material for radar and satellite programs, cementing long-term domestic supply.

Europe retains strength in automotive and industrial automation. Tier-1 suppliers source GaAs power devices to support ADAS radar and factory sensing, while stringent environmental directives spur circular-economy research on wafer reclamation. Coordinated EU funding backs pilot lines for 150 mm compound-semiconductor substrates, seeking to narrow the capacity gap with Asia.

- AXT Inc.

- China Crystal Technologies Co. Ltd.

- Freiberger Compound Materials GmbH

- Semiconductor Wafer Inc.

- Sumitomo Electric Industries, Ltd.

- Xiamen Powerway Advanced Material Co., Ltd.

- Wafer Technology Ltd.

- Vital Materials Co., Ltd.

- DOWA Electronics Materials Co., Ltd.

- American Elements, Inc.

- IQE plc

- WIN Semiconductors Corp.

- Advanced Wireless Semiconductor Co.

- Visual Photonics Epitaxy Co., Ltd. (VPEC)

- IntelliEPI, Inc.

- Global Communication Semiconductors, LLC

- Roditi Ltd.

- Veeco Instruments Inc.

- Applied Materials, Inc.

- AIXTRON SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G infrastructure roll-out fuels GaAs RF demand

- 4.2.2 Optoelectronic device boom (VCSELs, lasers)

- 4.2.3 Aerospace and defense uptake for high-freq radar

- 4.2.4 Asian epitaxy capacity boosts supply and lowers ASP

- 4.2.5 Micro-LED adoption in AR/VR wearables

- 4.2.6 Remote-epitaxy substrate reuse cuts wafer cost

- 4.3 Market Restraints

- 4.3.1 High production cost vs Si and SiC

- 4.3.2 Gallium supply concentration and export controls

- 4.3.3 GaN and SiC competition in RF / power

- 4.3.4 Environmental and safety compliance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Radio-Frequency Electronics

- 5.1.2 Optical and IR LEDs

- 5.1.3 Photovoltaic / Solar Cells

- 5.1.4 Photonic and Imaging Devices

- 5.1.5 Other Applications

- 5.2 By Wafer Diameter

- 5.2.1 2 inch (50 mm)

- 5.2.2 3 inch (76 mm)

- 5.2.3 4 inch (100 mm)

- 5.2.4 6 inch (150 mm)

- 5.2.5 8 inch (200 mm) and Above

- 5.3 By Growth Technology

- 5.3.1 Liquid-Encapsulated Czochralski (LEC)

- 5.3.2 Vertical Gradient Freeze (VGF)

- 5.3.3 Horizontal Bridgman (HB)

- 5.3.4 Molecular Beam Epitaxy (MBE)

- 5.3.5 Metal-Organic CVD (MOCVD)

- 5.4 By End-Use Industry

- 5.4.1 Telecom and 5G Infrastructure

- 5.4.2 Consumer Electronics

- 5.4.3 Aerospace and Defense

- 5.4.4 Automotive (ADAS, EV)

- 5.4.5 Industrial and Energy

- 5.5 By Conductivity Type

- 5.5.1 Semi-insulating GaAs

- 5.5.2 Semi-conducting GaAs (n-/p-type)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AXT Inc.

- 6.4.2 China Crystal Technologies Co. Ltd.

- 6.4.3 Freiberger Compound Materials GmbH

- 6.4.4 Semiconductor Wafer Inc.

- 6.4.5 Sumitomo Electric Industries, Ltd.

- 6.4.6 Xiamen Powerway Advanced Material Co., Ltd.

- 6.4.7 Wafer Technology Ltd.

- 6.4.8 Vital Materials Co., Ltd.

- 6.4.9 DOWA Electronics Materials Co., Ltd.

- 6.4.10 American Elements, Inc.

- 6.4.11 IQE plc

- 6.4.12 WIN Semiconductors Corp.

- 6.4.13 Advanced Wireless Semiconductor Co.

- 6.4.14 Visual Photonics Epitaxy Co., Ltd. (VPEC)

- 6.4.15 IntelliEPI, Inc.

- 6.4.16 Global Communication Semiconductors, LLC

- 6.4.17 Roditi Ltd.

- 6.4.18 Veeco Instruments Inc.

- 6.4.19 Applied Materials, Inc.

- 6.4.20 AIXTRON SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment