|

시장보고서

상품코드

2035095

인화인듐 웨이퍼 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Indium Phosphide Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

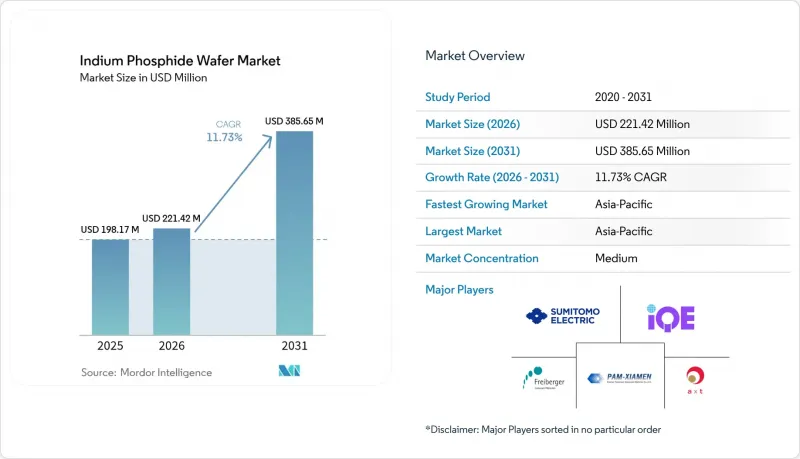

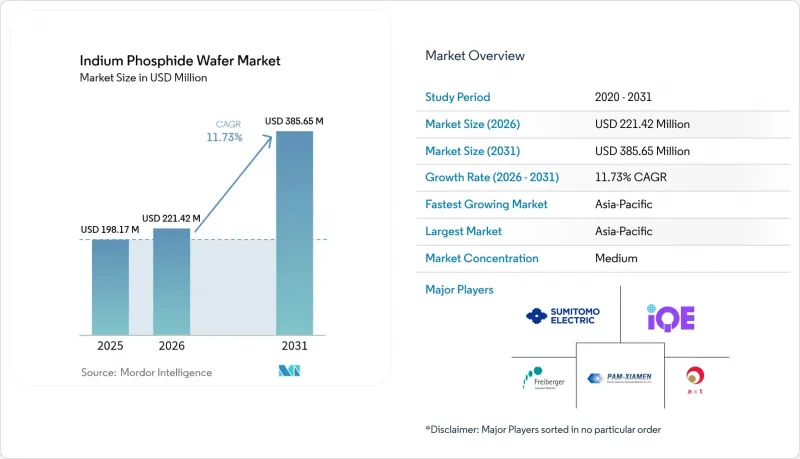

인화인듐 웨이퍼 시장 규모는 2025년 1억 9,817만 달러에서 2026년에는 2억 2,142만 달러로 확대되어 2026년부터 2031년까지 CAGR 11.73%로 성장을 지속하여, 2031년까지 3억 8,565만 달러에 이를 것으로 예측됩니다.

하이퍼스케일 데이터센터의 갱신은 800G 및 1.6T 광통신 장비에 대한 수요를 견인하고 있으며, 5G의 세계 확산과 6G 백홀 준비, 그리고 양자 광통신에 대한 자금 투입 확대가 그 뒤를 잇고 있습니다. 대구경 기판은 단가를 낮추고, InP-on-Si 하이브리드 플랫폼은 추가적인 확장성을 약속합니다. 아시아태평양의 통합된 화합물 반도체 생태계가 공급의 기반이 되고 있지만, 유럽과 미국의 리쇼어링(국내 회귀) 프로그램으로 인해 국내 생산 능력의 확대가 가속화되고 있습니다. 결정 성장 노하우, 다년간의 고객 인증 및 고가의 설비투자가 신규 진입을 막고 있기 때문에 경쟁의 강도는 중간 정도에 머물러 있습니다.

세계 인화인듐(InP) 웨이퍼 시장 동향 및 인사이트

고속 광트랜시버 수요로 인해 InP 채택 가속화

800G 및 1.6T 링크로 전환하는 클라우드 사업자는 필요한 속도로 작동하는 에지 방출 레이저와 포토다이오드를 필요로 하는데, 이를 제공할 수 있는 것은 인듐뿐입니다. Coherent는 2024년 4분기에 InP 디바이스 생산량을 3배로 늘렸고, 현재 3.2T 트랜시버 샘플을 제공합니다. 소스 포토닉스(Source Photonics)는 InP 기반 부품을 사용한 1.6T 코히런트 모듈을 시연하여 코패키지 광학에서 이 소재가 필수적이라는 것을 입증했습니다. 스위치 ASIC이 51T 대역폭으로 진화함에 따라 플러그인 광학은 온보드 레이저 엔진으로 전환되어 인듐-인광 웨이퍼 시장에서 기판 수요를 감소시키고 있습니다.

5G 인프라 구축이 mm파 수요를 견인할 것입니다.

상용 5G 백홀은 28GHz 이상에서 작동하지만, 이 주파수 대역에서 InP HBT는 450GHz 이상의 컷오프 주파수와 4.5V 이상의 내전압을 제공합니다. 노키아가 인피네라를 23억 달러에 인수하면서 전송 노드용 InP 코히런트 기술을 확보할 수 있게 되었습니다. 테라헤르츠 주파수를 검토하는 초기 6G 테스트베드는 610GHz까지 검증된 InP HEMT에 의존하고 있습니다. 그 결과, 인화인듐 웨이퍼 시장에서 광 프론트엔드뿐만 아니라 RF 체인용 기판 수요도 증가하고 있습니다.

공급망 취약성이 안정성을 위협합니다.

2024년 중국이 인듐 함유 화합물에 대한 수출 규제를 확대함에 따라 가격 변동성이 커지고 리드타임의 불확실성이 증가했습니다. 현재 유럽과 미국의 웨이퍼 제조업체들은 갈륨과 인의 대체 공급업체를 인증하고 있지만, 원자재 자급자족을 실현하는 데는 시간이 걸립니다. 코히런트의 CHIPS법 프로젝트는 리스크를 어느 정도 완화하지만, 단기적인 조달 압력으로 인해 인화인듐 웨이퍼 시장 전체의 수익률이 압박을 받고 있습니다.

부문 분석

2025년, 100mm급은 인화인듐 웨이퍼 시장에서 43.72%의 점유율을 유지했으며, 비용과 수율의 균형을 중시하는 주류 트랜시버 제품군에 대응하고 있습니다. AIXTRON의 G10-AsP 리액터를 채택한 노키아의 6인치 파일럿 라인을 필두로 150mm 기판으로의 전환이 진행되고 있습니다. 150mm 포맷 인화인듐 웨이퍼 시장 규모는 CAGR 13.15%로 확대될 것으로 예상되며, GaAs와의 비용 격차는 축소될 것으로 예측됩니다. 그러나 6인치를 초과하는 크기에서는 기계적 취약성이 추가 규모 확대의 걸림돌로 작용하기 때문에 두께 균일성이 엄격하게 요구되는 특수 포토닉스 분야에서는 76.2mm 웨이퍼에 대한 수요가 여전히 강세를 보이고 있습니다.

대구경 웨이퍼의 생산 확대는 저탄성률 결정용 캐리어 및 엣지 그립 장비에 대한 투자에 달려 있습니다. 코히런트의 텍사스 확장 계획은 파손을 줄이기 위해 자동 핸들링을 채택하고, 프라임 웨이퍼의 수율을 85% 이상 달성하는 것을 목표로 하고 있습니다. 한편, 50.8mm 웨이퍼는 장비 업데이트에 막대한 비용이 소요되는 대학 연구 개발에서 여전히 사용되고 있습니다. 따라서 2031년까지 인듐-인 웨이퍼 시장에는 다양한 직경 구성이 공존하게 될 것입니다.

2025년에는 불순물이 첨가되지 않은 전도성 기판이 36.18%의 점유율로 1위를 차지하며 광집적 회로의 에피택시화를 뒷받침했습니다. 반절연성 철(Fe) 첨가 웨이퍼는 저소음을 위해 기판 절연이 필요한 5G RF 전력 증폭기 수요 증가에 따라 CAGR 12.93%를 나타낼 것으로 예측됩니다. N형 주석(Sn) 도핑 및 P형 아연(Zn) 도핑 슬라이스는 HEMT 및 HBT 디바이스를 대상으로 하고 있지만, RF 프론트엔드용 인듐-인 웨이퍼 시장 규모에서 철(Fe) 도핑의 성장에 비해 생산량은 여전히 틈새 시장에 머물러 있습니다.

테라헤르츠 IC에 대한 조사에서는 300GHz에서 이득에 대한 배경 도펀트 농도의 영향을 강조하고 있습니다. 페르디난트 브라운 연구소의 HBT는 최적화된 Zn 보상을 통해 450GHz 이상의 동작 주파수(fT)를 달성했으며, 이는 기판 도핑 프로파일이 시스템 레벨의 진보를 어떻게 뒷받침하는지를 잘 보여줍니다. 양자 포토닉스 연구소에서 초순도 및 도핑되지 않은 웨이퍼에 대한 수요가 증가하고 있지만, 이러한 웨이퍼는 표준 전도성 등급의 3배에 달하는 비용으로 인해 가격 탄력성이 제한적입니다.

지역별 분석

아시아태평양은 2025년 매출의 41.55%를 차지했으며, CAGR 12.41%를 나타낼 것으로 예측됩니다. 일본의 JX닛코닛코금속은 정제된 인듐 및 인 원료의 수직계열화 공급 체제를 구축하고 있으며, 대만의 Visual Photonics Epitaxy는 데이터 통신용 레이저용 100mm 웨이퍼의 생산을 확대되고 있습니다. 한국의 첨단소재 생태계는 MOCVD용 소모품을 공급하고 있으며, 지역의 유동성을 강화하고 있습니다. 그러나 중국의 원자재 규제에 따른 수출 허가의 복잡성으로 인해 일본과 한국 생산자들에게 헤지 수요가 발생하고 있으며, 이들 생산자들은 인듐-인 웨이퍼 시장에서 가격 프리미엄을 요구할 수 있습니다.

북미의 점유율은 연방정부의 인센티브 혜택을 받고 있습니다. Coherent가 받은 3,300만 달러의 CHIPS 보조금은 텍사스 주 150mm 라인의 생산 능력을 확장하여 양자 컴퓨팅 및 국방 분야공급망을 확보할 수 있게 해줍니다. MIT 링컨 연구소 등 대학에서는 극저온 양자비트 제어를 위한 InP-on-Si 이미터 시제품을 제작하고 있으며, 이는 향후 상업적 수요의 씨앗이 될 수 있습니다. 그러나 국내 원재료가 해외에 의존하고 있는 것은 여전히 비용구조상의 문제로 남아있습니다.

유럽은 독일과 네덜란드에 걸친 깊은 포토닉스 전문성을 활용하고 있습니다. 페르디난트 브라운 연구소는 프라운호퍼 IZM과 협력하여 테라헤르츠 레이더용 InP HBT를 공동 설계하고 있으며, SMART Photonics는 InP 기반 PIC를 위한 파운드리 서비스를 추진하고 있습니다. Freiberger Compound Materials사는 전위밀도가 1e4 cm-2 미만인 VGF 웨이퍼를 공급하고 있으며, 양자통신 파일럿 프로젝트에서 채택된 실적을 보유하고 있습니다. EU의 연구 보조금이 설비투자를 보완하고 있지만, 에너지 가격 변동으로 인해 아시아 경쟁사 대비 수익률이 압박을 받고 있으며, 이는 인듐-인 웨이퍼 시장 경쟁 구도를 형성하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The indium phosphide wafer market size is expected to grow from USD 198.17 million in 2025 to USD 221.42 million in 2026 and is forecast to reach USD 385.65 million by 2031 at 11.73% CAGR over 2026-2031.

Hyperscale data-center upgrades drive momentum to 800 G and 1.6 T optics, the global rollout of 5 G and preparation for 6 G backhaul, as well as expanding quantum-photonics funding. Larger-diameter substrates lower unit costs, while hybrid InP-on-Si platforms promise further scalability. Asia-Pacific's integrated compound-semiconductor ecosystem anchors supply, yet Western re-shoring programs are accelerating domestic capacity. Competitive intensity stays moderate because crystal-growth know-how, long customer qualifications, and high capex deter new entrants.

Global Indium Phosphide Wafer Market Trends and Insights

High-speed optical-transceiver demand accelerates InP adoption

Cloud operators moving to 800 G and 1.6 T links require edge-emitting lasers and photodiodes that only indium phosphide can provide at the required speeds. Coherent tripled its InP-device output in Q4 2024 and is now sampling 3.2 T transceivers. Source Photonics demonstrated a 1.6 T coherent module using InP-based components, validating the material's indispensability for co-packaged optics. As switch ASICs advance toward 51T bandwidth, pluggable optics give way to on-board laser engines, reducing substrate volumes for the indium phosphide wafer market.

5G infrastructure rollout drives millimeter-wave demand

Commercial 5G backhaul operates above 28 GHz, where InP HBTs offer a cutoff frequency of more than 450 GHz and a breakdown voltage of more than 4.5 V. Nokia's USD 2.3 billion purchase of Infinera secures InP coherent expertise for transport nodes. Early 6G testbeds exploring terahertz frequencies rely on InP HEMTs, which have been validated up to 610 GHz. Consequently, substrate demand rises not only for optical front-ends but also for RF chains within the indium phosphide wafer market.

Supply-chain vulnerabilities threaten stability

China's 2024 expansion of export controls to indium-bearing compounds elevated price volatility and lead-time uncertainty. Western wafer makers now qualify alternative gallium and phosphorus suppliers, yet achieving raw-material self-sufficiency cannot be done quickly. Coherent's CHIPS Act project mitigates some risk, but near-term procurement pressure trims margins across the indium phosphide wafer market.

Other drivers and restraints analyzed in the detailed report include:

- Rising consumer SWIR sensing broadens addressable base

- Quantum-photonics R&D spurs specialty substrate demand

- Cost competitiveness limits penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 100 mm class retained a 43.72% indium phosphide wafer market share in 2025, catering to mainstream transceiver lines that strike a balance between cost and yield. A shift toward 150 mm substrates is underway, driven by Nokia's 6-inch pilot line utilizing AIXTRON G10-AsP reactors. The indium phosphide wafer market size for 150 mm formats is forecasted to grow at a 13.15% CAGR, narrowing the cost gap with GaAs. Yet, mechanical fragility above 6 inches restrains further scale, so 76.2 mm wafers remain relevant for specialty photonics that demand tight thickness uniformity.

Growth in large-diameter output hinges on investment in carriers and edge-grip tools designed for low-modulus crystals. Coherent's Texas expansion adopts automated handling to reduce breakage, targeting yields of over 85% for prime wafers. Meanwhile, 50.8 mm wafers persist in university R&D, where tooling upgrades are prohibitively expensive. A diverse diameter mix therefore co-exists within the indium phosphide wafer market through 2031.

Undoped conductive substrates led with a 36.18% share in 2025, underpinning photonic-integrated-circuit epitaxy. Semi-insulating Fe-doped wafers are projected to post a 12.93% CAGR, accelerating alongside 5G RF-power amplifiers that require substrate isolation for low noise. N-type Sn-doped and P-type Zn-doped slices target HEMT and HBT devices, but their volumes remain niche compared to Fe-doped growth in the indium phosphide wafer market size for RF front-ends.

Terahertz IC research highlights the impact of background dopant levels on gain at 300 GHz. The Ferdinand-Braun-Institut's HBTs utilized tailored Zn compensation to achieve a frequency of operation (fT) exceeding 450 GHz, underscoring how substrate doping profiles underpin system-level advances. Demand for ultra-pure, undoped wafers rises in quantum-photonics labs, but price elasticity is limited because such wafers can cost three times as much as standard conductive grades.

The Indium Phosphide Wafer Market Report is Segmented by Diameter (50. 8mm, 76. 2mm, and More), Wafer Doping Type (Undoped Conductive, and More), Application (Photonics and Optical Transceivers, and More), End-User Industry (Telecommunications and Datacom, and More), Manufacturing Technology (VGF-Grown Bulk, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 41.55% of revenue in 2025 and is projected to grow at a 12.41% CAGR. Japan's JX Nippon Mining and Metals provides a vertically integrated supply of purified indium and phosphorous feedstock, while Taiwan's Visual Photonics Epitaxy ramps 100 mm output for datacom lasers. Korea's advanced-materials ecosystem supplies MOCVD consumables, reinforcing regional liquidity. However, export-license complexities from China's raw-material controls create hedging demand for Japanese and Korean producers, who can command price premiums within the indium phosphide wafer market.

North America's share benefits from federal incentives. Coherent's USD 33 million CHIPS grant expands 150 mm line capacity in Texas to safeguard quantum-computing and defense supply chains. Universities such as MIT Lincoln Laboratory prototype InP-on-Si emitters for cryogenic qubit control, seeding future commercial pull. Yet domestic raw material dependence on overseas sources still challenges the cost structure.

Europe leverages deep photonics expertise across Germany and the Netherlands. Ferdinand-Braun-Institut collaborates with Fraunhofer IZM to co-design InP HBTs for terahertz radar, while SMART Photonics pushes foundry services for InP-based PICs. Freiberger Compound Materials supplies VGF wafers with <1e4 cm-2 dislocation density, securing design wins in quantum-communication pilots. EU research grants offset capex, but energy-price volatility narrows margins versus Asian peers, shaping competitive dynamics of the indium phosphide wafer market.

- Sumitomo Electric Semiconductor Materials, Inc.

- AXT, Inc.

- Freiberger Compound Materials GmbH

- Xiamen Powerway Advanced Material Co., Ltd.

- IQE plc

- II-VI Incorporated (Coherent Corp.)

- JX Nippon Mining & Metals Corporation

- Semiconductor Wafer, Inc.

- Visual Photonics Epitaxy Co., Ltd. (VPEC)

- IntellEPI

- VIGO Photonics S.A.

- Western Minmetals (SC) Corporation

- PAM-XIAMEN (Powerway Wafer)

- SHANGHAI FAMOUS TRADE CO., LTD (ZMKJ)

- Atecom Technology Co., Ltd.

- Ding Ten Industrial Inc.

- Logitech Ltd.

- LandMark Optoelectronics Corporation

- Epihouse Optoelectronics Co., Ltd.

- Century Goldray Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High-speed optical transceiver demand (400G/800G/1.6T)

- 4.2.2 5G and emerging 6G backhaul infrastructure rollout

- 4.2.3 Rising consumer SWIR sensing in smartphones and wearables

- 4.2.4 Quantum photonics R&D programs accelerating InP PIC funding

- 4.2.5 Defense IR-imaging re-shoring mandates boosting domestic InP substrates

- 4.2.6 Migration to 6-inch InP substrates to leverage idle GaAs 6-inch lines

- 4.3 Market Restraints

- 4.3.1 High wafer cost versus Si/GaAs alternatives

- 4.3.2 Supply-chain exposure to Ga-/P-export controls and price volatility

- 4.3.3 Mechanical fragility limiting yields beyond 6-inch wafers

- 4.3.4 Si-photonics hybrid laser platforms reducing pure InP wafer volumes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Diameter

- 5.1.1 50.8 mm

- 5.1.2 76.2 mm

- 5.1.3 100 mm

- 5.1.4 150 mm and Above

- 5.2 By Wafer Doping Type

- 5.2.1 Undoped Conductive

- 5.2.2 N-Type (S / Sn-doped)

- 5.2.3 P-Type (Zn-doped)

- 5.2.4 Semi-insulating (Fe-doped)

- 5.3 By Application

- 5.3.1 Photonics and Optical Transceivers

- 5.3.2 RF and mm-Wave Devices (HEMT, HBT)

- 5.3.3 Photovoltaics and Power Conversion

- 5.3.4 Quantum and Specialty Sensing

- 5.4 By End-user Industry

- 5.4.1 Telecommunications and Datacom

- 5.4.2 Consumer Electronics and Wearables

- 5.4.3 Aerospace and Defense

- 5.4.4 Automotive and Transportation

- 5.4.5 Medical and Life-sciences

- 5.5 By Manufacturing Technology

- 5.5.1 VGF-grown Bulk Wafers

- 5.5.2 LEC/tCZ-grown Bulk Wafers

- 5.5.3 Epitaxial InP-on-Si (Hybrid)

- 5.5.4 MBE/MOCVD Epi-ready Substrates

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Sumitomo Electric Semiconductor Materials, Inc.

- 6.4.2 AXT, Inc.

- 6.4.3 Freiberger Compound Materials GmbH

- 6.4.4 Xiamen Powerway Advanced Material Co., Ltd.

- 6.4.5 IQE plc

- 6.4.6 II-VI Incorporated (Coherent Corp.)

- 6.4.7 JX Nippon Mining & Metals Corporation

- 6.4.8 Semiconductor Wafer, Inc.

- 6.4.9 Visual Photonics Epitaxy Co., Ltd. (VPEC)

- 6.4.10 IntellEPI

- 6.4.11 VIGO Photonics S.A.

- 6.4.12 Western Minmetals (SC) Corporation

- 6.4.13 PAM-XIAMEN (Powerway Wafer)

- 6.4.14 SHANGHAI FAMOUS TRADE CO., LTD (ZMKJ)

- 6.4.15 Atecom Technology Co., Ltd.

- 6.4.16 Ding Ten Industrial Inc.

- 6.4.17 Logitech Ltd.

- 6.4.18 LandMark Optoelectronics Corporation

- 6.4.19 Epihouse Optoelectronics Co., Ltd.

- 6.4.20 Century Goldray Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment