|

시장보고서

상품코드

2035100

가스 크로마토그래피 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Gas Chromatography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

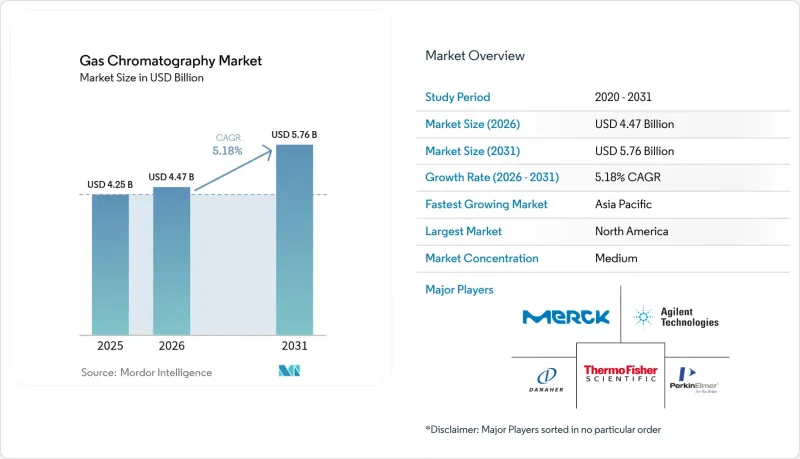

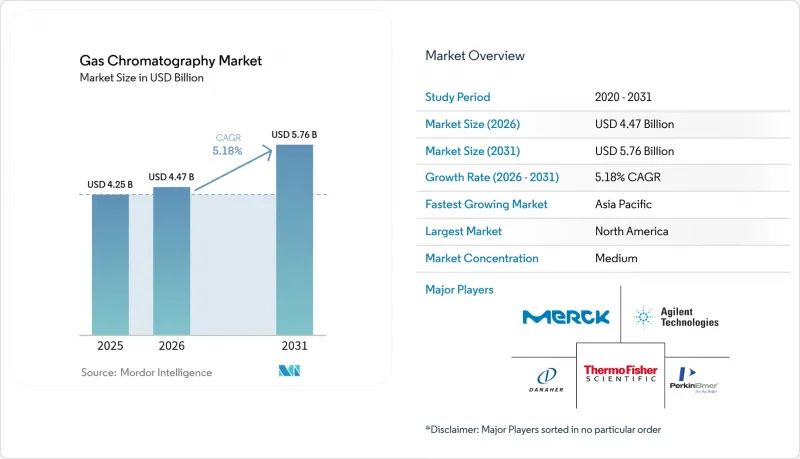

2026년 가스 크로마토그래피 시장 규모는 44억 7,000만 달러로 추정되며 2025년 42억 5,000만 달러에서 성장하여 2031년에는 57억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.18%를 나타낼 것으로 예측됩니다.

환경 및 의약품 테스트에 대한 규제 당국의 감시 강화, 수소 대응 시스템과 같은 빠른 기술 혁신, 그리고 캐리어 가스에 대한 적극적인 공급망 전략이 이러한 꾸준한 성장 궤도를 뒷받침하고 있습니다. 전 세계 연구소는 헬륨에서 수소와 질소로 전환하여 희소 가스 공급에 대한 의존도를 낮추면서 운영 비용을 절감하고 있습니다. 현재, 질량분석법과의 통합이 설비투자의 주요 과제가 되고 있습니다. 이는 분리와 식별을 하나의 분석 프로세스로 통합하여 처리 능력을 향상시키고 데이터 무결성을 높이기 위함입니다. 휴대용 및 마이크로 GC 장비는 현장 분석의 방식을 변화시키고 있으며, 특히 가스 발생기 및 저상비 모세관 컬럼과 같은 액세서리의 혁신은 2030년까지 지속 가능하고 자율적인 운영이 경쟁 우위를 결정하게 될 것임을 시사하고 있습니다.

세계 가스 크로마토그래피 시장 동향 및 인사이트

GC-MS 워크플로우 채택 확대

가스 크로마토그래피와 질량 분석의 연계는 현재 규제 산업에서 표준적인 방법으로 자리 잡았습니다. 제약 파이프라인에서 GC-MS는 불순물 프로파일링에 필수적이며, 신약 신청 서류의 80% 이상이 통합 크로마토그래피 데이터 시스템을 참조하고 있습니다. 환경 보호 기관은 미량 오염물질을 검출하기 위해 GC-MS를 활용하고 있으며, 대기압 화학 이온화(APCI) 등의 기술 개발로 감도는 더욱 향상되고 있습니다. 이러한 통합된 기능은 시료 준비 과정을 단축하고 분석가의 시간을 절약하며 규제 당국의 데이터 무결성 요건을 충족시켜 가스 크로마토그래피 시장의 성장세를 견인하고 있습니다.

의약품 승인에서 품질 관리에서 GC의 역할 확대

FDA의 엄격한 공정 분석 기술 지침은 실시간 모니터링을 의무화하고 있으며, 생산 현장에서 연속적으로 작동할 수 있는 견고한 GC 장비에 대한 투자를 장려하고 있습니다. 2차원 GC 및 불순물 자동 정량 기술은 점점 더 복잡해지는 생물학적 제제에 대응하고, 머신러닝 알고리즘은 피크 식별을 가속화하여 전체 가스 크로마토그래피 시장에서 승인 프로세스를 가속화하는 데 있어 GC의 역할을 강화하고 있습니다.

고급 GC 플랫폼에 대한 대규모 설비 투자

종합적인 2차원 GC-MS 시스템은 대당 50만 달러가 넘을 수 있으며, 설치비 및 유지보수 계약 비용을 더하면 총 비용의 30%가 증가할 수 있습니다. 소규모 연구소는 업그레이드를 미루는 경향이 있지만, 리스 프로그램과 장비 공유 프로그램이 활발해지면서 경제적 장벽이 완화되어 전체 가스 크로마토그래피 시장에서의 사용 확대가 촉진되고 있습니다.

부문 분석

시스템은 여전히 주력 제품이며, 2025년 매출의 38.12%를 차지했습니다. 이러한 탁상형 장비의 가스 크로마토그래피 시장 규모는 업데이트 주기 및 통합형 검출기의 보급에 힘입어 앞으로도 계속 확대될 것입니다. CAGR 9.25%로 성장하고 있는 휴대용 및 마이크로 GC 장비는 비상 대응, 광업 및 연료 유통 분야의 현장 모니터링 요구를 충족시키고 있습니다. FLIR Griffin G510과 같은 장치는 견고한 케이스에 실험실 수준의 감지 성능을 제공합니다. 현장 배치가 가능하기 때문에 시료 처리 시간을 단축하고 실시간 의사결정을 지원합니다. 또한, 연구소는 기술 격차를 해소하고 처리 능력을 표준화하기 위해 오토샘플러를 도입하고 있으며, 분획 수집기는 분획 워크플로우에서 독보적인 위치를 차지하고 있습니다. 검출기 업그레이드와 MEMS 기반 혁신으로 인해 이전에는 접근하기 어려웠던 환경에서도 분석이 가능해짐에 따라 가스 크로마토그래피 시장에서 휴대용 시스템의 중요성이 더욱 커지고 있습니다.

이와 함께 고성능 모듈의 소형화 추세가 진행되고 있습니다. 컬럼 히터, 마이크로 인젝터, 급속 냉각 설계 등의 기술을 통해 크로마토그래피 해상도를 유지하면서 물리적 설치 면적을 줄였습니다. 수소 캐리어 가스의 채택은 휴대용 장비의 전력 예산 및 환경 목표와 일치하여 수소 지원 마이크로 GC에 대한 수요를 촉진하고 있습니다. 지속적인 비용 개선으로 향후 5년간 휴대용 플랫폼이 가스 크로마토그래피 시장 점유율의 더 큰 비중을 차지할 것으로 예측됩니다.

컬럼은 2025년 지출의 45.88%를 차지하여 교체 주기를 예측할 수 있는 소모품으로서의 지위를 반영했습니다. 저상비 모세관 혁신으로 휘발성 황 화합물의 불활성도와 피크 형상이 개선되었습니다. 한편, 연구소가 실린더에서 온디맨드 수소, 질소, 제로 에어로 전환하는 가운데, 가스 발생기는 CAGR 8.28%로 빠르게 성장하고 있습니다. PEAK Scientific의 Noblegen 인수는 이 부문의 생산 능력과 세계 확장에 큰 도움이 될 것입니다. 가드 컬럼, 고순도 커넥터 등의 컬럼 액세서리는 유지보수 작업의 효율성을 유지합니다. 고급 합금으로 제작된 압력 조절기는 수소 환경에도 견딜 수 있으며, RFID 지원 밸브는 교체 시기를 자동으로 알려줍니다. 튜브의 개선으로 데드 볼륨이 감소하고, 피크 대칭이 개선되어 가스를 절약할 수 있습니다. 지속가능성에 대한 관심이 높아지면서 폐기물을 줄이고 장비 가동 시간을 연장하는 고품질 소모품은 가격 프리미엄을 얻으며 가스 크로마토그래피 시장에 직접적인 영향을 미치고 있습니다.

지역별 분석

북미는 2025년 전 세계 매출의 35.98%를 차지했으며, 그 배경에는 미국 환경보호청(EPA)의 엄격한 규제, 견조한 제약 생산, 그리고 분석을 많이 사용하는 산업의 두께가 있습니다. Thermo Fisher의 20억 달러 규모의 국내 확장 계획은 장비 수요의 지속에 대한 확신을 보여줍니다. 미국에서는 1조분의 1 단위 이하의 검출을 요구하는 PFAS 식수 기준이 시행되고 있으며, 이는 실험실의 설비 교체 및 신규 도입을 촉진하고 있습니다. 캐나다와 멕시코는 석유화학제품 생산과 조화로운 환경 프로토콜을 통해 성장을 보완하고 있으며, 예측 기간 동안 장비 교체 주기가 활발하게 유지될 수 있도록 보장하고 있습니다.

유럽은 광범위한 환경 지침과 엄격한 식품 안전 규제로 인해 2위를 유지하고 있습니다. EU 전역의 농약 잔류 규제와 적극적인 미세 플라스틱 대책으로 인해 고감도 GC 플랫폼에 대한 수요가 증가하고 있으며, 수소 전환에 대한 인센티브는 지역 에너지 목표와 일치합니다. 독일, 영국, 프랑스가 수주를 주도하는 반면, 이탈리아와 스페인은 농산물 품질 검사를 통해 성장하고 있습니다. 유럽 시장에서는 저전력으로 수소 분석에 최적화된 기기와 GDPR(EU 개인정보보호규정) 및 GMP 규정 준수를 간소화하는 통합형 데이터 무결성 모듈이 평가받고 있습니다.

아시아태평양은 산업화, 의약품 생산량 증가, 진보적인 모니터링 법규에 힘입어 가장 빠른 성장 궤도인 CAGR 8.29%를 기록했습니다. 중국은 여전히 가장 큰 기여국이지만, 거시경제적 역풍 속에서 벤더들의 매출은 변동이 있었습니다. 일본과 인도는 청정에너지 프로그램과 API 제조 규모 확대를 통해 수요를 가속화하고 있습니다. 한국은 초미량 분석이 필요한 하이테크 산업에 투자하고 있는 반면, 호주의 광업 부문은 현장 조사의 효율화를 위해 휴대용 GC 장비를 채택하고 있습니다. 기술 이전, 현지 생산 및 정부 자금 지원 제도는 대상 시장을 확대하고 향후 가스 크로마토그래피 시장 성장에 있어 이 지역의 역할을 확고히 하고 있습니다.

중동 및 아프리카에서는 석유화학 콤비나트가 품질 관리 실험실을 현대화함에 따라 새로운 모멘텀을 볼 수 있습니다. GCC 국가들의 정유시설 개보수 및 수소 생산에 대한 투자가 안정적인 설비 수주로 이어지고 있습니다. 한편, 남아공의 광업 및 화학 분야에서는 공정 제어를 위해 GC 플랫폼이 활용되고 있습니다. 경제 상황의 변동으로 인해 단기적인 판매량은 억제되고 있지만, 국제 표준에 대한 지역적 적응이 진행됨에 따라 점차 도입이 확대되고 있습니다.

남미에서는 완만하지만 안정적인 확대가 이루어지고 있습니다. 브라질의 제약 및 석유화학 클러스터가 수주의 기반이 되고 있으며, 아르헨티나의 농약잔류검사를 주도하는 것은 아르헨티나의 농업 비즈니스입니다. 지역 무역 협정에 따라 장비의 국경 간 이동이 용이해졌고, 칠레의 구리 광산 사업에서는 배출 규제 준수를 위해 온라인 GC 시스템을 도입하고 있습니다. 환율 변동과 정치 상황의 변화는 불안정한 요인이지만, 현지 유통업체은 금융 및 유지보수 계약을 통해 리스크를 상쇄하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20Gas Chromatography Market size in 2026 is estimated at USD 4.47 billion, growing from 2025 value of USD 4.25 billion with 2031 projections showing USD 5.76 billion, growing at 5.18% CAGR over 2026-2031.

Heightened regulatory scrutiny in environmental and pharmaceutical testing, rapid technology upgrades such as hydrogen-ready systems, and proactive supply-chain strategies around carrier gases underpin this steady trajectory. Laboratories worldwide are moving from helium to hydrogen and nitrogen, trimming operating costs while reducing dependence on scarce noble gas supplies. Integrations with mass spectrometry now dominate capital-spending agendas because they condense separation and identification into a single run, accelerating throughput and improving data integrity. Portable and micro-GC units are reshaping field analytics, and accessory innovations, particularly gas generators and low-phase-ratio capillary columns, signal that sustainable, autonomous operations will define competitive advantage through 2030.

Global Gas Chromatography Market Trends and Insights

Rising Adoption of GC-MS Workflows

Linking gas chromatography with mass spectrometry is now standard practice across regulated industries. Pharmaceutical pipelines rely on GC-MS for impurity profiling, and more than 80% of new-drug dossiers reference integrated chromatography data systems. Environmental agencies use GC-MS to detect contaminants at trace levels, and developments such as atmospheric pressure chemical ionization push sensitivity even further. These combined capabilities shorten sample preparation steps, free analyst time, and meet regulators' data-integrity demands, reinforcing the momentum of the gas chromatography market.

Growing Role of GC in Drug-Approval Quality Controls

Stringent process analytical technology guidance from the FDA mandates real-time monitoring, driving investment in rugged GC units that can run continuously on production floors. Two-dimensional GC and automated impurity quantitation address increasingly complex biologic formulations, while machine-learning algorithms accelerate peak identification, reinforcing GC's role in fast-tracking approvals, across the gas chromatography market.

High Capital Expenditure for Advanced GC Platforms

Comprehensive two-dimensional GC-MS systems can top USD 500,000 per unit, and installation plus service contracts can add 30% to total spend. Smaller laboratories delay upgrades, yet leasing programs and shared-instrument initiatives are gaining momentum, softening the financial barrier and supporting broader access across the gas chromatography market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Shale-Gas & Petrochemical Analytics

- Stringent Air & Water-Quality Regulations Worldwide

- Shortage of Trained Chromatographers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Systems remained the workhorse, contributing 38.12% to 2025 revenue. The gas chromatography market size for these benchtop units will continue to rise, propelled by replacement cycles and integrated detectors. Portable and micro-GC instruments, growing at 9.25% CAGR, meet on-site monitoring needs in emergency response, mining, and fuel distribution. Devices such as the FLIR Griffin G510 deliver laboratory-grade detection in rugged housing. Field deployability saves sample-handling time and supports real-time decision making. Laboratories also add auto-samplers to close skill gaps and standardize throughput, while fraction collectors carve niches in preparative workflows. Detector upgrades and MEMS-based innovations extend analytics to previously inaccessible environments, reinforcing the relevance of portable systems within the gas chromatography market.

A parallel trend is the miniaturization of high-performance modules: on-column heaters, micro-injectors, and rapid cooling designs shrink physical footprints while maintaining chromatographic resolution. The preference for hydrogen carrier gas aligns with portable power budgets and environmental objectives, reinforcing demand for hydrogen-ready micro-GCs. Continuous cost improvements suggest portable platforms will capture a growing slice of gas chromatography market share over the next five years.

Columns captured 45.88% of the 2025 spend, reflecting their status as consumables with predictable replacement intervals. Low-phase-ratio capillary innovations improve inertness and peak shape for volatile sulfur compounds. Gas generators, however, are racing ahead at an 8.28% CAGR as labs swap cylinders for on-demand hydrogen, nitrogen, and zero air. PEAK Scientific's takeover of Noblegen extends capacity and global reach in this segment. Column accessories such as guard columns and high-purity connectors keep maintenance workflows efficient. Pressure regulators made from advanced alloys withstand hydrogen service, while RFID-enabled valves automate replacement alerts. Tubing refinements cut dead volume, sharpening peak symmetry and conserving gas. As sustainability priorities climb, premium consumables that reduce waste and extend instrument uptime earn price premiums, directly influencing the gas chromatography market.

The Gas Chromatography Market is Segmented by Instrument (Systems, Detectors, Auto-Samplers, and More), Accessories & Consumables (Columns, Column Accessories, and More), Detector Type (Flame Ionization, Thermal Conductivity, and More), End User (Pharmaceutical & Biotechnology, Oil & Gas, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributes 35.98% of global revenue in 2025, anchored by robust EPA mandates, strong pharmaceutical output, and a deep bench of analytically intensive industries. Thermo Fisher's USD 2 billion domestic expansion plan asserts confidence in sustained equipment demand. The United States enforces PFAS drinking-water limits that require sub-parts-per-trillion detection, driving laboratory upgrades and new installations. Canada and Mexico supplement growth via petrochemical outputs and harmonized environmental protocols, ensuring replacement cycles stay active throughout the forecast window.

Europe maintains second-tier leadership through far-reaching environmental directives and stringent food-safety regulations. Union-wide pesticide residue controls and vigorous microplastic initiatives elevate demand for sensitive GC platforms, and hydrogen conversion incentives align with regional energy goals. Germany, the United Kingdom, and France dominate orders, while Italy and Spain grow through agricultural quality testing. The European market rewards low-power, hydrogen-optimized instruments and integrated data integrity modules that simplify compliance with GDPR and GMP provisions.

Asia Pacific records the fastest trajectory at 8.29% CAGR, driven by industrialization, rising pharmaceutical output, and progressive monitoring laws. China remains the largest contributor, though vendor sales fluctuated amid macroeconomic headwinds. Japan and India accelerate demand through clean-energy programs and API manufacturing scale-up. South Korea invests in high-tech industries requiring ultra-trace analytics, whereas Australia's mining sector adopts portable GC units for site survey efficiency. Technology transfer, local production, and government funding schemes expand the addressable base, cementing the region's role in future gas chromatography market growth.

Middle East and Africa register emerging momentum as petrochemical complexes modernize quality labs. GCC investments in refinery upgrades and hydrogen production translate into steady instrument orders, while South Africa's mining and chemicals sectors rely on GC platforms for process control. Economic variance tempers short-term volumes, but regional alignment with international standards fosters gradual adoption.

South America presents moderate yet stable expansion. Brazil's pharmaceutical and petrochemical clusters anchor orders, and Argentine agribusiness drives pesticide residue testing. Regional trade pacts ease cross-border equipment movement, and Chilean copper operations integrate online GC systems for emission compliance. Currency swings and political shifts add volatility, but local distributors offset risk by offering financing and maintenance contracts.

- Agilent Technologies

- Shimadzu

- Thermo Fisher Scientific

- Danaher (Cytiva & Pall)

- PerkinElmer

- Merck

- Waters Corporation

- Teledyne Technologies

- Restek

- Chromatotec

- Scion Instruments

- Sartorius

- Air Liquide (Extended Life Sciences)

- Process Sensing Tech (LDetek)

- Hobre Instruments

- Phenomenex

- Bruker

- LECO

- Markes International

- Falcon Analytical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of GC-MS Workflows

- 4.2.2 Growing Role of GC In Drug-Approval Quality Controls

- 4.2.3 Expansion of Shale-Gas & Petrochemical Analytics

- 4.2.4 Stringent Air- & Water-Quality Regulations Worldwide

- 4.2.5 Shift To Hydrogen Carrier Gas Amid Global Helium Shortage

- 4.2.6 Surge In PFAS/Micro-Plastic Monitoring Requirements

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure For Advanced GC Platforms

- 4.3.2 Shortage Of Trained Chromatographers

- 4.3.3 Supply-Chain Volatility for Helium Impacting Uptime

- 4.3.4 Emission-Control Compliance Costs for GC Solvents

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Instrument Type

- 5.1.1 Systems

- 5.1.2 Detectors

- 5.1.3 Auto-samplers

- 5.1.4 Fraction Collectors

- 5.1.5 Micro & Portable GC

- 5.1.6 Other Instruments

- 5.2 By Accessories & Consumables

- 5.2.1 Columns

- 5.2.2 Column Accessories

- 5.2.3 Pressure Regulators

- 5.2.4 Gas Generators

- 5.2.5 Fittings & Tubing

- 5.2.6 Others

- 5.3 By Detector Type

- 5.3.1 Flame Ionization Detector (FID)

- 5.3.2 Thermal Conductivity Detector (TCD)

- 5.3.3 Electron Capture Detector (ECD)

- 5.3.4 Mass-Spectrometry Detector (GC-MS)

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Oil & Gas / Petrochemical Industry

- 5.4.3 Environmental & Waste-water Agencies

- 5.4.4 Food & Beverage Industry

- 5.4.5 Academic & Government Research Institutes

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies

- 6.3.2 Shimadzu Corporation

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Danaher (Cytiva & Pall)

- 6.3.5 PerkinElmer

- 6.3.6 Merck KGaA

- 6.3.7 Waters Corporation

- 6.3.8 Teledyne Technologies

- 6.3.9 Restek Corporation

- 6.3.10 Chromatotec

- 6.3.11 Scion Instruments

- 6.3.12 Sartorius

- 6.3.13 Air Liquide (Extended Life Sciences)

- 6.3.14 Process Sensing Tech (LDetek)

- 6.3.15 Hobre Instruments BV

- 6.3.16 Phenomenex

- 6.3.17 Bruker Corporation

- 6.3.18 LECO Corporation

- 6.3.19 Markes International

- 6.3.20 Falcon Analytical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment