|

시장보고서

상품코드

2035102

폴리프로필렌 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

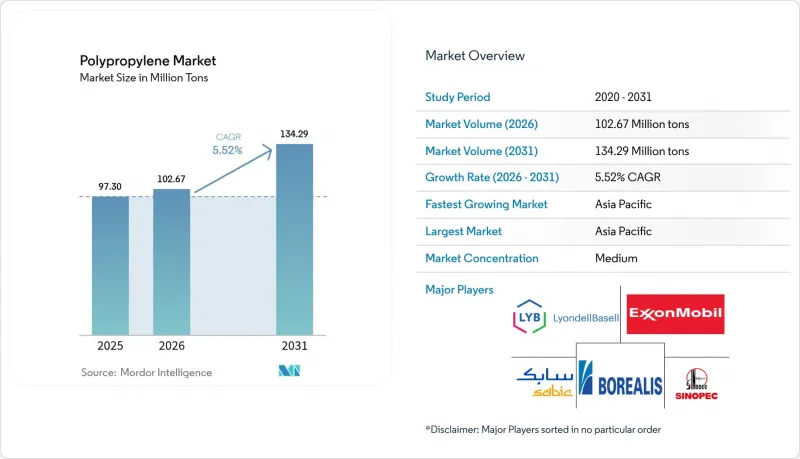

폴리프로필렌 시장 규모는 2025년에 9,730만 톤으로 평가되어 2026년 1억 267만 톤에서 2031년까지 1억 3,429만 톤에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.52%를 나타낼 전망입니다.

이러한 성장을 뒷받침하는 것은 연포장, 자동차 경량화, 부직포 응용 분야의 지속적인 수요이며, 한편으로는 프로판 탈수소(PDH)에 대한 투자가 현금 비용을 절감하고 지역 경쟁력을 강화하는 데 기여하고 있습니다. 생산업체는 고융점 강도를 생성하는 특수 촉매 시스템에 자본을 투자하고 있으며, 이를 통해 재료 사용량과 차량 중량을 줄이는 발포 부품 생산이 가능해졌습니다. 화학적 재활용 관련 공급 계약의 급속한 확대로 재생 원료에 대한 프리미엄 판로가 열리고 있지만, 여전히 버진 수지공급량이 주류를 차지하고 있습니다. 동시에 EU의 플라스틱 세금으로 대표되는 규제 차이로 인해 가공업체들은 단일 소재 구조로 전환해야 하며, 폴리에틸렌 테레프탈레이트(PET) 및 첨단 폴리에틸렌 필름과의 경쟁이 심화되고 있습니다.

세계 폴리프로필렌 시장 동향 및 인사이트

자동차 및 e-모빌리티의 경량화 추진

배터리 항속거리 연장을 목표로 하는 자동차 제조업체들은 특히 계기판과 후드 하부 실드에서 충돌 안전성을 유지하면서 부품 중량을 최대 40%까지 줄일 수 있는 고융점 강도 폴리프로필렌 폼으로 금속 어셈블리를 대체하고 있습니다. 통합 촉매 시스템은 현재 프로필렌 엘라스토머를 생산하고 있으며, 고무 그로밋과 씰을 대체하여 설계자에게 조립 시간을 단축할 수 있는 통합 기회를 제공합니다. Tier 1 공급업체들은 사이클 타임을 최적화하기 위해 금형 전략을 박막 사출 성형으로 전환하고 있으며, 이는 유럽 전역에 걸쳐 성형기 개조 붐을 일으키고 있습니다. 북미 OEM 업체들은 제품 수명 종료 시 재활용 가능성 목표와 수지 선택 매트릭스를 일치시키고 있으며, 이는 단일 소재의 인테리어에 대한 수요를 더욱 촉진하고 있습니다. 그 결과, 자동차 응용 분야의 CAGR은 6.29%로, 폴리프로필렌 시장은 전동화 추세의 중요한 수혜를 받는 시장으로 자리매김했습니다.

단일 소재 연포장에 대한 수요 급증

세계 브랜드들은 2025년까지 포장재 100% 재활용을 위한 자발적 목표를 앞당기고 있으며, 이에 따라 컨버터 업체들은 다층 라미네이트에서 배리어 코팅이 적용된 폴리프로필렌 필름으로 전환을 추진하고 있습니다. 유럽 슈퍼마켓에서는 현재 생산자책임재활용(EPR) 비용을 최소화하기 위해 단일 폴리머 구조로 만들어진 진열용 파우치를 지정하고 있으며, 이로 인해 자체 표면 처리 라인의 도입이 급증하고 있습니다. 아시아태평양의 포장 제조업체들은 규모의 경제를 활용하여 식품 접촉 적합성을 충족시키면서 빠른 가동 속도를 실현하는 무용제 라미네이팅 기술을 채택하고 있습니다. 그 결과, 포장재는 여전히 최대 생산량을 유지하면서 고가격을 책정할 수 있는 고수익률의 장벽 형태로 전환하고 있습니다. 이러한 전환은 기계적 재활용 공정에서 베일의 순도를 높이고, 간접적으로 폴리프로필렌 시장의 소비재 제조업체들 사이에서 재생 폴리프로필렌 펠릿에 대한 수요를 증가시켰습니다.

고성능 대체 수지의 가용성

연포장 제품 개발자들은 폴리프로필렌과 동등한 산소 차단성을 가지면서도 더 낮은 밀봉 온도에서 가공할 수 있는 금속화 폴리에틸렌 필름을 점점 더 많이 시험하고 있으며, 이로 인해 폴리프로필렌이 가지고 있던 비용적 이점을 잃어가고 있습니다. 음료용 캡 분야에서는 폴리에스테르 공급업체들이 화학적 재활용 소재의 함유량과 우수한 투명성을 강조하며 지속가능성을 중시하는 브랜드 가이드라인을 도입하려 하고 있습니다. 아크릴로니트릴 부타디엔 스티렌(ABS)은 높은 표면 광택과 내충격성을 무기로 가전제품 M커버 시장에서 점유율을 지속적으로 확대하며 고급스러움을 추구하는 분야에서 폴리프로필렌을 압박하고 있습니다. 이에 대해 수지 제조업체들은 강성 대 충격비를 개선한 개량형 폴리프로필렌 등급을 출시하여 대응하고 있지만, 그 채택은 컨버터가 금형 재인증을 하려는 의지에 달려있습니다. 재료 선택 팀이 기계적 성능과 재활용 가능성의 목표를 저울질하면서 이 줄다리기가 심화되고 있으며, 이는 예상 CAGR에 0.9 포인트의 마이너스 요인으로 작용하고 있습니다.

부문 분석

2025년 기준, 호모폴리머는 폴리프로필렌 시장 점유율의 69.53%를 차지했으며, 이는 강성 대 중량비가 최우선 순위인 캡, 클로저 및 원사 분야에서 가격 민감도를 반영합니다. 이 부문은 PDH(폴리디에틸렌하이드로카본)의 가격 경쟁력에 힘입어 5.63%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 2031년까지 호모폴리머 폴리프로필렌 시장 규모는 9,337만 톤에 달할 것으로 예측됩니다. 생산자들은 루프 리액터 기술을 사용하여 분자량 분포를 좁히고 강성을 잃지 않으면서 투명성을 높이고 있으며, 이는 유제품 용기의 랜덤 공중합체에서 전환을 촉진하고 있습니다. 코폴리머는 생산량은 적지만 자동차 범퍼, 세탁기 통 등 내충격성이 매우 중요한 부품에서 높은 가격을 유지하고 있습니다. 촉매의 지속적인 개선을 통해 기존의 성능 격차가 줄어들고 있으며, 호모폴리머에 가까운 경제성과 공중합체 수준의 인성을 갖춘 하이브리드 제품이 가능해졌습니다. 이러한 수렴으로 인해 조달 부문은 표면적인 수지 가격이 아닌 총 도입 비용에 주목하게 되었고, 특수 등급이 확대되는 가운데서도 호모폴리머의 압도적인 점유율이 유지되고 있습니다.

2세대 기체상 반응 장치를 통해 신속한 등급 전환이 가능해졌고, 전환 시 발생하는 스크랩을 줄여 소비재 가공업체가 요구하는 적시 물류 체제를 촉진하고 있습니다. 에틸렌-프로필렌 고무 도메인을 활용한 내충격성 공중합체는 신뢰성 높은 저온 연성으로 인해 추운 지역용 자동차 전면 패널에 널리 보급되고 있습니다. 랜덤 코폴리머는 감마선 멸균에 대한 안정성이 요구되는 의료용 주사기 분야에서 틈새 시장을 형성하고 있습니다. 그러나 호모폴리머 블렌드에서 내멸균성 첨가제 증가는 향후 시장 잠식 가능성을 시사하고 있습니다. 첨가제 마스터배치 배합이 성숙해짐에 따라 호모폴리머의 생산량은 공중합체의 증분 성장을 빼앗아 규모의 우위를 확고히 할 수 있습니다.

폴리프로필렌 시장 보고서는 유형(호모폴리머, 코폴리머), 가공 기술(사출 성형, 블로우 성형, 압출 성형, 기타), 최종 사용자 산업(포장, 자동차, 소비재, 전기/전자, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동/아프리카)별로 분류되어 있습니다. 시장 예측은 수량(톤) 기준으로 제공됩니다.

지역별 분석

아시아태평양의 점유율 58.78%는 이 지역의 제조업 규모가 얼마나 큰지 보여주지만, 2025년 중국의 생산량이 68% 급증하면서 공급과잉이 발생하여 수익률을 압박하고, 인도네시아와 필리핀의 반덤핑 조치를 불러일으켰습니다. 현재 각 주 정부는 신규 PDH 프로젝트에 대한 환경 승인을 엄격하게 심사하여 향후 생산 능력의 점진적인 증가를 억제하고 있습니다. 인도에서는 소비재 보급이 확대됨에 따라 다운스트림 수요가 가속화되고 있습니다. 80억 달러 규모의 에탄크래커가 건설될 예정으로, 수입 의존도를 낮추고 아시아 지역 내 무역구조를 재편할 수 있을 것으로 기대됩니다.

북미는 폴리프로필렌 시장에서 PDH의 원료적 우위와 회복세를 보이고 있는 자동차 산업과의 지리적 근접성을 활용하여 남미와 유럽으로 경쟁력 있는 수출을 실현하고 있습니다. 에탄이 풍부한 셰일가스가 프로필렌의 저비용 생산을 뒷받침하고 있으며, 세계 가격 변동에도 불구하고 멕시코만 연안의 플랜트들은 높은 가동률을 유지하고 있습니다. 캐나다 사니아에 위치한 크래커는 이미 구축된 철도 물류망을 통해 중서부 지역 가공업체에 공급되어 지역 공급 안정성을 강화하고 있습니다.

유럽은 에너지 가격 급등과 엄격한 폐기물 규제라는 이중의 역풍에 직면해 있습니다. 생산업체들은 EU의 포장 및 포장 폐기물 규정을 준수하기 위해 영구적인 가동 중단이나 재생 원료 플랫폼으로의 전환을 고려하고 있습니다. 한편, 중동에서 유럽으로 향하는 폴리머 무역의 흐름이 확대되고 있습니다. 이는 통합 정유 및 석유화학 허브가 나프타의 저렴한 가격을 활용하고, 튀르키예의 컨버터가 EU 관세동맹에 대한 무역 관문 역할을 하고 있기 때문입니다. 수입에 크게 의존하고 있는 남미에서는 업스트림부문에 대한 투자유치가 진행되고 있지만, 환율 변동과 정책의 불확실성으로 인해 대규모 신규 프로젝트가 지연되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Polypropylene Market size was valued at 97.30 million tons in 2025 and estimated to grow from 102.67 million tons in 2026 to reach 134.29 million tons by 2031, at a CAGR of 5.52% during the forecast period (2026-2031).

Sustained demand in flexible packaging, automotive lightweighting, and non-woven fiber applications underpins this expansion, while propane-dehydrogenation (PDH) investments compress cash costs and shore up regional competitiveness. Producers are channeling capital toward specialty catalyst systems that yield high-melt-strength grades, enabling foamed parts that cut material use and vehicle weight. Rapid scale-up of chemical-recycling supply agreements is opening premium outlets for recycled feedstocks, although virgin resin volumes still dominate. At the same time, regulatory divergence-exemplified by the EU plastics tax-nudges converters toward mono-material structures, intensifying competition with polyethylene terephthalate and advanced polyethylene films.

Global Polypropylene Market Trends and Insights

Lightweighting Push in Automotive and E-Mobility

Automakers targeting extended battery range are replacing metal assemblies with high-melt-strength polypropylene foams that cut part mass by up to 40% while retaining crashworthiness, particularly in instrument panels and under-hood shields Integrated catalyst systems now produce propylene-based elastomers that displace rubber grommets and seals, offering designers consolidation opportunities that trim assembly time. Tier-one suppliers are shifting tooling strategies toward thin-wall injection molding to optimize cycle times, spurring a fresh wave of press retrofits across Europe. North American OEMs are aligning resin selection matrices with end-of-life recyclability targets, giving an additional boost to mono-material interiors. The resulting 6.29% CAGR for automotive applications positions the polypropylene market as a pivotal beneficiary of electrification trends.

Exploding Demand for Mono-Material Flexible Packaging

Global brands have fast-tracked voluntary targets demanding 100% recyclable packaging by 2025, prompting converters to abandon multi-layer laminates in favor of barrier-coated polypropylene films. European supermarkets now specify shelf-ready pouches made from single-polymer structures to minimize extended-producer-responsibility fees, sparking a surge in proprietary surface-treatment lines. Asia-Pacific packagers, capitalizing on economies of scale, are adopting solvent-free lamination technologies that deliver high-speed runs while meeting food-contact compliance. As a result, packaging retains the largest volume base yet transitions toward higher-margin barrier formats that command premium pricing. The migration also elevates bale purity in mechanical recycling streams, indirectly raising demand for recycled polypropylene pellets among fast-moving consumer-goods companies in the polypropylene market.

Availability of High-Performance Substitute Resins

Product developers in flexible packaging are increasingly testing metallized polyethylene films that match polypropylene's oxygen barrier while delivering lower sealing temperatures, eroding polypropylene's historic cost advantage. In beverage closures, polyester suppliers tout chemical-recycling content and superior clarity to capture sustainability-oriented brand guidelines. Acrylonitrile-butadiene-styrene (ABS) continues to win share in consumer electronics m-covers through higher surface gloss and impact resistance, pressuring polypropylene in premium aesthetics. Resin makers counter by launching inspired polypropylene grades with boosted stiffness-to-impact ratios, but adoption hinges on converter willingness to requalify molds. The tug-of-war intensifies as material selection teams weigh mechanical performance against recyclability targets, creating a net 0.9 percentage-point drag on forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Surge of PDH Units Lowering Cash Cost

- High-Melt-Strength PP Enabling Foamed, Low-Density Applications

- Crude-Oil and Propylene Price Volatility Squeezing Converter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Homopolymer accounted for 69.53% of polypropylene market share in 2025, reflecting price sensitivity in caps, closures, and yarns where stiffness-to-weight ratio is paramount. The segment is forecast to post a 5.63% CAGR supported by PDH-driven cost competitiveness, with the polypropylene market size for homopolymers expected to reach 93.37 million tons by 2031. Producers are narrowing molecular-weight distributions using loop-reactor technology, enhancing clarity without sacrificing rigidity, which aids transition from random copolymer in dairy containers. Copolymers, while smaller in tonnage, secure premium pricing in impact-critical parts such as automotive bumpers and washing-machine tubs. Continuous catalyst upgrades blur the historical performance gap, enabling hybrid products that echo copolymer toughness at near-homopolymer economics. This convergence keeps procurement teams attentive to total-installed-cost rather than headline resin price, sustaining homopolymer's dominant share even as specialty grades expand.

Second-generation gas-phase reactors allow rapid grade switches, reducing transition scrap and favoring just-in-time logistics demanded by consumer-goods converters. Impact copolymers leveraging ethylene-propylene rubber domains gain traction in cold-climate automotive fascia owing to reliable low-temperature ductility. Random copolymers maintain a niche in medical syringes requiring gamma-sterilization stability. Yet rising sterilization-resistant additives in homopolymer blends signal potential future cannibalization. As additive master-batch formulations mature, homopolymer volumes could siphon incremental growth from copolymer, cementing their scale advantage.

The Polypropylene Market Report is Segmented by Type (Homopolymer, Copolymer), Processing Technology (Injection Molding, Blow Molding, Extrusion Molding, and Others), End-User Industry (Packaging, Automotive, Consumer Products, Electrical and Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's 58.78% share underscores the region's manufacturing heft, but China's 68% production surge in 2025 spawned oversupply that pressured margins and spurred anti-dumping actions in Indonesia and the Philippines. Provincial governments are now scrutinizing environmental approvals for new PDH projects, tempering future capacity creep. India's downstream demand is accelerating as consumer-goods penetration deepens; the country's upcoming USD 8 billion ethane cracker promises to narrow import dependency, reshuffling intra-Asian trade.

North America leverages PDH feedstock advantages and proximity to a resurgent automotive sector in the polypropylene market, translating into competitive export offerings to South America and Europe. Ethane-rich shale gas underpins low propylene cash costs, enabling Gulf Coast plants to run at high utilization despite global volatility. Canada's Sarnia-based crackers feed into Midwestern converters through well-established rail logistics, fortifying regional supply security.

Europe faces twin headwinds of elevated energy pricing and stringent waste regulations. Producers are evaluating permanent shutdowns or conversions to recycled-feedstock platforms to stay compliant with the EU Packaging and Packaging Waste Regulation. Concurrently, polymer trade flows from the Middle East into Europe expand as integrated refinery-petrochemical hubs exploit low naphtha costs, while Turkish converters act as trading gateways into the EU customs union. South America, largely import-dependent, is courting upstream investment; however, currency volatility and policy uncertainty delay large-scale grassroots projects.

- Borealis AG

- Braskem

- China National Petroleum Corporation

- Ducor Petrochemicals

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- Hanwha Total Petrochemical Co., Ltd

- HMC Polymers Company Limited

- INEOS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals Inc.

- OQ SAOC

- PJSC SIBUR Holding

- Reliance Industries Limited

- SABIC

- Sinopec

- Sumitomo Chemical Co. Ltd.

- TotalEnergies

- Trinseo PLC

- Vioneo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting Push in Automotive and E-Mobility

- 4.2.2 Exploding Demand for Mono-Material Flexible Packaging

- 4.2.3 Capacity Surge of Propane-Dehydrogenation (PDH) Units Lowering Cash-Cost

- 4.2.4 High-Melt-Strength PP Enabling Foamed, Low-Density Applications

- 4.2.5 Rapid Scale-Up of Chemical-Recycling Supply Agreements

- 4.3 Market Restraints

- 4.3.1 Availability of High-Performance Substitute Resins (PE, PET, ABS)

- 4.3.2 Crude-Oil and Propylene Price Volatility Squeezing Converter Margins

- 4.3.3 EU Plastics Tax Steering Converters Toward Mono-PE Laminates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Price Trends

- 4.7 Import-Export Trends

- 4.8 Feedstock Analysis

- 4.9 Technological Snapshot

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Homopolymer

- 5.1.2 Copolymer

- 5.2 By Processing Technology

- 5.2.1 Injection Molding

- 5.2.2 Blow Molding

- 5.2.3 Extrusion Molding

- 5.2.4 Others

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Consumer Products

- 5.3.4 Electrical and Electronics

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Borealis AG

- 6.4.2 Braskem

- 6.4.3 China National Petroleum Corporation

- 6.4.4 Ducor Petrochemicals

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Formosa Plastics Corporation

- 6.4.7 Hanwha Total Petrochemical Co., Ltd

- 6.4.8 HMC Polymers Company Limited

- 6.4.9 INEOS

- 6.4.10 LG Chem

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Mitsubishi Chemical Group Corporation

- 6.4.13 Mitsui Chemicals Inc.

- 6.4.14 OQ SAOC

- 6.4.15 PJSC SIBUR Holding

- 6.4.16 Reliance Industries Limited

- 6.4.17 SABIC

- 6.4.18 Sinopec

- 6.4.19 Sumitomo Chemical Co. Ltd.

- 6.4.20 TotalEnergies

- 6.4.21 Trinseo PLC

- 6.4.22 Vioneo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment