|

시장보고서

상품코드

2035120

인도의 CCTV 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)India CCTV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

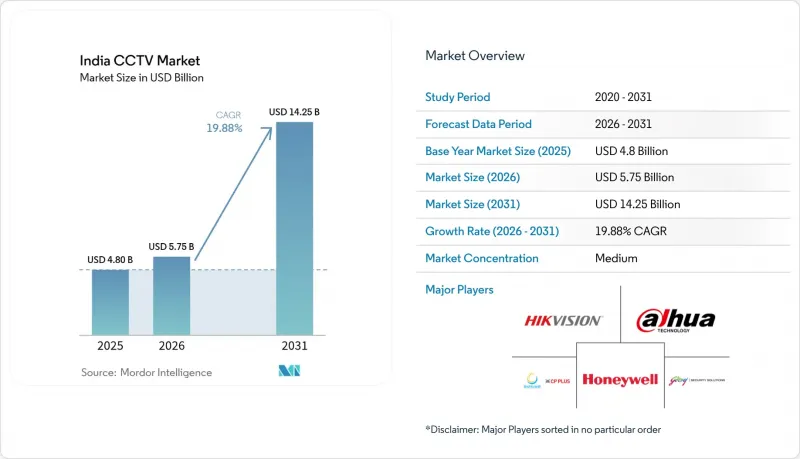

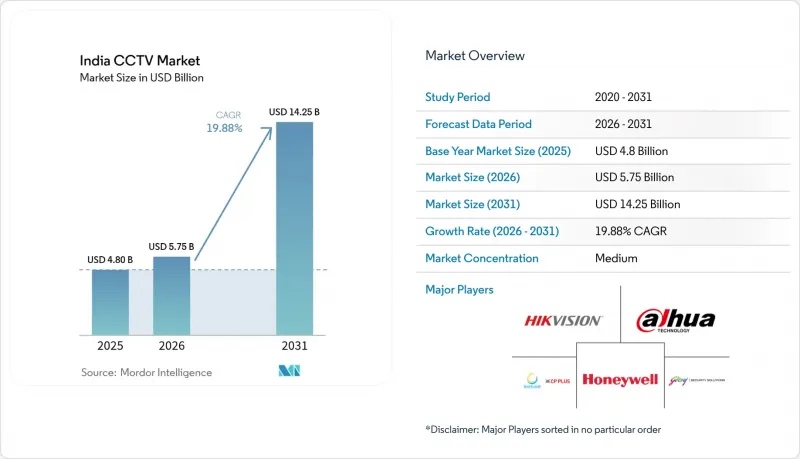

인도의 CCTV 시장 규모는 2025년에 48억 달러로 평가되었고 2026년 57억 5,000만 달러에서 2031년까지 142억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 19.88%를 나타낼 전망입니다.

'스마트 시티 미션'의 전개, 공공 안전 관련 규제 의무화, STQC 인증 의무화에 힘입어 국내 제조를 촉진하는 것이 현재의 성장을 견인하고 있습니다. 이러한 노력은 도시 인프라를 강화하고, 공공 안전을 개선하며, 기술 제조의 자급자족을 촉진하여 시장 확대에 유리한 환경을 조성하는 것을 목표로 하고 있습니다. 또한, 정부가 디지털 전환과 스마트 인프라 개발에 집중하면서 도시 계획 및 공공 안전 시스템에서 첨단 기술 도입이 더욱 가속화되고 있습니다.

100개 도시에 7만 6,000대의 카메라가 설치되었고, 공항과 지하철의 업그레이드도 진행 중이기 때문에 수요는 계속 견조합니다. 도시 지역과 교통 거점에서의 모니터링 시스템 도입은 보안과 운영 효율성에 대한 관심이 높아지고 있음을 보여주며, 시장 성장에 더욱 박차를 가하고 있습니다. 또한, 이러한 시스템에 고급 분석 기술 및 인공지능을 통합함으로써 그 효율성이 향상될 것으로 예상되며, 예측 기간 동안 지속적인 성장에 기여할 것으로 보입니다.

인도의 CCTV 시장 동향과 인사이트

정부의 스마트시티 모니터링 추진

'스마트시티 미션'을 통해 감시는 사후 대응형 경찰 활동에서 예측형 도시 관리로 진화했습니다. 총 1조 4,400억 루피(160억 6,000만 달러)에 달하는 프로젝트의 90%가 2025년 3월까지 확정되었으며, 현재 7만 6,000대의 카메라가 지휘통제센터와 연계되어 교통, 폐기물, 비상대응 모듈에 데이터를 수집하고 있습니다. 조달 프로세스의 표준화를 통해 상호운용성 기준을 충족할 수 있는 공급업체를 우대하고 있습니다. 마디야 프라데시 주 통합관제센터와 같은 클라우드 호스팅 플랫폼은 각 공공 서비스의 자원 최적화를 보여주고 있습니다. 이러한 기반은 교통 체증과 범죄 활동을 사전에 예방하는 예측 분석도 뒷받침하고 있으며, 인도의 CCTV 시장 전체에서 안정적인 수요를 견인하고 있습니다.

공공장소에서의 감시 의무화

주법에 따라 CCTV에 대한 지출은 컴플라이언스 준수에 필수적인 항목이 되고 있습니다. 카르나타카주의 '공공 안전 집행법'은월방문자 수가 500명 이상인 시설에 대해 카메라를 경찰 네트워크에 연결하도록 의무화하고 있으며, 방갈로르의 약 1만 개 매장에 영향을 미치고 있습니다. 이와 같은 법령은 경찰서의 감시 범위에 대한 대법원의 지시에 따른 것으로, 컴플라이언스 미비점을 드러내고 즉각적인 조달을 촉구하고 있습니다. 사양서에는 프레임 속도, 암호화, 보존 기간이 표준화되어 있어 제품의 품질을 높이는 동시에 기준을 충족하지 못하는 수입품을 배제하고 있습니다.

여러 지점에 배포할 때 높은 총소유비용(TCO)

대규모 네트워크에서는 하드웨어 비용을 훨씬 초과하는 비용이 발생합니다. 여기에는 유지보수, 대역폭, 클라우드 스토리지가 포함되며, 3년 이내에 초기 투자비용을 초과할 수 있습니다. 분산된 거점에서는 대부분 위성 회선이나 전용 광섬유 회선이 필요하며, 1개 거점당 연간 5만-10만 루피의 비용이 소요됩니다. 고해상도 영상은 매월 수 테라바이트의 데이터를 생성할 수 있으며, 기업들은 엣지 스토리지나 상위 클라우드 플랜으로 전환해야 합니다. 2, 3급 도시의 숙련공 부족은 설치 비용을 높이고 가동 시작을 지연시킵니다. 이러한 요인으로 인해 중소기업의 도입이 둔화되고 있으며, 수익성이 낮은 부문에서 인도의 CCTV 시장의 성장 속도에 제동이 걸릴 수 있습니다.

부문 분석

2025년 인도의 CCTV 시장에서 아날로그 장비는 51.65%의 점유율을 유지했습니다. 이는 비용 중심의 공공 부문 입찰과 기존 동축 케이블 배선에 힘입은 것입니다. IP 모델은 원격 모니터링과 PoE의 편리함으로 인해 40.55%의 점유율을 차지했습니다. PTZ 카메라는 5.85%를 차지하며, 공항, 석유 터미널 등 광범위한 모니터링에 대응하고 있습니다. AI 탑재 스마트 카메라는 틈새 시장이지만, CAGR 20.55%로 확대될 것으로 예상되며, 지능형 엔드포인트 분야의 인도의 CCTV 시장 규모를 직접적으로 견인할 것으로 예측됩니다.

저렴한 도입 비용과 교체 용이성으로 아날로그 방식은 여전히 존재감을 유지하고 있지만, 2025년 4월 시행된 STQC(보안기술기준)의 규정에 따라 구매자는 사이버 보안 대책이 적용되고 업그레이드가 가능한 장치로 전환하고 있습니다. Aditya Infotech, Prama Hikvision과 같은 국내 기업들은 현재 전자정보기술부의 요구사항을 준수하기 위해 인 디바이스 분석 기능과 보안 부팅 기능을 결합하여 제공합니다. 이에 따라 AI 지원 모델이 아날로그 방식의 점유율을 잠식하며 향후 인도의 CCTV 시장 점유율 추이를 재구성하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The India CCTV market size was valued at USD 4.8 billion in 2025 and estimated to grow from USD 5.75 billion in 2026 to reach USD 14.25 billion by 2031, at a CAGR of 19.88% during the forecast period (2026-2031).

Smart Cities Mission rollouts, mandatory public-safety regulations, and a push for indigenous manufacturing, spurred by the STQC certification mandate, fuel the current growth. These initiatives aim to enhance urban infrastructure, improve public safety, and promote self-reliance in technology manufacturing, creating a favorable environment for market expansion. Additionally, the government's focus on digital transformation and smart infrastructure development further accelerates the adoption of advanced technologies in urban planning and public safety systems.

With 76,000 cameras installed in 100 cities and ongoing upgrades at airports and metros, demand remains robust. The deployment of surveillance systems in urban areas and transportation hubs underscores the growing emphasis on security and operational efficiency, further driving the market's momentum. Moreover, the integration of advanced analytics and artificial intelligence in these systems is expected to enhance their effectiveness, contributing to sustained growth in the forecast period.

India CCTV Market Trends and Insights

Government Smart-City Surveillance Push

The Smart Cities Mission elevated surveillance from reactive policing to predictive city management. With 90% of projects worth INR 1.44 trillion (USD 16.06 billion) finalized by March 2025, 76,000 cameras now integrate with command-and-control centers that funnel data to traffic, waste, and emergency modules. Standardized procurement favors suppliers able to meet interoperability benchmarks. Cloud-hosted platforms, such as Madhya Pradesh's Integrated Control and Command Centre, illustrate resource optimization across utilities. The same backbone supports predictive analytics that pre-empt congestion and criminal activity, reinforcing steady demand across the India CCTV market.

Mandatory Surveillance Regulations for Public Spaces

State legislation is turning CCTV expenditure into a compliance item. Karnataka's Public Safety Enforcement Act requires establishments with 500-plus monthly footfall to connect cameras to police networks, impacting roughly 10,000 Bengaluru outlets. Similar statutes follow Supreme Court directives for police-station coverage, exposing non-compliance gaps that spur immediate procurement. specifications standardize frame rates, encryption, and retention periods, elevating product quality while weeding out sub-standard imports.

High Total Cost of Ownership for Multi-Site Rollouts

Large networks incur costs far beyond hardware, covering maintenance, bandwidth, and cloud storage that can outstrip initial capital outlay within three years. Dispersed sites often need satellite or private fiber links costing INR 50,000-100,000 yearly per location. High-definition video can generate several terabytes monthly, pushing enterprises toward edge storage or higher-tier cloud plans. Skilled labor shortages in tier-2 and tier-3 cities inflate installation fees and delay commissioning. These dynamics slow adoption among SMEs and may cap the expansion speed of the India CCTV market in less bankable segments.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Infrastructure Expansion of Airports and Metro Systems

- AI-Driven Compliance and Safety Analytics Adoption

- Rising Privacy and Data-Protection Obligations (DPDP Act)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Analog units retained a 51.65% share of the India CCTV market in 2025, supported by cost-sensitive public-sector tenders and legacy coaxial cabling. IP models reached 40.55% share thanks to remote monitoring and PoE convenience. PTZ cameras contributed 5.85%, addressing large-area coverage in airports and oil terminals. AI-enabled smart cameras, although niche, are forecast to expand at a 20.55% CAGR, directly lifting the India CCTV market size for intelligent endpoints.

Low acquisition cost and ease of swap-out keep analog in play, yet STQC rules that took effect in April 2025 push buyers toward cyber-secure, upgradeable devices. Domestic firms such as Aditya Infotech and Prama Hikvision now bundle on-device analytics and secure boot to comply with the Ministry of Electronics mandates. AI-ready models thereby erode analog headroom, reshaping future India CCTV market share trajectories.

The India CCTV Market Report is Segmented by Type (Analog Cameras, IP Cameras, PTZ Cameras, AI-Enabled Smart Cameras), End-User Verticals (Government, Industrial and Manufacturing, BFSI, Transportation and Logistics, Residential and Smart Homes, Retail and Hospitality, Healthcare and Education), Connectivity (Wired and Wireless), and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- HIKVISION Digital Technology Co. Ltd (Hikvision India)

- Dahua Technology India Pvt. Ltd

- Aditya Infotech Ltd (CP Plus)

- Honeywell Commercial Security

- Godrej Security Solutions

- Axis Video Systems India Pvt. Ltd

- Bosch Security Systems India

- D-Link India Limited

- Videocon Industries Limited

- Zicom Electronic Security Systems

- Electronic Eye Systems

- Vantage Security Ltd

- Vintron Informatics Ltd

- Digitals India Security Products Pvt. Ltd

- Total Surveillance Solutions Pvt. Ltd

- HFCL Ltd

- Prizor Viztech Limited

- Dixon Technologies (India) Limited

- Sparsh Securitech Pvt. Ltd

- Qubo (Hero Electronix Private Limited)

- Uniview Technology India

- Samsung Hanwha Techwin India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government smart-city surveillance push

- 4.2.2 Mandatory surveillance regulations for public spaces

- 4.2.3 Rapid infrastructure expansion of airports and metros

- 4.2.4 AI-driven compliance and safety analytics adoption

- 4.2.5 Shift toward indigenous manufacturing post STQC/BIS norms

- 4.2.6 Solar-powered edge CCTV deployments in rural schemes

- 4.3 Market Restraints

- 4.3.1 High total cost of ownership for multi-site rollouts

- 4.3.2 Rising privacy and data-protection obligations (DPDP Act)

- 4.3.3 Cyber-security certification burden slowing launches

- 4.3.4 Semiconductor and import restrictions disrupting supply

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 AI video analytics and VSaaS

- 4.6.2 Edge-based low-power cameras

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Domestic Production vs Imports

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Analog Cameras

- 5.1.2 IP Cameras (Non-PTZ)

- 5.1.3 PTZ Cameras

- 5.1.4 AI-enabled Smart Cameras

- 5.2 By End-user Verticals

- 5.2.1 Government

- 5.2.2 Industrial and Manufacturing

- 5.2.3 BFSI

- 5.2.4 Transportation and Logistics

- 5.2.5 Residential and Smart Homes

- 5.2.6 Retail and Hospitality

- 5.2.7 Healthcare and Education

- 5.2.8 Other End-user Verticals

- 5.3 By Connectivity

- 5.3.1 Wired

- 5.3.2 Wireless (Wi-Fi/4G/5G)

- 5.4 By Region

- 5.4.1 North India

- 5.4.2 South India

- 5.4.3 East India

- 5.4.4 West India

- 5.4.5 Central India

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HIKVISION Digital Technology Co. Ltd (Hikvision India)

- 6.4.2 Dahua Technology India Pvt. Ltd

- 6.4.3 Aditya Infotech Ltd (CP Plus)

- 6.4.4 Honeywell Commercial Security

- 6.4.5 Godrej Security Solutions

- 6.4.6 Axis Video Systems India Pvt. Ltd

- 6.4.7 Bosch Security Systems India

- 6.4.8 D-Link India Limited

- 6.4.9 Videocon Industries Limited

- 6.4.10 Zicom Electronic Security Systems

- 6.4.11 Electronic Eye Systems

- 6.4.12 Vantage Security Ltd

- 6.4.13 Vintron Informatics Ltd

- 6.4.14 Digitals India Security Products Pvt. Ltd

- 6.4.15 Total Surveillance Solutions Pvt. Ltd

- 6.4.16 HFCL Ltd

- 6.4.17 Prizor Viztech Limited

- 6.4.18 Dixon Technologies (India) Limited

- 6.4.19 Sparsh Securitech Pvt. Ltd

- 6.4.20 Qubo (Hero Electronix Private Limited)

- 6.4.21 Uniview Technology India

- 6.4.22 Samsung Hanwha Techwin India

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment