|

시장보고서

상품코드

2035131

유럽의 공조 장비 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Air Conditioning Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

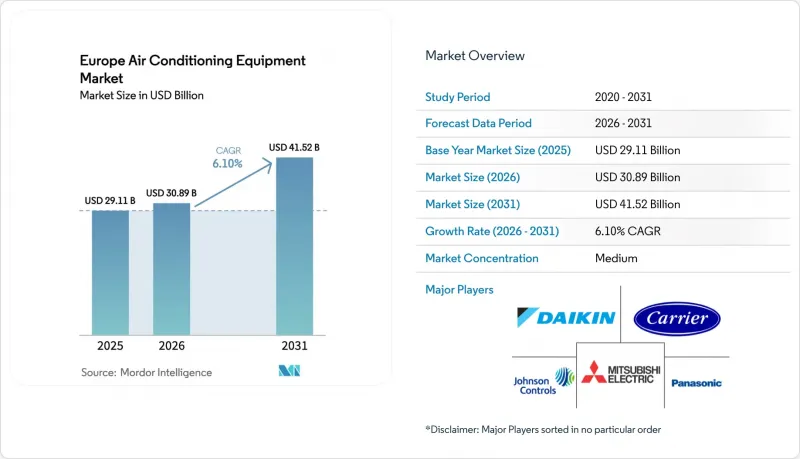

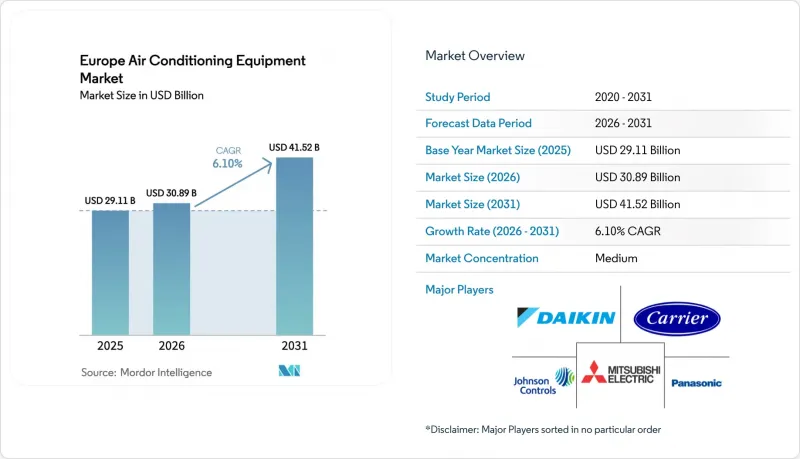

2026년 유럽의 공조 장비 시장 규모는 308억 9,000만 달러로 추계되며 2025년 291억 1,000만 달러에서 성장하여 2031년에는 415억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 6.1%를 나타낼 것으로 예측됩니다.

EU 그린딜에 대한 정책의 빠른 정합성, F가스 할당량 강화, 2030년까지 6,000만 대의 히트펌프 설치라는 REPowerEU의 목표에 따라 유럽의 공조 장비 시장에서는 에너지 효율이 높고 GWP(지구온난화지수)가 낮은 기술이 지속적으로 평가되는 환경이 조성되고 있습니다. 2024년 천연 냉매 제품 라인을 확장하고 인버터 컴프레서 생산 능력을 확보한 제조업체는 현재 리드 타임 단축, 공공 입찰에서의 경쟁 우위, 평균 판매 가격 상승의 혜택을 누리고 있습니다. 또한, 유럽의 공조 장비 시장은 FLAP-D 허브의 데이터센터 건설 붐, 남유럽 대도시의 도시 열섬화 방지 프로그램, 기업 시설 관리자들 사이에서 인기를 끌고 있는 'HVAC-as-a-Service' 계약의 확산으로 인해 수혜를 받고 있습니다. 대형 상업용 바이어들이 프로젝트 중간에 설계 변경 없이 향후 SEER 기준을 충족하는 사양 패키지를 확보하고자 함에 따라 주요 고객에 대한 직접 판매가 가속화되고 있습니다.

유럽의 공조 장비 시장 동향 및 인사이트

EU의 REPower 목표에 힘입어 히트펌프 보급 가속화 추진

회원국들의 규제가 화석연료 보일러의 주요 대안으로 히트펌프에 수렴하고 있으며, 2025년 이후 연간 설치대수는 600만 대에 육박했습니다. 독일에서는 2024년 신축 주택의 76%에서 히트펌프 도입이 승인되었습니다. 프랑스는 부가가치세(VAT) 인하, 보조금, 신속한 허가 절차를 배경으로 2030년까지 국내 생산 능력을 연간 100만 대까지 확대할 계획입니다. 유럽 위원회의 '히트펌프 가속 플랫폼'은 인센티브 제도를 조정하여 제조업체에 전례 없는 수요 가시성을 제공하고, 이를 통해 다년간의 설비 투자 의사결정을 위한 토대를 마련하고 있습니다. 유럽의 공조 장비 시장이 냉난방 겸용 기기로 전환하는 가운데, 압축기와 제어장치 생산을 수직적으로 통합한 공급업체가 가장 큰 우위를 점하고 있습니다.

F가스 규제 개정 이후 저GWP 냉매에 대한 수요 증가 추세

규정(EU) 2024/573에 따라 2025년부터 신규 히트펌프 시스템에서 GWP(지구온난화지수)가 750을 초과하는 냉매의 사용이 금지됩니다. 다이킨은 소매점용 CO2 VRV 시리즈를 출시했고, 미쓰비시 중공업은 GWP675의 R-32 시스템을 출시하는 등 각 제조업체들은 발빠르게 대응하고 있습니다. 2025년 4,290만 톤 CO2 환산 기준에서 2032년까지 900만 톤으로 감축되는 할당량은 HFC공급을 압박하고, 프로판이나 CO2와 같은 대체 냉매의 채택을 가속화하고 있습니다. 서비스 제공업체 네트워크는 현재 가연성 A3 냉매를 다루는 기술자의 기술력 향상에 투자하고 있으며, 이는 애프터 서비스 시장을 더욱 전문화하여 유럽의 공조 장비 시장 전체에서 브랜드 충성도를 강화하고 있습니다.

엄격한 계절별 에너지 효율 비율(SEER) 최소 기준은 비용을 증가시킵니다.

에코디자인 규제에 따라 정적인 실험실 값이 아닌 실사용 환경에서의 효율 테스트가 의무화되었고, 이 변경으로 인해 시스템 개발비용이 7-10% 증가했습니다. 중소 OEM 업체들은 추가 R&D 비용과 인증 획득 비용 조달에 어려움을 겪고 있으며, 이는 업계 구조조정을 촉진하고 유럽의 공조 장비 시장의 엔트리 레벨 제품군에서 모델 선택의 폭을 좁힐 수 있습니다. 건축 기준의 강화로 투자 회수 기간이 더욱 단축되어 가격에 민감한 일부 주택 소유자들은 주택 교체 결정을 미루는 상황이 발생하고 있습니다.

부문 분석

룸 에어컨은 2025년 기준 유럽의 공조 장비 시장에서 27.48%의 점유율을 유지했으며, 소규모 주택 및 소규모 상업시설의 교체 수요를 여전히 주도하고 있습니다. VRF 시스템은 낮은 베이스, 부분부하 시 고효율로 냉난방 동시 운전이 가능하고, 건물 소유주가 EPBD(에너지 성능 지침) 목표를 달성하는 데 도움이 되기 때문에 2031년까지 연평균 복합 성장률(CAGR) 9.15%를 나타낼 것으로 예측됩니다. 소매 체인은 제한된 외관 공간을 최적화하기 위해 다중 분할 설계를 채택하고 있지만, 교외 소매 시설과 물류 시설에서는 옥상 설치형 패키지 유닛이 여전히 선호되고 있습니다. 각 제조업체들은 VRF 제품군을 프로판과 CO2에 대응시켜 F가스 할당량에 대한 영향을 줄이고, 지속가능성 측면에서 차별화를 꾀하고 있습니다.

이 부문에서 경쟁의 초점은 제어 시스템의 상호 운용성과 원격 진단으로 옮겨가고 있습니다. 통합된 BMS 기능을 통해 에너지 관리자는 테넌트의 사용 현황을 가시화하고 설정값을 미세 조정할 수 있으며, 이 기능은 HVAC-as-a-Service 계약의 계약 지속률 향상에 기여하고 있습니다. 휴대용 스팟 쿨러는 특히 남부 수도권의 폭염이 심할 때 긴급 대응이나 행사장 등 틈새 수요에 대응하고 있습니다. 열 저장 기능의 추가는 야간 재생 에너지의 잉여 전력을 낮 시간대 피크 시간대 냉방에 활용할 수 있게 함으로써 유럽의 공조 장비 시장이 보다 광범위한 전력 시스템 균형 조정이라는 목표와 일치하고 있음을 강조합니다.

2025년 기준, 비인버터식 유닛은 유럽의 공조 장비 시장 점유율의 67.95%를 차지했으며, 주요 수요처는 저가형 주거용 채널입니다. 그러나 부품 비용의 하락으로 초기 가격 차이가 줄어들면서 인버터식 솔루션은 CAGR 8.85%로 확대되고 있습니다. 가변 주파수 드라이브는 시동 시 전류 소비를 줄이고, 더 작은 전기 설비를 가능하게 하며, 공급 용량이 제한된 역사적 건축물의 개보수 기회를 창출하고 있습니다. 계절별 효율을 평가하는 전력회사의 리베이트 프로그램은 인버터 설계로 조달을 더욱 기울이고 있습니다.

각 제조업체들은 AI 기반 예측 알고리즘을 통합하여 사용량 및 일기 예보에 따라 압축기 회전수를 조정하고 있습니다. 이 소프트웨어 계층을 통해 유럽의 공조 장비 시장의 가치 제안은 단순한 하드웨어에서 데이터 기반 서비스로 진화하고 있습니다. 냉매 냉각식 파워일렉트로닉스가 50,000시간의 평균 고장 간격(MTBF) 성능을 입증하면서 인버터의 보급을 가로막았던 신뢰성에 대한 우려가 해소되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20Europe Air Conditioning Equipment Market size in 2026 is estimated at USD 30.89 billion, growing from 2025 value of USD 29.11 billion with 2031 projections showing USD 41.52 billion, growing at 6.1% CAGR over 2026-2031.

Rapid policy alignment with the EU Green Deal, stricter F-Gas quotas, and the REPowerEU goal of 60 million installed heat pumps by 2030 are creating an environment in which the Europe air conditioning equipment market consistently rewards energy-efficient, low-GWP technologies. Manufacturers that scaled natural-refrigerant product lines and secured inverter compressor capacity during 2024 now enjoy shorter lead-times, a competitive edge in public tenders, and higher average selling prices. The Europe air conditioning equipment market also benefits from a data-center construction wave in FLAP-D hubs, municipal heat-island programs in Southern capitals, and the growing popularity of HVAC-as-a-Service contracts among corporate facility managers. Direct-to-key-account sales are accelerating as large commercial buyers look to lock in specification packages that meet upcoming SEER thresholds without mid-project redesigns.

Europe Air Conditioning Equipment Market Trends and Insights

Accelerated Heat-Pump Uptake Driven by EU REPower Targets

Member-state mandates are converging on heat pumps as the primary replacement for fossil-fuel boilers, pushing annual installations toward 6 million units from 2025. Germany already approved heat pumps in 76% of new residential buildings in 2024. France is ramping domestic capacity to 1 million units per year by 2030, supported by reduced VAT, grant finance, and fast-track permitting. The European Commission's Heat Pump Accelerator Platform is synchronizing incentive structures, giving manufacturers unprecedented demand visibility that anchors multi-year capex decisions. As the Europe air conditioning equipment market pivots toward hybrid heating-cooling equipment, suppliers with vertically integrated compressor and controls production gain the most leverage.

Rising Demand for Low-GWP Refrigerants Post F-Gas Revision

Regulation (EU) 2024/573 bans refrigerants with GWP > 750 in new heat-pump systems from 2025. Manufacturers have responded swiftly: Daikin debuted CO2 VRV lines for retail formats, and Mitsubishi Heavy Industries rolled out R-32 systems with 675 GWP. The quota cut from 42.9 million t CO2-eq in 2025 to 9 million t by 2032 tightens HFC supply, accelerating adoption of propane and CO2 alternatives. Service-provider networks now invest in technician up-skilling to handle flammable A3 refrigerants, further professionalizing after-sales markets and reinforcing brand loyalty across the Europe air conditioning equipment market.

Stringent Seasonal Energy-Efficiency Ratio (SEER) Minimums Raising Costs

Ecodesign rules now require real-life efficiency testing rather than static lab values, a change that adds 7-10% to system development costs. Smaller OEMs struggle to finance additional R&D and certification, prompting consolidation and potentially reducing model choice in entry-level tiers of the Europe air conditioning equipment market. Tougher building codes further compress payback windows, delaying some replacement decisions among price-sensitive homeowners.

Other drivers and restraints analyzed in the detailed report include:

- Urban Heat-Island Mitigation Projects in Southern Europe

- Data-Centre Expansion in FLAP-D Cities Boosting Precision Cooling

- Supply-Chain Disruptions in Compressors & Micro-chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Room Air Conditioners maintained 27.48% share of the Europe air conditioning equipment market in 2025 and continue to dominate replacement demand in small residential and light commercial spaces. VRF configurations, though starting from a lower base, post a 9.15% CAGR through 2031 by offering simultaneous heating and cooling with partial-load efficiencies that help building owners meet EPBD targets. Retail chains adopt multi-split designs to optimize limited facade space, while rooftop packaged units remain favored in out-of-town retail and logistics. Manufacturers adapt VRF lines to propane and CO2, mitigating F-Gas quota exposure and differentiating on sustainability credentials.

The segment's competitive focus is shifting toward controls interoperability and remote diagnostics. Integrated BMS features allow energy managers to visualize tenant usage and fine-tune setpoints, a capability that raises retention rates in HVAC-as-a-Service contracts. Portable spot coolers serve niche requirements such as emergency response and event venues, especially during severe heat waves in Southern capitals. Thermal storage add-ons extend nighttime renewable surplus into peak daytime cooling, underlining the Europe air conditioning equipment market's alignment with broader grid-balancing objectives.

Non-Inverter units retained 67.95% Europe air conditioning equipment market share in 2025, mainly in low-ticket residential channels. However, inverter solutions expand at 8.85% CAGR as falling component costs close the upfront-price gap. Variable-frequency drives reduce start-up current draw, enabling smaller electrical infrastructure and opening retrofit opportunities in heritage buildings with limited supply capacity. Utility rebate programs that reward seasonal efficiency further skew procurement toward inverter designs.

Manufacturers are integrating AI-based predictive algorithms that adjust compressor speed based on occupancy and weather forecasts. This software layer enhances the Europe air conditioning equipment market value proposition from pure hardware to data-driven services. Reliability concerns that once hindered inverter adoption are dissipating as refrigerant-cooled power electronics demonstrate 50,000-hour MTBF performance in field trials.

The Europe Air Conditioning Equipment Market Report is Segmented by Product Type (Room AC, VRF, Chillers, and More), Cooling Capacity (less Than 8kW, 8-15kW, 15-20kW, Greater Than 20kW), Refrigerant Type (R-32, R-410A, R-290, CO2, and More), Technology (Inverter, Non-Inverter), End User (Residential, Commercial, Industrial), Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Mitsubishi Electric Corp.

- Carrier Global Corp.

- Johnson Controls-Hitachi Air Conditioning

- Panasonic Corp.

- LG Electronics Inc.

- Trane Technologies plc

- Lennox International Inc.

- Danfoss A/S

- Bosch Thermotechnology GmbH

- Emerson Electric Co.

- Samsung Electronics Co. Ltd.

- Gree Electric Appliances Inc. of Zhuhai

- Midea Group Co. Ltd.

- CIAT Group (United Technologies)

- Vertiv Holdings Co.

- Grundfos Holding A/S

- Systemair AB

- FlaktGroup Holding GmbH

- Glen Dimplex Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Heat-Pump Uptake Driven by EU REPower Targets

- 4.2.2 Rising Demand for Low-GWP Refrigerants Post F-Gas Revision

- 4.2.3 Urban Heat-Island Mitigation Projects in Southern Europe

- 4.2.4 Data-Centre Expansion in FLAP-D Cities Boosting Precision Cooling

- 4.2.5 Energy-Efficiency Renovation Wave Under EU Green Deal

- 4.2.6 HVAC-as-a-Service Contracts Gaining Traction Among Facility Managers

- 4.3 Market Restraints

- 4.3.1 Stringent Seasonal Energy-Efficiency Ratio (SEER) Minimums Raising Costs

- 4.3.2 Supply-Chain Disruptions in Compressors and Micro-chips

- 4.3.3 Skilled-Labour Shortage for Low-GWP Refrigerant Handling

- 4.3.4 Rebound Energy-Consumption Concerns Limiting Subsidy Scope

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.5.1 EU Ecodesign and Energy-Labelling Framework

- 4.5.2 F-Gas Phase-Down and PFAS Restrictions

- 4.5.3 Smart, IoT-Enabled Predictive Maintenance Platforms

- 4.5.4 Thermally-Driven and Hybrid AC Technologies

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis

- 4.8 Investments Analysis

- 4.9 Impact Assessment of COVID-19 and Energy-Price Shock

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Room Air Conditioners

- 5.1.1.1 Window / Wall-Mounted Units

- 5.1.1.2 Portable / Spot Coolers

- 5.1.1.3 Single-Split Systems

- 5.1.1.4 Multi-Split Systems

- 5.1.2 Variable Refrigerant Flow (VRF) Systems

- 5.1.3 Rooftop Packaged Units

- 5.1.4 Air Handling Units (AHU)

- 5.1.5 Chillers

- 5.1.5.1 Centrifugal

- 5.1.5.2 Screw

- 5.1.5.3 Scroll

- 5.1.6 Fans and Ventilation Equipment

- 5.1.7 Others (Evaporative Coolers, Thermal Storage, Etc.)

- 5.1.1 Room Air Conditioners

- 5.2 By Cooling Capacity (kW)

- 5.2.1 Less than 8 kW

- 5.2.2 8 - 15 kW

- 5.2.3 15 - 20 kW

- 5.2.4 Greater than 20 kW

- 5.3 By Refrigerant Type

- 5.3.1 R-32

- 5.3.2 R-410A

- 5.3.3 R-290 / Propane

- 5.3.4 CO2 (R-744)

- 5.3.5 Hydro-Fluoro-Olefin (HFO-1234yf/ze)

- 5.4 By Technology

- 5.4.1 Inverter

- 5.4.2 Non-Inverter

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.2.1 Offices and Co-Working Spaces

- 5.5.2.2 Hospitality (Hotels, Resorts)

- 5.5.2.3 Healthcare Facilities

- 5.5.2.4 Retail and Shopping Centres

- 5.5.2.5 Data Centres

- 5.5.3 Industrial

- 5.5.3.1 Food and Beverage Processing

- 5.5.3.2 Pharmaceuticals and Cleanrooms

- 5.6 By Distribution Channel

- 5.6.1 Direct (Manufacturer to Key Accounts)

- 5.6.2 Indirect (Distributors / Installers / E-Commerce)

- 5.7 By Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 France

- 5.7.4 Italy

- 5.7.5 Spain

- 5.7.6 Netherlands

- 5.7.7 Nordics (Sweden, Denmark, Norway, Finland)

- 5.7.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, JVs, Licensing)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 Carrier Global Corp.

- 6.4.4 Johnson Controls-Hitachi Air Conditioning

- 6.4.5 Panasonic Corp.

- 6.4.6 LG Electronics Inc.

- 6.4.7 Trane Technologies plc

- 6.4.8 Lennox International Inc.

- 6.4.9 Danfoss A/S

- 6.4.10 Bosch Thermotechnology GmbH

- 6.4.11 Emerson Electric Co.

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 Gree Electric Appliances Inc. of Zhuhai

- 6.4.14 Midea Group Co. Ltd.

- 6.4.15 CIAT Group (United Technologies)

- 6.4.16 Vertiv Holdings Co.

- 6.4.17 Grundfos Holding A/S

- 6.4.18 Systemair AB

- 6.4.19 FlaktGroup Holding GmbH

- 6.4.20 Glen Dimplex Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment