|

시장보고서

상품코드

2035146

싱가포르의 데이터센터 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Singapore Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

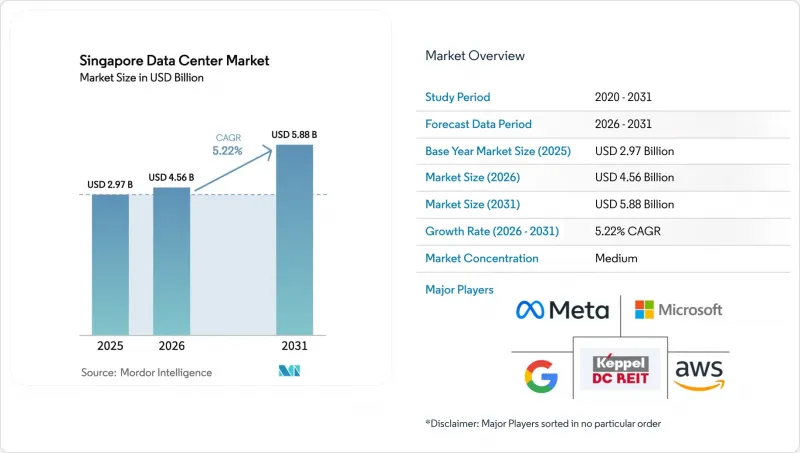

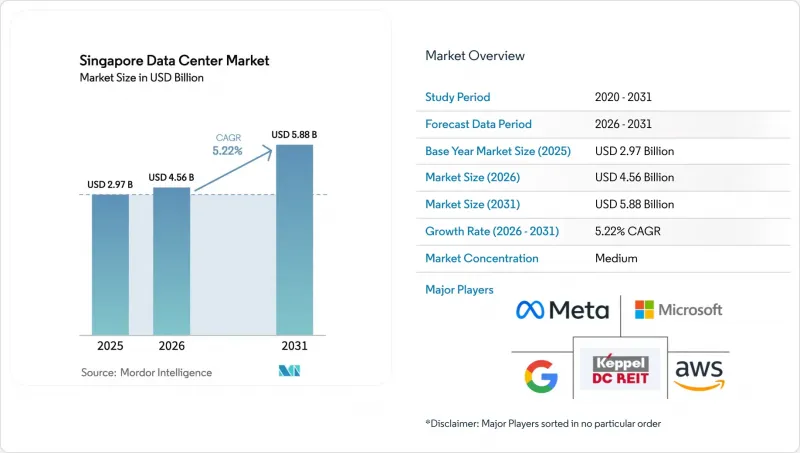

싱가포르의 데이터센터 시장 규모는 2025년에 43억 3,000만 달러로 평가되었고 예측 기간(2026-2031년)에 CAGR 5.22%로 확대되어 2026년 45억 6,000만 달러에서 2031년에는 58억 8,000만 달러에 이를 것으로 추정되고 있습니다.

IT 부하 용량 측면에서 시장은 2025년 2,970MW에서 2030년까지 3,010MW로 확대될 것으로 예상되며, 예측 기간(2025-2030년) 동안 0.28%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 시장 세분화에 따른 점유율 및 예측치는 메가와트(MW) 단위로 계산되어 보고됩니다. 토지와 전력의 제약으로 공급이 부족한 상황에서도 인공지능(AI)에 최적화된 인프라, 하이퍼스케일러의 지속적인 설비 투자, 그리고 동남아시아의 연결 허브로서 싱가포르의 역할이 수요를 뒷받침하고 있습니다. 이러한 모멘텀은 아마존 웹 서비스(AWS)의 120억 싱가포르 달러 규모의 확장 계획과 구글의 누적 50억 달러 투자 약속으로 더욱 강화되고 있으며, 이는 모두 이 지역 클라우드 구축에 있어 싱가포르가 선도적인 위치에 있다는 것을 입증하고 있습니다. 해저 케이블 설치, 캐리어 중립적이고 밀집된 생태계, "친환경" 설계에 대한 신속한 허가 절차는 계속해서 새로운 워크로드를 끌어들이고 있습니다. 한편, '그린 데이터센터 로드맵'을 통해 사업자들은 전력사용효율(PUE) 1.3 미만이라는 목표에 계속 집중하고 있습니다. GPU가 다수 탑재된 랙은 현재 40-60kW의 전력을 소비하고 있으며, 이를 침수 냉각이나 액체 냉각으로 개조하여 시설별 운영 효율과 지속가능성 측면에서 차별화를 꾀하고 있습니다. 이러한 배경에서 각 사업자들은 조호르와 바탐에서 국경을 넘나드는 전략을 추진하여 현지 용량 제한을 완화하는 한편, 타의 추종을 불허하는 네트워크 밀도와 규제 안정성을 이유로 싱가포르의 랙에 여전히 프리미엄 가격을 책정하고 있습니다.

싱가포르의 데이터센터 시장 동향 및 인사이트

하이퍼스케일러로 인한 클라우드 설비투자 급증

아마존이 2030년까지 진행하는 사상 최대 규모인 120억 싱가포르 달러 규모의 프로그램은 15년간의 현지 사업 확장에 이어 GPU 클러스터, 스토리지, 저지연 엣지 노드를 여러 가용성 영역에 걸쳐 확장하는 것입니다. 마이크로소프트가 2025년 3월 발표한 AI 피나클 이니셔티브의 확대는 인프라 확충과 인력 역량 강화를 위한 노력의 결합을 통해 이러한 추세에 부합합니다. 이러한 수십억 달러 규모의 투자는 스위칭 패브릭, 축전지, 첨단 냉각 시스템 공급업체를 유치하여 싱가포르의 데이터센터 시장 전체에 설비투자 파급효과를 가져오고 있습니다. 이러한 투자 규모는 각 하이퍼스케일러들이 태국과 말레이시아에 위성지역을 구축하면서도 싱가포르를 동남아시아에서 대체할 수 없는 컨트롤플레인으로 간주하고 있음을 시사합니다. 그 결과, 2027년까지의 홀세일 코로케이션 파이프라인이 예약으로 가득 차 있고, 사전 임대료율은 몇년만에 최고치를 기록했으며, 기존 부동산 소유자의 협상력이 강화되었습니다. 이미 전력 공급권이나 토지를 확보한 사업자들은 희소한 용량을 프리미엄 수익률로 수익화하고 있어 후발주자들의 진입장벽을 더욱 높이고 있습니다.

AI 지원 고밀도 랙 수요

NVIDIA DGX H100 섀시는 8U에서 최대 10.2kW를 소비하고, Blackwell B200 카드는 개당 1,000W를 초과하기 때문에 랙 밀도가 40-60kW로 상승하여 기존 냉각수 시스템에 도전이 되고 있습니다. Singtel은 Nscale 및 Bridge Alliance와의 제휴를 통해 STT Singapore 6에 설치된 Direct-to-Chip 수냉 및 침수 냉각 포드를 활용한 GPU-as-a-Service 번들을 제공하여 PUE를 1.03의 낮은 수준으로 낮췄습니다. ST Engineering의 Jalan Boon Lay 시설(2027년 인도 예정)은 다양한 가속기 로드맵에 대응할 수 있도록 다양한 냉각 옵션을 표준으로 갖추고 있습니다. 턴키 AI 케이지에 대한 수요로 인해 사업자들은 표준 코로케이션 공간에 비해 10-15%의 가격 프리미엄을 얻을 수 있으며, 사용 가능한 메가와트 수가 제한되어 있는 상황에서도 kW당 수익을 향상시킬 수 있습니다. 금융 서비스 및 첨단 제조 산업 테넌트들은 점점 더 액체 냉각이 가능한 화이트스페이스를 지정하고 있으며, 2020년 이전에 가동된 시설의 경우 리노베이션 주기가 진행되고 있습니다.

제한된 토지와 전력 공급의 제약

타이센과 같은 성숙된 허브의 산업용 구획 임대료는 현재 평방피트당 연간 200싱가포르달러를 넘어서고 있어, 바닥 하중과 엘리베이터 용량의 설계 한계를 뛰어넘는 수직 적층 설계가 요구되고 있습니다. 에너지시장청은 신규 건설에 대한 전력 할당량을 연간 약 200MW로 제한하고 있으며, 이 한도는 이미 초기 단계의 허가 신청 중인 프로젝트에 의해 이미 확보되어 있어 신규 시장 진출기업의 발목을 잡고 있습니다. 20km 북쪽에 위치한 조호르주는 이러한 수요를 활용하여 2025년 2분기에 42개의 프로젝트를 승인하고, 재생에너지 할당제를 통해 요금 우대 혜택을 제공합니다. 싱가포르의 기존 사업자들은 국경을 넘나드는 캠퍼스 확장을 통해 선택권을 확보하는 한편, 시내에 설치가 필수적인 지연에 민감한 랙을 위한 높은 가격대를 유지하고 있습니다. 그러나 토지와 전력 부족으로 인해 납기 장기화, 예비비 증가, 그리고 인근 시장에 대체 용량이 조기에 공급될 경우 테넌트 이탈 리스크가 커질 수 있다는 우려도 있습니다.

부문 분석

2025년 싱가포르의 데이터센터 시장 점유율의 16.10%를 대규모 시설이 차지했습니다. 이는 하이퍼스케일러 포드 및 소버린 컴퓨팅 인클로저를 위해 설계된 기관 투자자를 위한 캠퍼스의 보급을 반영합니다. 이들 시설은 다차원적 중복성, 온사이트 유틸리티, 캐리어 호텔과 인접한 입지를 갖추고 있으며, 표면상 성장률은 둔화되고 있지만 프리미엄 임대료 수준을 유지하고 있습니다. 한편, 중규모 사이트는 기업들이 거버넌스 관리를 유지하면서 엣지 분석을 지역화함에 따라 CAGR 1.17%를 나타낼 것으로 예측됩니다. 평균 밀도 10-15kW의 수직형 설계는 한정된 토지를 최적화하고 고층 건물에 기계, 전기, 배관 설비를 집적화하여 활용하며, 이 접근 방식은 이미 태국 센에서 시범적으로 도입되었습니다. 대규모 및 초대형 카테고리는 용량의 25%에 불과하지만, 48시간의 에너지 저장 버퍼와 캠퍼스 규모의 열 회수 루프를 의무화함으로써 설계 기준에 영향을 미치고 있습니다.

소규모 시설은 정부기관이나 알고리즘 트레이딩 기업들을 위한 고보안 및 에어갭 방식 도입에 특화되어 있습니다. 신규 건설 허가에 필요한 '그린마크 플래티넘'을 포함한 규제적 장애물로 인해 5MW 미만 부지의 단위당 설비투자(CAPEX)가 증가하고 있으며, 소유주들은 자금 조달을 위해 REIT와 제휴할 수밖에 없는 상황입니다. 2025년부터 2030년까지 공급 증가는 그린필드 개발보다는 메자닌층 확장 및 미활용 공간의 리노베이션에 중점을 둘 것입니다. 그 결과, 싱가포르의 데이터센터 시장은 바벨 구조를 유지하게 될 것입니다. 한쪽 끝에는 광활한 하이퍼스케일 시설이, 다른 한쪽 끝에는 컴플라이언스 중심의 소형 노드가 위치하고 있으며, 각 노드는 활발한 2차 서비스 생태계에 의해 뒷받침되고 있습니다.

Tier 3 시설은 전체 용량의 82.55%를 차지하며, 비용과 병렬 유지보수 가능 운영의 최적 균형을 통해 싱가포르의 데이터센터 시장 점유율 1위 자리를 지키고 있습니다. 금융기관과 SaaS 벤더들은 듀얼 리전 페일오버와 결합하면 Tier 3로 충분하다고 생각합니다. 그럼에도 불구하고, AI 학습 중단은 몇 주에 걸친 모델 개발 주기를 중단시켜 막대한 기회 손실을 초래할 수 있기 때문에 Tier 4는 CAGR 2.48%를 나타낼 것으로 예측됩니다. Uptime Institute의 인증을 받은 Tier 4 홀은 싱가포르에서 15-20%의 임대료 프리미엄이 부과되지만, 공실률은 2% 미만으로 유지되고 있습니다.

현재 Tier 1 및 Tier 2 시설은 주로 스테이징, 개발 및 테스트, 비임계 워크로드를 처리하고 있지만, 고객이 서비스 수준 계약(SLA)을 표준화함에 따라 이들 사이트도 점차 이중화를 위한 리노베이션이 진행되고 있습니다. GPU 클러스터는 단일 장애 지점(SPOF)의 영향을 확대하기 때문에 사업자는 Tier 4의 특징인 독립적인 전력 경로와 이중 냉각 루프를 도입해야 합니다. 장기적으로는 Tier 4로 단계적으로 전환될 가능성이 높지만, 비용 중심의 부문에서는 여전히 Tier 3가 주류를 이루고 있기 때문에 싱가포르의 데이터센터 시장은 해외 경쟁에 대한 견고함을 유지하고 있습니다.

"싱가포르의 데이터센터 시장 보고서는 데이터센터 규모(대규모, 초대형, 중대형, 중형, 메가, 소형), 계층 유형(Tier 1 및 2, Tier 3, Tier 4), 데이터센터 유형(하이퍼스케일/자체 구축, 엔터프라이즈/엣지, 코로케이션), 최종 사용자(은행, 금융서비스 및 보험(BFSI), IT 및 ITES, E-커머스, 정부, 기타), 핫스팟(주롱, 타이센, 우드우드, 기타) 등 다양한 데이터센터 유형별로 분류하여 분석하였습니다. 시장 예측은 IT 부하 용량(MW) 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(메가와트)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Singapore Data Center Market size was valued at USD 4.33 billion in 2025 and estimated to grow from USD 4.56 billion in 2026 to reach USD 5.88 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031).

In terms of the IT load capacity, the market is expected to grow from 2.97 thousand megawatts in 2025 to 3.01 thousand megawatts by 2030, at a CAGR of 0.28% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Artificial-intelligence-optimized infrastructure, sustained hyperscaler capital expenditure, and Singapore's role as Southeast Asia's connectivity hub anchor demand even as land and power constraints tighten supply. Momentum is reinforced by Amazon Web Services' SGD 12 billion expansion pledge and Google's cumulative USD 5 billion commitment, both of which underline the city-state's primacy for regional cloud deployments. Subsea cable build-outs, a dense carrier-neutral ecosystem, and expedited permitting for "green" designs continue to attract new workloads, while the Green Data Centre Roadmap keeps operators focused on power-usage effectiveness targets of less than 1.3. GPU-rich racks now draw 40-60 kW, prompting immersion and liquid cooling retrofits that differentiate facilities on operating efficiency and sustainability credentials. Against this backdrop, operators pursue cross-border strategies in Johor and Batam to mitigate local capacity caps yet still price Singapore racks at a premium due to unparalleled network density and regulatory stability.

Singapore Data Center Market Trends and Insights

Heightened Hyperscaler Cloud CapEx Surge

Amazon's record SGD 12 billion program, earmarked through 2030, extends its 15-year presence and scales GPU clusters, storage, and low-latency edge nodes across multiple availability zones. Microsoft's March 2025 expansion of the AI Pinnacle initiative aligns with this trajectory by pairing infrastructure additions with workforce upskilling commitments. Such multi-billion-dollar commitments crowd-in suppliers of switching fabric, battery-energy storage, and advanced cooling, creating a capex multiplier across the Singapore data center market. The scale of spend suggests that hyperscalers view Singapore as an irreplaceable Southeast Asian control plane, even as they activate satellite regions in Thailand and Malaysia. Consequently, wholesale-colocation pipelines are booked out through 2027, pushing pre-lease rates to multi-year highs and consolidating bargaining power among established landlords. Operators that already hold power allocations and land parcels monetize scarce capacity at premium yields, reinforcing barriers to entry for latecomers.

AI-Ready High-Density Rack Demand

NVIDIA DGX H100 chassis consumes up to 10.2 kW in 8U, and Blackwell B200 cards exceed 1,000 watts each, escalating rack densities to 40-60 kW and challenging legacy chilled-water systems. Singtel, through partnerships with Nscale and Bridge Alliance, is offering GPU-as-a-Service bundles that utilize direct-to-chip liquid cooling and immersion pods hosted in STT Singapore 6, achieving a PUE as low as 1.03. ST Engineering's Jalan Boon Lay build, slated for 2027 delivery, bakes in manifold cooling options to accommodate heterogeneous accelerator roadmaps. Demand for turnkey AI cages has enabled operators to capture a 10-15% pricing premium versus standard colocation footprints, boosting revenue per kW even as available megawatts remain capped. Financial services and advanced manufacturing tenants increasingly specify liquid-ready whitespace, prompting retrofit cycles in facilities commissioned before 2020.

Limited Land and Power Supply Constraints

Industrial-zoned plots in mature hubs, such as Tai Seng, now exceed SGD 200 per square foot annually, compelling vertical stack designs that push the floor loading and elevator capacity engineering envelopes. The Energy Market Authority restricts new-build allocations to roughly 200 MW per year, a cap already pre-committed by projects in early-stage permitting, thus stalling greenfield entrants. Johor, located 20 kilometers north, capitalizes on overflow by approving 42 projects in Q2 2025 and offering tariff relief via renewable-energy quotas. Singapore incumbents secure optionality through cross-border campuses while preserving premium price points for latency-sensitive racks that must reside within city limits. However, the land-and-power squeeze elongates delivery lead times, inflates contingency budgets, and amplifies tenant churn risk if alternative capacity opens sooner in neighboring markets.

Other drivers and restraints analyzed in the detailed report include:

- Subsea Cable Landing Expansion Boosting Interconnection

- Green Data Centre Roadmap Power Allocation Incentives

- High Electricity Tariffs Impacting OPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large facilities captured 16.10% of the Singapore data center market share in 2025, reflecting the prevalence of institutional-grade campuses designed for hyperscaler pods and sovereign compute enclosures. Their multidimensional redundancy, on-site utilities, and carrier-hotel-adjacent footprints sustain premium lease rates despite slower headline growth. Medium-sized sites, however, are forecast to expand at a 1.17% CAGR as enterprises regionalize edge analytics while retaining governance control. Vertical designs with an average density of 10-15 kW optimize scarce land and leverage high-rise mechanical, electrical, and plumbing stacks, an approach already piloted in Tai Seng. Massive and mega-scale categories, despite occupying only 25% of the capacity, influence design norms by mandating 48-hour energy-storage buffers and campus-scale heat-recovery loops.

Smaller footprints are increasingly specializing in high-security, air-gapped deployments for government agencies and algorithmic trading firms. Regulatory hurdles, including Green Mark Platinum for new build permits, raise unit CAPEX for sub-5 MW sites, nudging owners to partner with REITs for financing. Between 2025 and 2030, supply additions focus on mezzanine expansions and white-space retrofits rather than greenfield acreage. Consequently, the Singapore data center market maintains a barbell structure: sprawling hyperscale blocks at one end and compact, compliance-driven nodes at the other, each supported by a thriving secondary services ecosystem.

Tier 3 installations comprised 82.55% of total capacity and underpin the Singapore data center market share leadership due to their sweet-spot balance between cost and concurrently maintainable operations. Financial institutions and software-as-a-service vendors view Tier 3 as sufficient when paired with dual-region failover. Nevertheless, Tier 4 is expected to record a 2.48% CAGR, as AI training outages can derail multi-week model development cycles and incur heavy opportunity costs. Uptime-Institute-verified Tier 4 halls command 15-20% rental premiums yet enjoy sub-2% vacancy in Singapore.

Tier 1 and Tier 2 footprints now primarily cater to staging, development-test, and non-critical workloads, but even these sites are gradually being retrofitted with higher redundancy as clients standardize their service-level agreements. GPU clusters magnify the repercussions of single-point-of-failure, pressuring operators to deploy independent electrical paths and twin cooling loops characteristic of Tier 4. Over the long term, a measured migration toward Tier 4 is likely, but cost-sensitive segments will preserve the bulk of Tier 3 dominance, which keeps the Singapore data center market resilient against offshore competition.

The Singapore Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, and More), and Hotspot (Jurong, Tai Seng, Woodlands, and Rest of Singapore). The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Amazon Web Services Inc.

- Google LLC

- Microsoft Corporation

- Meta Platforms Inc.

- Keppel DC REIT Management Pte Ltd.

- Equinix Inc.

- STT GDC Pte Ltd.

- Digital Realty Trust Inc.

- Singapore Telecommunications Ltd. (Nxera)

- AirTrunk Operating Pty Ltd.

- SAP SE

- Tencent Cloud Computing (Beijing) Co. Ltd.

- Global Switch Holdings Limited

- 1-Net Singapore Pte Ltd.

- Princeton Digital Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened hyperscaler cloud CapEx surge

- 4.2.2 AI-ready high-density rack demand

- 4.2.3 Subsea-cable landing expansion boosting interconnection

- 4.2.4 Green Data Centre Roadmap power-allocation incentives

- 4.2.5 Edge- and 5G-led enterprise workload localization

- 4.2.6 Sovereign compute and fintech regulations driving on-island hosting

- 4.3 Market Restraints

- 4.3.1 Limited land and power-supply constraints

- 4.3.2 High electricity tariffs impacting OPEX

- 4.3.3 Strict PUE and sustainability mandates raising CAPEX

- 4.3.4 Talent shortage for AI/HPC operations

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Jurong

- 5.5.2 Tai Seng

- 5.5.3 Woodlands

- 5.5.4 Rest of Singapore

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 Meta Platforms Inc.

- 6.4.5 Keppel DC REIT Management Pte Ltd.

- 6.4.6 Equinix Inc.

- 6.4.7 STT GDC Pte Ltd.

- 6.4.8 Digital Realty Trust Inc.

- 6.4.9 Singapore Telecommunications Ltd. (Nxera)

- 6.4.10 AirTrunk Operating Pty Ltd.

- 6.4.11 SAP SE

- 6.4.12 Tencent Cloud Computing (Beijing) Co. Ltd.

- 6.4.13 Global Switch Holdings Limited

- 6.4.14 1-Net Singapore Pte Ltd.

- 6.4.15 Princeton Digital Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment