|

시장보고서

상품코드

2035165

지속가능성 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sustainability - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

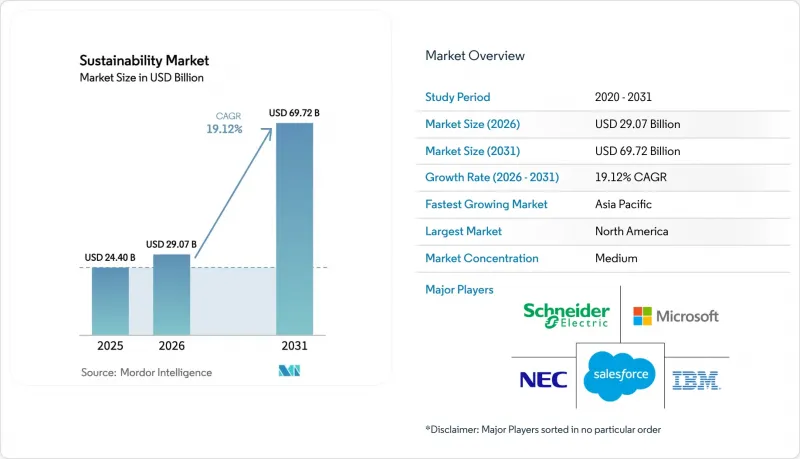

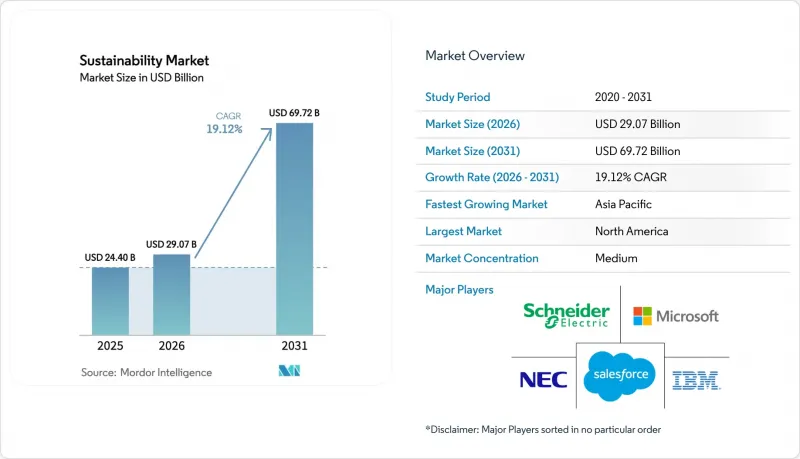

2026년 지속가능성 시장 규모는 290억 7,000만 달러로 추정되고 있어 2025년 244억 달러에서 성장하여 2031년에는 697억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 19.12%를 나타낼 것으로 예측됩니다.

특히 유럽연합(EU)의 '기업 지속가능성 보고 지침'과 미국의 기후 변화 정보공개 규정으로 인해 환경보고는 임의적 활동에서 의무사항으로 변화하고 있습니다. 그 결과, 자동화된 데이터 관리 플랫폼에 대한 수요가 급증하고 있으며, 기업의 순 제로 목표, 지속가능성 연계 금융, 그리고 명확한 비용 절감 가능성을 보여주는 실시간 분석으로 인해 수요가 더욱 증가하고 있습니다. IoT 센서와 인공지능을 통합하는 공급업체들은 기업들이 수동적인 데이터 수집보다 예측적 인사이트를 우선시하게 되면서 일찌감치 우위를 점하고 있습니다. 반면, 표준화 불일치 및 신흥국에서의 전문 인력 부족, 특히 도입 비용에 어려움을 겪는 중소기업의 경우 단기적인 보급을 억제하고 있습니다.

세계 지속가능성 시장 동향 및 인사이트

ESG 보고 의무 규정으로 인해 솔루션 도입 가속화

광범위한 공개 의무는 현재 유럽에서 5만 개 이상의 기업을 대상으로 하고 있으며, 미국 연방 정부 계약업체도 병행 규정에 따라 기후 데이터를 제공해야 합니다. EU 지침에 따라 디지털 태깅이 의무화됨에 따라 구조화된 환경 데이터를 수집하고 보증 워크플로우에 공급할 수 있는 자동 수집 도구에 대한 수요가 급증하고 있습니다. 북미에서는 새로운 주정부 차원의 조치로 인해 관할권별 지표가 추가되어 다국적 기업들은 중복되는 규칙을 조정할 수 있는 플랫폼으로 전환해야 하는 상황에 처해 있습니다. 컴플라이언스 위반에 대한 벌금이 플랫폼 라이선스 비용보다 높은 경우가 많기 때문에 조달 결정에서 가격에 대한 민감도는 상대적으로 낮습니다. XBRL 태깅과 사전 설정된 템플릿을 통합한 공급업체는 예산이 엄격하게 관리되고 있음에도 불구하고, 판매 주기가 단축되는 것을 볼 수 있습니다.

북미의 탄소 회계 수요를 견인하는 넷제로 약속을 주도하고 있습니다.

1,500개 이상의 기업이 과학적 근거에 기반한 목표를 발표했으며, 투자자들은 현재 상세한 Scope 3 배출량 데이터를 요구하고 있습니다. 금융기관은 'Partnership for Carbon Accounting Financials(PCAF)' 기준에 따라 더욱 엄격한 심사를 받고 있으며, 이 기준은 전체 대출 포트폴리오에 대한 대출 관련 배출량 기준선을 요구하고 있습니다. 카테고리별 배출 계수의 복잡성으로 인해 공급업체의 송장을 면밀히 검토하고 수천 개의 활동 코드와 대조할 수 있는 AI 엔진이 도입되고 있습니다. 이러한 추세는 공급망 전체에 영향을 미치고 있으며, 중소 공급업체는 검증된 배출량 데이터를 업로드해야 하며, 그렇지 않으면 거래 자격을 잃을 위험에 직면해 있습니다.

표준의 파편화로 인해 데이터 상호운용성 문제가 발생하고 있습니다.

세계 기업들은 GRI, SASB, TCFD 등 각 프레임워크를 동시에 운용하는 경우가 많으며, 각 프레임워크마다 고유한 지표, 단위, 마감일을 정하고 있습니다. 기존 플랫폼이 통일된 API(애플리케이션 프로그래밍 인터페이스)를 지원하는 경우는 드물고, 기업은 별도의 시스템을 운영하거나 취약한 스프레드시트를 통한 브리징에 의존할 수 밖에 없습니다. 특히 공급업체 간에 공통된 데이터 분류 체계가 없는 경우, 통합 프로젝트는 총소유비용을 증가시키고 투자 회수를 지연시킬 수 있습니다. 지역 표준화 기관은 표준의 통합을 약속하고 있지만, 완전한 통합이 이루어질 때까지의 일정은 여전히 불투명합니다.

부문 분석

2025년에는 솔루션이 지속가능성 시장 수익의 68.12%를 차지했습니다. 이는 데이터 수집의 기반이 되는 센서 어레이, 클라우드 플랫폼, 엣지 프로세싱 게이트웨이가 뒷받침하고 있습니다. 서비스 수익은 CAGR 18.34%로 더 빠르게 성장하고 있으며, 이는 조직이 규제, 운영, 산업별 상황에 맞게 도입을 맞춤화할 필요가 있기 때문입니다. 2026년부터 2031년까지 조달 부서는 가동 일정을 앞당기기 위해 자문 업무와 플랫폼 라이선스 번들 계약을 점점 더 많이 체결할 것입니다. 시스템 통합사업자는 시설 수준의 배출량을 관할권별 배출량 공개 요건에 매핑하는 분류 체계를 설계하여 다운스트림 프로세스의 감사 대응을 보장합니다. 애널리틱스 컨설턴트는 이상값을 해석하고 투자 의사결정에 도움이 되는 인사이트로 전환하여 고객의 초점을 단순한 컴플라이언스 준수에서 성능 최적화로 전환합니다. 대기업이 지출의 대부분을 차지하고 있지만, 간소화된 SaaS 서비스의 등장으로 초기 투자 장벽이 낮아지면서 중견기업들 수요도 증가하고 있습니다. 규제에 대한 심층적인 전문지식과 모듈식 서비스 카탈로그를 제공하는 벤더는 계약 갱신율과 지속적인 수익의 구성 비율을 높이고 있습니다. 서비스 수익률이 하드웨어 수익률보다 높아짐에 따라, 여러 플랫폼 제공업체들은 현재 매니지드 서비스 계약을 중시하고 있으며, 고객과의 친밀감을 강화하는 동시에 다년간의 현금 흐름을 확보하기 위해 관리형 서비스 계약을 중요시하고 있습니다. 이러한 추세는 지속가능성 시장이 성숙기에 접어들었고, 차별화의 핵심은 기본적인 데이터 수집이 아닌 도입 후 가치 제공에 있다는 것을 보여줍니다.

IoT는 지속가능성 시장의 40.21%를 차지하고 있으며, 공장, 사무실, 물류 차량에서 온도, 미립자 물질, 온실가스 데이터를 스트리밍하는 저전력 소모 장치를 제공합니다. 그러나 AI와 애널리틱스는 2031년까지 연평균 복합 성장률(CAGR) 20.08%를 달성할 것으로 예상되며, 경영진의 논의는 데이터 가용성에서 실용적인 선견지명으로 옮겨가고 있습니다. 엣지 AI 모듈은 센서 스트림을 압축 및 전처리하여 대역폭의 제약을 완화하고, 산업 플랜트 내에서 1초 이내에 이상 징후를 감지할 수 있도록 합니다. 클라우드 하이퍼스케일러는 On-Premise 하드웨어 업데이트 없이도 계절적 확장 및 인수에 대응할 수 있는 탄력성을 제공합니다. 블록체인 노드는 공급망의 출처를 증명하고, 위변조가 불가능한 원장을 제공하여 그린워싱의 주장을 막는 역할을 합니다. 디지털 트윈은 실내 공기질 임계값에 따른 HVAC 설정값 조정과 같은 정책 옵션을 시뮬레이션하여 시설 관리자가 시행 전에 트레이드오프를 정량화할 수 있도록 지원합니다. 기술 융합을 통해 스위트 제공업체들은 단일 구독에 AI 라이브러리, 데이터 레이크 커넥터, 로우코드 오케스트레이션 툴을 통합하고 있습니다. 시멘트 가마, 콜드체인 창고 또는 폐수 처리에 초점을 맞춘 스타트업은 범용 프레임워크보다 사전 학습된 알고리즘을 선호하는 사업자로부터 계약을 체결하고 있습니다. 예측 기간 동안 기업이 모델의 출력뿐만 아니라 모델의 발자국도 면밀히 조사함에 따라 알고리즘의 설명 가능성과 탄소 인식 코딩 기술이 점점 더 중요해질 것입니다.

지역별 분석

북미는 2025년 매출의 35.02%를 차지해 지속가능성 시장에서 가장 규모가 큰 지역적 기여를 하는 지역임을 재확인했습니다. 투자 자문사 및 정부 계약업체를 대상으로 하는 연방 공시 규정에 따라, 지속가능성을 주변적인 이슈로 취급하던 분야로까지 컴플라이언스 의무가 확대되었습니다. 캘리포니아 주와 뉴욕주의 주법 의무화가 이러한 추세를 촉진하고 있으며, 여러 주에 걸쳐 있는 기업들은 통일된 플랫폼으로 보고를 통합해야 하는 상황에 직면해 있습니다. 이 지역은 이미 광범위한 클라우드 인프라를 보유하고 있으며, 주요 소프트웨어 벤더를 보유하고 있어 도입까지 소요되는 리드 타임을 단축할 수 있습니다. 재생에너지를 활용한 하이퍼스케일러의 데이터센터와 같은 전략적 노력은 국내 기술 생태계가 어떻게 정책과 혁신의 선순환을 가속화하고 있는지를 잘 보여줍니다. 메탄 회수 분석과 그리드 규모의 전력 저장에 초점을 맞춘 벤처 자금에 의한 스타트업은 지역 솔루션의 다양성을 더욱 풍부하게 하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 21.05%를 나타낼 것으로 예측되며, 지속가능성 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 중국, 인도, 일본의 국가 산업 정책은 공해 대책과 경쟁력 향상이라는 목표를 융합하여 공장에 IoT와 AI를 생산 라인에 도입하도록 추진하고 있습니다. 싱가포르의 녹색 금융 우대 조치와 베트남의 재생에너지 목표는 재정적 조치와 규제 로드맵이 어떻게 융합되어 기업의 도입을 촉진할 수 있는지를 보여줍니다. 이 지역의 높은 제조업 집중도로 인해 작은 효율 향상도 절대적인 배출량 감소로 큰 효과를 가져와 투자 경제성을 높이고 있습니다. 그러나 동남아시아의 소규모 공장은 여전히 기술 인력 부족에 직면하고 있으며, 지역 개발 기관이 보조금 지원 교육 및 클라우드 크레딧을 제공하는 상황으로 인해 진행 상황에 편차가 있습니다.

유럽은 지속가능성 시장의 중요한 축을 담당하고 있습니다. 이는 '유럽 그린딜'과 '기업 지속가능성 보고 지침'에 힘입은 것으로, 모두 기업 전략 전반에 지속가능성을 제도화하고 있습니다. EU의 2024년 옴니버스 ESG 규정은 중복된 공시 요건을 25% 줄이는 것을 목표로 하고 있으며, 기존 프레임워크와 새로운 프레임워크의 데이터 세트를 통합할 수 있는 소프트웨어에 대한 수요를 촉진하고 있습니다. 유럽 기업들은 소비재에 블록체인을 통한 추적성을 실험적으로 도입하여 공급망 감사를 마케팅 차별화 요소로 전환하고 있습니다. 전력회사들은 증가하는 분산형 재생에너지를 흡수하기 위해 스마트그리드 시범사업을 확대하고 있으며, 이는 환경 목표와 에너지 안보의 목적을 결합한 체계적인 접근의 한 예가 되고 있습니다. 규제가 명확해짐에 따라 시장 진출기업들은 순환 경제 분석과 범위 3의 운송 모듈에 초점을 맞춘 제2의 투자 붐을 예상하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20Sustainability market size in 2026 is estimated at USD 29.07 billion, growing from 2025 value of USD 24.40 billion with 2031 projections showing USD 69.72 billion, growing at 19.12% CAGR over 2026-2031.

Rising regulatory alignment, notably the European Union's Corporate Sustainability Reporting Directive and climate-disclosure rules in the United States, is converting environmental reporting from a discretionary activity into a compliance obligation. The resulting surge in demand for automated data-management platforms is reinforced by corporate net-zero targets, sustainability-linked financing, and real-time analytics that demonstrate clear cost-saving potential. Suppliers that integrate IoT sensors with artificial intelligence are capturing early advantage because enterprises now prioritize predictive insights over passive data collection. Meanwhile, a fragmented standards landscape and scarcity of specialist talent in emerging economies temper near-term uptake, especially among smaller businesses that struggle with implementation costs.

Global Sustainability Market Trends and Insights

Mandatory ESG-reporting Regulations Accelerating Solution Uptake

Extensive disclosure mandates now cover more than 50,000 European companies, and parallel rules require climate data from US federal contractors. Digital tagging obligations under the EU directive have created urgent demand for automated collection tools that ingest structured environmental data and feed assurance workflows. In North America, new state-level measures add jurisdiction-specific metrics, pushing multinational firms toward platforms that reconcile overlapping rulesets. Penalties for non-compliance often exceed platform licence fees, making procurement decisions relatively price-insensitive. Suppliers that embed XBRL tagging and pre-configured templates are seeing sales cycles shorten despite budget scrutiny.

Net-zero Commitments Driving Carbon Accounting Demand in North America

More than 1,500 corporations have public science-based targets, and investors now request granular Scope 3 emissions data. Financial institutions face additional scrutiny under the Partnership for Carbon Accounting Financials standard, which requires financed-emissions baselines across lending books. Complexity around category-based emission factors is propelling the adoption of AI engines that can sift supplier invoices and map them against thousands of activity codes. The trend is cascading down supply chains, forcing smaller vendors to upload verified emissions data or risk disqualification.

Fragmented Standards Causing Data-interoperability Issues

Global organizations often juggle GRI, SASB, and TCFD frameworks, each with discrete metrics, units, and cutoff dates. Legacy platforms rarely support harmonized application programming interfaces, forcing firms to run separate instances or rely on brittle spreadsheet bridges. Integration projects inflate the total cost of ownership and postpone the return on investment, especially when suppliers lack shared data taxonomies. Regional standard-setting bodies promise convergence, yet timelines for full alignment remain uncertain.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-linked Financing Pushing Adoption in APAC Manufacturing

- AI-led Resource-efficiency Gains in Heavy Industries

- Skilled-talent Shortage in Southeast-Asian SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 68.12% of sustainability market revenue in 2025, underpinned by sensor arrays, cloud platforms, and edge-processing gateways that anchor data acquisition. Services revenue is climbing faster at an 18.34% CAGR because organizations must tailor deployments to divergent regulatory, operational, and industry contexts. During 2026-2031, procurement teams increasingly bundle advisory engagements with platform licences to accelerate go-live schedules. Systems integrators design taxonomies that map facility-level emissions to jurisdiction-specific disclosures, ensuring downstream audit readiness. Analytics consultants interpret anomalies and translate them into investment-grade insights, moving client focus from pure compliance toward performance optimization. Large enterprises dominate spending, yet mid-market demand is rising as simplified SaaS offerings shrink upfront capital hurdles. Vendors that cultivate deep regulatory expertise and offer modular service catalogs are improving renewal rates and recurring revenue mix. As service margins eclipse hardware margins, several platform providers now emphasize managed-service contracts, locking in multi-year cash flows while strengthening customer intimacy. The pattern signals a maturing sustainability market where differentiation lies in post-deployment value delivery rather than basic data capture.

IoT underpins 40.21% of the sustainability market, supplying low-power devices that stream temperature, particulate, and greenhouse-gas data from factories, offices, and logistics fleets. Yet AI and analytics are projected to deliver a 20.08% CAGR to 2031, shifting boardroom conversations from data availability to actionable foresight. Edge-AI modules compress and preprocess sensor streams, easing bandwidth constraints and enabling sub-second anomaly detection inside industrial plants. Cloud hyperscalers add elasticity that supports seasonal scaling or acquisitions without on-premise hardware refreshes. Blockchain nodes certify provenance in supply chains, providing immutable ledgers that deter greenwashing claims. Digital twins simulate policy choices, such as adjusting HVAC setpoints against indoor-air-quality thresholds, allowing facilities managers to quantify trade-offs before implementation. Technology convergence prompts suite providers to embed AI libraries, data-lake connectors, and low-code orchestration tools inside single subscriptions. Start-ups focusing on sector-specific data models, cement kilns, cold-chain warehousing, or wastewater treatment, win contracts from operators that prefer pre-trained algorithms over generic frameworks. Over the forecast horizon, algorithm explainability and carbon-aware coding techniques will gain prominence as enterprises scrutinize model footprints alongside model outputs.

The Sustainability Market is Segmented by Component (Solutions and Services), by Technology (Internet of Things, and Others), by Application (Green Building, and Others), by End-User Industry (Manufacturing, and Others), by Organization Size (Large Enterprises, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 35.02% of 2025 revenue, reaffirming its position as the largest regional contributor to the sustainability market. Federal disclosure rules that cover investment advisers and government contractors have extended compliance obligations into sectors that previously treated sustainability as peripheral. State mandates in California and New York reinforce momentum, compelling multi-state corporations to consolidate reporting under unified platforms. The region already owns extensive cloud infrastructure and hosts leading software vendors, shortening deployment lead times. Strategic initiatives, such as hyperscaler data centers powered by renewable energy, highlight how domestic technology ecosystems accelerate positive feedback between policy and innovation. Venture-funded start-ups focusing on methane-capture analytics and grid-scale storage further enrich local solution diversity.

Asia-Pacific is forecast to record a 21.05% CAGR to 2031, making it the fastest-growing region within the sustainability market. National industrial policies in China, India, and Japan blend pollution control with competitiveness goals, driving factories to instrument production lines with IoT and AI. Singapore's green-finance incentives and Vietnam's renewable-energy targets illustrate how fiscal measures and regulatory roadmaps converge to stimulate enterprise adoption. The region's manufacturing concentration means even marginal efficiency gains translate into large absolute emissions reductions, reinforcing investment economics. Yet progress is uneven because small factories in Southeast Asia still face skills shortages, prompting regional development agencies to offer subsidized training and cloud credits.

Europe remains a critical pillar in the sustainability market, , propelled by the European Green Deal and the Corporate Sustainability Reporting Directive, both of which institutionalize sustainability across corporate strategy. The EU's 2024 Omnibus ESG Regulation seeks to cut overlapping disclosure requirements by 25%, catalyzing demand for software that can harmonize datasets across legacy and new frameworks. European enterprises experiment with blockchain traceability for consumer goods, transforming supply-chain audits into marketing differentiators. Utility firms expand smart-grid pilots to absorb growing volumes of distributed renewables, exemplifying systemic approaches that combine environmental targets with energy-security objectives. As regulatory clarity improves, market participants anticipate a second investment wave focused on circular-economy analytics and scope-3 transportation modules.

- Schneider Electric

- Microsoft

- IBM

- NEC Corporation

- SAP SE

- Salesforce

- Wolters Kluwer (Enablon)

- Sphera Solutions

- Johnson Controls

- Brambles

- SGS SA

- Morningstar Sustainalytics

- Telefonica

- Deloitte

- EY

- Sanofi

- NRI*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory ESG-Reporting Regulations (EU CSRD, SEC) Accelerating Solution Uptake

- 4.2.2 Net-Zero Commitments Driving Carbon Accounting Demand in North America

- 4.2.3 Sustainability-Linked Financing Pushing Adoption in APAC Manufacturing

- 4.2.4 AI-Led Resource-Efficiency Gains in Heavy Industries (JP, DE)

- 4.2.5 Blockchain-Enabled Ethical Traceability Boosting Retail & Fashion

- 4.2.6 Nature-Based Offset Surge in Brazil Creating Data-Management Needs

- 4.3 Market Restraints

- 4.3.1 Fragmented Standards Causing Data-Interoperability Issues

- 4.3.2 Skilled-Talent Shortage in SE-Asia SMEs

- 4.3.3 High TCO of Industrial IoT in South America

- 4.3.4 Greenwashing Litigation Risk in the US

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Geopolitics Impact Assessment

5 Market Size & Growth Forecasts (Value, USD Bn)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Technology

- 5.2.1 Internet of Things (IoT)

- 5.2.2 AI & Analytics

- 5.2.3 Digital Twin

- 5.2.4 Cloud Computing

- 5.2.5 Blockchain

- 5.3 By Application

- 5.3.1 Green Building

- 5.3.2 Carbon Footprint Management

- 5.3.3 Air & Water Pollution Monitoring

- 5.3.4 Weather Monitoring & Forecasting

- 5.3.5 Fire Detection

- 5.3.6 Crop Monitoring

- 5.3.7 Soil & Forest Monitoring

- 5.4 By End-User Industry

- 5.4.1 Manufacturing

- 5.4.2 Energy & Utilities

- 5.4.3 Transport & Logistics

- 5.4.4 Consumer Goods & Retail

- 5.4.5 Healthcare & Life Sciences

- 5.4.6 BFSI

- 5.4.7 ICT & Telecom

- 5.4.8 Others

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small & Mid-Sized Enterprises

- 5.6 By Deployment Mode

- 5.6.1 Cloud

- 5.6.2 On-Premise

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Peru

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.7.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.7.3.8 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 South Korea

- 5.7.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Qatar

- 5.7.5.4 Kuwait

- 5.7.5.5 Turkey

- 5.7.5.6 Egypt

- 5.7.5.7 South Africa

- 5.7.5.8 Nigeria

- 5.7.5.9 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Schneider Electric

- 6.4.2 Microsoft

- 6.4.3 IBM

- 6.4.4 NEC Corporation

- 6.4.5 SAP SE

- 6.4.6 Salesforce

- 6.4.7 Wolters Kluwer (Enablon)

- 6.4.8 Sphera Solutions

- 6.4.9 Johnson Controls

- 6.4.10 Brambles

- 6.4.11 SGS SA

- 6.4.12 Morningstar Sustainalytics

- 6.4.13 Telefonica

- 6.4.14 Deloitte

- 6.4.15 EY

- 6.4.16 Sanofi

- 6.4.17 NRI*

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment