|

시장보고서

상품코드

2043836

자동 액체 충전기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automatic Liquid Filling Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

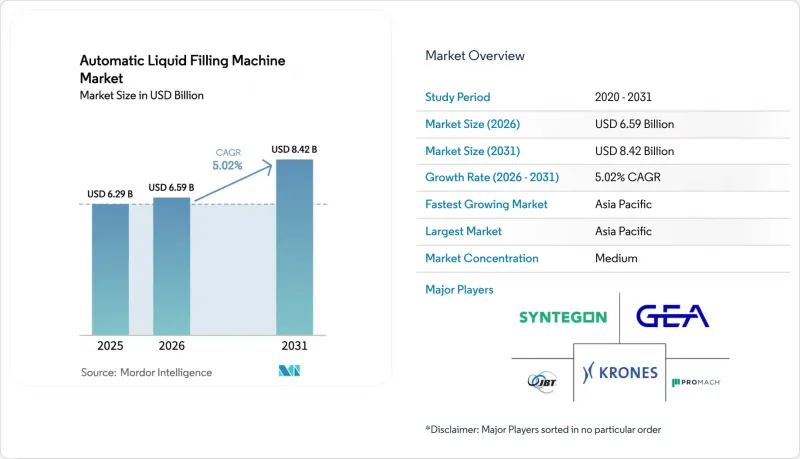

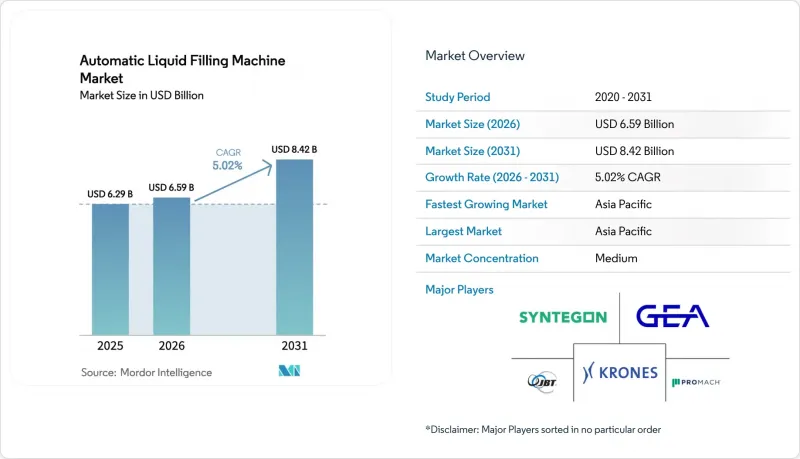

자동 액체 충전기 시장 규모는 2025년에 62억 9,000만 달러로 평가되었고 2026년 65억 9,000만 달러에서 2031년까지 84억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.02%를 나타낼 전망입니다.

제약회사가 무균 가공을 채택하고, 음료 브랜드가 1회용 포장으로 전환하고, 위탁 포장 파트너가 턴키 설비 투자를 부담함에 따라 수요가 가속화되고 있습니다. 고속 음료 라인에서는 여전히 회전식 플랫폼이 주류를 이루고 있지만, 바이오 의약품 및 건강 보조 식품 SKU가 상온 보관이 가능한 패키지로 전환됨에 따라 아이솔레이터 기반 무균 시스템이 빠르게 확대되고 있습니다. 디지털 트윈 분석, 엣지 기반 상태 모니터링, 블록체인을 통한 추적성은 개념증명(PoC) 단계에서 표준 장비 사양으로 전환되고 있으며, 소프트웨어의 부가가치를 포함하지 못하는 OEM 업체들의 수익률을 압박하고 있습니다. 니켈 가격 변동, 위조 부품, 유럽에서 강화된 재생 소재 함유량 규제가 공급망에 압박을 가하고 있지만, 동시에 구매자들이 경량 PET 설계와 장기적인 철강 조달 계약으로 향하고 있습니다.

세계 자동 액체 충전기 시장 동향 및 인사이트

엄격한 위생 기준이 무균 충전 라인에 대한 수요를 주도합니다.

2023년 미국 FDA 부속서 1 개정으로 실시간 오염 모니터링 요건이 강화됨에 따라 제약 공장은 열 스트레스 없이 6 로그의 포자 감소를 실현하는 아이솔레이터식 충전기를 도입해야 합니다. 이와 병행하여 유럽위생공학설계그룹(EHEDG)은 2024년 가이드라인을 개정하여 공구 없는 분해와 0.8마이크로미터 미만의 표면 거칠기를 의무화했습니다. 이로 인해 설비 투자는 증가하지만, 검증 리드 타임은 20% 단축됩니다. 상온 안정형 바이알 충전이 보편화됨에 따라 mRNA 백신에 대한 콜드체인 제약이 완화되고 있으며, 원격지의 냉장 창고 비용이 절감되고 있습니다. 음료 제조업체는 또한 교대 근무 중 아데노신 삼인산(ATP) 생발광 스왑 검사를 의무화하는 3-A 위생 표준을 준수하기 위해 무균 기술을 채택하고 있습니다. 이러한 규제 변화와 맞물려 기존에는 핫필이나 터널식 멸균장치가 주류를 이루던 분야에서도 턴키 방식의 무균라인으로 조달 판단이 기울고 있습니다.

인더스트리 4.0을 통한 리노베이션, IoT 지원 센서 및 분석

압력에 민감한 음료 생산 공정의 가동 중단 시간은 시간당 2만 달러가 넘을 수 있기 때문에 생산자들은 치명적인 고장이 발생하기 전에 베어링의 마모를 경고하는 예지보전 시스템을 도입하고 있습니다. GEA의 디지털 트윈 플랫폼은 200개 이상의 임베디드 센서에서 토크, 진동, 온도 데이터를 스트리밍하여 고장이 발생하기 72시간 전에 기술자를 배치합니다. 무균 제조 시설에서는 그 혜택이 특히 큽니다. 예기치 않은 중단이 발생하면 전체 CIP(고정식 세척) 및 멸균 사이클이 필요하고, 라인이 반 교대 근무 시간 동안 중단될 수 있기 때문입니다. 블록체인으로 보호되는 배치 기록은 바이알 및 주사기 포장의 일련화 기반으로서 부상하고 있으며, 규제 당국이 QR 코드를 스캔하여 변조 불가능한 충전 중량 이력을 확인할 수 있도록 하고 있습니다. 분당 1,200개의 병을 처리할 수 있는 비전 가이드 불량품 선별 시스템은 엣지 AI와 하이퍼스펙트럼 카메라를 결합하여 기존 광전 센서에 비해 오감지율을 15% 감소시켰습니다.

전자동 로터리 시스템의 고가의 초기 설비 투자

턴키 방식의 회전식 무균 충전기의 가격은 150만 달러에서 400만 달러에 달하고, 많은 중견 음료 브랜드가 시장 진입에 어려움을 겪고 있습니다. 리스 금융이나 장비 구독 계약은 초기 비용의 부담을 덜어주지만, 중소기업이 보장하기 어려운 다년간의 생산량 약정을 수반하기 때문에 중소기업이 감당하기 어렵습니다. 제약 라인의 검증 비용은 하드웨어 비용에 더해 20-30% 추가되며, 청구 금액이 유로 또는 달러에 연동되어 있는 경우 환율 변동으로 인해 비용이 더욱 상승합니다. OEM 업체들은 30만 달러에서 60만 달러의 가격대에서 단계적 생산능력 증대가 가능한 모듈식 인라인 시스템을 제공함으로써 대응하고 있지만, 대량 생산되는 SKU의 경우 처리 능력의 트레이드오프가 여전히 큰 과제입니다.

부문 분석

제약 및 프리미엄 음료 제조업체가 콜드체인 비용을 피할 수 있는 상온 보관이 가능한 SKU를 선택함에 따라 무균 플랫폼은 2031년까지 연평균 6.43%의 성장률을 보일 것으로 예측됩니다. 한편, 회전식 시스템은 탄산음료 분야에서 독보적인 처리 능력으로 인해 2025년 자동 액체 충진기 시장 점유율 40.93%를 유지했습니다. 인라인 및 선형 충전기는 주당 20개 이상의 SKU를 취급하는 크래프트 맥주 양조장 및 특수 식품 공장에서 여전히 인기가 있습니다. 직선형 레이아웃으로 설치 면적을 25% 줄일 수 있고, 위생 관리를 빠르게 할 수 있기 때문입니다. 모노블록 린스-필-캡(RFC) 설계는 3교대 생산 체제를 유지하기 위해 45분 이내에 CIP(정위치 세척) 사이클을 완료해야 하는 유제품 가공업체들이 선호하고 있습니다.

프리필드시린지용 아이솔레이터가 장착된 충전기는 현재 로봇에 의한 네스트 로딩 및 자동 스토퍼 설치 기능을 갖추고 있어 A등급 구역에서 사람의 개입을 배제하고 있습니다. 2025년에 발표된 GEA의 모듈식 무균 플랫폼은 로터리 피스톤 헤드와 페리스탈틱 헤드를 공구 없이 교체할 수 있어 검증 기간을 6주 이내로 단축할 수 있습니다. 인라인 설비는 속도가 느리고, 배치 중간에 샘플링을 위해 일시 정지할 수 있는 것이 필수적인 500-1,000개 단위 규모의 임상시험 생산에 적합합니다. ISO 13485, ISO 22716 및 FDA 21 CFR Part 11 표준의 통합으로 화장품 브랜드조차도 데드스페이스가 매우 적고 손끝에서 안전하게 교체할 수 있는 부품을 갖춘 '위생 설계(HBD)' 아키텍처로 전환하고 있습니다.

체적 시스템은 2025년 28.12%의 점유율을 차지했습니다. 이는 피스톤식 또는 자기유량계로 계량하는 경우 제품 밀도가 변동해도 정확도가 유지되는 반면, 중량식 라인에서는 지속적으로 재교정이 필요하기 때문입니다. 무균 및 장기보관 가능한 구성은 무방부제 음료에 대한 소비자 수요와 FDA의 무균 가공 장려 정책과 맞물려 CAGR 6.67%를 기록했습니다. 탄산음료 공장에서는 CO2를 절약하기 위해 가압식 및 등압식 충전기가 주류를 이루고 있지만, 와인 및 증류주 분야에서는 기포 발생을 방지하고 ±1ml의 공차 계약을 충족하는 진공식 설계에 밀려 중력식 장비는 점유율이 떨어지고 있습니다.

투명 증류주 및 식용유 분야에서는 여전히 오버플로 충전기가 주류를 이루고 있습니다. 이는 '스필백' 현상으로 인해 액체 레벨의 메니스커스가 균일하게 유지되어 소매점 진열대에서 중요한 시각적 품질 지표가 되기 때문입니다. 제약용 블로우-필-씰 장비는 용기 성형, 충전 및 밀봉을 단일 무균 챔버에 통합하여 일회용 안과용 점안액 틈새 시장을 개척하고 있습니다. 이를 통해 바이알 충전 라인에 비해 입자 오염을 90% 감소시켰습니다. 진공 기술은 뉴트리슈티컬 분야에서도 확대되고 있습니다. 산소에 민감한 오메가3 오일의 경우, 기존 중력식 충진기에서는 두 번의 공정이 필요했던 질소에 의한 헤드스페이스 세정을 한 번의 배기 및 충진 스트로크로 수행해야 합니다.

지역별 분석

아시아태평양은 2025년 39.85%의 점유율을 확보해, 중국의 '쌍순환' 제조 전략과 인도의 의약품 수출 확대 의지에 힘입어 2031년까지 연평균 6.87%의 성장률을 보일 것으로 전망됩니다. 다국적 음료 및 주사제 제조업체들이 생산의 현지화를 추진하고 있는 가운데, 상하이와 푸네 주변의 위탁 포장 클러스터는 2024년까지 10억 달러 이상의 충전 설비를 도입했습니다. 일본의 고령화 사회는 공간 제약이 있는 도시형 공장에 설치할 수 있는 소형 무균 충전기에 대한 수요를 촉진하고 있습니다. 한편, 국내 화장품 대기업은 AI 비전 시스템을 도입해 쿠션 컴팩트 내 미세한 기포를 감지해 소비자 반품률을 40%나 줄였습니다. 호주의 와인 수출업체들은 유리병에서 경량 PET병으로 전환을 추진하고 있으며, 얇은 벽의 용기에도 흠집 없이 채울 수 있는 서보 제어 노즐의 후방 개조를 추진하고 있습니다.

북미에서는 의약품의 콜드체인 확대와 수제 음료의 보급에 힘입어 견조한 기반을 유지하고 있습니다. FDA 파트 11 규정에 따라 수탁 제조업체는 기존의 반자동 기계를 충전 중량과 작업자 ID를 자동으로 기록하는 전자동 모델로 교체해야 합니다. 2025년 2억 달러 시장 규모가 예상되는 캐나다의 대마초 함유 음료 부문에서는 질소를 이용한 헤드스페이스 플러싱을 통해 테트라하이드로칸나비놀의 안정성을 유지하는 무균 충전 라인이 필수적입니다. 한편, 멕시코의 니어쇼어링이 급증하면서 2025년 말까지 5억 달러의 보틀링 투자를 유치하여 국내 시장과 미국 수출 채널 모두에 공급하고 있습니다. 북미의 대형 소매점에서 선반 공간을 확보하고자 하는 위탁 포장업체에게 SQF(Safe Quality Food) 인증은 사실상 필수적입니다.

유럽에서는 독일, 스위스, 아일랜드의 지속가능성 및 제약 혁신의 거점인 독일, 스위스, 아일랜드에 힘입어 꾸준한 성장이 예상됩니다. 유럽의 포장 및 포장 폐기물 규제에서 재활용 재료 함유량 의무화는 PET 경량화 프로젝트를 추진하고 있으며, 충진업체에 근적외선 수지 선별 모듈을 도입하도록 압박하고 있습니다. 독일 기계산업 클러스터는 2024년 12억 달러 상당의 무균 시스템을 수출하고, Syntegon사와 Groninger사는 해외 고기능성 바이오의약품 시설에 장비를 공급하고 있습니다. 브렉시트 이후 이중 컴플라이언스 부담으로 인해 영국 충전업체들의 검증 기간이 길어지고 있지만, 신속한 재구성이 가능한 모듈식 설비가 이러한 환경 속에서 틈새 시장을 개척하고 있습니다. 중동 및 아프리카는 고성장이 예상되는 프론티어 지역입니다. '사우디 비전 2030'은 무균 형식을 우선시하는 턴키 음료 공장에 자본을 투입하고 있으며, 나이지리아 유업 협동조합은 급증하는 도시 지역 수요를 충족시키기 위해 수동식 파우치 충전에서 반자동 충전기로 전환하기 시작했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The automatic liquid filling machine market size was valued at USD 6.29 billion in 2025 and is estimated to grow from USD 6.59 billion in 2026 to reach USD 8.42 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

Demand is accelerating as pharmaceutical firms adopt aseptic processing, beverage brands pivot toward single-serve formats, and contract-packaging partners absorb capital outlays for turnkey equipment. Rotary platforms still dominate high-speed beverage lines, yet isolator-based aseptic systems are scaling quickly as biologics and nutraceutical SKUs migrate to ambient-stable packaging. Digital-twin analytics, edge-based condition monitoring, and blockchain traceability are moving from proof-of-concept to standard equipment specifications, tightening margins for OEMs unable to embed software value. Nickel-price volatility, counterfeit components, and tightening European recycled-content rules are pressuring supply chains, but they are simultaneously nudging buyers toward lightweight PET designs and long-term steel-sourcing contracts.

Global Automatic Liquid Filling Machine Market Trends and Insights

Stringent Hygiene Standards Driving Demand for Aseptic Lines

Revisions to the United States FDA Annex 1 in 2023 tightened real-time contamination monitoring requirements, pushing pharmaceutical plants to adopt isolator-based fillers that deliver 6-log spore reduction without thermal stress. In parallel, the European Hygienic Engineering and Design Group updated its 2024 guidelines to mandate tool-free disassembly and sub-0.8 micrometer surface roughness, raising capital outlays but shaving 20% off validation lead times. Cold-chain constraints for mRNA vaccines are easing as ambient-stable vial filling gains ground, eliminating refrigerated warehousing costs in remote regions. Beverage processors are also embracing aseptic technology to comply with 3-A sanitary standards that require adenosine triphosphate bioluminescence swabs between shifts. Collectively, these rule changes tip procurement decisions toward turnkey sterile lines, even in segments historically dominated by hot-fill or tunnel-pasteurization equipment.

Industry 4.0 Retrofits, IoT-Enabled Sensors and Analytics

Downtime in pressure-sensitive beverage operations can exceed USD 20,000 per hour, motivating producers to deploy predictive-maintenance suites that flag bearing wear before catastrophic failure. GEA's digital-twin platform streams torque, vibration, and temperature data from more than 200 embedded sensors and schedules technicians 72 hours ahead of a predicted fault. Aseptic facilities benefit disproportionately, because an unscheduled stop forces a full clean-in-place and sterilization cycle that can idle the line for half a shift. Blockchain-secured batch records are emerging as the serialization backbone for vial and syringe packaging, enabling regulators to scan QR codes and view immutable fill-weight histories. Vision-guided reject systems that run at 1,200 bottles per minute now combine edge AI with hyperspectral cameras to reduce false positives by 15% versus legacy photo-electric sensors.

High Up-Front CAPEX for Fully-Automatic Rotary Systems

Turnkey rotary aseptic fillers range from USD 1.5 million to USD 4 million, pricing many mid-tier beverage brands out of the market. Lease-financing and equipment-as-a-service contracts blunt the sticker shock but introduce multi-year volume commitments that smaller firms struggle to guarantee. Validation costs in pharmaceutical lines add another 20% to 30% on top of hardware, and currency swings escalate costs where invoices are pegged to EUR or USD. OEMs have responded with modular inline systems priced between USD 300,000 and USD 600,000 that allow incremental capacity adds, but the throughput trade-off remains significant for high-volume SKUs.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Mandates Favoring Lightweight PET over Glass

- Shift to Ready-to-Drink Nutraceutical Beverages

- Shortage of Skilled Mechatronics Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aseptic platforms are advancing at a 6.43% annual clip through 2031 as pharmaceutical and premium-beverage producers opt for ambient-stable SKUs that bypass cold-chain costs, while rotary systems retained 40.93% of automatic liquid filling machine market share in 2025 by virtue of unmatched throughput in carbonated soft drinks. Inline and linear machines remain popular among craft breweries and specialty-food plants operating 20-plus SKUs per week because straight-line layouts reduce footprint by 25% and accelerate sanitation. Monobloc rinse-fill-cap designs appeal to dairy processors whose clean-in-place cycles must finish within 45 minutes to sustain three-shift campaigns.

Isolator-equipped fillers aimed at pre-filled syringes now feature robotic nest loading and automated stopper placement that remove human intervention from Grade A zones. GEA's modular aseptic platform unveiled in 2025 permits tool-free swaps between rotary-piston and peristaltic heads, trimming validation windows to six weeks. Inline equipment, though slower, satisfies clinical-trial runs of 500 to 1,000 units where the ability to pause mid-batch for sampling is critical. Convergence of ISO 13485, ISO 22716, and FDA 21 CFR Part 11 standards is steering even cosmetic brands toward hygienic-by-design architectures with negligible dead legs and fingertip-safe change parts.

Volumetric systems secured 28.12% of the share in 2025 because piston or magnetic flowmeter dosing maintains accuracy when product density varies, whereas gravimetric lines need constant recalibration. Aseptic and extended-shelf-life configurations are charting a 6.67% CAGR as consumer demand for preservative-free beverages coincides with FDA sterile-processing incentives. Pressure and isobaric fillers dominate carbonated-drink plants to conserve CO2, while gravity equipment is losing ground in wine and spirits to vacuum designs that eliminate foaming and meet +-1 milliliter tolerance contracts.

Overflow fillers still rule clear spirits and cooking oils because the "spill-back" guarantees a level meniscus, a key visual quality cue on retail shelves. Pharmaceutical blow-fill-seal units are carving a niche for single-use ophthalmic droppers by integrating container molding, filling, and sealing in a single sterile chamber, reducing particulate contamination by 90% compared with vial-filling lines. Vacuum technology is expanding in nutraceuticals, where oxygen-sensitive omega-3 oils require nitrogen headspace flushing executed in a single evacuation-and-fill stroke that would otherwise need two steps on traditional gravity machines.

The Automatic Liquid Filling Machine Market Report is Segmented by Machine Type (Rotary Systems, Inline/Linear Systems, Monobloc Filling-Capping Systems, and Aseptic Filling Systems), Filling Technology (Volumetric, and More), Automation Level (Fully-Automatic, Semi-Automatic, and Manual), End-User Industry (Food and Beverage, Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured 39.85% of the share in 2025 and is forecast to expand at 6.87% annually to 2031 thanks to China's dual-circulation manufacturing push and India's pharmaceutical export ambitions. Contract-packaging clusters around Shanghai and Pune absorbed more than USD 1 billion of filling equipment in 2024 as multinational beverages and injectables localized production. Japan's aging society is fueling demand for compact aseptic fillers that slot into space-constrained urban plants, while South Korea's cosmetics giants apply AI vision systems to detect micro-bubbles in cushion compacts, slicing consumer returns by 40%. Australia's wine exporters are migrating from glass to lightweight PET, driving servo-controlled nozzle retrofits that handle thinner walls without scuffing.

North America maintains a solid base driven by pharma cold-chain expansions and craft-beverage proliferation. FDA Part 11 rules are forcing contract manufacturers to swap legacy semi-automatic machines for fully-automatic models that auto-record fill weights and operator IDs. Canada's cannabis-infused drinks sector, valued at USD 200 million in 2025, mandates aseptic lines that preserve tetrahydrocannabinol stability via nitrogen headspace flushing, while Mexico's near-shoring binge attracted USD 500 million in bottling investments by late 2025 to serve both domestic and United States export channels. Safe Quality Food certification is effectively compulsory for co-packers seeking shelf space in leading North American retailers.

Europe posts steady growth led by sustainability and pharmaceutical innovation corridors in Germany, Switzerland, and Ireland. The European Packaging and Packaging Waste Regulation's recycled-content mandate drives PET lightweighting projects, compelling fillers to integrate near-infrared resin-sorting modules. Germany's machinery cluster exported USD 1.2 billion of aseptic systems in 2024, with Syntegon and Groninger supplying high-potency biologics facilities abroad. Post-Brexit dual-compliance burdens lengthen validation for United Kingdom fillers, but modular equipment capable of quick reconfiguration is carving a niche in this environment. Middle East and Africa represent high-growth frontiers; Saudi Vision 2030 funnels capital into turnkey beverage plants favoring aseptic formats, and Nigerian dairy cooperatives have begun shifting from manual pouches to semi-automatic fillers to meet surging urban demand.

- GEA Group AG

- KHS GmbH

- ProMach, Inc.

- Syntegon Technology GmbH

- JBT Corporation

- Accutek Packaging Equipment Company, Inc.

- APACKS Packaging Systems, LLC

- Filamatic LLC

- Universal Filling Machine Company Ltd.

- Inline Filling Systems LLC

- OPTIMA packaging group GmbH

- Groninger & Co. GmbH

- Hondon Packaging & Food Machinery Factory

- Grace Food Processing & Packaging Machinery

- Best Crown Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth of Single-Serve Packaging Formats

- 4.2.2 Stringent Hygiene Standards Driving Demand for Aseptic Lines

- 4.2.3 Industry 4.0 Retrofits, IoT-Enabled Sensors and Analytics

- 4.2.4 Expansion of Contract Packaging in Emerging Markets

- 4.2.5 Sustainability Mandates Favoring Lightweight PET over Glass

- 4.2.6 Shift to Ready-to-Drink Nutraceutical Beverages

- 4.3 Market Restraints

- 4.3.1 High Up-Front CAPEX for Fully-Automatic Rotary Systems

- 4.3.2 Shortage of Skilled Mechatronics Technicians

- 4.3.3 Volatility in Stainless-Steel and Electronic-Component Prices

- 4.3.4 Increasing Counterfeit Equipment from Low-Cost Suppliers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Machine Type

- 5.1.1 Rotary Systems

- 5.1.2 Inline / Linear Systems

- 5.1.3 Monobloc Filling-Capping Systems

- 5.1.4 Aseptic Filling Systems

- 5.2 By Filling Technology

- 5.2.1 Volumetric

- 5.2.2 Gravity

- 5.2.3 Pressure / Isobaric

- 5.2.4 Vacuum

- 5.2.5 Overflow

- 5.2.6 Aseptic / ESL

- 5.3 By Automation Level

- 5.3.1 Fully-Automatic

- 5.3.2 Semi-Automatic

- 5.3.3 Manual

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceuticals

- 5.4.3 Cosmetics and Personal Care

- 5.4.4 Chemicals and Lubricants

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 GEA Group AG

- 6.4.2 KHS GmbH

- 6.4.3 ProMach, Inc.

- 6.4.4 Syntegon Technology GmbH

- 6.4.5 JBT Corporation

- 6.4.6 Accutek Packaging Equipment Company, Inc.

- 6.4.7 APACKS Packaging Systems, LLC

- 6.4.8 Filamatic LLC

- 6.4.9 Universal Filling Machine Company Ltd.

- 6.4.10 Inline Filling Systems LLC

- 6.4.11 OPTIMA packaging group GmbH

- 6.4.12 Groninger & Co. GmbH

- 6.4.13 Hondon Packaging & Food Machinery Factory

- 6.4.14 Grace Food Processing & Packaging Machinery

- 6.4.15 Best Crown Machinery Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment