|

시장보고서

상품코드

2043843

유럽의 분자체 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Molecular Sieves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

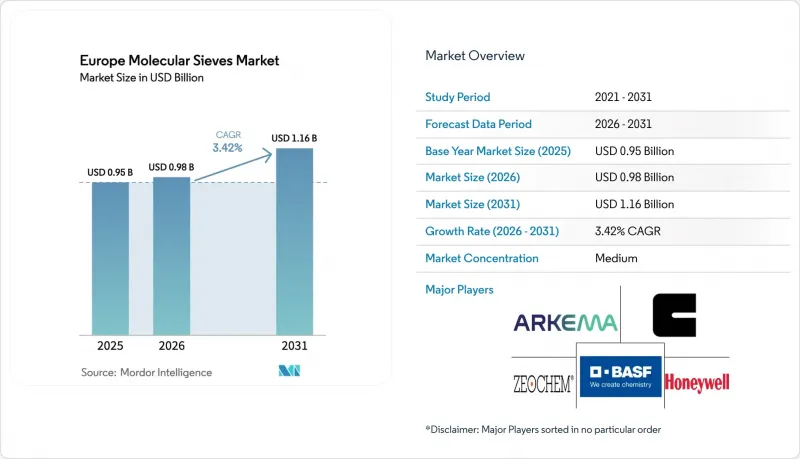

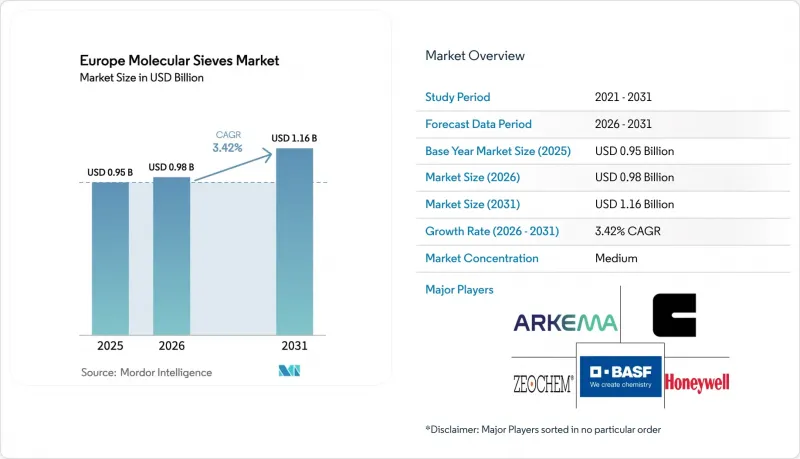

유럽의 분자체 시장 규모는 2025년 9억 5,000만 달러로 평가되었습니다. 2026년 9억 8,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 3.42%를 나타내, 2031년에는 11억 6,000만 달러에 이를 것으로 예측됩니다.

확대되는 전해조 공장의 초건조 수소 수요 증가, 코로나19 이후 병원용 산소 플랜트에 대한 투자 가속화, 탄소 국경 조정 메커니즘(CBAM)으로 인한 전체 산업용 가스 네트워크의 업그레이드로 인해 흡착제의 응용 기반이 확대되고 있습니다. 바이오가스 업그레이드 및 대기중 이산화탄소 직접 포집(DAC)프로젝트에서는 저온에서의 재생 특성이 선호되기 때문에 탄소분자체는 점차 기존의 제올라이트를 능가하고 있습니다. 형태에 대한 선호도도 변화하고 있습니다. 인산염을 사용하지 않는 세제에서는 분말 등급이 부상하고 있으며, 대형 공기 분리 장치에서는 펠릿이 여전히 주류입니다. 현재 경쟁 전략은 바인더가 없는 제올라이트 기술, 에너지 효율이 높은 재생 기술, 운영 비용 부담을 줄이는 하이브리드형 멤브레인 및 흡착기 제품에 초점을 맞추었습니다.

유럽의 분자체 시장 동향과 인사이트

REACH 및 CBAM에 따른 규제 강화 : 수분 및 VOC 표준 강화

REACH(화학물질의 등록, 평가, 허가 및 제한에 관한 법률) 개정과 2026년부터 단계적으로 도입되는 CBAM으로 인해 산업용 가스, 석유화학, 제약 플랜트에서 허용되는 수분 및 VOC(휘발성 유기화합물) 기준치가 낮아짐에 따라, 사업자들은 검증된 반응 속도를 가진 고성능 제올라이트 층으로 전환해야 합니다. 유럽 산업용 가스 협회는 2025년 업계 매출을 212억 유로로 추산하고 CBAM에 따른 에너지 비용 리스크를 지적하며, 이로 인해 고효율 흡착 공정의 가치가 높아졌다고 밝혔습니다. 에어리퀴드는 독일 드레스덴의 새로운 공기분리 설비에 2억 5,000만 유로 이상을 투자하고, 오로비스사와 협력하여 불가리아에 1억 유로 규모의 공장을 건설할 계획이며, 모두 CBAM을 준수하는 분자체 패키지를 채택하고 있습니다. ISO 9001 인증을 획득한 공정을 보유하고, 2ppm(100만분의 1) 미만의 수분 투과율을 실현할 수 있는 공급업체가 조기 갱신 계약을 체결하고 있습니다.

EU의 노후화된 병원과 소형 공장으로 인한 PSA 산소 수요 급증으로 인한 PSA 산소 수요 급증

팬데믹 이후 병원 개보수 및 고령화로 인해 PSA 산소 설비 도입이 증가하고 있으며, 독일, 프랑스, 영국에서는 제올라이트에 대한 지역 수요가 CAGR 5.8-7.8%로 증가하고 있습니다. 허니웰 UOP의 OXYSIV 시리즈는 2021년 감염 확산 시 이탈리아 병원에 긴급 공급되어 전략적 위치 근접성의 이점을 부각시켰습니다. 지방의 진료소나 요양시설에서는 유지보수 주기를 18개월 이상 연장할 수 있는 컴팩트한 비드형 필러를 선호하고 있으며, 이로 인해 유럽의 분자체 시장은 더욱 확대되고 있습니다.

EU의 탄소 가격 상승에 따른 에너지 집약적 재생에너지 비용 상승 전망

진공 온도 스윙 또는 열 스윙 사이클은 탈착되는 CO2 1톤당 최대 90kWh의 전력과 2.9GJ의 열을 소비하며, EU-ETS(유럽연합 배출권 거래제) 할당량이 증가함에 따라 운영 비용이 상승하고 있습니다. 자본이 부족한 소규모 바이오가스 및 PSA 산소 사업자들은 경제적인 어려움을 느끼고 있으며, 침대 교체를 미룰 가능성이 있어 단기적인 수요를 억제하는 요인으로 작용하고 있습니다.

부문 분석

2025년 기준, 펠렛 등급은 유럽의 분자체 시장 규모의 39.71%를 차지하며, 공기 분리 및 정유시설의 PSA(압력 스윙 흡착) 타워에서 압력 사이클을 견딜 수 있는 기계적 강도의 이점을 누렸습니다. 포맷 전환에는 많은 설비 투자가 필요하지만, 유럽의 분자체 시장에서는 송풍기의 에너지 소비를 줄이기 위해 펠릿을 저압손실 압출 성형품으로 교체하는 단계적 개조가 진행되고 있습니다.

분말형 분자체는 예측 기간(2026-2031년) 동안 CAGR 3.90%를 나타낼 것으로 예측되며, 높은 비표면적이 취급 편의성을 능가하는 세제 및 빠른 사이클 흡착의 틈새 시장에 침투하고 있습니다. 이러한 추세는 제올라이트 A의 우위를 공고히 하는 인산염 무사용 규제와 일치합니다. 비드형 제품은 점유율이 작고, 주로 소형 의료용 산소 농축기에 사용되며, 분진 억제를 통해 필터의 수명을 연장하고 있습니다.

미세 다공성 재료는 2025년 유럽 분자체 시장 점유율의 64.57%를 차지했으며, 예측 기간(2026-2031년) 동안 CAGR 3.99%를 나타낼 것으로 예측됩니다. 이는 공기 분리에 대한 지속적인 수요를 반영합니다. 에어리퀴드가 2억 5,000만 유로를 투자한 드레스덴 ASU(공기분리장치)에 대한 투자 등은 CBAM(탄소국경조정메커니즘)의 효율 기준을 충족하기 위해 13배의 베드 수에 의존하고 있습니다.

메조 다공성 및 매크로 다공성 등급은 촉매 및 특수 크로마토그래피 응용 분야에 사용됩니다. 제오포아가 2025년 5월에 발표한 메조다공성 제품 출시는 수소화 분해 및 바이오연료 분야에서 모멘텀을 보여주고 있지만, 건조, 정제, CO2 포집를 지배하는 주력 제품인 미세다공성 제품에 비해 그 생산량은 여전히 소규모에 머물러 있습니다.

유럽의 분자체 시장은 형태(펠릿, 비드, 분말), 크기(미세공극, 중공극, 대공극), 제품 유형(탄소, 점토, 다공성 유리, 실리카겔, 제올라이트, 기타 제품 유형), 최종 사용자 산업(농산물, 공기정화, 자동차 산업, 화장품 등), 지역(독일, 영국, 영국, 프랑스, 스페인, 러시아, 기타 유럽) 이탈리아, 영국, 프랑스, 스페인, 러시아, 기타 유럽)

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Europe Molecular Sieves Market size is expected to grow from USD 0.95 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.16 billion by 2031 at a 3.42% CAGR over 2026-2031.

Surging demand for ultra-dry hydrogen in expanding electrolyzer parks, accelerated post-COVID investments in hospital oxygen plants, and Carbon Border Adjustment Mechanism (CBAM)-driven upgrades across industrial gas networks are widening the application base for adsorbents. Carbon molecular sieves are edging ahead of traditional zeolites as biogas upgrading and direct air-capture projects prefer their lower-temperature regeneration profiles. Format preferences are also shifting: powdered grades are gaining ground in phosphate-free detergents while pellets retain primacy in large air-separation units. Competitive strategy now pivots on binder-free zeolite technologies, energy-efficient regeneration, and hybrid membrane-adsorber offerings that blunt operating-cost headwinds.

Europe Molecular Sieves Market Trends and Insights

Regulatory Tail-Winds From REACH and CBAM Tightening Moisture/VOC Specs

REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) updates and the phased CBAM roll-out from 2026 are lowering allowable moisture and VOC (Volatile Organic Compound) thresholds across industrial gas, petrochemical, and pharmaceutical plants, pushing operators toward high-performance zeolite beds with documented kinetics. The European Industrial Gases Association put 2025 industry revenue at EUR 21.2 billion and flagged energy-cost exposure under CBAM, heightening the value of efficient adsorption trains. Air Liquide earmarked over EUR 250 million for new air-separation capacity in Dresden, Germany, and partnered with Aurubis on a EUR 100 million Bulgarian unit, both specifying CBAM-compliant molecular sieve packages. Suppliers able to certify ISO 9001 processes and deliver moisture breakthroughs below 2 ppm (parts per million) are winning early replacement contracts.

Explosive PSA Oxygen Demand From Ageing EU Hospitals and Mini-Plants

Post-pandemic hospital retrofits and an aging population have lifted PSA oxygen installations, sending regional zeolite demand higher at 5.8-7.8% CAGR in Germany, France, and the United Kingdom. Honeywell UOP's OXYSIV range supplied emergency volumes to Italian hospitals during the 2021 surges, underscoring strategic proximity benefits. Rural clinics and nursing homes favor compact beaded beds that stretch service intervals beyond 18 months, further widening the Europe Molecular Sieves market.

Energy-Intensive Regeneration Costs Amid EU Carbon Price Escalation

Vacuum-temperature swing or thermal swing cycles consume up to 90 kWh of electricity and 2.9 GJ of heat per tonne of CO2 desorbed, inflating operating costs as EU-ETS (European Union Emissions Trading System) allowances rise. Smaller biogas and PSA oxygen operators with limited capital find the economics challenging and may defer bed replacements, dampening short-term volumes.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Green-Hydrogen Electrolyzer Build-Outs Requiring Ultra-Dry H2 Streams

- Petro-Refinery Revamps to Meet Euro 7 Fuel Standards

- Competition From Hybrid Membrane-Adsorber Skids in Biogas Upgrading

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pelleted grades represented 39.71% of the Europe Molecular Sieves market size in 2025, benefiting from mechanical strength that withstands pressure cycles in air-separation and refinery PSA (Pressure Swing Adsorption) towers. Although format changeovers are capital-heavy, the Europe Molecular Sieves market is witnessing incremental retrofits in which pellets are swapped for low-pressure-drop extrudates to trim blower energy.

Powdered molecular sieves, forecast to grow at a 3.90% CAGR during the forecast period (2026-2031), are penetrating detergent and rapid-cycle adsorption niches, where high surface area overrides handling convenience. The trend aligns with phosphate-free mandates that solidify Zeolite A dominance. Beaded variants occupy a smaller share, mainly in compact medical oxygen concentrators, where dust control extends filter life.

Microporous materials held 64.57% of the Europe Molecular Sieves market share in 2025 and will rise at a 3.99% CAGR during the forecast period (2026-2031), reflecting sustained air-separation demand. Investments such as Air Liquide's EUR 250 million Dresden ASU lean on 13X beds to meet CBAM efficiency thresholds.

Mesoporous and macroporous grades serve catalyst and specialty chromatographic uses. Zeopore's May 2025 mesoporized launch demonstrates momentum in hydrocracking and biofuel routes, but volumes remain modest against microporous workhorses that dominate drying, purification, and CO2 capture.

The Europe Molecular Sieves Market is Segmented by Shape (Pelleted, Beaded, and Powdered), Size (Microporous, Mesoporous, and Macroporous), Product Type (Carbon, Clay, Porous Glass, Silica Gel, Zeolite, and Other Product Types), End-User Industry (Agricultural Products, Air Purification, Automotive Industry, Cosmetics, and More), and Geography (Germany, United Kingdom, Italy, France, Spain, Russia, and Rest of Europe)

List of Companies Covered in this Report:

- Arkema Group

- Axens

- BASF SE

- Bear River Zeolite Co.

- Bete Ceramics Co. Ltd.

- Cabot Corporation

- CARBOTECH AC GMBH

- Clariant

- Dalian absorbent Co., Ltd

- Desicca Chemicals Pvt. Ltd.

- Graver Technologies

- Honeywell International Inc.

- KNT Group

- Merck KGaA

- Shanghai Hengye Molecular Sieve Co. Ltd

- SHOWA DENKO K.K.

- Solvay

- Tosoh Corporation

- W. R. Grace & Co.-Conn.

- Zeolyst International

- Zeochem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory tail-winds from REACH and CBAM tightening moisture/VOC specs

- 4.2.2 Explosive PSA oxygen demand from ageing European Union hospitals and mini-plants (post-COVID)

- 4.2.3 Surge in green-hydrogen electrolyser build-outs requiring ultra-dry H2 streams

- 4.2.4 Petro-refinery revamps to meet Euro 7 fuel standards

- 4.2.5 Detergent phosphate bans boosting 4A zeolite uptake

- 4.3 Market Restraints

- 4.3.1 Energy-intensive regeneration costs amid European Union carbon price escalation

- 4.3.2 Competition from hybrid membrane-adsorber skids in biogas upgrading

- 4.3.3 Raw-material (soda-ash, sodium-silicate) price volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Shape

- 5.1.1 Pelleted

- 5.1.2 Beaded

- 5.1.3 Powdered

- 5.2 By Size

- 5.2.1 Microporous (< 2 nm)

- 5.2.2 Mesoporous (2-50 nm)

- 5.2.3 Macroporous (> 50 nm)

- 5.3 By Product Type

- 5.3.1 Carbon

- 5.3.2 Clay

- 5.3.3 Porous Glass

- 5.3.4 Silica Gel

- 5.3.5 Zeolite

- 5.3.6 Others

- 5.4 By End-user Industry

- 5.4.1 Agricultural Products

- 5.4.2 Air Purification

- 5.4.3 Automotive Industry

- 5.4.4 Detergents Industry

- 5.4.5 Cosmetics

- 5.4.6 Heating and Refrigeration Industry

- 5.4.7 Industrial Gas Production

- 5.4.8 Nuclear Industry

- 5.4.9 Petroleum Refining and Petrochemicals

- 5.4.10 Pharmaceutical Industry

- 5.4.11 Plastics and Polymers Industry

- 5.4.12 Waste and Water Treatment

- 5.4.13 Others

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Arkema Group

- 6.4.2 Axens

- 6.4.3 BASF SE

- 6.4.4 Bear River Zeolite Co.

- 6.4.5 Bete Ceramics Co. Ltd.

- 6.4.6 Cabot Corporation

- 6.4.7 CARBOTECH AC GMBH

- 6.4.8 Clariant

- 6.4.9 Dalian absorbent Co., Ltd

- 6.4.10 Desicca Chemicals Pvt. Ltd.

- 6.4.11 Graver Technologies

- 6.4.12 Honeywell International Inc.

- 6.4.13 KNT Group

- 6.4.14 Merck KGaA

- 6.4.15 Shanghai Hengye Molecular Sieve Co. Ltd

- 6.4.16 SHOWA DENKO K.K.

- 6.4.17 Solvay

- 6.4.18 Tosoh Corporation

- 6.4.19 W. R. Grace & Co.-Conn.

- 6.4.20 Zeolyst International

- 6.4.21 Zeochem

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment