|

시장보고서

상품코드

2043853

데이터 유출 방지(DLP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Data Loss Prevention (DLP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

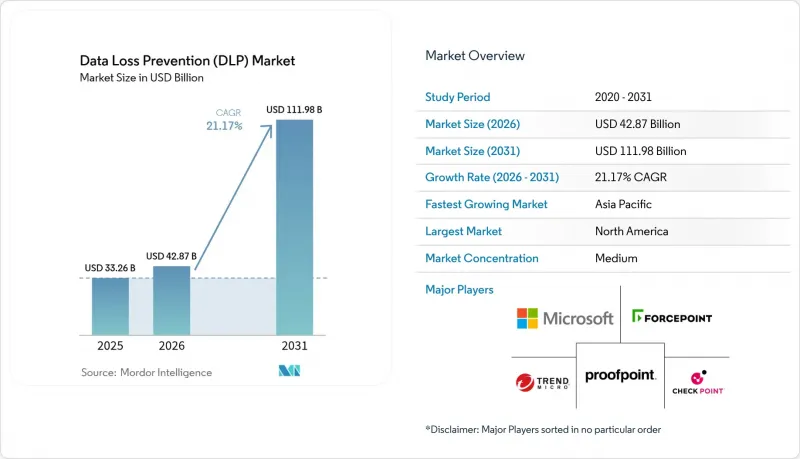

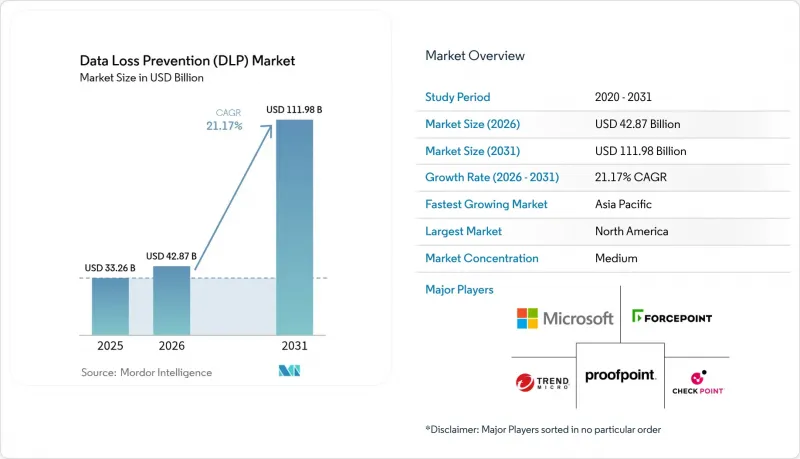

데이터 유출 방지(DLP) 시장 규모는 2025년 332억 6,000만 달러로 평가되었습니다. 2026년 428억 7,000만 달러로 확대되어 2031년까지 1,119억 8,000만 달러에 이르며, 2026년부터 2031년에 걸쳐 CAGR 21.17%를 나타낼 전망입니다.

GDPR(EU 개인정보보호규정) 2.0 및 개정된 CCPA 규정에 따라 강화된 처벌로 인해 침해된 각 기록에 대해 실질적인 비용이 부과됨에 따라 이사회는 더 큰 DLP 예산을 승인했습니다. 생성형 AI 코파일럿의 등장으로 채팅 프롬프트 내에 새로운 데이터 유출 경로가 생겨나면서 위협 모델이 파일 중심에서 대화 중심의 벡터로 변화하고 있습니다. 중국, 러시아, 인도, 유럽연합의 소버린 클라우드 의무화로 인해 국내 처리가 요구됨에 따라, 전 세계 기업들은 현지 암호화 키 관리 요건을 준수하는 DLP 정책을 병행하여 운영하고 있습니다. 벤더들은 클라우드 액세스 보안 브로커, 데이터 보안 현황 관리, DLP 기능을 단일 콘솔에 통합하여 이러한 복잡성을 해결하고 오감지율을 낮추며 도입 주기를 단축하고 있습니다. 그 결과, 클라우드 도입이 신규 지출의 대부분을 차지하게 되었고, 엔드포인트 에이전트가 네트워크 어플라이언스를 능가하는 추세를 보이고 있습니다.

세계의 데이터 유출 방지(DLP) 시장 동향 및 인사이트

GDPR(EU 개인정보보호규정) 2.0 및 CCPA 개정에 따른 사이버 침해 과징금 급증

2025년 유럽 규제 당국은 GDPR(EU 개인정보보호규정)에 따라 12억 유로의 막대한 벌금을 부과했으며, 이는 전년 대비 22%나 증가한 수치입니다. 이 같은 증가는 지역 전체에서 데이터 보호 규정의 집행이 강화되고 있음을 여실히 보여줍니다. 주목할 만한 사례로는 TikTok에 대한 5억 3,000만 유로의 벌금 부과를 들 수 있으며, 이는 국경 간 데이터 전송 및 GDPR(EU 개인정보보호규정) 요건 준수에 대한 감시가 강화되고 있다는 점을 강조하고 있습니다. 한편, 2025년 1월부터 시행된 캘리포니아주 개정 CCPA에서는 개인의 집단소송을 허용하는 새로운 규정이 도입되었습니다. 이 변경으로 인해 기업은 무제한적인 손해배상 책임이 발생할 수 있으며, 견고한 데이터 보호 조치의 중요성이 더욱 강조되고 있습니다. 벌금이 기업 전 세계 매출의 최대 4%에 달할 수 있기 때문에 최고 정보 보안 책임자(CISO)는 고도의 실시간 데이터 유출 방지(DLP) 대책을 도입해야 합니다. 이러한 조치는 데이터 유출을 방지하고, 법적 기준을 초과하지 않도록 하며, 조직이 진화하는 규정을 계속 준수할 수 있도록 보장하기 위해 고안되었습니다.

하이브리드 업무로 인한 데이터 확산으로 엔드포인트와 클라우드의 위험성이 증가하고 있습니다.

2024년 포티넷의 조사에 따르면, 77%의 조직이 내부자에 의한 침해사고를 경험했으며, 그중 절반 가까이가 현재의 DLP 툴이 효과적이지 않다고 평가했습니다. BYOD(개인 소유 단말기의 업무 활용) 프로그램과 관리 대상에서 제외된 파일 공유 앱의 확산으로 잠재적인 데이터 유출 경로가 크게 확대되어 조직이 기밀 정보를 보호하는 것이 점점 더 어려워지고 있습니다. 현재 기업들은 평균 4.3개의 IaaS(Infrastructure-as-a-Service) 플랫폼을 이용하고 있으며, 플랫폼 간 통일된 라벨링과 일관된 데이터 보호 정책의 유지가 큰 과제로 대두되고 있습니다. IBM 시큐리티의 침해 보고서는 평균 침해 비용이 미화 488만 달러에 달할 것으로 추정하며, 이에 따른 금전적 위험을 강조하는 동시에 강력한 예방 조치의 필요성을 강조하고 있습니다. 그 결과, 이사회는 리스크를 줄이고 잠재적 손실을 줄이기 위해 사후 조사보다 예방 전략을 우선시하고 있습니다.

멀티 클라우드 도입의 복잡성 및 기술 격차 해소

2024년 ISC2는 사이버 보안 인력에 있어 350만 명의 인력 부족을 지적하며, 이 분야의 숙련된 전문가에 대한 수요가 증가하고 있음을 강조했습니다. 특히 데이터 보호의 역할은 수요가 많고 기밀 정보 보호에 있어 매우 중요하기 때문에 급여가 18% 더 높습니다. AWS, Azure, Google Cloud를 포함한 각 하이퍼스케일 클라우드 플랫폼은 각각 고유한 정책 구문을 채택하고 있으며, 이는 플랫폼 간 라벨 매핑을 시도하는 엔지니어들에게 어려움을 주고 있습니다. 이러한 표준화의 부재로 인해, 기업들은 최대 12개월 동안 두 개의 DLP(데이터 유출 방지) 스택을 병렬로 운영해야 하는 상황에 처하게 되는 경우가 많습니다. 그 결과, 이러한 접근 방식은 운영 비용과 관련 위험을 두 배로 증가시키고, 마이그레이션 프로세스를 더욱 복잡하게 만듭니다.

부문 분석

2025년 기준, 클라우드 배포는 데이터 유출 방지(DLP) 시장 매출의 67.31%를 차지했으며, 2031년까지 연평균 복합 성장률(CAGR) 21.23%로 확대될 것으로 예측됩니다. 이는 탄력적인 컴퓨팅과 세계 거점이 인라인 API 검사에 유리하게 작용하고 있음을 보여줍니다. On-Premise형 어플라이언스는 클라우드로의 데이터 유출을 금지하는 국방 기관이나 원자력 사업자에게는 여전히 유용하지만, TLS 1.3의 사용 확대로 패시브 탭에 대한 가시성이 떨어지면서 규제 대상 기업들도 고객 관리형 키를 사용하는 클라우드 프록시로 전환해야 하는 상황에 처해 있습니다. 하고 있습니다.

또한, 탄력적인 확장성으로 인해 단가도 낮아지고 있습니다. Zscaler는 하루에 3,000억 건 이상의 트랜잭션을 처리하기 때문에 사용자 1인당 추가 비용은 몇 달러가 아닌 몇 센트에 불과합니다. 하이브리드 모델에서는 SaaS 트래픽을 클라우드 프록시로 라우팅하면서 파일 서버의 보호는 On-Premise에서 유지하지만, 통합 관리가 이루어지지 않으면 정책의 불일치가 발생합니다. 따라서 각 벤더들은 두 환경에 동일한 라벨 구문을 적용하는 통합 콘솔을 통합하고 있습니다.

2025년 매출에서 네트워크 도구가 차지하는 비중은 34.23%였으나, 엔드포인트 에이전트가 가장 빠르게 성장할 것으로 예상되며, 2031년까지 예상 CAGR은 23.91%를 나타낼 것으로 예측됩니다. 이러한 급증은 기존의 경계 제어의 틀을 넘어 노트북, 스마트폰, IoT 센서의 중요성이 높아진 것이 주요 요인으로 작용하고 있습니다. 원격 근무가 보편화되면서 분산된 업무 환경에서 기밀 데이터를 보호하기 위한 강력한 보안 조치에 대한 요구가 증가함에 따라, 이러한 엔드포인트 관련 데이터 유출 방지(DLP) 솔루션 시장 규모가 크게 확대될 것으로 예측됩니다.

Digital Guardian은 오프라인 모드에서도 클립보드, USB, 인쇄 활동을 모니터링하여 설정된 정책을 위반하는 전송을 사전에 차단합니다. 이 종합적인 모니터링은 장치가 네트워크에서 연결이 끊어진 경우에도 데이터의 안전을 보장합니다. 한편, CrowdStrike는 경고를 악성코드 지표와 연동하여 DLP의 효과를 높이고, 이를 통해 대응 시간을 단축하여 위협 감소를 전반적으로 향상시키고 있습니다. 에어 갭이 있는 군사 연구소에서는 네트워크 어플라이언스가 여전히 필수적이지만, 주요 벤더들은 이러한 특수한 환경에서도 유효성을 유지하기 위해 시그니처 팩을 업데이트하고 있습니다. 그러나 조직이 진화하는 기술 환경에 적응함에 따라 보안 우선순위가 광범위하게 변화하고 있음을 반영하여, 성장 추세가 엔드포인트 분야에 크게 편중되어 있는 것은 분명합니다.

지역별 분석

2025년 북미는 전체 매출의 40.12%라는 큰 비중을 차지하며 시장에서 우위를 점했습니다. 2024년 미국에서는 3,205건의 정보 유출 사고가 발생하여 3억 5,300만 명이 피해를 입었습니다. 이러한 정보 유출 건수의 놀라운 증가로 인해, 위험을 줄이고 컴플라이언스를 준수하기 위한 강력하고 효과적인 관리 방안을 도입하는 것이 경영진 차원에서 시급히 요구되고 있습니다. 캐나다의 PIPEDA와 멕시코의 INAI 규정은 모두 기업에게 72시간이라는 엄격한 기한 내에 정보 유출 통지를 하도록 규정하고 있습니다. 이에 따라 기업들은 취약점을 적극적으로 파악하고, 컴플라이언스 위반으로 인해 발생할 수 있는 법적 처벌을 피하기 위해 지속적인 모니터링 체제를 도입하는 사례가 늘고 있습니다.

아시아태평양은 23.62%의 놀라운 CAGR을 기록하며 시장의 주요 기업로 부상하고 있으며, 빠른 성장세를 보이고 있습니다. 중국의 '개인정보보호법', 인도의 '디지털 개인 정보 보호법', 일본의 '개인정보보호법(APPI)' 개정안은 이 지역에서 데이터 현지화 및 컴플라이언스의 중요성을 높이고 있습니다(MEITY.GOV.IN). 이러한 규제 동향으로 인해 기업들은 엄격한 현지화 요건을 충족하기 위해 사업 운영을 조정해야 하는 상황에 처해 있습니다. IBM은 안전하고 컴플라이언스를 준수하는 데이터 스토리지 솔루션에 대한 수요가 증가함에 따라 이 지역 전체 소버린 클라우드 지출이 연간 31.5%의 견조한 성장률을 나타낼 것으로 예상했습니다. 이러한 추세는 규제 및 보안 문제를 해결하기 위해 국내 키 관리 기능을 제공하는 데이터 유출 방지(DLP) 플랫폼의 도입을 촉진하고 있습니다.

GDPR(EU 개인정보보호규정)의 엄격한 감시를 받고 있는 유럽은 규제 리더의 지위를 유지하고 있으며, 2025년에는 총 12억 유로의 벌금이 부과되었습니다. '슐렘스 II 판결'은 미국으로부터의 데이터 전송에 심각한 복잡성을 초래하고, 이 지역에서 사업을 운영하는 다국적 기업들에게 도전이 되고 있습니다. 이에 대응하기 위해 이들 조직은 고급 클라이언트 측 암호화를 도입하고 EU 내에서 호스팅된 키를 활용하여 보안 조치를 강화하여 GDPR(EU 개인정보보호규정) 요건을 준수하고 있습니다. 특히 2024년에는 영국, 스페인, 이탈리아가 집행 조치를 강화하면서 데이터 보호 규정 준수의 중요성이 더욱 강조되었습니다. 이러한 움직임으로 인해 EEA 역외로의 데이터 전송을 차단할 수 있는 정책 엔진에 대한 수요가 증가하고 있으며, 기업들은 기밀 정보를 보호하면서 컴플라이언스를 유지할 수 있게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Data loss prevention (DLP) market size expanded from USD 33.26 billion in 2025, to USD 42.87 billion in 2026, and will touch USD 111.98 billion by 2031, rising at a 21.17% CAGR during 2026-2031.

Penalty escalation under GDPR 2.0 and amended CCPA rules now assigns material cost to every breached record, so boards approve bigger DLP budgets. Gen-AI copilots have opened new exfiltration paths inside chat prompts, changing threat models from file-centric to conversation-centric vectors. Sovereign-cloud mandates in China, Russia, India, and the European Union require on-shore processing, so global companies run parallel DLP policies that respect local cryptographic-key custody. Vendors answer this complexity by merging cloud-access security broker, data-security-posture-management, and DLP functions inside one console, lowering false-positive rates and shortening deployment cycles. As a result, cloud deployments now dominate new spending, and endpoint agents outpace network appliances.

Global Data Loss Prevention (DLP) Market Trends and Insights

Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

In 2025, European regulators imposed a substantial EUR 1.2 billion in fines under the GDPR, marking a significant 22% increase compared to the previous year. This rise underscores the growing enforcement of data protection regulations across the region. A notable case involved a EUR 530 million fine levied against TikTok, which highlighted the increasing scrutiny on cross-border data transfers and compliance with GDPR requirements. Meanwhile, California's updated CCPA, which came into effect in January 2025, introduced new provisions allowing private class actions. This change has the potential to expose companies to unlimited damages, further emphasizing the importance of robust data protection measures. With penalties reaching as high as 4% of a company's global turnover, chief information security officers are now compelled to implement advanced real-time Data Loss Prevention (DLP) measures. These controls are designed to prevent data exfiltration proactively, ensuring that legal thresholds are not breached and organizations remain compliant with evolving regulations.

Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

In 2024, Fortinet found that 77% of organizations encountered insider incidents, and nearly half deemed their current DLP tools ineffective. The rise of bring-your-own-device programs and unmanaged file-sharing apps has significantly expanded avenues for potential data leakage, making it increasingly difficult for organizations to safeguard sensitive information. With enterprises now averaging 4.3 infrastructure-as-a-service platforms, achieving unified labeling and maintaining consistent data protection policies across platforms has become a considerable challenge. Highlighting the financial stakes involved, the IBM Security breach report pegged the average breach cost at a staggering USD 4.88 million, underscoring the need for robust preventive measures. As a result, boards are now prioritizing prevention strategies over post-incident forensics to mitigate risks and reduce potential losses.

Complexity and Skills Gap in Multi-Cloud Roll-Outs

In 2024, ISC2 identified a significant 3.5 million-person shortfall in the cybersecurity workforce, highlighting the growing demand for skilled professionals in this field. Data-protection roles, in particular, are in high demand, commanding an 18% salary premium due to their critical importance in safeguarding sensitive information. Each hyperscale cloud platform, including AWS, Azure, and Google Cloud, employs its own distinct policy syntax, which creates challenges for engineers attempting to map labels across these platforms. This lack of standardization often forces firms to operate dual DLP (Data Loss Prevention) stacks for an extended period of up to twelve months during migration processes. Consequently, this approach results in a doubling of both operational expenses and associated risks, further complicating the migration process.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of DLP with CASB and DSPM Platforms

- AI-Assisted Policy Tuning Slashing False-Positive Rates

- High TCO for Legacy On-Prem Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments held 67.31% of Data loss prevention (DLP) market revenue in 2025 and are forecast to climb at 21.23% CAGR to 2031, highlighting how elastic compute and global points of presence favor inline API inspection. On-prem appliances stay relevant for defense and nuclear operators that forbid cloud egress, yet rising TLS 1.3 usage reduces the visibility of passive taps, pushing even regulated firms toward cloud proxies with customer-managed keys.

Elastic scale also drives unit pricing lower. Zscaler processes more than 300 billion daily transactions, so each incremental user costs cents, not dollars. Hybrid models route SaaS traffic to cloud proxies while keeping file-server coverage on-premise, but policy drift emerges without federated management. Vendors are therefore embedding unified consoles that push the same label grammar to both environments.

While network tools accounted for 34.23% of the 2025 revenue, endpoint agents are set to experience the swiftest growth, boasting a projected CAGR of 23.91% through 2031. This surge is largely fueled by the rising prominence of laptops, smartphones, and IoT sensors, which increasingly operate beyond traditional perimeter controls. As remote work continues to be the norm, the market size for data loss prevention (DLP) solutions tied to these endpoints is anticipated to see a significant uptick, driven by the growing need for robust security measures to protect sensitive data in decentralized work environments.

Digital Guardian monitors clipboard, USB, and printing activities, even in offline mode, proactively blocking any transfers that breach established policies. This comprehensive monitoring ensures that data remains secure, even when devices are disconnected from the network. Meanwhile, CrowdStrike enhances the DLP's efficacy by linking alerts to malware indicators, thereby expediting the response time and improving overall threat mitigation. Although network appliances are still vital for air-gapped military laboratories, leading vendors are updating their signature packs to maintain relevance in these specialized environments. However, it's evident that the growth trajectory is heavily skewed towards the endpoint segment, reflecting the broader shift in security priorities as organizations adapt to evolving technological landscapes.

The Data Loss Prevention (DLP) Market Report is Segmented by Deployment (On-Premise, and Cloud-Based), Solution (Network DLP, Endpoint DLP, and More), End-User Industry (BFSI, IT and Telecom, Government and Defense, Healthcare, Retail and Logistics, and More), Application (Cloud Storage Security, Email and Collaboration Protection, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America accounted for a significant 40.12% of the total revenue, showcasing its dominance in the market. In 2024, the United States recorded a staggering 3,205 breach incidents, which impacted 353 million individuals. This alarming surge in breach volume has heightened urgency at the board level for implementing robust and effective controls to mitigate risks and ensure compliance. Both Canada's PIPEDA and Mexico's INAI regulations mandate firms to issue breach notices within a tight 72-hour window. As a result, companies are increasingly adopting continuous monitoring practices to proactively identify vulnerabilities and sidestep potential statutory penalties that could arise from non-compliance.

Asia-Pacific is emerging as a dominant player in the market, boasting an impressive 23.62% CAGR, which highlights its rapid growth trajectory. China's Personal Information Protection Law, India's Digital Personal Data Protection Act, and Japan's APPI amendments are collectively amplifying the stakes for data localization and compliance in the region [MEITY.GOV.IN]. These regulatory developments are compelling businesses to adapt their operations to meet stringent localization requirements. IBM projects a robust 31.5% annual growth in sovereign cloud spending across the region, driven by increasing demand for secure and compliant data storage solutions. This trend is fueling the adoption of Data Loss Prevention (DLP) platforms, particularly those offering in-country key management capabilities to address regulatory and security concerns.

Europe, under the stringent watch of GDPR, continues to maintain its position as a regulatory leader, levying fines totaling EUR 1.2 billion in 2025. The Schrems II ruling has introduced significant complexities for U.S. data transfers, creating challenges for multinational corporations operating in the region. In response, these organizations are bolstering their security measures by incorporating advanced client-side encryption and utilizing EU-hosted keys to ensure compliance with GDPR requirements. Notably, in 2024, the U.K., Spain, and Italy intensified their enforcement actions, further emphasizing the importance of adhering to data protection regulations. This escalation has led to a heightened demand for policy engines capable of blocking data transfers to regions outside the EEA, ensuring that businesses remain compliant while safeguarding sensitive information.

- Broadcom Inc.

- Microsoft Corporation

- GTB Technologies, Inc.

- CoSoSys SRL

- Digital Guardian LLC

- Forcepoint LLC

- Proofpoint, Inc.

- Zscaler, Inc.

- Trend Micro Incorporated

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- CrowdStrike Holdings, Inc.

- Netskope, Inc.

- Trellix Corporation

- Spirion LLC

- Safetica, a.s.

- Code42 Software, Inc.

- Nightfall AI, Inc.

- Cyera, Inc.

- Fortinet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Cyber-Breach Fines Under GDPR 2.0 and CCPA Amendments

- 4.2.2 Hybrid-Work Data Sprawl Raising Endpoint and Cloud Risk

- 4.2.3 Convergence of DLP with CASB and DSPM Platforms

- 4.2.4 AI-Assisted Policy Tuning Slashing False-Positive Rates

- 4.2.5 Zero-Trust and SASE Road Maps Mandating Integrated DLP

- 4.2.6 Gen-AI Code Copilots Creating New Exfiltration Vectors

- 4.3 Market Restraints

- 4.3.1 Complexity and Skills Gap in Multi-Cloud Roll-Outs

- 4.3.2 High TCO for Legacy On-Prem Policies

- 4.3.3 Privacy-by-Design Push Limiting Deep Content Inspection

- 4.3.4 Sovereign-Cloud Mandates Fragmenting Global Policy Sets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud-Based

- 5.2 By Solution

- 5.2.1 Network DLP

- 5.2.2 Endpoint DLP

- 5.2.3 Storage / Datacenter DLP

- 5.2.4 Others

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Retail and Logistics

- 5.3.6 Manufacturing

- 5.3.7 Others

- 5.4 By Application

- 5.4.1 Cloud Storage Security

- 5.4.2 Email and Collaboration Protection

- 5.4.3 IP Protection and Source-Code Governance

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Broadcom Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 GTB Technologies, Inc.

- 6.4.4 CoSoSys SRL

- 6.4.5 Digital Guardian LLC

- 6.4.6 Forcepoint LLC

- 6.4.7 Proofpoint, Inc.

- 6.4.8 Zscaler, Inc.

- 6.4.9 Trend Micro Incorporated

- 6.4.10 Check Point Software Technologies Ltd.

- 6.4.11 Cisco Systems, Inc.

- 6.4.12 Palo Alto Networks, Inc.

- 6.4.13 CrowdStrike Holdings, Inc.

- 6.4.14 Netskope, Inc.

- 6.4.15 Trellix Corporation

- 6.4.16 Spirion LLC

- 6.4.17 Safetica, a.s.

- 6.4.18 Code42 Software, Inc.

- 6.4.19 Nightfall AI, Inc.

- 6.4.20 Cyera, Inc.

- 6.4.21 Fortinet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment