|

시장보고서

상품코드

2043855

5G 칩셋 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)5G Chipset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

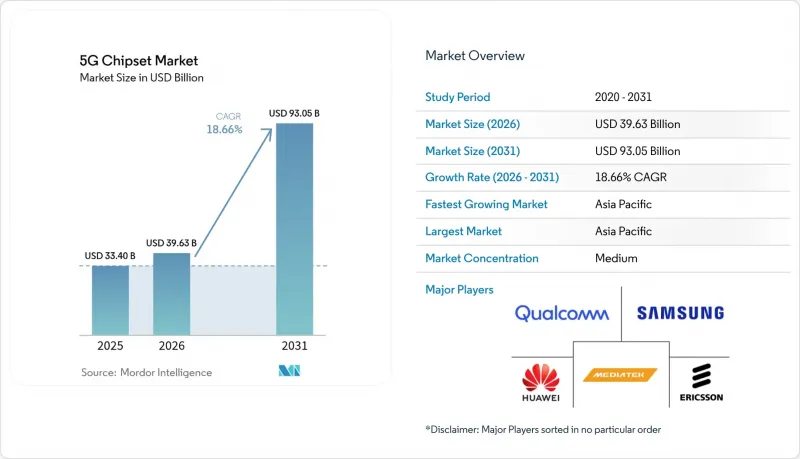

5G 칩셋 시장 규모는 2025년 334억 달러로 평가되었습니다. 2026년 396억 3,000만 달러에서 2031년까지 930억 5,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 18.66%를 나타낼 전망입니다.

지속적인 인프라 투자, 엣지 AI 워크로드 증가, 프라이빗 네트워크 도입 확대는 전용 실리콘에 대한 수요를 지속적으로 견인하고 있습니다. Sub-6GHz 대역의 출시로 공급량은 높은 수준을 유지하는 한편, mm파(mmWave) 및 3nm 이하 공정으로의 전환은 프리미엄 가격 책정을 통해 부가가치를 창출하고 있습니다. 정부의 인센티브, 특히 527억 달러 규모의 'CHIPS법'은 미국 내 팹(반도체 제조 공장)의 생산 능력을 확대하는 데 큰 역할을 하고 있습니다. 수출 규제와 갈륨 공급을 둘러싼 지정학적 리스크가 높아지면서 이중 소싱 전략의 필요성이 부각되고 있습니다. 이러한 배경에서 5G 칩셋 시장은 차별화된 지적재산권(IP)과 공급 탄력성을 확보하기 위해 장치 제조업체와 네트워크 벤더 간의 수직적 통합이 강화되면서 수혜를 받고 있습니다.

세계의 5G 칩셋 시장 동향과 인사이트

전 세계 5G RAN 구축 급증으로 인프라 반도체 수요 견인

상용 5G의 인구 커버리지는 2024년 40%에서 2029년 80%를 나타낼 것으로 예측되며, 이에 따라 통신사업자들은 네트워크 밀도를 높이고 대용량 백홀에 투자해야 하는 상황입니다. 스몰셀 아키텍처에는 미드밴드 및 mm파(mmWave) 동작에 최적화된 효율적인 RF 프론트엔드 모듈이 필요하며, 대규모 MIMO 도입에는 에너지 소비를 억제하는 고급 전원 관리 IC가 필요합니다. 수요 급증은 아시아태평양에서 가장 두드러지며, 중국에서는 2024년에만 80만 개 이상의 5G 기지국이 추가될 것으로 예측됩니다. 이러한 요인들로 인해 디지털 및 아날로그 5G 칩셋 시장 진출기업 모두에게 폭넓은 수익 기반이 유지되고 있습니다.

mm파 대역의 주파수 경매, 첨단 반도체 기술 기회 창출

24-47GHz 대역의 적극적인 주파수 경매를 통해 미국, 일본, 한국에서는 2024년 이후 350억 달러 이상의 입찰금액을 유치한 바 있습니다. mm파의 짧은 전파 거리 특성으로 인해 첨단 빔포밍 IC, 고선형성 전력 증폭기, 적응형 안테나 조정 칩이 필수적이며, 이는 모두 높은 매출 총이익률을 가져옵니다. 고정형 무선 액세스의 확산은 특히 열 설계와 수율 향상에 중점을 두고 있으며, 강력한 보정 소프트웨어를 갖춘 통합 프런트엔드 레퍼런스 디자인을 제공할 수 있는 벤더에게 유리합니다.

지정학적 수출 규제가 반도체의 전략적 병목현상을 야기하고 있습니다.

미국 산업보안국(BIS)은 특정 중국 팹리스 기업에 대한 고급 EDA 툴, 리소그래피 시스템 및 HBM의 수출을 제한하는 기업 목록을 확대했습니다. 중국의 갈륨 및 게르마늄 수출 제한 조치로 인해 갈륨 가격은 150% 상승하고 미국 GDP는 34억 달러 감소할 수 있습니다. 이러한 움직임으로 인해 설계 업체들은 노드 재인증, 재고 버퍼 구축 및 다양한 공급 경로를 확보해야 하며, 이는 5G 칩셋 시장 전체의 단기적인 수익성을 떨어뜨릴 수 있습니다.

부문 분석

2025년에는 OEM 업체들이 전력 효율에 최적화된 용도 특화형 성능을 추구한 결과, ASIC가 매출 점유율 25.40%로 가장 큰 비중을 차지했습니다. 이러한 장점은 레이어 1의 스케줄링 작업을 오프로드하는 무선 유닛용 베이스밴드 프로세서에서 두드러지게 나타납니다. 반면, FPGA는 진화하는 3GPP 릴리스에 대한 재구성성을 강조하는 Open RAN의 파일럿 프로젝트에 힘입어 19.94%의 연평균 복합 성장률(CAGR)로 다른 모든 경쟁 제품을 능가하는 성장이 예상됩니다. ASIC 기반 베이스밴드 유닛에 할당된 5G 칩셋 시장 규모는 2031년까지 342억 달러에 달할 것으로 예측됩니다. 모뎀을 통합한 시스템온칩(SoC) 솔루션은 PCB 면적을 줄이고 부품 비용을 절감할 수 있어 스마트폰, 웨어러블 기기, C-V2X 모듈에서 지속적으로 인기를 얻고 있습니다.

FPGA는 또한 x86 서버의 순방향 오류 수정 작업을 줄여주는 인라인 가속기 카드의 기반이 되어 가상화 RAN 배포의 스펙트럼 효율을 향상시킵니다. RFIC는 안정적인 출하량을 유지하고 있으며, 광대역 프론트엔드 필터링 및 위상 어레이 빔 포밍을 중대역 및 mm파 대역 모두에서 실현하고 있습니다. mm파 기술 칩, 안테나 튜너, LNA, 전력 증폭기 및 전력 관리 IC는 자유롭게 조합할 수 있는 레퍼런스 디자인을 중심으로 에코시스템을 구성하고 있습니다. 이러한 카테고리가 결합되어 5G 칩셋 시장은 범용 제품 분야와 고수익 틈새 시장 모두에서 호황을 누리고 있습니다.

스마트폰용 모뎀 및 클라우드 가속기 ASIC의 테이프아웃 물량이 견조한 가운데, 5nm 플랫폼은 2025년 매출의 31.10%를 차지했습니다. 그러나 엣지 AI 워크로드에서는 와트당 우수한 성능이 요구되기 때문에 3nm 미만 웨이퍼가 20.12%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. TSMC가 2025년 하반기에 N2 공정 양산을 시작하고 삼성이 MBCFET GAA(Gate All Around) 아키텍처를 도입함에 따라 2nm 칩의 5G 칩셋 시장 점유율은 상승할 것으로 예측됩니다. 7nm는 여전히 중급 휴대전화를 위한 주요 공정 노드이며, 16nm와 28nm는 비용 중심의 IoT 게이트웨이와 RF 스위치 매트릭스용으로 계속 채택될 것입니다.

28nm 이상의 성숙한 공정 노드는 전압 허용 오차가 집적도보다 중요시되는 전원 관리 및 아날로그 주변기기의 기반이 되고 있습니다. 이러한 균형 잡힌 노드 구성은 수요 및 공급의 변동을 완화하고, 지정학적 요인이나 자연재해로 인한 충격으로 최첨단 생산 능력이 중단되는 경우에도 가용성을 보장할 수 있는 설계 유연성을 제공합니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 47.50%를 차지했으며, 2031년까지 연평균 19.22%의 성장률을 나타낼 것으로 전망됩니다. 중국은 수출 규제 압력에도 불구하고 2025년 중반까지 180만 개 이상의 5G 기지국을 설치하여 RF 프론트엔드 및 베이스밴드 ASIC에 대한 국내 수요를 확보했습니다. 한국과 일본은 mm파(mmWave) 밀도 향상을 중시하고 있으며, 수익성이 높은 칩셋 부품 구성을 촉진하고 있습니다. 인도의 PLI(생산 연동형 인센티브) 제도는 28nm 전력 관리 및 RF 스위치 노드를 대상으로 하는 신흥 팹 프로젝트를 지원하여 지역 공급의 다양성을 확대되고 있습니다.

북미는 CHIPS 법에 의한 자금 투입과 초기 mm파 도입의 혜택을 누리고 있습니다. 미국은 전 세계 mm파 디바이스 출하량의 80% 이상을 차지하며 빔포밍 IC 수요를 주도하고 있습니다. 캐나다는 6GHz 미만의 C-band 프론트엔드를 선호하는 지방 고정형 무선 이니셔티브에 집중하고 있습니다. 유럽은 독립형(SA) 코어 채택이 뒤쳐져 있으며, 2025년 기준 완전한 SA 기능을 갖춘 기지국은 2%에 불과합니다. 이는 미국의 24%에 비해 낮은 수치입니다. 그러나 북유럽 통신 사업자들은 거의 완벽한 커버리지를 유지하고 있으며, 추운 지역에 적합한 에너지 절약형 매크로셀을 위한 지역 밀착형 실리콘 부품에 대한 수요를 주도하고 있습니다.

중동 및 아프리카에서는 걸프협력회의(GCC) 회원국들이 대규모 IoT 회랑을 구축하고 있으며, 꾸준한 성장세를 보이고 있습니다. 남미에서는 브라질이 발전하는 반면 아르헨티나는 거시경제적 제약에 직면해 있어 진행상황이 엇갈리고 있습니다. 전반적으로, 지역 정책 지원과 주파수 할당 속도는 5G 칩셋 시장의 모멘텀을 좌우하는 주요 요인으로 작용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

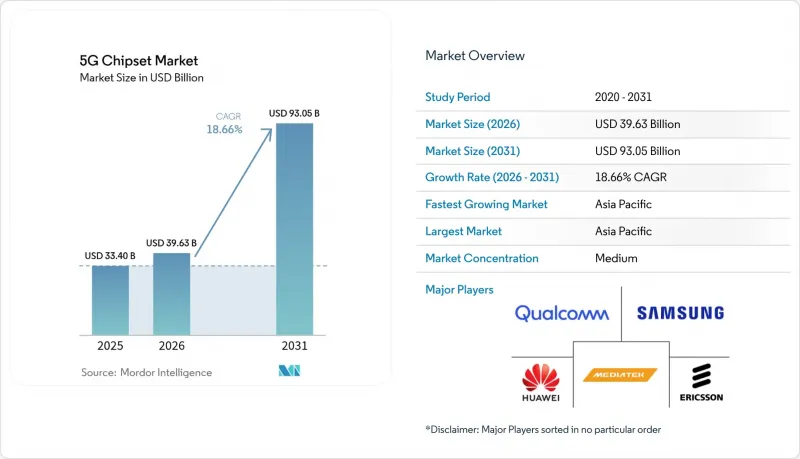

KTH 26.05.29The 5G Chipset Market size is projected to expand from USD 33.40 billion in 2025 and USD 39.63 billion in 2026 to USD 93.05 billion by 2031, registering a CAGR of 18.66% between 2026 to 2031.

Sustained infrastructure spending, growing edge-AI workloads, and intensified private-network adoption continue to fuel demand for specialized silicon. Sub-6 GHz roll-outs keep volumes high, while mmWave and sub-3 nm migrations add value through premium pricing. Government incentives, most notably the USD 52.7 billion CHIPS Act, are boosting domestic fab capacity in the United States. Rising geopolitical risk around export controls and gallium supply underscores the need for dual-sourcing strategies. Against this backdrop, the 5G chipset market is benefiting from tighter vertical integration among device makers and network vendors that seek to secure differentiated IP and supply resilience.

Global 5G Chipset Market Trends and Insights

Surging Global 5G RAN Roll-outs Drive Infrastructure Semiconductor Demand

Commercial 5G population coverage is set to reach 80% by 2029, up from 40% in 2024, pushing operators to densify networks and invest in high-capacity backhaul. Small-cell architectures require efficient RF front-end modules optimized for mid-band and mmWave operation, while massive MIMO deployments call for advanced power-management ICs that keep energy budgets in check. Demand spikes are most visible across Asia-Pacific, where China added over 800,000 5G base stations in 2024 alone. These factors sustain a broad revenue base for both digital and analog 5G chipset market participants.

mmWave Spectrum Auctions Unlock Advanced Silicon Opportunities

Aggressive spectrum auctions in the 24-47 GHz bands have attracted more than USD 35 billion in bids since 2024 in the United States, Japan, and South Korea. mmWave's short propagation range mandates advanced beam-forming ICs, high-linearity power amplifiers, and adaptive antenna-tuning chips, each commanding premium gross margins. Fixed-wireless access roll-outs place particular stress on thermal design and yield improvements, rewarding vendors that can offer integrated front-end reference designs with robust calibration software.

Geopolitical Export Controls Create Strategic Semiconductor Bottlenecks

The U.S. Bureau of Industry and Security has expanded its Entity List to restrict the export of advanced EDA tools, lithography systems, and HBM to select Chinese fabless firms. China's countermeasure limiting gallium and germanium exports could raise gallium prices by 150% and shave USD 3.4 billion off U.S. GDP. These moves force design houses to requalify nodes, build inventory buffers, and invest in diversified supply routes, trimming near-term profitability across the 5G chipset market.

Other drivers and restraints analyzed in the detailed report include:

- Edge-AI Workloads Accelerate Advanced Node Adoption

- Open RAN Disaggregation Transforms Vendor Ecosystem Dynamics

- Supply-Chain Fragility Threatens Compound Semiconductor Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ASICs captured the largest 25.40% revenue share in 2025 as OEMs pursued power-optimized, application-specific performance. This dominance is evident in radio-unit baseband processors that offload Layer-1 scheduling duties. By contrast, FPGAs are forecast to outpace all peers at a 19.94% CAGR, buoyed by Open RAN pilots that value reconfigurability for evolving 3GPP releases. The 5G chipset market size allocated to ASIC-based baseband units is expected to reach USD 34.2 billion by 2031. System-on-Chip solutions with integrated modems continue gaining popularity in smartphones, wearables, and C-V2X modules because they shrink PCB footprint and lower bill-of-materials costs.

FPGAs also underpin inline accelerator cards that relieve x86 servers of forward-error correction tasks, thereby improving spectral efficiency in virtualized RAN deployments. RFICs maintain steady volume, delivering wide-band front-end filtering and phase-array beam-forming at both mid-band and mmWave frequencies. Millimeter-wave technology chips, antenna tuners, LNAs, power amplifiers, and power-management ICs round out an ecosystem built around mix-and-match reference designs. Collectively, these categories ensure that the 5G chipset market remains vibrant across both commodity and high-margin niches.

The 5 nm platform accounted for 31.10% of 2025 sales thanks to strong tape-out volume from smartphone modems and cloud accelerator ASICs. Yet sub-3 nm wafers will generate the fastest 20.12% CAGR because edge-AI workloads demand superior performance per watt. The 5G chipset market share for 2 nm chips is projected to climb as TSMC ramps N2 in H2 2025 and Samsung introduces MBCFET gate-all-around architecture. 7 nm remains the node of choice for mid-range handsets, while 16 nm and 28 nm continue serving cost-sensitive IoT gateways and RF switch matrices.

Mature nodes above 28 nm anchor power-management and analog peripherals, where voltage tolerance outweighs density. This balanced node mix cushions supply-demand swings and offers design-for-availability flexibility when geopolitical or natural-disaster shocks disrupt cutting-edge capacity.

The 5G Chipset Market Report is Segmented by Chipset Type (Application-Specific Integrated Circuits, System-On-Chip With Integrated Modem, and More), Technology Node (<3nm, 3nm, 5nm, 7nm, and More), Operational Frequency (Sub-6 GHz, 26-39 GHz, and Above 39 GHz), End-User Industry (IT, Telecom and Network Infrastructure, Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 47.50% of global revenue in 2025 and is projected to grow at a 19.22% CAGR through 2031. China alone installed more than 1.8 million 5G base stations by mid-2025 despite export-control pressure, securing local demand for RF front-ends and baseband ASICs. South Korea and Japan emphasize mmWave densification, encouraging higher-margin chipset bill-of-materials. India's PLI scheme supports emerging fab projects targeting 28 nm power-management and RF switch nodes, broadening regional supply diversity.

North America benefits from the CHIPS Act's infusion and early mmWave adoption. The United States accounts for over 80% of global mmWave device shipments and drives demand for beam-forming ICs. Canada focuses on rural fixed-wireless initiatives that favor sub-6 GHz C-band front-ends. Europe lags in standalone-core adoption; only 2% of sites had full SA functionality by 2025, compared with 24% in the United States. Nordic operators, however, maintain near-complete coverage, driving localized silicon content for energy-efficient macro-cells suited to cold climates.

The Middle East and Africa experience stepped growth, with Gulf Cooperation Council nations building large-scale IoT corridors. South America sees uneven progress as Brazil pushes forward while Argentina grapples with macroeconomic constraints. Overall, regional policy support and spectrum allocation pace remain leading determinants of 5G chipset market momentum.

List of Companies Covered in this Report:

- Qualcomm Incorporated

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Broadcom Inc.

- Fujitsu Limited

- Renesas Electronics Corporation

- Marvell Technology, Inc.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Murata Manufacturing Co., Ltd.

- Anokiwave, Inc.

- pSemi Corporation

- GlobalFoundries Inc.

- Taiwan Semiconductor Manufacturing Company Ltd.

- United Microelectronics Corporation

- Cree Wolfspeed, Inc.

- Integrated Device Technology, Inc. (Renesas Subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Global 5G RAN Roll-outs

- 4.2.2 mmWave Spectrum Auctions Unlocking New Silicon Demand

- 4.2.3 Edge-AI Workloads Shifting Toward 5 nm and Below Nodes

- 4.2.4 Open RAN Disaggregation Driving Merchant Silicon Uptake

- 4.2.5 Private-5G Adoption Across Industry 4.0 Facilities

- 4.2.6 Government CHIPS-style Subsidies for Domestic Fabs

- 4.3 Market Restraints

- 4.3.1 Geopolitical Export Controls on Advanced Nodes

- 4.3.2 Supply-chain Fragility for Compound Semiconductors

- 4.3.3 High Cap-ex Requirements Below 3 nm

- 4.3.4 Power-efficiency Trade-offs in mmWave Devices

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Chipset Type

- 5.1.1 Application-Specific Integrated Circuits (ASICs)

- 5.1.2 System-on-Chip with Integrated Modem (SoC)

- 5.1.3 Radio-Frequency Integrated Circuits (RFICs)

- 5.1.4 Millimeter-Wave Technology Chips

- 5.1.5 Field-Programmable Gate Arrays (FPGAs)

- 5.1.6 Power Management ICs

- 5.1.7 Antenna Tuner ICs

- 5.1.8 Switches

- 5.1.9 LNAs and Power Amplifiers

- 5.1.10 Others (Filters, Discrete Memory, Converters, etc.)

- 5.2 By Technology Node

- 5.2.1 < 3 nm

- 5.2.2 3 nm

- 5.2.3 5 nm

- 5.2.4 7 nm

- 5.2.5 16 nm

- 5.2.6 28 nm

- 5.2.7 > 28 nm

- 5.3 By Operational Frequency

- 5.3.1 Sub-6 GHz

- 5.3.2 26-39 GHz

- 5.3.3 Above 39 GHz

- 5.4 By End-User Industry

- 5.4.1 IT, Telecom and Network Infrastructure

- 5.4.2 Consumer Electronics (incl. Smart Home)

- 5.4.3 Industrial Automation

- 5.4.4 Automotive and Transportation

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare

- 5.4.7 Retail

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Singapore

- 5.5.4.6 Australia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Qualcomm Incorporated

- 6.4.2 MediaTek Inc.

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Huawei Technologies Co., Ltd.

- 6.4.5 Telefonaktiebolaget LM Ericsson

- 6.4.6 Nokia Corporation

- 6.4.7 Broadcom Inc.

- 6.4.8 Fujitsu Limited

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 Marvell Technology, Inc.

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 NXP Semiconductors N.V.

- 6.4.13 Skyworks Solutions, Inc.

- 6.4.14 Qorvo, Inc.

- 6.4.15 Analog Devices, Inc.

- 6.4.16 STMicroelectronics N.V.

- 6.4.17 Infineon Technologies AG

- 6.4.18 Murata Manufacturing Co., Ltd.

- 6.4.19 Anokiwave, Inc.

- 6.4.20 pSemi Corporation

- 6.4.21 GlobalFoundries Inc.

- 6.4.22 Taiwan Semiconductor Manufacturing Company Ltd.

- 6.4.23 United Microelectronics Corporation

- 6.4.24 Cree Wolfspeed, Inc.

- 6.4.25 Integrated Device Technology, Inc. (Renesas Subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment