|

시장보고서

상품코드

2043862

미국의 공작기계 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Machine Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

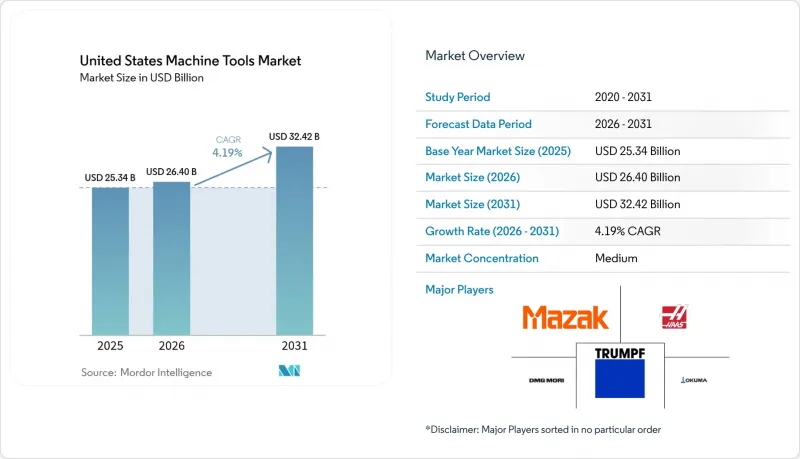

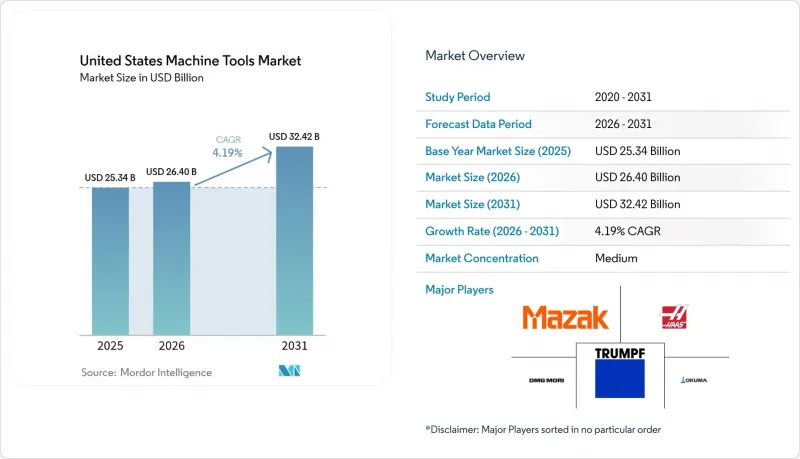

미국의 공작기계 시장 규모는 2025년에 253억 4,000만 달러로 평가되었습니다. 2026년 264억 달러에서 2031년까지 324억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.19%를 나타낼 전망입니다.

연방법인 '인프라 투자 및 고용법', 'CHIPS 및 과학법', '인플레이션 억제법'에 따라 이미 2조 달러 이상의 지출이 승인되었으며, 2021년부터 2024년까지 제조업의 건설 지출은 2배로 증가하고, 반도체, 배터리, 방위산업 분야에서 정밀기기에 대한 수요가 급증했습니다. 공급업체들은 AI 기반 개조 키트를 통해 사이클 타임을 최대 12% 단축시켜 정책금리가 완만하게 인하되고 있는 상황에서도 구매자가 설비 투자를 정당화할 수 있도록 돕고 있습니다. 2024년 공장 평균 임금보다 1.8% 포인트 높은 숙련 기계공의 임금 상승은 노동력 절감을 위한 자동화에 대한 시급성을 높이고 있지만, 높은 자금 조달 비용으로 인해 투자 회수 기간이 길어지고 있습니다. 원자재 가격의 변동도 상황을 더욱 복잡하게 만들고 있습니다. 2025년 초, 텅스텐 카바이드 가격이 전년 대비 22% 상승하여 OEM 업체들은 마진을 안정화하기 위해 공구 홀더의 구성을 변경하거나 고정 가격 서비스 계약을 추진해야만 합니다.

미국의 공작기계 시장 동향과 인사이트

IRA, CHIPS, IIJA의 설비투자 활성화 방안

연방정부의 인센티브에 따라 원래 10년에 걸쳐 진행되어야 할 설비투자가 3년으로 앞당겨졌습니다. 반도체 및 배터리 산업 클러스터에서는 웨이퍼 및 전극을 가공할 수 있는 첨단 연삭기, 방전가공기, 5축 가공기 등을 주문했습니다. 초기 자금 지출은 2024-2025년에 정점을 찍었지만, 지불 조건을 보조금 마일스톤에 연동하는 공급업체는 민간으로부터 추가 자금이 확보될 때까지 점유율을 유지할 수 있을 것으로 보입니다. 특히 배터리용 분리막과 포일에서 공급망 중류에서 공급 부족이 발생할 수 있으며, 2027년 이후 공작기계 수주가 둔화될 수 있습니다. 성공의 열쇠는 제품 로드맵을 CHIPS 법의 나머지 자금 배분 프레임과 일치시키는 데 달려 있습니다.

EV 및 배터리 기가팩토리에서의 정밀 공작기계 수요

기가팩토리는 레이저 용접기, 고속 프레스 등의 판매는 활발하게 이루어지고 있지만, 현장의 가공 수요가 예상보다 낮아 범용 선반과 밀링 머신의 수주가 억제되고 있습니다. 완성차 업체들은 자체 셀 생산과 합작 투자를 통한 공급 계약을 비교 검토하고 있으며, 여전히 신중한 태도를 유지하고 있습니다. 셀의 형태와 화학적 구성이 빠르게 진화하고 있기 때문에 재구성 가능한 셀과 IATF 16949 인증을 강조하는 벤더들이 인기를 끌고 있습니다. 모듈형 설비를 화학 성분 변화에 대한 헤지 수단으로 포지셔닝하는 것은 2026년부터 2028년까지 지연된 수주를 확보하는 데 있어 매우 중요합니다.

숙련된 공작기계공의 임금 상승

2024년 공작기계 작업자의 시간당 평균 임금은 24.82달러로 일반 공장 근로자의 임금보다 높아져 가격 경쟁력이 낮은 수탁 가공업체의 이윤을 압박했습니다. 임금 상승은 기업의 자동화 추진을 촉진하는 한편, 이와 유사한 비용 압박으로 인해 투자 회수율(ROI)이 높아져 수주가 둔화되고 있습니다. 턴키 방식의 로봇 셀에 성능 보증을 결합한 솔루션을 제공하는 공급업체는 임금 충격을 완화하고 구매자의 신뢰를 회복하고 있습니다.

부문 분석

2025년 매출에서 밀링 머신이 차지하는 비중은 30.32%로 미국의 공작기계 시장에서 가장 큰 점유율을 차지했습니다. 그러나 다축 머시닝 센터는 2031년까지 연평균 5.41% 성장할 것으로 예상되며, 가장 빠르게 성장하는 하위 카테고리입니다. 원 셋업 기능은 환자별 임플란트에 대한 FDA의 검증 지침과 ASME B5.54의 성능 기준을 충족합니다. 레이저, 방전가공(EDM), 워터젯, 플라즈마 가공기는 전체 매출의 약 20%를 차지하며, 비접촉 가공을 통해 공구 마모를 줄일 수 있는 분야에서 수요가 증가하고 있습니다. 공급망이 짧아지고 로트 사이즈가 축소됨에 따라 구매자는 단순한 처리 능력보다 유연성을 중시하게 되었고, 다축 가공기나 레이저 가공 솔루션을 선호하는 경향이 있습니다.

또한, 다축 가공의 도입으로 고정비를 다양한 공작물에 분산시킬 수 있어 수요 변동에 대한 중요한 리스크 헤지가 가능합니다. DMG MORI와 Mazak과 같은 기업들은 디지털 트윈을 새로운 기종에 번들로 제공하고 가상 시운전을 통해 ROI를 입증하고 있습니다. 한편, TRUMPF의 베벨 커팅 레이저 시리즈는 용접 준비 시간을 최대 40%까지 단축합니다. 이러한 특징이 결합되어 단일 용도 드릴 및 연삭기에 대한 투자가 감소하고 있으며, 미국의 공작기계 시장에서 구성 가능한 플랫폼의 우위가 더욱 강화되고 있습니다.

CNC 공작기계는 2025년 기술 매출의 66.56%를 차지했으며, 이는 미국 공작기계 시장에서의 수십 년간의 도입 실적의 우위를 반영합니다. 생성형 AI 애드온이 섀시 교체 없이도 생산성을 향상시킬 수 있기 때문에 이 부문은 2031년까지 연평균 복합 성장률(CAGR) 5.19%의 견조한 성장세를 유지할 것으로 예측됩니다. 기존의 수동식 장비는 학교나 수리공장에 남아 있지만, 임금 상승과 안전 규제 강화로 인해 그 수가 감소하는 추세입니다. 하이브리드형(적층가공과 절삭가공을 병행하는) 장비는 전체 판매량의 10% 미만에 불과하지만, 니어 네트 쉐이프(Near Net Shape, 성형 후 형상에 가까운 형상)로 폐기물을 줄일 수 있는 항공우주 시제품이나 의료용 임플란트 분야에서 틈새 시장을 개척하고 있습니다.

경쟁 환경은 점점 더 치열해지고 있습니다. 아시아 신규 진입 업체 중 일부는 현재 포지셔닝 정확도에서 기존 업체들과 동등한 성능을 구현하면서도 정가를 20-30% 낮게 책정하고 있습니다. 따라서 기존 제조업체들은 자체 소프트웨어 생태계, 공구 마모 예측, 클라우드 대시보드, 종량제 분석 기능을 번들로 묶어 서비스 수익을 확보하려 하고 있습니다. 이러한 서비스 중심의 자세는 미국의 공작기계 산업 전반에서 하드웨어가 상품화되는 상황에서도 수익률을 유지하는 데 도움이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe United States machine tools market size was valued at USD 25.34 billion in 2025 and is estimated to grow from USD 26.40 billion in 2026 to reach USD 32.42 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031).

Federal legislation, the Infrastructure Investment and Jobs Act, CHIPS and Science Act, and Inflation Reduction Act have already triggered more than USD 2 trillion in authorized outlays, doubling manufacturing construction spending between 2021 and 2024 and sharply lifting demand for precision equipment across semiconductor, battery, and defense corridors.Suppliers are responding with AI-enabled retrofit kits that shorten cycle times by up to 12%, helping buyers justify capex even as policy rates soften only gradually. Wage inflation for skilled machinists, which ran 1.8 percentage points ahead of average factory pay in 2024, is adding urgency to labor-saving automation but is also lengthening payback horizons where financing costs remain high.Commodity swings compound the picture: tungsten-carbide inputs rose 22% year-over-year in early 2025, forcing OEMs to alter toolholder compositions and push fixed-price service contracts to stabilize margins.

United States Machine Tools Market Trends and Insights

IRA, CHIPS & IIJA CapEx Stimulus

Federal incentives front-loaded what would have been a decade of capital spending into a three-year window. Semiconductor and battery corridors ordered advanced grinders, EDM units, and 5-axis centers capable of wafer and electrode processing. While early disbursements peaked in 2024-2025, suppliers tying payment terms to grant milestones stand to hold share until private follow-on funds materialize. The possibility of midstream supply-chain gaps, especially in battery separators and foils, could moderate tooling orders after 2027. Success will depend on synchronizing product roadmaps with the remaining CHIPS Act tranches.

EV and Battery-Gigafactory Precision-Tooling Demand

Gigafactories have driven brisk sales of laser welders and high-speed presses, yet lower-than-expected onsite machining intensity has curbed orders for general-purpose lathes and mills. Automakers remain cautious, weighing in-house cell production against joint-venture supply pacts. Vendors highlighting reconfigurable cells and IATF 16949 documentation gain traction because cell formats and chemistries evolve quickly. Positioning modular equipment as a hedge against chemistry shifts is central to capturing delayed orders in 2026-2028.

Skilled-Machinist Wage Inflation

Median machinist pay hit USD 24.82 per hour in 2024, outpacing general factory wages and compressing margins for low-pricing-power job shops. While higher pay pushes firms toward automation, the same cost pressure raises ROI hurdles, slowing orders. Suppliers bundling turnkey robotic cells with performance guarantees cushion the wage shock and rebuild buyer confidence.

Other drivers and restraints analyzed in the detailed report include:

- Commercial and Defense Aerospace Titanium-Machining Rebound

- Industry 4.0 Retrofit Acceleration

- High Interest-Rate-Driven Payback Extension

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Milling machines accounted for 30.32% of 2025 revenue, the largest slice of the United States machine tools market share. However, multi-axis machining centers are projected to grow at 5.41% annually through 2031, the fastest-rising subcategory. Their single-setup capability aligns with FDA validation guidance for patient-specific implants and with ASME B5.54 performance benchmarks. Laser, EDM, waterjet, and plasma units jointly hold roughly 20% of sales and gain traction where contactless processing reduces tool wear. As supply chains shorten and batch sizes shrink, buyers value flexibility over raw throughput, favoring multi-axis and laser solutions.

Multi-axis adoption also spreads fixed costs across varied workpieces, an important hedge against demand volatility. Companies like DMG MORI and Mazak bundle digital twins with new machines to prove ROI via virtual commissioning, while TRUMPF's bevel-cut laser series cuts weld-prep time by up to 40%. Collectively, these features are steering capital away from single-purpose drills or grinders, reinforcing a premium position for configurable platforms within the United States machine tools market.

CNC machines commanded 66.56% of 2025 technology sales, reflecting decades of installed-base advantages in the United States machine tools market. The segment is still forecast to advance at a robust 5.19% CAGR through 2031 as generative-AI add-ons lift productivity without requiring chassis replacement. Conventional manual equipment lingers in schools and repair shops but faces attrition as wages rise and safety regulations tighten. Hybrid additive-subtractive units, although below 10% of volume, are carving a niche in aerospace prototypes and medical implants where near-net shapes curb waste.

Competitive dynamics are intensifying. Several Asian entrants now match positional accuracy at 20-30% lower list prices. Incumbents therefore bundle proprietary software ecosystems, tool-wear prediction, cloud dashboards, and pay-per-use analytics to lock in service revenue. This service-centric stance helps defend margins even as hardware commoditizes within the broader United States machine tools industry.

The United States Machine Tools Market Report is Segmented by Product Type (Metal Cutting Tools (Milling Machines, and More), Metal Forming Tools (Presses and More)), by Technology (Conventional, CNC, Additive/Hybrid), by End-User Industry (Automotive, Aerospace & Defense, Electrical & Electronics, and More), and by Sales Channel (Direct Sales, Dealers, Online/E-commerce). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Haas Automation

- TRUMPF Inc.

- DMG MORI USA

- Mazak Corp.

- Okuma America

- Amada America

- Lincoln Electric

- Hardinge Inc.

- Hurco Companies

- Fives Machining Systems

- JTEKT (Toyoda)

- MC Machinery Systems

- Bystronic Inc.

- Mate Precision Tooling

- Cincinnati Inc.

- Koike Aronson

- FANUC America

- United Grinding NA

- Starrag USA

- GROB Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IRA, CHIPS & IIJA CapEx stimulus

- 4.2.2 EV & battery-gigafactory precision-tooling demand

- 4.2.3 Commercial & defence aerospace titanium-machining rebound

- 4.2.4 Industry 4.0 retrofit acceleration

- 4.2.5 DoD hypersonic-materials machining niche

- 4.2.6 Generative-AI adaptive tool-path ROI

- 4.3 Market Restraints

- 4.3.1 Skilled-machinist wage inflation

- 4.3.2 High interest-rate-driven payback extension

- 4.3.3 Volatile steel / rare-earth cost inflation

- 4.3.4 CMMC 2.0 compliance-cost burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (Key Government Regulations & Initiatives)

- 4.6 Technology Snapshot

- 4.6.1 Connected & Automated Machines

- 4.6.2 Advanced Controls / Motion Systems

- 4.6.3 Digitalisation & Industry 4.0

- 4.6.4 AI-Enhanced Metal Cutting Accuracy

- 4.7 Metalworking Industry Snapshot

- 4.8 Impact of Geopolitics on the Machine Tools Market

- 4.9 Industry Attractiveness - Porter?s Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product

- 5.1.1 Metal Cutting Tools

- 5.1.1.1 Milling Machines

- 5.1.1.2 Drilling Machines

- 5.1.1.3 Turning (Lathe) Machines

- 5.1.1.4 Grinding Machines

- 5.1.1.5 Laser Cutting Machines

- 5.1.1.6 Electrical Discharge Machines (EDM)

- 5.1.1.7 Waterjet Cutting Machines

- 5.1.1.8 Plasma Cutting Machines

- 5.1.1.9 Multi-Axis Machining Centres

- 5.1.1.10 Others (Boring, etc.)

- 5.1.2 Metal Forming Tools

- 5.1.2.1 Presses (Mechanical, Hydraulic, Servo)

- 5.1.2.2 Forging Machines

- 5.1.2.3 Bending Machines

- 5.1.2.4 Others (Shearing, Extrusion, Rolling, etc.)

- 5.1.1 Metal Cutting Tools

- 5.2 By Technology

- 5.2.1 Conventional Machines (Manually or Semi-Manually)

- 5.2.2 CNC Machines

- 5.2.3 Additive Manufacturing / Hybrid Machines

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defence

- 5.3.3 Electrical & Electronics

- 5.3.4 Industrial Machinery & Equipment

- 5.3.5 Medical Devices

- 5.3.6 Shipbuilding & Marine

- 5.3.7 Precision Engineering

- 5.3.8 Energy & Power

- 5.3.9 Metal Fabrication (Job Shops, etc.)

- 5.3.10 Other Industries (Railway, Other General Manufacturing, etc.)

- 5.4 By Sales Channel

- 5.4.1 Direct Sales (OEMs to End Users)

- 5.4.2 Dealers & Distributors

- 5.4.3 Online / E-commerce

- 5.4.4 Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Haas Automation

- 6.4.2 TRUMPF Inc.

- 6.4.3 DMG MORI USA

- 6.4.4 Mazak Corp.

- 6.4.5 Okuma America

- 6.4.6 Amada America

- 6.4.7 Lincoln Electric

- 6.4.8 Hardinge Inc.

- 6.4.9 Hurco Companies

- 6.4.10 Fives Machining Systems

- 6.4.11 JTEKT (Toyoda)

- 6.4.12 MC Machinery Systems

- 6.4.13 Bystronic Inc.

- 6.4.14 Mate Precision Tooling

- 6.4.15 Cincinnati Inc.

- 6.4.16 Koike Aronson

- 6.4.17 FANUC America

- 6.4.18 United Grinding NA

- 6.4.19 Starrag USA

- 6.4.20 GROB Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment