|

시장보고서

상품코드

2043865

디지털 교실 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Classroom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

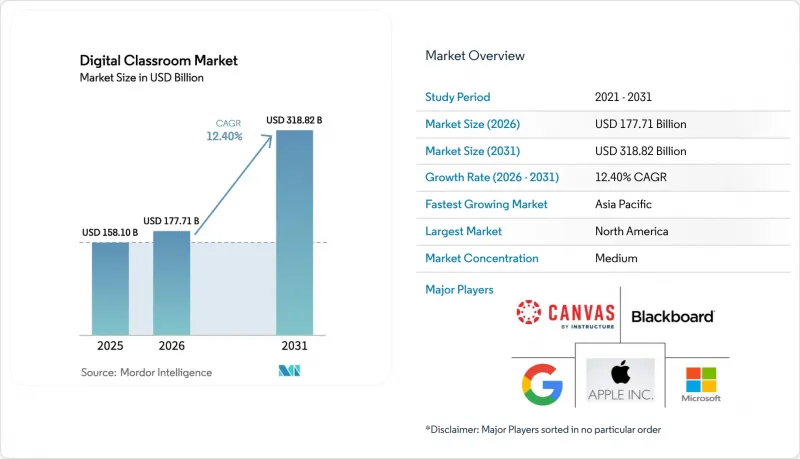

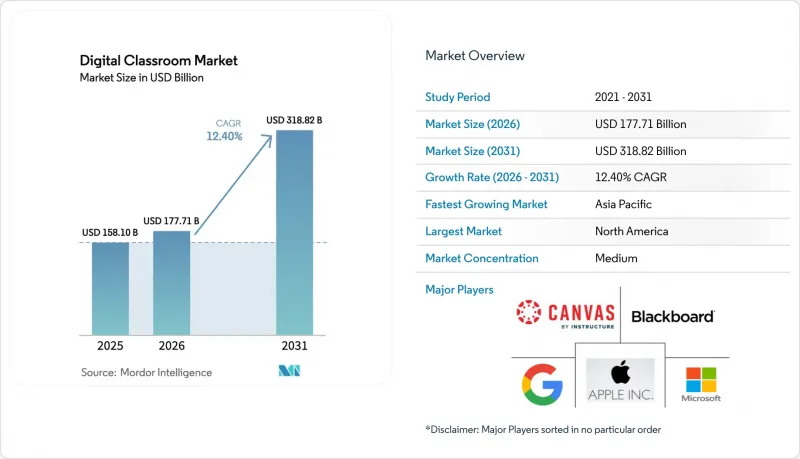

디지털 교실 시장 규모는 2025년 1,581억 달러로 평가되었습니다. 2026년 1,777억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 12.40%를 나타내, 2031년에는 3,188억 2,000만 달러에 이를 것으로 예측됩니다.

2025년 북미가 62.21%의 시장 점유율을 차지했으며, 아시아태평양은 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 17.52%를 나타낼 것으로 예측됩니다. 이러한 성장은 정부의 투자와 대규모 학습자층의 클라우드 도입 확대에 힘입은 바 큽니다. 교육기관은 클라우드 네이티브 플랫폼, 컴플라이언스 대응 거버넌스, 내구성 높은 디바이스를 채택하고, 플랫폼 중심 모델로 전환하고 있습니다. FERPA, GDPR(EU 개인정보보호규정) 등의 규제 프레임워크가 조달에 영향을 미치고 있으며, 감사 가능성, ID 관리, 데이터 최소화가 강조되고 있습니다. 2024년 Instructure가 48억 달러에 인수한 것은 디지털 교실 시장에서 제품 혁신을 강화하고 세계 사업을 확장하기 위한 것으로, 업계의 통합이 진행되고 있음을 보여줍니다.

세계의 디지털 교실 시장 동향과 인사이트

광대역의 보급과 저렴한 가격의 디바이스로 인해 디지털 교실 시장에 대한 접근성이 확대되고 있습니다.

저렴한 가격의 클라우드 최적화 기기와 지역과 소득 수준에 관계없이 향상된 연결 환경으로 인해 디지털 교실 시장은 성장하고 있습니다. 현재 학군에서는 예산의 예측가능성을 보장하고 동시 지원 종료로 인한 혼란을 피하기 위해 일괄 구매보다 단계적 업데이트 일정을 선호하는 경향이 있습니다. 구글의 크롬OS 지원 기간 연장은 보안과 관리성을 유지하면서 총소유비용 절감에 기여하고 있습니다. 저궤도 위성은 원격지 학교까지 커버리지를 확장하고 있으며, 실시간 교육 및 클라우드 협업에 적합한 대역폭과 낮은 지연을 제공합니다. AI 기능을 갖춘 인터랙티브 디스플레이는 실시간 협업, 필사, 콘텐츠 검색을 가능하게 하여 연결된 교실의 기능을 향상시킵니다. 향상된 연결성과 향상된 디바이스 신뢰성은 하이브리드 사용 모델을 지원하며, 인프라의 제한이나 유지보수 중에도 연속성을 보장합니다. 이러한 발전은 교실을 현대의 교육적 요구를 충족시키는 역동적이고 협력적인 환경으로 변화시키고 있습니다.

디지털 학습에 대한 정부의 투자로 교육 시스템 전반에 걸쳐 도입이 가속화되고 있습니다.

정부 프로그램은 디지털 플랫폼과 콘텐츠로의 전환을 가속화하고, 디지털 교실 시장에 대한 투자와 교사연수를 지원하고 있습니다. 미국 교육부는 2026년 1월, FIPSE 보조금으로 1억 6,900만 달러를 배정했으며, 그중 5,000만 달러는 교육 및 성과 향상을 위한 AI 이니셔티브에 사용되었습니다. 2025 회계연도 주요 K-12 프로그램의 보조금 보류 조치로 인해 필수 플랫폼과 컴플라이언스 서비스에 중점을 재분배하는 한편, 고등교육에 대한 투자에 있어서는 AI가 우선순위를 차지하게 되었습니다. 유럽연합(EU)의 '디지털 교육 행동계획(2027년)'은 디지털 기술, 교육자 교육, 인프라를 중점 분야로 삼고 있으며, 2030년까지 시민의 80%가 기본적인 디지털 기술을 습득하는 것을 목표로 하고 있습니다. 인도의 정책은 예산 배분으로 뒷받침되며, 새로운 역량 목표에 부합하는 기기, 콘텐츠, 교육에 대한 접근성을 확대되고 있습니다. 유네스코의 노력은 전 세계 지식의 공유를 촉진하고 중복을 줄이며, 확장 가능한 정책 및 플랫폼 모델을 지원하고 있습니다.

미국 K-12 교육에서 ESSER 종료 후 예산 급감에 따른 자금 조달 문제가 디지털 학습에 대한 지속적인 투자를 제한하고 있습니다.

ESSER 자금이 만료됨에 따라 각 학군의 재량 예산이 압박을 받고 있으며, 디지털 교실 시장의 보조 도구 업데이트에 대한 조사가 강화되고 있습니다. 2025 회계연도에 타이틀 I-C, 타이틀 II-A, 타이틀 IV-B 보조금에서 연방정부가 유보한 금액은 총 7억 달러에 달하며, 이는 필수 플랫폼으로의 전환, 다년 계약 및 보다 엄격한 조달 기준으로의 전환을 촉진했습니다. 일리노이주 학군에서는 구제기금이 거의 전액 활용된 반면, 시카고 공립학교는 2026년도 예산 적자에 직면해 인력 감축과 운영 체제의 변화를 강요당하고 있습니다. 컴플라이언스 및 일상 업무에 필수적인 LMS, SIS, ID 관리 서비스 등 기간계 시스템은 재량 계약보다 여전히 견조합니다. 팬데믹 기간 동안 도입된 장비의 노후화로 인해 하드웨어 업데이트 주기에 대한 압박이 증가하고 있으며, 단계적 업데이트와 보다 엄격한 라이프사이클 관리가 요구되고 있습니다. 측정 가능한 효율성, 컴플라이언스 문서, 안정적인 통합 로드맵을 제공할 수 있는 벤더는 고객 유지에 유리합니다.

부문 분석

2025년 디지털 교실 시장에서 소프트웨어는 42.31%의 점유율을 차지했습니다. 이는 클라우드 학습 플랫폼, 협업 도구, 그리고 지도 및 학생 운영 관리를 위한 분석 도구의 도입이 주도한 것입니다. 업계는 LMS, SIS, ERP 시스템을 통합한 솔루션으로 전환하고 있으며, 이를 통해 관리 업무를 줄이고 분석 기능을 향상시키고 있습니다. 전 세계 2억 명의 학습자에게 서비스를 제공하는 Canvas는 제품 개발을 가속화하고 세계 진출을 확대하기 위해 2024년 민간 기업으로 전환했습니다. PowerSchool은 5,000만 명 이상의 학생들을 지원하고 있으며, 출석 관리, 평가, 중재 계획을 위한 통합 플랫폼의 이점을 보여주고 있습니다. 이러한 추세는 벤더의 다양성을 줄이고, 프라이버시를 우선시하며, 디지털 교실에서 분석과 AI의 기반을 구축하는 조달 전략의 중요성을 강조하고 있습니다.

VR 및 AR 헤드셋은 하드웨어 하위 부문 중 가장 빠르게 성장하고 있으며, 실험실, 의료 및 직업 훈련 분야의 몰입형 시뮬레이션에 힘입어 2031년까지 19.56%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. 콘텐츠, 커리큘럼, 평가의 일관성이 향상되고 있는 것이 이러한 성장을 뒷받침하고 있습니다. 인터랙티브 디스플레이는 실시간 요약, 회의록 작성 등의 기능을 갖춘 AI 지원 협업 허브로 진화하고 있습니다. 출하 추세를 보면, 더 큰 포맷과 공유 디지털 캔버스가 선호되고 있음을 알 수 있습니다. 현재 디바이스 전략은 디지털 교실 시장에서 다운타임을 최소화하고 비용을 안정화하기 위해 수리 가능성, 배터리 수명 연장 및 차량 관리에 초점을 맞추었습니다.

디지털 교실 시장은 구성 요소(하드웨어, 소프트웨어, 서비스), 도입 형태(클라우드, On-Premise), 최종 사용자(초중고교, 고등교육기관, 기업 및 전문직 교육, 정부 및 비영리단체), 지역(북미, 남미, 아시아태평양, 유럽, 중동 및 아프리카)으로 구분됩니다. 구분되어 있습니다. 시장 예측은 10억 달러 단위로 제시되고 있습니다.

지역별 분석

북미는 높은 IT 인프라, 안정적인 플랫폼 파트너십, 학생 1인당 높은 기술 투자에 힘입어 2025년 디지털 교실 시장에서 62.21%의 점유율을 차지했습니다. 각 학군은 ESSER(교육지원 및 보안 긴급구호법) 만료에 대응하기 위해 필수 플랫폼과 벤더의 통합에 집중했습니다. 이로 인해 환승 비용이 증가하여 컴플라이언스 및 ID 통합에 강점을 가진 제공업체가 수혜를 입었습니다. 연방정부의 고등교육 기술에 대한 지원은 계속되고 있으며, 2026년 FIPSE 보조금은 주요 분야의 교육 및 학습 개선을 위한 AI 이니셔티브에 5,000만 달러가 배정될 예정입니다. Canvas와 PowerSchool은 교육 및 학생 업무의 중심적인 역할을 계속하고 있으며, 다년 계약을 통해 시장의 안정성을 보장하고 있습니다. FERPA와 같은 규제 준수는 벤더 선정과 데이터 관리에 영향을 미치며, 감사에 대응할 수 있는 문서와 강력한 프라이버시 관리 기능에 대한 수요를 촉진하고 있습니다.

아시아태평양에서는 각국의 디지털 교육 계획이 디바이스, 플랫폼, 기술 도입을 가속화하면서 2026년부터 2031년까지 연평균 17.52%의 성장률을 나타낼 것으로 예측됩니다. 인도는 광범위한 학교 시스템 전반에 걸쳐 디지털 인프라와 역량 강화에 중점을 두고 있으며, 이는 국가 정책 및 예산 우선순위와도 일치합니다. 이 지역 시장 성장은 중앙 집중식 조달과 모바일 우선 학습 행동 증가에 의해 뒷받침되고 있습니다. 중국에서는 교실의 디지털화와 교육 기술 분야의 조정된 조달로 인해 국내 공급업체들의 점유율과 공급망이 형성되고 있습니다. 이러한 노력은 디바이스, 콘텐츠, 분석에서 규모의 경제를 강화하고, AI를 활용한 학습 목표와 일치합니다.

유럽에서는 현대화와 엄격한 프라이버시 및 보안 대책이 결합된 하이브리드 아키텍처와 유럽연합(EU)이 호스팅하는 서비스에 중점을 두고 있습니다. 유럽연합의 디지털 교육 계획은 2030년 기술 목표를 설정하고, 교사 교육 및 학교 역량 강화를 추진하고 있습니다. 국경을 초월한 네트워크는 확장성이 높은 도구와 사례의 공유를 촉진하고 있습니다. 유럽의 'European School Net' 이니셔티브는 학교가 분석 기능과 적응형 학습을 도입하는 가운데, 하이브리드형 교사 교육이 어떻게 수업 실천을 향상시킬 수 있는지를 보여주고 있습니다. 원격지에서는 위성 통신과 엣지 서비스가 광섬유 네트워크의 확장을 보완하여 안정적인 액세스를 보장하고 라스트 마일의 문제를 완화하고 있습니다. 이러한 요인들은 교육적 요구와 규제 요건에 부합하는 플랫폼과 서비스의 꾸준한 조달을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The digital classroom market size is expected to grow from USD 158.1 billion in 2025 to USD 177.71 billion in 2026 and is forecast to reach USD 318.82 billion by 2031 at a 12.40% CAGR over 2026-2031.

North America accounted for a 62.21% market share in 2025, while Asia-Pacific is expected to grow at a 17.52% CAGR from 2026 to 2031. Growth is driven by government investments and increased cloud adoption among large learner populations. Institutions are adopting cloud-native platforms, compliance-ready governance, and durable devices, shifting to platform-centric models. Regulatory frameworks like FERPA and GDPR influence procurement, emphasizing auditability, identity management, and data minimization. Consolidation is evident with Instructure's USD 4.8 billion acquisition in 2024, aimed at enhancing product innovation and scaling global operations in the digital classroom market.

Global Digital Classroom Market Trends and Insights

Broadband expansion and affordable devices are widening access to the Digital Classroom Market

The digital classroom market is growing due to affordable, cloud-optimized devices and improved connectivity across regions and income levels. Districts now prefer rolling refresh schedules over bulk purchases to ensure predictable budgeting and avoid disruptions caused by simultaneous device end-of-life events. Google's extended ChromeOS support helps reduce total ownership costs while maintaining security and manageability. Low Earth orbit satellites are expanding coverage to remote schools, offering bandwidth and latency suitable for real-time instruction and cloud collaboration. Interactive displays with AI features enable live collaboration, transcription, and content search, enhancing the functionality of connected classrooms. Improved connectivity and device reliability support hybrid usage models, ensuring continuity even during infrastructure limitations or maintenance. These advancements are transforming classrooms into dynamic, collaborative environments that meet modern educational needs.

Government investment in digital learning is accelerating adoption across education systems

Government programs are accelerating the shift to digital platforms and content, supporting investments and teacher training in the digital classroom market. The United States Department of Education allocated USD 169 million in FIPSE awards in January 2026, with USD 50 million directed toward AI initiatives to improve instruction and outcomes. FY25 grant withholdings in key K-12 programs redirected focus to essential platforms and compliance services, while higher education investments prioritized AI. The European Union's Digital Education Action Plan (2027) targets digital skills, educator training, and infrastructure, aiming for 80% of citizens to achieve basic digital skills by 2030. India's policies, backed by budget allocations, expand access to devices, content, and training aligned with new competency goals. UNESCO's initiatives promote global knowledge-sharing, reducing duplication, and supporting scalable policy and platform models.

Funding challenges from the post-ESSER budget cliff in the United States K-12 are limiting sustained investment in digital learning

The expiration of ESSER funding tightened discretionary budgets for districts, increasing scrutiny on renewing supplemental tools in the digital classroom market. Federal withholdings from Title I-C, Title II-A, and Title IV-B grants in FY25 totaled nearly USD 7 billion, driving a shift toward essential platforms, multi-year contracts, and stricter procurement criteria. Illinois districts reported nearly full utilization of relief funds, while Chicago Public Schools faced a 2026 budget deficit, leading to staffing cuts and operational changes. Core systems like LMS, SIS, and identity services, critical for compliance and daily operations, remain more resilient than discretionary contracts. Aging pandemic-era devices add pressure on hardware replacement cycles, prompting rolling refreshes and stricter lifecycle management. Vendors offering measurable efficiency gains, compliance documentation, and stable integration roadmaps are better positioned to retain accounts.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-native LMS ecosystems are scaling rapidly, enhancing integration and flexibility

- AI-driven personalized learning analytics are improving engagement and learning outcomes

- The digital-skills gap among teachers is slowing the effective integration of classroom technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 42.31% of the digital classroom market share in 2025, driven by the adoption of cloud learning platforms, collaboration tools, and analytics for managing instruction and student operations. The industry has shifted to integrated solutions combining LMS, SIS, and ERP systems, reducing administrative tasks and improving analytics. Canvas, serving 200 million learners globally, transitioned to private ownership in 2024 to accelerate product development and expand its global reach. PowerSchool supports over 50 million students, showcasing the benefits of a unified platform for attendance, assessment, and intervention planning. These trends emphasize procurement strategies that reduce vendor diversity, prioritize privacy, and establish a foundation for analytics and AI in digital classrooms.

VR and AR headsets are the fastest-growing hardware subsegment, with a projected 19.56% CAGR through 2031, driven by immersive simulations in labs, healthcare, and vocational training. Improved alignment between content, curriculum, and assessment supports this growth. Interactive displays are evolving into AI-enabled collaboration hubs with features like real-time summarization and transcript capture. Shipment trends indicate a preference for larger formats and shared digital canvases. Device strategies now focus on repairability, extended battery life, and fleet management to minimize downtime and stabilize costs in the digital classroom market.

The Digital Classroom Market is Segmented by Components (hardware, Software, Services), Deployment Mode (cloud, On-Premises), End User (K-12 Schools, Higher Education, Corporate and Professional Training, Government and Non-Profit), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts are Provided in Terms of USD Billion.

Geography Analysis

North America held a 62.21% share of the digital classroom market in 2025, supported by advanced IT infrastructure, stable platform partnerships, and high per-student technology investments. Districts addressed the ESSER expiration by focusing on essential platforms and vendor consolidation, which increased switching costs and benefited providers with strong compliance and identity integrations. Federal support for higher education technology continues, with FIPSE grants in 2026 allocating USD 50 million to AI initiatives aimed at improving teaching and learning in key disciplines. Canvas and PowerSchool remain central to instruction and student operations, with multi-year agreements ensuring market stability. Regulatory compliance, such as FERPA, influences vendor selection and data management, driving demand for audit-ready documentation and robust privacy controls.

Asia-Pacific is expected to grow at a 17.52% CAGR from 2026 to 2031, driven by national digital education plans that accelerate the adoption of devices, platforms, and skills. India emphasizes digital infrastructure and competency-building across its extensive school systems, aligning with national policy and budget priorities. The region's market growth is supported by centralized procurement and increasing mobile-first learning behaviors. In China, centralized classroom digitization and coordinated procurement in education technology are shaping domestic vendor shares and supply chains. These efforts enhance scale effects in devices, content, and analytics, aligning with AI-enabled learning objectives.

Europe combines modernization with strict privacy and security enforcement, emphasizing hybrid architecture and European Union-hosted services. The European Union's Digital Education Plan sets 2030 skill targets and promotes teacher training and school capacity building. Cross-border networks facilitate the sharing of scalable tools and practices. European School net initiatives demonstrate how hybrid professional development enhances classroom practices as schools adopt analytics and adaptive learning. In remote areas, satellite and edge services complement fiber expansions, ensuring consistent access and mitigating last-mile challenges. These factors drive steady procurement of platforms and services aligned with instructional and regulatory needs.

- Google LLC

- Microsoft Corporation

- Apple Inc.

- Instructure Inc. (Canvas)

- Blackboard Inc.

- D2L Corporation (Brightspace)

- Zoom Video Communications

- Lenovo Group Ltd.

- HP Inc.

- Dell Technologies Inc.

- Acer Inc.

- ViewSonic Corporation

- SMART Technologies ULC

- Promethean World Ltd.

- Samsung Electronics Co. Ltd.

- LG Electronics Inc.

- Panasonic Corporation

- Pearson plc

- BYJU'S

- Coursera Inc.

- Kahoot! ASA

- Edmodo LLC

- Nearpod Inc.

- ClassIn (Eeo Technology)*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Broadband expansion and affordable devices are widening access to the Digital Classroom Market

- 4.2.2 Government investment in digital learning is accelerating adoption across education systems

- 4.2.3 Cloud-native LMS ecosystems are scaling rapidly, enhancing integration and flexibility

- 4.2.4 AI-driven personalized learning analytics are improving engagement and learning outcomes

- 4.2.5 Device-as-a-Service models are simplifying procurement for K-12 institutions

- 4.2.6 Low-orbit satellite connectivity is enabling digital classrooms in remote and underserved schools

- 4.3 Market Restraints

- 4.3.1 Funding challenges from the post-ESSER budget cliff in the United States K-12 are limiting sustained investment in digital learning

- 4.3.2 The digital-skills gap among teachers is slowing the effective integration of classroom technologies

- 4.3.3 Stricter data-privacy regulations are adding compliance burdens for education platforms

- 4.3.4 Sustainability pressures tied to e-waste are complicating hardware refresh cycles in schools

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component (Value)

- 5.1.1 Hardware

- 5.1.1.1 Interactive Flat-Panel Displays

- 5.1.1.2 Laptops and Chromebooks

- 5.1.1.3 Tablets

- 5.1.1.4 VR/AR Headsets

- 5.1.1.5 Classroom Robotics

- 5.1.2 Software

- 5.1.2.1 Learning Management Systems

- 5.1.2.2 Classroom Collaboration Tools

- 5.1.2.3 Assessment and Proctoring Platforms

- 5.1.2.4 Content Authoring and Digital Curriculum

- 5.1.2.5 Classroom Management Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By End-user

- 5.3.1 K-12 Schools

- 5.3.2 Higher Education

- 5.3.3 Corporate and Professional Training

- 5.3.4 Government and Non-profit

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Google LLC

- 6.4.2 Microsoft Corporation

- 6.4.3 Apple Inc.

- 6.4.4 Instructure Inc. (Canvas)

- 6.4.5 Blackboard Inc.

- 6.4.6 D2L Corporation (Brightspace)

- 6.4.7 Zoom Video Communications

- 6.4.8 Lenovo Group Ltd.

- 6.4.9 HP Inc.

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Acer Inc.

- 6.4.12 ViewSonic Corporation

- 6.4.13 SMART Technologies ULC

- 6.4.14 Promethean World Ltd.

- 6.4.15 Samsung Electronics Co. Ltd.

- 6.4.16 LG Electronics Inc.

- 6.4.17 Panasonic Corporation

- 6.4.18 Pearson plc

- 6.4.19 BYJU'S

- 6.4.20 Coursera Inc.

- 6.4.21 Kahoot! ASA

- 6.4.22 Edmodo LLC

- 6.4.23 Nearpod Inc.

- 6.4.24 ClassIn (Eeo Technology)*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment