|

시장보고서

상품코드

2043868

플렉서블 에폭시 수지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flexible Epoxy Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

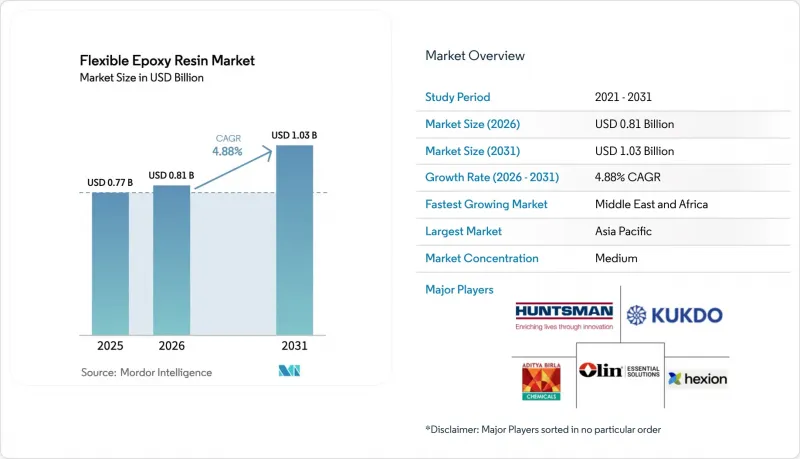

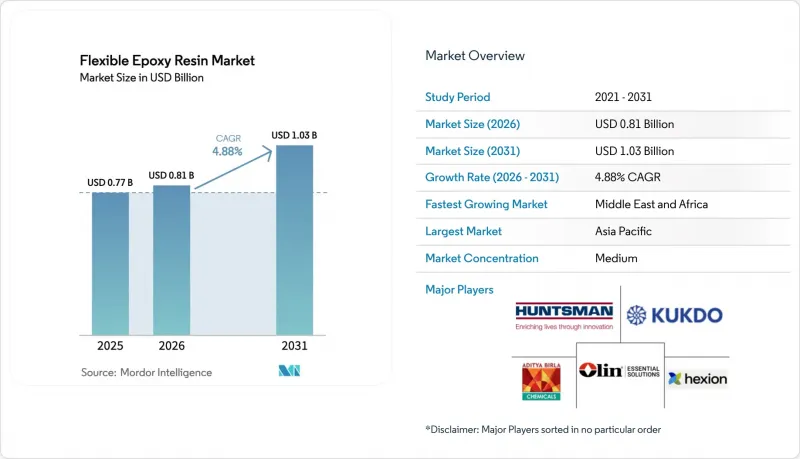

플렉서블 에폭시 수지 시장 규모는 2025년 7억 7,000만 달러로 평가되었습니다. 2026년 8억 1,000만 달러에서 2031년까지 10억 3,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.88%를 나타낼 전망입니다.

과거에는 범용 건축용 접착제가 주를 이루었으나, 현재 업계는 고부가가치 용도에 초점을 맞추었습니다. 전기자동차의 파워 일렉트로닉스, 풍력 터빈 블레이드 수리, 웨어러블 기기용 플렉서블 인쇄 회로 기판 등이 이에 해당합니다. 구조용 복합재료는 여전히 고무 개질 등급이 주류를 이루고 있지만, 특히 전자제품의 밀봉 응용 분야에서 우레탄 개질 화학물질의 사용이 크게 증가하고 있습니다. 활기찬 전자 및 건설 부문에 힘입어 아시아태평양은 주요 수요 거점으로 자리매김하고 있습니다. 그러나 사우디아라비아의 야심찬 인프라 개발 계획과 획기적인 NEOM 프로젝트에 힘입어 중동 및 아프리카이 가장 빠른 성장세를 보이고 있습니다. 이러한 성장에도 불구하고, 에피클로로히드린의 가격 변동과 비스페놀 A 디글리시딜 에테르에 대한 규제 당국의 감시 강화로 인해 업계의 수익성은 어려운 상황에 직면해 있습니다. 이러한 변화하는 상황에서 수직계열화 기업이나 바이오 혁신기업은 원료 확보와 컴플라이언스 이슈에 대한 대응력이 뛰어나 유리한 고지를 점하고 있습니다.

세계의 플렉서블 에폭시 수지 시장 동향 및 인사이트

건설 및 인프라 지출 급증

아시아태평양, 중동 및 북미의 인프라 예산이 플렉서블 에폭시 접착제 및 코팅제에 대한 꾸준한 수요를 주도하고 있습니다. 2024년, 중국은 철로 및 지하철 연장에 많은 예산을 배정하여 진동 흡수형 에폭시 조인트의 필요성을 강조했습니다. 동시에 인도의 국가 인프라 계획은 도로 및 도시 교통에 초점을 맞추고 있으며, 2025년까지 막대한 자금이 투입되었습니다. 이러한 노력은 특히 해안가 고가도로의 철근용 부식방지 에폭시 코팅에 대한 수요를 자극했습니다. 지난 5년간 미국은 교량 보수에 많은 투자를 하고 있으며, 폐쇄 기간을 절반으로 줄일 수 있는 균열 주입용 에폭시를 선호하고 있습니다. 사우디아라비아의 '비전 2030' 개발 프로젝트(NEOM이 주도하는)는 사막의 혹독한 열에 대한 내구성을 확보하기 위해 저 VOC 플렉서블 에폭시 코팅의 중요성을 강조했습니다. 그러나 이러한 프로젝트가 견인하는 견고한 수요에도 불구하고, 자금 조달 지연과 환율 변동으로 인해 접착제 조달 기간이 최대 1년까지 연장될 수 있다는 점을 인지해야 합니다.

소비자 가전 및 전기자동차용 파워 일렉트로닉스의 전기화

현재 모든 배터리 전기자동차(BEV)에는 수천 개의 적층 세라믹 커패시터가 장착되어 있으며, 이들은 플렉서블 에폭시 단자의 이점을 누리고 있습니다. 이 숫자는 기존 내연기관 모델에서 볼 수 있는 숫자를 크게 상회하는 수치입니다. 이 단자는 -40℃에서 +150℃의 온도 범위에서 솔더 조인트의 내구성을 보장합니다. 배터리 전기자동차의 세계 생산량은 최근 몇 년 동안 크게 증가했으며, 이러한 추세는 앞으로도 지속될 것으로 예측됩니다. 그 결과, 포팅재와 봉지재의 사용도 함께 증가하고 있습니다. 소비자용 전자기기에서는 폴더블 스마트폰과 건강관리용 웨어러블 기기에서 우레탄 변성 에폭시 수지의 활용이 확대되고 있습니다. 높은 연신율로 유명한 이 특수 에폭시 수지는 엄격한 굽힘 시험을 통과하도록 설계되었습니다. 주목할 만한 업계 동향으로, 일본과 한국 기업들이 첨단 패키징 기술에 많은 투자를 하고 있으며, 2020년 말까지 완성되었습니다. 이러한 첨단 패키지의 핵심 구성 요소는 저탄성률 에폭시안더필(epoxy underfill)입니다. 이러한 전자제품 분야의 동향은 2026년부터 2031년까지 예측 기간 동안 이 부문의 CAGR을 6.31%까지 끌어올릴 것으로 예측됩니다.

에피클로로히드린 및 비스페놀 A의 원료 가격의 변동성

최근 몇 년 동안 중국 생산업체들이 생산능력을 대폭 확대한 결과, 에피클로로히드린과 비스페놀A의 현물가격이 크게 변동하고 있습니다. 이 두 가지 화학물질은 생산 비용의 대부분을 차지합니다. 그 결과, 연간 계약에 묶여 있는 유럽과 미국의 배합업체들은 가격 불안정성으로 어려움을 겪었습니다. 프로파일렌 원료 가격의 급등으로 유럽 에피클로로히드린 가격이 급등하여 매출 총이익률이 하락했습니다. 헤지 전략이나 후방 통합이 없는 중소형 컨버터는 접착제 공급 계약 가격을 조정하지 못하면 분기별로 손실 위험에 직면하게 됩니다.

부문 분석

2025년에는 2단계 구조를 활용한 고무 개질 등급이 매출의 41.38%를 차지하여 파괴 인성을 향상시켰습니다. 이러한 개선은 풍력 발전용 블레이드 및 산업용 접착제에 적용될 때 매우 중요한 것으로 입증되었습니다. 고무 개질 플렉서블 에폭시 수지 시장은 건설 및 복합재료 부문 수요에 힘입어 2026년부터 2031년까지 예측 기간 동안 전체 시장의 CAGR과 보조를 맞출 것으로 예측됩니다. 우레탄 개질 화학제품은 전자기기 밀봉에 대한 역할에 힘입어 6.24%의 연평균 복합 성장률(CAGR)(2026-2031년)로 확대될 것으로 예측됩니다. 여기서 높은 연신율과 영하의 유리 전이 온도와 같은 특성은 솔더 조인트의 보호에 필수적입니다. 이러한 추세를 반영하여 2024년 제품 출시에서는 탄성률이 현저히 낮아져 저응력 다이애착에 적합한 재료로의 전환이 강조되었습니다. 반면, 점유율은 작지만, 디머산계 제품은 특수 선박용 도료에 초점을 맞추고 있으며, 발수성과 바이오 함량을 중시하고 있습니다.

시장 세분화는 비용 대비 성능의 미묘한 상호 작용에 의해 이루어집니다. 구조용 접착제 사용자는 고무 개질 등급을 선호하는 경향이 있습니다. 반면, 칩 제조업체는 현장 고장으로 인한 보증 책임의 가능성을 강하게 인식하고 있으며, 가격이 비싸더라도 우레탄을 선택합니다. 플렉서블 에폭시 수지 시장의 주요 업체들은 이러한 상황을 슬기롭게 극복하고, 자동차 전장 분야에서는 우레탄 사용을 촉진하는 한편, 건설 분야에서는 고무계 제품의 점유율을 유지하고 있습니다. 캐슈넛 유래의 디머산 수지는 해상풍력 발전의 기초 구조에서 일정한 위치를 차지하고 있습니다. 그러나 이 틈새 시장은 성장이 둔화될 것으로 예상되며, 탄소가격제로 인한 재료의 조기 대체에 따른 수요 증가가 기대되고 있습니다.

지역별 분석

2025년 아시아태평양은 매출의 47.36%로 압도적인 점유율을 차지했지만, 이후 성장세가 둔화되고 있습니다. 이러한 둔화는 중국 건설 경기의 냉각과 전자제품 생산의 성숙에 기인합니다. KUKDO, Nan Ya 등 국내 기업들은 경쟁사보다 낮은 착륙 비용으로 PCB 어셈블러에 공급하고 있으며, 이는 이 지역의 우위를 강화하고 있습니다. 그러나 인도의 인프라 프로젝트는 몬순의 영향과 자금 조달의 어려움으로 인해 때때로 정체되어 단기적인 전망을 둔화시키고 있습니다. 한편, 일본과 한국의 반도체 투자가 연간 수지 수요를 견인하고 있으며, 스마트폰 조립의 정체 추세를 상쇄하고 있습니다. 아세안 국가들은 진전을 보이고 있지만, 물류와 정책의 불일치로 인해 생산능력 확대가 둔화되고 있습니다.

2025년 주요 소비 지역인 북미는 2026년부터 2031년까지 예측 기간 동안 꾸준한 성장세를 보일 것으로 예측됩니다. 연방정부의 교량 유지보수 프로그램에서는 다운타임을 크게 줄일 수 있는 균열 주입용 에폭시 수지를 점점 더 많이 채택하고 있습니다. 오린의 에피클로로히드린의 전략적 국내 생산 확대는 중국으로부터의 수입 의존도를 낮추기 위한 것입니다. 2025년, 배터리 전기자동차의 생산이 증가함에 따라 봉지재에 대한 수요도 증가하였습니다. 이 수요는 기존 건설 부문에 비해 여전히 작지만, 캐나다의 철도 전기화 및 멕시코의 근해 전자제품 생산 라인과 같은 이니셔티브는 눈에 띄는 성장 기회를 제공합니다.

유럽은 2025년 매출에서 큰 비중을 차지했지만, 에너지 비용 상승과 REACH 규제 강화라는 문제에 직면해 있습니다. 그러나 이 대륙은 지속 가능한 화학 기술을 선도하고 있습니다. 유럽은 재활용 가능한 풍력 발전용 블레이드를 장려하고, 탄소 국경 조정 메커니즘을 통해 바이오 배합 재료에 대한 인센티브를 제공합니다. 2025년 이후 독일과 영국은 재활용 가능한 복합재료 사용을 의무화하여 스완콜의 'EzCiclo'의 채택을 가속화하고 있습니다. 한편, 프랑스와 이탈리아는 저 VOC(휘발성유기화합물) 실내용 페인트를 사용한 철도 개보수를 우선적으로 추진하고 있습니다. 러시아에서의 활동은 여전히 저조하지만, 독일과 영국은 이러한 추세의 최전선에 서 있습니다.

중동 및 아프리카는 2026년부터 2031년까지 예측 기간 동안 CAGR 5.94%를 나타내며 가장 빠른 성장세를 보이고 있습니다. 사우디 아람코의 자흐라 파이프라인, NEOM 스마트시티 등의 프로젝트에서 열충격과 모래에 의한 마모에 대한 내성을 인정받아 플렉서블 에폭시 수지가 채택되었습니다. GCC(걸프협력회의) 국가들의 해수담수화 플랜트나 두바이의 고층 빌딩 외벽에는 에너지 효율이 높은 경화 공정으로 평가받는 수성 에폭시 수지가 활용되고 있습니다. 남아프리카공화국에서는 해안 철도 개보수 공사에 콜타르 프리 페인트를 채택하고 있지만, 재정적 제약으로 인해 조달이 지연되고 있습니다. 남미는 브라질의 지하철 프로젝트와 아르헨티나의 셰일 개발에 힘입어 꾸준한 성장세를 보이고 있습니다. 그러나 관세 변동과 환율 변동 등의 문제로 인해 원자재 비용이 상승하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe Flexible Epoxy Resin Market size is projected to expand from USD 0.77 billion in 2025 and USD 0.81 billion in 2026 to USD 1.03 billion by 2031, registering a CAGR of 4.88% between 2026 to 2031.

Once centered on commodity construction adhesives, the industry is now pivoting towards high-value applications. These encompass electric-vehicle power electronics, wind-turbine blade repairs, and flexible printed circuits designed for wearables. While rubber-modified grades continue to dominate structural composites, there is a marked rise in the use of urethane-modified chemistries, particularly for electronics encapsulation. The Asia-Pacific region, strengthened by its vibrant electronics and construction sectors, stands as the primary demand hub. Yet, the Middle-East and Africa are experiencing the swiftest growth, spurred by Saudi Arabia's ambitious infrastructure initiatives and the groundbreaking NEOM project. Despite this growth, industry profitability is challenged by the volatile pricing of epichlorohydrin and intensified regulatory scrutiny on bisphenol-A diglycidyl ether. In this evolving landscape, vertically integrated firms and bio-based innovators find themselves at an advantage, adeptly securing feedstock and navigating compliance hurdles.

Global Flexible Epoxy Resin Market Trends and Insights

Surging Construction and Infrastructure Spending

Infrastructure budgets across Asia-Pacific, the Middle-East, and North America are driving a steady demand for flexible epoxy adhesives and coatings. In 2024, China made a significant budget allocation for rail lines and metro extensions, highlighting the need for vibration-damping epoxy joints. Concurrently, India's National Infrastructure Pipeline set its sights on roads and urban transit, with substantial funding slated for 2025. This initiative spurred demand for anti-corrosion epoxy coatings, particularly for rebar in coastal flyovers. Over the past five years, the United States has channeled significant investments into bridge rehabilitation, favoring crack-injection epoxies that halve closure times. Saudi Arabia's Vision 2030 development project, with NEOM at its forefront, underscored the importance of low-VOC flexible epoxy coatings, ensuring durability against the desert's harsh heat. Yet, despite the robust demand driven by these projects, it is essential to recognize that financing delays and currency fluctuations could extend adhesive procurement timelines by up to a year.

Electrification of Consumer Electronics and Electric-Vehicle Power Electronics

Thousands of multilayer ceramic capacitors in every battery electric vehicle (BEV) now benefit from flexible epoxy terminations. This number notably surpasses that found in traditional combustion engine models. These terminations ensure solder-joint durability across a temperature range of -40 to +150 degrees Celsius. The global production of battery electric vehicles has increased significantly in recent years, with forecasts indicating this trend will continue. As a result, there has been a corresponding rise in the use of potting and encapsulants. In consumer electronics, foldable phones and health wearables are increasingly utilizing urethane-modified epoxies. These specialized epoxies, known for their high elongation, are designed to pass rigorous bend tests. In a noteworthy industry development, firms from Japan and South Korea are channeling substantial investments into advanced packaging, targeting completion by the end of the decade. A pivotal component for these cutting-edge packages is the low-modulus epoxy underfills. These trends in electronics are driving the segment's projected 6.31% CAGR during the forecast period of 2026-2031.

Volatile Prices of Epichlorohydrin and Bis-A Raw Materials

In recent years, Chinese producers expanded their capacity significantly, leading to notable fluctuations in spot prices for epichlorohydrin and bisphenol-A. These two chemicals constitute a major portion of production costs. As a result, Western formulators, tied to annual contracts, grappled with pricing instability. A spike in propylene feedstocks drove European epichlorohydrin prices up sharply, reducing gross margins. Smaller converters, lacking hedging strategies or backward integration, faced the risk of quarterly losses if they could not adjust prices in their adhesive supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Wind-Energy Blade Production and Repair

- Rising Demand for Corrosion-Resistant Industrial Coatings

- Occupational Toxicity and REACH/EPA Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, rubber-modified grades, leveraging two-phase morphologies, accounted for 41.38% of the revenue, enhancing fracture toughness. This enhancement proved vital for applications in wind blades and industrial adhesives. The market for rubber-modified flexible epoxy resins is projected to grow in tandem with the overall CAGR during the forecast period of 2026-2031, driven by demand from the construction and composite sectors. Urethane-modified chemistries are expected to expand at a 6.24% CAGR (2026-2031), fueled by their role in electronics encapsulation. Here, attributes such as high elongation and a glass-transition temperature below freezing are essential for safeguarding solder joints. Echoing this trend, a 2024 product launch marked a notable reduction in modulus, highlighting a pivot toward materials adept for lower-stress die attachment. On a different note, dimer-acid products, with a small share, focus on specialized marine coatings, emphasizing hydrophobicity and bio-content.

The market's segmentation thrives on a nuanced interplay of cost-performance dynamics. Structural adhesive users lean toward rubber-modified grades. Conversely, chipmakers opt for urethane at a premium, acutely aware of potential warranty liabilities from field failures. Dominant players in the flexible epoxy resin market skillfully navigate this terrain, championing urethane applications in automotive electronics while preserving rubber shares for the construction sector. Cashew-based dimer-acid resins have carved out a space in offshore wind foundations. However, this niche anticipates sluggish growth, eyeing a possible uplift from hastened material substitutions spurred by carbon pricing.

The Flexible Epoxy Resin Market Report is Segmented by Type (Urethane Modified, Rubber Modified, and Dimer Acid Modified), Application (Electrical and Electronics, Adhesives, Composites, Paints and Coatings, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region held a commanding 47.36% share of the revenue, but growth has since moderated. This slowdown is attributed to a cooling construction cycle in China and a maturing electronics output. Domestic players, such as KUKDO and Nan Ya, are supplying printed-circuit assemblers at landed costs lower than those of their competitors, which strengthens the region's dominance. However, India's infrastructure projects have occasionally stalled due to monsoon impacts and financing challenges, tempering short-term expectations. Meanwhile, investments in semiconductors from Japan and South Korea are driving annual resin demand, counterbalancing a plateau in smartphone assembly. The ASEAN nations are progressing, but inconsistencies in logistics and policy are slowing their capacity expansions.

North America, a significant consumer in 2025, is projected to experience steady growth during the forecast period of 2026-2031. Federal bridge programs are increasingly favoring crack-injection epoxies, which notably minimize downtime. Olin's strategic domestic expansion of epichlorohydrin aims to reduce reliance on Chinese imports. In 2025, as battery electric vehicle production increased, so did the demand for encapsulants. While this demand remains modest compared to the more established construction sector, initiatives such as Canada's rail electrification and Mexico's nearshored electronics lines are providing notable growth opportunities.

Europe, while accounting for a significant share of 2025 sales, has faced challenges such as high energy costs and stringent REACH filings. However, the continent is leading sustainable chemistry initiatives. Europe is advocating for recyclable wind blades and incentivizing bio-based formulations through the Carbon Border Adjustment Mechanism. Starting in 2025, both Germany and the United Kingdom have mandated recyclable composites, accelerating the adoption of Swancor's EzCiclo. Meanwhile, France and Italy are prioritizing rail upgrades with low-VOC interior coatings. While Russia's activity remains subdued, Germany and the United Kingdom are at the forefront of these developments.

The Middle-East and Africa are experiencing the fastest growth, boasting a 5.94% CAGR during the forecast period of 2026-2031. Projects such as Saudi Aramco's Jafurah pipeline and the NEOM smart city are opting for flexible epoxies, highlighting their resistance to thermal shock and sand abrasion. GCC desalination plants and the facades of Dubai's high-rises are utilizing water-borne epoxies, which are recognized for their energy-efficient curing. In South Africa, coastal rail rehabilitation is employing coal-tar-free coatings but is facing procurement delays due to fiscal constraints. South America, driven by metro projects in Brazil and shale developments in Argentina, is on a steady growth path. However, challenges such as tariff fluctuations and currency swings are increasing feedstock costs.

- Aditya Birla Chemicals

- BASF SE

- Cardolite Corporation

- Conren Limited

- DIC Corporation

- Dow

- EPOXONIC

- Henkel AG & Co. KGaA

- Hexion

- Huntsman Corporation

- INTERTRONICS

- KUKDO Chemical (Kunshan) Co., Ltd.

- LymTal International, Inc.

- Mereco Technologies

- Nan Ya Plastic Corporation

- Olin Corporation

- Sicomin Epoxy Systems

- Solvay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging construction and infrastructure spending

- 4.2.2 Electrification of consumer electronics and Electric Vehicle power-electronics

- 4.2.3 Rapid expansion of wind-energy blade production and repair

- 4.2.4 Rising demand for corrosion-resistant industrial coatings

- 4.2.5 Adoption of flexible epoxies in wearable and IoT flexible PCBs

- 4.3 Market Restraints

- 4.3.1 Volatile prices of epichlorohydrin and bis-A raw materials

- 4.3.2 Occupational toxicity and REACH/EPA compliance costs

- 4.3.3 Scope-3 emissions scrutiny across epoxy value chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Urethane Modified

- 5.1.2 Rubber Modified

- 5.1.3 Dimer Acid Modified

- 5.2 By Application

- 5.2.1 Electrical and Electronics

- 5.2.2 Adhesives

- 5.2.3 Composites

- 5.2.4 Paints and Coatings

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 Conren Limited

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 EPOXONIC

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hexion

- 6.4.10 Huntsman Corporation

- 6.4.11 INTERTRONICS

- 6.4.12 KUKDO Chemical (Kunshan) Co., Ltd.

- 6.4.13 LymTal International, Inc.

- 6.4.14 Mereco Technologies

- 6.4.15 Nan Ya Plastic Corporation

- 6.4.16 Olin Corporation

- 6.4.17 Sicomin Epoxy Systems

- 6.4.18 Solvay

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment