|

시장보고서

상품코드

2043870

연질 엘라스토머 폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flexible Elastomeric Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

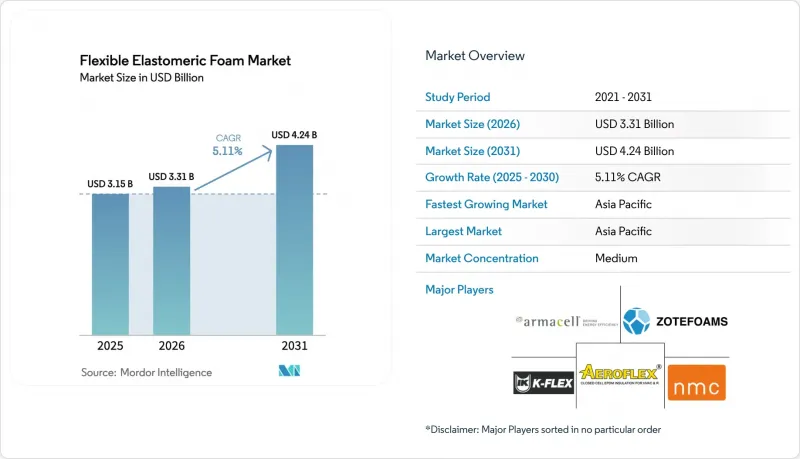

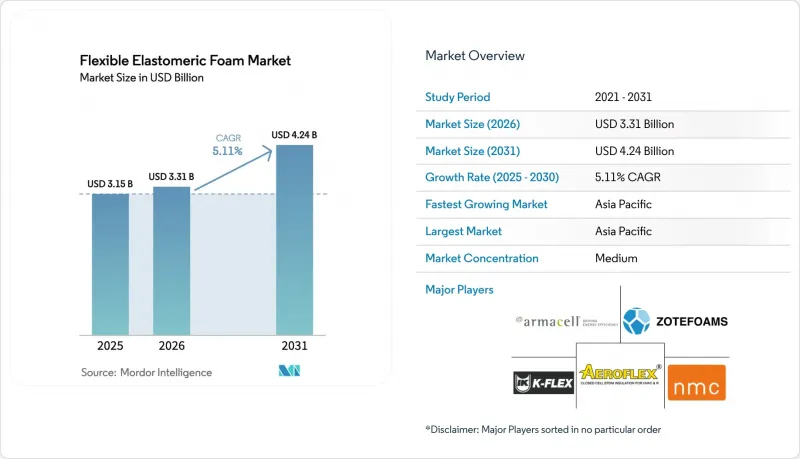

연질 엘라스토머 폼 시장 규모는 2025년에 31억 5,000만 달러로 평가되었습니다. 2026년 33억 1,000만 달러에서 2031년까지 42억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.11%를 나타낼 전망입니다.

아시아태평양에서는 건축물의 에너지 규제 강화, HVAC(난방, 환기, 공조) 및 냉동 설비의 지속적인 개보수, 콜드체인 프로젝트의 급속한 확대가 결합되어 기초 수요를 증가시키고 있습니다. 규제 당국이 고GWP(지구온난화지수) 냉매 사용을 단계적으로 감축하고 있는 가운데, 설비 교체가 예상보다 빠르게 진행되고 있습니다. R-410A에서 고압의 R-32 또는 R-454B 냉각기로 전환하려면 더 두껍고 투과성이 낮은 배관 단열재가 필요합니다. 이러한 변화로 인해 엘라스토머 단열폼 시장이 크게 확대되고 있습니다. 또한, 부타디엔과 네오프렌공급망에 대한 압박으로 인해 컨버터 업체들은 EPDM으로의 전환을 가속화하고 있습니다. 이러한 변화는 재료 구성의 다양화를 가져올 뿐만 아니라 난연성, 무할로겐, 저탄소 폼의 혁신을 촉진하고 있습니다. 에어로겔, 바이오물질 수지, 초임계 CO2 발포 기술로의 회귀를 시도하는 공급업체는 특히 고객이 제품 내재 탄소 배출량 감소에 대한 증거를 요구함에 따라 경쟁 우위를 확보할 수 있습니다.

세계의 연질 엘라스토머 폼 시장 동향 및 인사이트

HVAC 및 냉동 시스템의 리노베이션 활동 증가

누수 수리 및 단계적 폐지 의무 기한에 직면한 상업용 HVAC 설비 소유주들은 예상보다 빨리 전체 시스템 교체를 선택하고 있습니다. 업계가 R-410A에서 R-32 및 R-454B로 전환함에 따라 배출 압력이 급증하고 있습니다. 독립기포 엘라스토머 폼은 이러한 결로 위험에 대응할 수 있는 몇 안 되는 단열재 중 하나로 각광받고 있습니다. 이러한 단열재에 대한 수요는 R-290으로의 전환을 촉진하는 중국 정부의 보조금과 유럽 전역의 공공 부문 건물에서 유사한 전환에 대한 인센티브에 의해 더욱 촉진되고 있습니다. 이러한 추세를 뒷받침하는 Armacell의 Advanced Insulation 부문은 견조한 매출 성장을 보고하고 있으며, 리노베이션 중심 수요가 미치는 영향을 강조하고 있습니다. CO2 트랜스 크리티컬 랙으로 전환을 추진하고 있는 슈퍼마켓에서는 현재 -40°C의 저온에 대응하는 폼을 조달하고 있으며, NBR/PVC에서 EPDM과 클로로프렌까지 제품 선택이 확대되고 있습니다.

F-가스 단계적 감축 준수 기한 시행

유럽연합(EU)은 2030년까지 HFC 할당량을 감축할 방침이며, 2027년과 2029년에 중요한 고비가 있습니다. 이러한 움직임으로 인해 냉각기 교체 주기가 빨라지고 있습니다. 건물주들은 여전히 새로운 단열재를 필요로 하는 드롭인 방식의 개보수를할 것인지, 아니면 더 두꺼운 단열재를 필요로 하는 자연냉매 시스템으로 전환할 것인지 선택해야 합니다. 두 가지 옵션 모두 단기적으로 조달 수요가 급증하고 있습니다. 마찬가지로, 일본의 키가리 협정 조기 이행 일정과 한국의 냉매 회수 의무화도 이러한 추세를 반영하여 적어도 2027년까지 수요를 앞당기고 있습니다. EU 전역의 유통업체들은 연질 엘라스토머 폼 시장의 제품에 대해 6개월까지 주문이 꽉 차 있다고 보고하고 있으며, 2026년에는 공급이 타이트해질 가능성이 높다는 것을 시사하고 있습니다.

부타디엔 및 네오프렌의 원료 가격 변동

2025년 초까지 아시아태평양의 스팀 크래커 가동 중단과 나프타 가격 상승으로 인해 부타디엔 현물 가격이 크게 상승하여 NBR의 비용 곡선에 직접적인 영향을 미쳤습니다. 동시에 듀폰의 라플레이스 공장의 가동 중단으로 세계 네오프렌 공급이 타이트해져 북미의 네오프렌 가격이 급등했습니다. 마진이 줄어들면서 많은 컨버터들이 에틸렌과 프로파일렌 공급이 더 안정적인 EPDM으로 전환했습니다. 이 전환은 가격 상승을 피하는 데 도움이 되지만, 최종 사용자와의 적합성 테스트가 필요하며, 출하 주기가 일시적으로 지연될 수 있습니다.

부문 분석

2025년 단열 응용 분야는 수요의 75.22%를 차지했으며, 2026년부터 2031년까지 예측 기간 동안 연평균 5.29%의 성장률을 나타낼 것으로 예측됩니다. 이러한 성장은 주로 500 Hz에서 2 kHz 범위의 진동 감쇠가 필요한 전기자동차 배터리 하우징 및 철도 차량에 대한 수요 증가에 의해 주도되고 있습니다. 연질 엘라스토머 폼 시장 점유율은 미국 및 유럽 에너지 표준에 규정된 필수 커버링 요건에 의해 뒷받침되고 있습니다. 반면, 방음 용도로의 사용은 자발적인 '에너지 및 환경 디자인 리더십(LEED)' 크레딧과 임차인의 기대에 의해 더 큰 영향을 받고 있습니다.

단열 응용 분야는 더 두꺼운 단열재를 필요로 하는 냉매 전환의 혜택을 누리고 있습니다. 반면, 음향 부문은 기업들이 유연성을 잃지 않으면서도 음향 투과 손실을 중시하는 경향이 있기 때문에 우위를 점하고 있습니다. 전기자동차 플랫폼의 확대와 데이터센터의 펌프에서 발생하는 새로운 진동 문제로 인해 음향용 폼의 성장이 예상됩니다. 그러나 2031년까지 단열 용도가 절대적인 매출에서 우위를 유지할 것으로 예측됩니다.

지역별 분석

2025년 아시아태평양은 전체 매출의 45.25%를 차지했습니다. 인도는 냉장 보관 용량을 두 배로 늘리고 중국은 광범위한 HVAC 개조 프로젝트를 진행함에 따라 2026-2031년의 예측 기간 동안 7.09%의 견고한 CAGR을 나타낼 것으로 예측됩니다. Armacell은 푸네에 새로운 에어로겔 제조 시설을 설립했으며, Huamei와 같은 현지 기업들은 현지 조달을 활용하고 업계 표준을 준수하여 사업 운영을 최적화하고 있습니다.

북미에서는 2026년 1월부터 시행된 누수 수리 규정과 더불어 캘리포니아주와 뉴욕주의 엄격한 건축 외피 기준이 시장을 주도하고 있습니다. 그 결과, 대리점들은 선구매 기회를 활용해 2026년 하반기까지 수주 잔량을 확대했습니다. 유럽 시장 성장은 F가스 단계적 감축에 의해 촉진되고 있으며, 이로 인해 냉각기와 히트펌프의 교체가 가속화되고 있습니다. 높은 인건비에 대응하기 위해 시장에서는 설치 시간을 단축하는 프리폼 파이프 섹션의 채용이 증가하고 있으며, 이러한 추세에 히라산업과 K-Flex와 같은 기업들이 대응하고 있습니다.

남미, 중동 및 아프리카는 세계 전체 매출에서 차지하는 비중은 작지만, 두 자릿수 성장세를 보이고 있습니다. 이러한 급격한 성장은 주로 섭씨 45도 이상의 폭염에 시달리는 지역의 의약품 물류 및 식료품 배송 수요에 힘입은 바 큽니다. 또한, 일본과 한국의 정책적 움직임은 냉매 회수를 추진하고 2027년까지 신규 R-410A의 수입을 금지하는 것을 목표로 하고 있어, 시장 구조가 크게 변화할 것으로 예측됩니다. 이러한 노력으로 동북아시아는 유럽의 부상과 마찬가지로 빠른 성장 궤도에 올라섰으며, 건설 부문이 둔화되더라도 동북아시아의 활기를 유지할 수 있을 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Flexible Elastomeric Foam Market size was valued at USD 3.15 billion in 2025 and is estimated to grow from USD 3.31 billion in 2026 to reach USD 4.24 billion by 2031, at a CAGR of 5.11% during the forecast period (2026-2031).

In the Asia-Pacific region, a surge in building-energy regulations, ongoing retrofits in HVAC and refrigeration, and a swift expansion of cold-chain projects are collectively driving up baseline demand. As regulators phase down high-GWP refrigerants, equipment replacements are occurring sooner than anticipated. Each transition from R-410A to the higher-pressure R-32 or R-454B chillers requires thicker, lower-permeability pipe insulation. This shift is significantly expanding the market for flexible elastomeric foam. Additionally, with supply-chain pressures on butadiene and neoprene, converters are increasingly turning to EPDM. This shift not only diversifies the material mix but also drives innovation in fire-safe, halogen-free, and low-carbon foams. Suppliers that integrate back into aerogel, biomass-balance, and super-critical CO2 foaming are gaining a competitive edge, especially as customers demand evidence of embodied-carbon reduction.

Global Flexible Elastomeric Foam Market Trends and Insights

Increasing Retrofitting Activities in HVAC and Refrigeration Systems

Owners of commercial HVAC equipment, facing mandatory deadlines for leak repairs or phase-outs, are opting to replace entire systems sooner than anticipated. As the industry transitions from R-410A to R-32 and R-454B, discharge pressures have surged. Closed-cell elastomeric foam stands out as one of the few insulation materials capable of managing this increased condensation risk. The demand for this insulation is further bolstered by provincial subsidies in China promoting R-290 conversions, along with incentives for such transitions in public-sector buildings across Europe. Armacell's Advanced Insulation division, which underscores this trend, reported robust revenue growth, highlighting the impact of retrofit-driven demand. Supermarkets making the switch to CO2 transcritical racks are now procuring foam rated for temperatures as low as -40°C, broadening their product selection from NBR/PVC to also encompass EPDM and chloroprene.

Implementation of F-Gas Phase-Down Compliance Deadlines

By 2030, the European Union is set to reduce its HFC quotas, with key checkpoints in 2027 and 2029. This move is hastening chiller-replacement cycles. Building owners face a choice: retrofit with drop-ins that still necessitate new insulation or transition to natural-refrigerant systems, which require a thicker wrap. Both options are driving a surge in near-term procurement. Similarly, Japan's expedited Kigali timeline and South Korea's enforced refrigerant reclamation are echoing this trend, pulling demand forward at least until 2027. Distributors throughout the EU are noting that orders for products in the flexible elastomeric foam market are booked out for six months, signaling a likely tight supply in 2026.

Butadiene and Neoprene Feedstock Volatility

By early 2025, steam-cracker outages and rising naphtha costs significantly increased butadiene spot prices in the Asia-Pacific, directly influencing NBR cost curves. At the same time, a shutdown at DuPont's LaPlace facility tightened the global neoprene supply, leading to a surge in North American prices. As margins narrowed, many converters shifted to EPDM, benefiting from its more stable ethylene and propylene streams. While this transition helps avoid price surges, it requires qualification testing with end users, temporarily delaying shipment cycles.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Building Energy-Efficiency Regulations

- Rapid Growth of Cold-Chain Infrastructure for Last-Mile Grocery Delivery

- Fire-Safety Bans on Halogenated Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, thermal insulation accounted for 75.22% of the demand and is projected to grow at a CAGR of 5.29% during the forecast period of 2026-2031. This growth is primarily driven by the increasing demand for electric-vehicle battery housings and rail rolling stock, which require vibration dampening in the 500 Hz to 2 kHz range. The market share of flexible elastomeric foam in thermal applications is supported by a mandatory wrap requirement, as stipulated by U.S. and European energy codes. In contrast, its use in acoustic applications is influenced more by voluntary Leadership in Energy and Environmental Design (LEED) credits and tenant expectations.

Thermal applications are also benefiting from refrigerant transitions that necessitate thicker insulation. Meanwhile, the acoustic segment gains an advantage as companies emphasize sound transmission loss without compromising flexibility. With the expansion of electric vehicle platforms and emerging vibration challenges from data-center pumps, acoustic foam is poised for growth. However, thermal insulation is expected to maintain its lead in absolute revenues through 2031.

The Flexible Elastomeric Foam Market Report is Segmented by Function (Thermal Insulation, and Acoustic Insulation), Type (Natural Rubber/Latex, Nitrile Butadiene Rubber/Polyvinyl Chloride, Ethylene Propylene Diene Monomer, and More), Application (HVAC, Automotive, Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region accounted for 45.25% of total revenue. With India doubling its cold-storage capacity and China rolling out an extensive HVAC retrofit pipeline, the region is poised for a robust 7.09% CAGR during the forecast period of 2026-2031. Armacell has set up a new aerogel facility in Pune, while local players such as Huamei are optimizing their operations by leveraging localized supplies and aligning with industry codes.

In North America, leak-repair regulations that came into effect in January 2026, coupled with stringent envelope codes in California and New York, are driving the market. Consequently, distributors have bolstered their order books into late 2026, capitalizing on pre-buying opportunities. Europe's market growth is spurred by the F-Gas phase-down, which is accelerating the replacement of chillers and heat pumps. In response to high labor costs, markets are increasingly adopting pre-formed pipe sections to reduce installation time, a trend addressed by companies such as Hira Industries and K-Flex.

Although South America and the Middle-East and Africa hold a smaller share of global revenue, they are experiencing double-digit growth. This surge is largely fueled by the demands of pharmaceutical logistics and grocery deliveries in regions grappling with sweltering temperatures surpassing 45 degrees Celsius. Additionally, policy moves in Japan and South Korea are set to reshape the landscape by aiming to reclaim refrigerants and banning the import of virgin R-410A by 2027. Such initiatives position Northeast Asia on a rapid growth trajectory, mirroring Europe's ascent, ensuring the region remains buoyant even as the construction sector cools.

- Aeroflex USA, Inc.

- Armacell International S.A.

- BASF

- DuPont

- Era Polymers Pty Ltd

- Hira Industries LLC

- Huamei Energy-saving Technology Group Co., Ltd.

- Intec Foams Ltd

- Jinan Retek Industries Inc.

- Johns Manville (Berkshire Hathaway)

- Kingwell World Industries Inc.

- L'Isolante K-FLEX S.p.A.

- NMC SA

- Owens Corning

- Rogers Corporation

- Rubberlite, Inc.

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Trelleborg AB

- Zotefoams plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing retrofitting activities in HVAC and refrigeration systems

- 4.2.2 Implementation of F-Gas phase-down compliance deadlines

- 4.2.3 Tightening building energy-efficiency regulations

- 4.2.4 Rapid growth of cold-chain infrastructure for last-mile grocery delivery

- 4.2.5 Rising adoption of high-temperature foam in solar-thermal collectors

- 4.3 Market Restraints

- 4.3.1 Butadiene and neoprene feedstock volatility

- 4.3.2 Fire-safety bans on halogenated additives

- 4.3.3 PFAS-linked blowing-agent supply risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Thermal Insulation

- 5.1.2 Acoustic Insulation

- 5.2 By Type

- 5.2.1 Natural Rubber/Latex

- 5.2.2 Nitrile Butadiene Rubber/Polyvinyl Chloride

- 5.2.3 Ethylene Propylene Diene Monomer

- 5.2.4 Chloroprene

- 5.2.5 Other Types (ECO, SBR, etc.)

- 5.3 By Application

- 5.3.1 HVAC

- 5.3.2 Automotive

- 5.3.3 Transportation

- 5.3.4 Solar Installations

- 5.3.5 Refrigeration Systems

- 5.3.6 Other Applications (Medical and Healthcare Devices, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aeroflex USA, Inc.

- 6.4.2 Armacell International S.A.

- 6.4.3 BASF

- 6.4.4 DuPont

- 6.4.5 Era Polymers Pty Ltd

- 6.4.6 Hira Industries LLC

- 6.4.7 Huamei Energy-saving Technology Group Co., Ltd.

- 6.4.8 Intec Foams Ltd

- 6.4.9 Jinan Retek Industries Inc.

- 6.4.10 Johns Manville (Berkshire Hathaway)

- 6.4.11 Kingwell World Industries Inc.

- 6.4.12 L'Isolante K-FLEX S.p.A.

- 6.4.13 NMC SA

- 6.4.14 Owens Corning

- 6.4.15 Rogers Corporation

- 6.4.16 Rubberlite, Inc.

- 6.4.17 Saint-Gobain

- 6.4.18 Sekisui Chemical Co., Ltd.

- 6.4.19 Trelleborg AB

- 6.4.20 Zotefoams plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Flexible elastomeric foam adoption in hyperscale data-centres