|

시장보고서

상품코드

2043872

콘크리트 믹서 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Concrete Mixer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

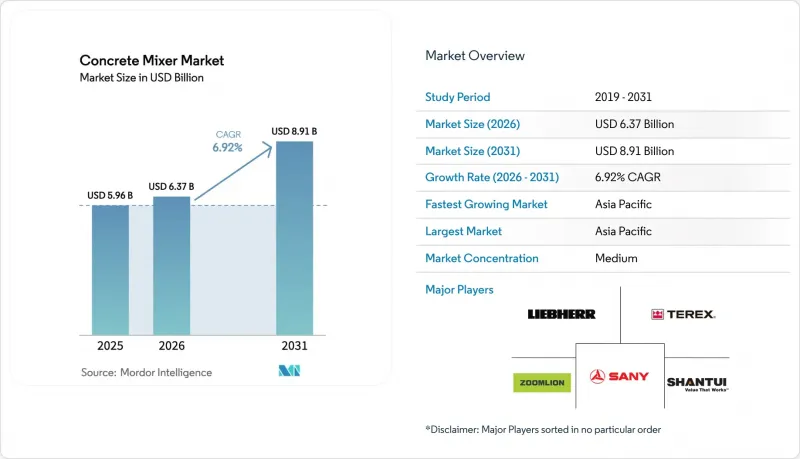

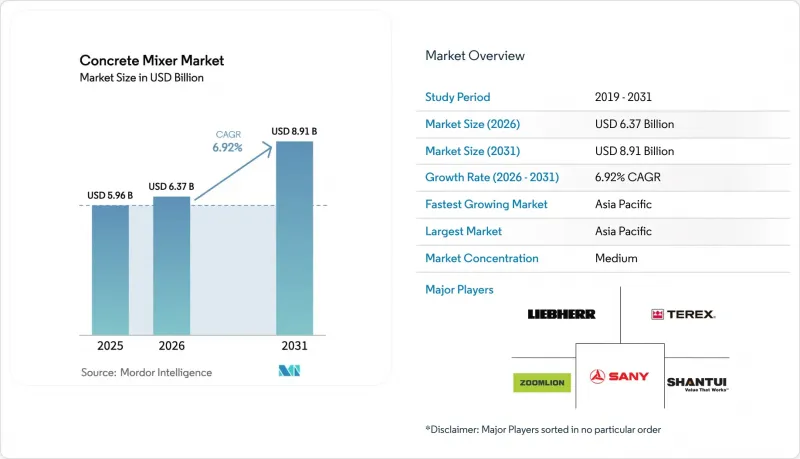

콘크리트 믹서 시장 규모는 2025년에 59억 6,000만 달러로 평가되었습니다. 2026년 63억 7,000만 달러에서 2031년까지 89억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.92%를 나타낼 전망입니다.

아시아태평양과 중동의 견조한 공공 프로젝트, 유럽과 북미의 강화된 CO2 배출 및 소음 규제, 그리고 렌탈 및 EaaS(Equipment as a Service) 계약으로의 전환이 가속화됨에 따라 조달 전략이 재편되고 있습니다. 건설사들은 메가 프로젝트를 위한 대용량 고정식 플랜트와 도심 재개발 현장을 위한 휴대용 전기 유닛으로 구매를 분산하고 있으며, 캘리포니아 주와 EU의 차량 운영사들은 감가상각 주기를 앞두고 디젤 차량 퇴출을 추진하고 있습니다. 따라서 거대한 인프라 투자와 전기화 의무화라는 두 가지 요인이 결합되어 수요는 더 크고 자동화되고 점점 더 많은 배터리 구동 모델로 향하고 있습니다. 경쟁의 격렬함은 중간 정도이지만, 텔레매틱스 기능을 무상으로 번들링하는 중국의 신생 업체들이 기존 업체들의 수익률을 압박하고 있으며, 유럽과 미국의 OEM 업체들은 가동 시간을 보장하는 구독 모델로 전환해야 하는 상황에 처해 있습니다.

세계의 콘크리트 믹서 시장 동향 및 인사이트

거대 인프라 투자 급증(2026-2031년)

2025년 세계 각국 정부는 인프라 프로젝트에 2조 3,000억 달러를 투자했으며, 아시아태평양은 발표된 파이프라인 금액의 약 58%를 차지했습니다. 인도의 국가 인프라 계획만 보더라도 2030년까지 1조 4,000억 달러의 자본 지출을 목표로 하고 있으며, 지속적인 콘크리트 공급이 필요한 고속도로, 지하철, 산업 회랑에 우선순위를 두고 있습니다. 사우디아라비아의 메가시티 'NEOM'과 이집트의 '신행정수도'에서는 외딴 사막의 건설 현장에서 트럭의 왕복 횟수를 최소화하려는 계약자들이 중동 프로젝트에서 과거 평균보다 더 빠른 속도로 대용량 고정식 믹서를 도입하고 있습니다. 추정에 따르면, 인프라 지출 10억 달러당 프로젝트 밀도와 배치 플랜트의 근접성에 따라 약 120-150대의 콘크리트 믹서에 대한 수요가 발생한다고 합니다. 이러한 승수효과는 아시아태평양에서 가장 두드러지게 나타나고 있으며, 공급망의 분절화와 레디믹스트 콘크리트의 낮은 보급률로 인해 건설업체들은 현장 혼합 능력을 도입할 수밖에 없고, 그 결과 2028년까지 드럼 및 트윈 샤프트 모델의 수주 잔고는 두 자릿수 성장률을 유지할 것으로 예측됩니다. 유지될 것으로 예측됩니다.

원격지에서 셀프 로딩 및 용적형 믹서의 급속한 확산

오지 광산 캠프, 풍력 발전소 기초 공사, 모듈 식 주택 프로젝트에서 고정식 배치 플랜트의 설비 투자 비용을 정당화 할 수 없기 때문에 셀프 로딩 믹서 및 체적 믹서는 CAGR 16.52%로 확장되어 기존 드럼식 장치를 능가하고 있습니다. 미국 국립재생에너지연구소(NREL)의 2025년 연구에 따르면, 용적식 믹서를 사용하면 작업자가 구조 사양에 맞게 배합 설계를 실시간으로 조정할 수 있기 때문에 모듈식 건설 현장에서 콘크리트 폐기물을 줄일 수 있는 것으로 나타났습니다. 호주에서는 리오틴토(Rio Tinto)가 2025년 필바라 철광석 사업장에 47대의 셀프 로딩 유닛을 도입하여 트럭 탑재형 드럼 믹서 대비 콘크리트 이송 리드타임을 22% 단축했다고 보고했습니다. 영국 교통부는 2024년 용적식 믹서의 무게 제한을 재검토했습니다. 교통부는 차량 총중량 제한을 44톤으로 상향 조정할 것을 제안하고 있으며, 이를 통해 운전자가 더 많은 골재를 적재할 수 있게 되어 원격지 현장의 경제성을 더욱 향상시킬 수 있습니다. 또한, 이 유닛은 라틴아메리카 및 사하라 사막 이남 아프리카의 계약자들도 선호하고 있습니다. 이러한 지역에서는 도로 인프라가 대형 레미콘 트럭을 수용할 수 없기 때문에 농촌 지역의 전기화 및 관개 프로젝트에서 자립형 배치가 유일한 실용적인 선택이 되고 있습니다.

철강 및 부품 가격의 변동으로 OEM의 수익률 압박

OECD 철강위원회의 2025년 전망에 따르면 열연코일 가격은 2025년 톤당 평균 720달러로 2022년 최고치인 1,150달러에서 하락했지만 여전히 2019년보다 38% 높은 수준입니다. 콘크리트 믹서 제조업체는 보통 생산 6-9개월 전에 철강 계약을 확정하기 때문에 현물가격이 급등하면 수익률 압박을 받게 됩니다. Zoomlion은 2024년 연례 보고서에서 원자재 가격 상승으로 인해 전년 대비 총이익률이 210bp 하락했으며, 2025년 초에 정가를 4.5% 인상할 수 밖에 없었다고 밝혔습니다. "Engineering News-Record의 2025년 3분기 비용 보고서에 따르면, 반도체 부족과 중국산 부품에 대한 관세 인상을 배경으로 2024년부터 2025년까지 유압 부품, 전기 모터, 전자 제어 장치의 가격이 12%에서 18%까지 상승했습니다. 국제통화기금(IMF)의 2025년 10월 최신 금속 가격 전망에 따르면, 전기자동차 배터리 팩과 와이어 하니스에 필수적인 니켈과 구리의 가격은 2027년까지 장기 평균보다 25% 높은 수준에서 유지될 것으로 예상되며, 무공해 제품 라인에 대한 비용 압박이 지속될 것으로 예측됩니다. 헤지 능력이 제한되어 있는 중소 OEM 업체들이 가장 취약합니다. 유럽의 여러 제조업체들은 불리한 부품 계약을 확정하는 것을 피하기 위해 2025년 신차 출시를 연기하고, 철강과 유압장비를 자체 생산하는 수직계열화된 중국 경쟁업체에 시장 점유율을 내주었습니다.

부문 분석

드럼 믹서는 2025년 매출의 58.16%를 차지했으며, 이는 연속 배출과 높은 처리 능력을 중시하는 레디믹스트콘크리트(RMC) 차량에서 확고한 위치를 반영합니다. 원격지의 경제성으로 인해 주문형 일괄 처리 수요가 증가함에 따라 셀프 로딩 및 용적형 콘크리트 믹서 시장 규모는 2031년까지 연평균 16.52%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 팬형과 행성형은 유럽과 일본의 프리캐스트 및 내화물과 같은 틈새 분야에서 활용되고 있는 반면, 트윈 샤프트형은 중국과 인도의 산업화 된 건설 수요 증가로 인해 점점 더 많은 관심을 받고 있습니다. 호주와 사하라 사막 이남 아프리카의 가격에 민감한 광산 사업자들은 운반 거리를 단축하기 위해 셀프 로딩 유형을 지정하는 경우가 증가하고 있으며, 이러한 추세로 인해 이들 지역에서 드럼형 믹서의 우위는 점점 줄어들고 있습니다.

트윈 샤프트 믹서는 균질성과 빠른 사이클 타임을 중시하는 프리캐스트 공장에서 꾸준히 입지를 다지고 있습니다. 유성식은 석유화학 및 항공우주 프로젝트에서 초강력 콘크리트에 여전히 선호되고 있으며, 장기적으로 안정적인 수요가 예상됩니다. 팬식 믹서는 생산량보다 엄격한 품질관리가 우선시되는 틈새 시장을 점유하고 있습니다. 이에 따라 OEM 업체들은 프로젝트 형태가 다양해지는 가운데 시장 점유율을 유지하기 위해 대용량 고정식 플랜트와 이동성이 높은 셀프 로딩 솔루션을 모두 아우를 수 있도록 제품 라인업을 확장하고 있습니다.

5m3-10m3 용량의 믹서는 2025년 출하량의 51.08%를 차지했습니다. 이는 대형 트럭의 표준 적재량 제한 및 물류 창고, 지하철역, 중층 오피스 빌딩에 필요한 배치 크기와 일치합니다. 2m3 미만 모델은 DIY 부문과 교외 주택 붐으로 인해 이동성이 높고 저렴한 장비를 선호하면서 2031년까지 연평균 복합 성장률(CAGR) 9.82%를 나타낼 것으로 예측됩니다. 10m3 이상의 대형 모델은 댐, 활주로, 대도시 기초공사 등에 사용되며, 연속 타설 시 트럭의 왕복 횟수를 줄이기 위해 최대 드럼 용량이 요구됩니다.

2m3에서 5m3의 콘크리트 믹서 시장 점유율은 감소하는 추세입니다. 이는 건설사들이 규모의 경제를 활용하기 위해 상위 기종으로 이동하거나, 개보수 공사의 틈새 시장을 개척하기 위해 하위 기종으로 이동하고 있기 때문이며, 이로 인해 용량 선호도에 있어 바벨형 분포가 형성되고 있습니다. 개정된 ISO 18650 표준은 유럽과 미국의 정의가 통일되어 국경을 초월한 판매를 간소화하고, OEM 업체들이 중량급 간 플랫폼을 보다 적극적으로 공유할 수 있게 되었습니다.

본 "콘크리트 믹서 시장 보고서'는 제품 유형(드럼식, 팬식, 유성식, 트윈 샤프트식), 용량(2m3 미만, 2-10m3, 10m3 이상), 용도(주거용, 상업용, 기타), 모델 유형(휴대형, 고정형), 구동 방식(내연기관, 전기), 운전 모드(수동, 기타), 지역(북미, 남미, 기타)으로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

아시아태평양은 2025년 매출의 44.16%를 차지했으며, 중국의 지하철 프로젝트와 인도의 1조 4,000억 달러 규모의 '가티 샤크티(Gati Shakti)' 계획에 힘입어 2031년까지 연평균 6.18% 성장할 것으로 예측됩니다. 청두, 우한 등 중국의 2급 도시에서는 2025년까지 18개의 신규 지하철 노선이 승인되었으며, 각 노선마다월약 34만m3의 콘크리트가 필요합니다. 인도에서는 운송 시간 단축과 레미콘 공급 부족을 완화하기 위해 간선도로를 따라 셀프 로딩 믹서를 도입했습니다. 일본에서는 신규 건설 둔화로 출하량이 3.2% 감소했지만, 2027년부터 시작된 도쿄의 디젤차 규제 구역으로 인해 전기믹서의 도입이 증가했습니다. 한국에서는 교량 개보수에 예산이 투입되면서 소형 휴대용 유닛에 대한 수요가 증가했습니다.

북미와 유럽은 2025년 매출의 38%를 차지했습니다. 미국 인프라법에서 1,100억 달러의 예산 배분으로 2026년까지 믹서 이용률은 70% 이상을 유지합니다. 독일에서는 금리 상승으로 생산량이 1.8% 감소했지만, 2030년 CO2 배출량 제한에 앞서 대응하기 위해 전기 믹서기 판매는 42% 증가했습니다. 영국에서는 인력 부족과 통관상의 마찰에 직면하여 건설업체들은 휴대용 렌탈 기계로 전환할 수밖에 없었습니다. 프랑스에서는 '그랑 파리 익스프레스(Grand Paris Express)' 계획으로 인해 고정형 믹서 수주가 증가했고, 이탈리아에서는 역사적인 중심지의 내진 보강 공사로 인해 휴대용 솔루션이 선호되었습니다. 스페인 해안 지역의 주택 건설 회복은 구매가 아닌 렌탈에 대한 의존도가 높아졌습니다.

남미, 중동 및 아프리카이 전체 매출의 약 18%를 차지했습니다. 브라질의 240억 달러 규모의 인프라 구축 계획은 아마존 지역과 북동부 지역에서의 판매를 증가시켰지만, 전력망의 취약성으로 인해 상파울루 이외의 지역에서는 전기 믹서의 보급이 제한적이었습니다. 아르헨티나의 긴축 재정으로 인해 시장은 7.2% 축소되었습니다. 사우디의 NEOM과 이집트의 뉴캐피털(New Capital)은 2025년 사막 콘크리트 타설을 위해 68대의 대용량 믹서를 도입했습니다. UAE는 주택 착공 둔화에도 불구하고 2025년 엑스포 레거시 프로젝트를 활용하여 수요를 유지했습니다. 남아공에서는 계획된 정전이 발생하여 당사의 일정에 차질을 빚어 배터리 유닛 도입에 차질을 빚었습니다. 튀르키예는 지진 복구와 공항 확장으로 9.4%의 회복세를 보였으나, 환율 변동으로 인해 단가가 18% 상승했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Concrete Mixer Market size was valued at USD 5.96 billion in 2025 and is estimated to grow from USD 6.37 billion in 2026 to reach USD 8.91 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031).

Strong public-works pipelines in Asia-Pacific and the Middle East, stricter CO2 and noise regulations in Europe and North America, and the accelerating pivot to rental and equipment-as-a-service contracts are reshaping procurement strategies. Contractors are splitting purchases between high-capacity stationary plants for mega-projects and portable electric units for urban infill sites, while fleet operators in California and the EU are advancing diesel retirements ahead of depreciation cycles. Twin forces, mega-infrastructure spending and electrification mandates, are therefore nudging demand toward larger, automated, and increasingly battery-powered models. Competitive intensity is moderate, yet Chinese entrants that bundle telematics at zero cost are pressuring incumbent margins, pushing European and U.S. OEMs to pivot toward subscription models with guaranteed uptime.

Global Concrete Mixer Market Trends and Insights

Surge in Mega-Infrastructure Spending (2026-2031)

Governments worldwide committed USD 2.3 trillion to infrastructure projects in 2025, with Asia-Pacific accounting for approximately 58% of the announced pipeline value. India's National Infrastructure Pipeline alone targets USD 1.4 trillion in capital outlays through 2030, prioritizing highways, metro rail, and industrial corridors that require continuous concrete supply. Saudi Arabia's NEOM megacity and Egypt's New Administrative Capital are absorbing high-capacity stationary mixers at rates that exceed historical norms for Middle Eastern projects, as contractors seek to minimize truck cycles on remote desert sites. Estimates suggest that every USD 1 billion in infrastructure spending generates demand for approximately 120 to 150 concrete mixer units, depending on project density and the proximity of batching plants. This multiplier effect is most pronounced in Asia-Pacific, where fragmented supply chains and limited ready-mix penetration compel contractors to deploy on-site mixing capacity, thereby sustaining double-digit order books for drum and twin-shaft models through 2028.

Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites

Self-loading and volumetric mixers are expanding at 16.52% CAGR, outpacing traditional drum units, because remote mining camps, wind-farm foundations, and modular housing projects cannot justify the capital cost of fixed batching plants. A 2025 study by the National Renewable Energy Laboratory found that modular construction sites reduce concrete waste when using volumetric mixers, as operators can adjust mix designs in real time to match structural specifications. In Australia, Rio Tinto deployed 47 self-loading units across its Pilbara iron-ore operations in 2025, citing a 22% reduction in concrete delivery lead times compared to truck-mounted drum mixers. The UK Department for Transport reviewed volumetric mixer weight limits in 2024. It proposed increasing the weight limit to 44 tons gross vehicle weight, allowing operators to carry larger aggregate payloads and further enhancing the economics of remote sites. These units also appeal to contractors in Latin America and Sub-Saharan Africa, where road infrastructure is inadequate for heavy ready-mix trucks, making self-contained batching the only viable option for rural electrification and irrigation projects.

Steel and Component Price Volatility Squeezing OEM Margins

Hot-rolled coil steel prices averaged USD 720 per tonne in 2025, down from the 2022 peak of USD 1,150 but still 38% above 2019 levels, according to the OECD Steel Committee's 2025 outlook. Concrete-mixer manufacturers typically lock in steel contracts 6 to 9 months ahead of production, exposing them to margin compression when spot prices spike; Zoomlion disclosed in its 2024 annual report that raw-material inflation eroded gross margin by 210 basis points year-over-year, forcing the company to raise list prices by 4.5% in early 2025. Engineering News-Record's Q3 2025 cost report noted that hydraulic components, electric motors, and electronic control units saw price increases of 12% to 18% in 2024-2025, driven by semiconductor shortages and tariff escalations on Chinese-manufactured parts. The International Monetary Fund's October 2025 metals-price update projects that nickel and copper-critical inputs for electric-mixer battery packs and wiring harnesses-will remain 25% above long-term averages through 2027, sustaining cost pressure on zero-emission product lines. Smaller OEMs with limited hedging capacity are most vulnerable: several European manufacturers delayed new-model launches in 2025 to avoid locking in unfavorable component contracts, ceding market share to vertically integrated Chinese competitors that produce steel and hydraulics in-house.

Other drivers and restraints analyzed in the detailed report include:

- Electrification of On-Road Mixer Fleets Amid CO2 Regulations

- Job-Site Digitalization (IoT, Telematics, and Predictive Maintenance)

- Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers In Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drum mixers delivered 58.16% of 2025 revenue, reflecting entrenched positions in ready-mix fleets that value continuous discharge and high throughput. The concrete mixer market size for self-loading and volumetric units is projected to expand at a 16.52% CAGR through 2031 as remote-site economics reward on-demand batching. Pan and planetary variants serve niche precast and refractory segments in Europe and Japan, while twin-shaft designs are gaining momentum in China and India's industrialized construction drive. Price-sensitive mining operators in Australia and Sub-Saharan Africa increasingly specify self-loading models to slash haul distances, a pivot that is eroding drum dominance in those geographies.

Twin-shaft mixers are securing a foothold in precast factories that prioritize homogeneity and rapid cycle times. Planetary types remain favored for ultra-high-performance concrete in petrochemical and aerospace projects, suggesting long-cycle, stable demand. Pan mixers occupy a niche where strict quality control trumps output volume. Consequently, OEMs are broadening portfolios to straddle both high-capacity stationary plants and agile self-loading solutions, aiming to retain wallet share as project profiles splinter.

Mixers rated 5 m3 to 10 m3 accounted for 51.08% of 2025 shipments, aligning with standard heavy-truck payload limits and the batch sizes required for logistics warehouses, metro stations, and mid-rise offices. Sub-2 m3 units are growing at a 9.82% CAGR through 2031 as the do-it-yourself segment and suburban housing boom favor maneuverable, lower-cost gear. Above-10 m3 giants serve dams, runways, and megacity foundations where continuous pours demand maximum drum capacity to cut truck cycles.

The concrete mixer market share for the 2 m3 to 5 m3 band is eroding as contractors either trade up to exploit economies of scale or trade down to tap renovation niches, creating a barbell distribution in capacity preferences. Revised ISO 18650 metrics now align European and U.S. definitions, simplifying cross-border sales and enabling OEMs to platform-share more aggressively across weight classes.

The Concrete Mixer Market Report is Segmented by Product Type (Drum, Pan, Planetary, and Twin-Shaft), Capacity (Below 2 M3, 2-10 M3, and Above 10 M3), Application (Residential, Commercial, and Others), Model Type (Portable and Stationary), Drive Type (ICE and Electric), Operating Mode (Manual and More), and Geography (North America, South America, and More). Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific contributed 44.16% of 2025 revenue and is set for a 6.18% CAGR to 2031, driven by China's metro tie-ups and India's USD 1.4 trillion Gati Shakti program. Chinese tier-2 cities such as Chengdu and Wuhan approved 18 new metro lines in 2025, each requiring roughly 340,000 m3 of concrete per month. India added self-loading mixers along highway corridors to curb haul times and mitigate ready-mix undersupply. Japan's shipments dipped 3.2% as new builds slowed, yet electric uptake rose due to Tokyo's diesel exclusion zone, which began in 2027. South Korea shifted its budget to bridge rehab, elevating demand for compact portable units.

North America and Europe jointly delivered 38% of 2025 sales. The U.S. Infrastructure Act's USD 110 billion allocation sustains mixer utilization above 70% through 2026. Germany's output slipped 1.8% under higher interest rates, but electric mixer sales grew 42% as fleets pre-complied with 2030 CO2 caps. The UK faced labor shortages and customs friction, nudging contractors toward portable rentals. France's Grand Paris Express buoyed stationary mixer orders, while Italy's seismic retrofits favored portable solutions for historic cores. Spain's coastal housing revival relied heavily on rental fleets rather than outright purchases.

South America, the Middle East, and Africa together held roughly 18% of revenue. Brazil's USD 24 billion infrastructure push buttressed sales in the Amazon and Northeast, yet grid weaknesses limited electric penetration outside Sao Paulo. Argentina's austerity led to a 7.2% contraction in the market. Saudi Arabia's NEOM and Egypt's New Capital absorbed 68 high-capacity mixers in 2025 for desert pours. The UAE leveraged Expo 2025 legacy projects to sustain demand despite softer residential starts. South Africa's load-shedding episodes disrupted our schedules, hurting the adoption of battery units. Turkey rebounded 9.4% on earthquake reconstruction and airport expansion, though currency volatility raised unit costs by 18%.

- Liebherr Group

- SANY Group

- Zoomlion Heavy Industry Science & Technology Co. Ltd

- Schwing Stetter Group

- Shantui Construction Machinery Co. Ltd.

- AB Volvo

- KYB Corporation

- Caterpillar Inc.

- XCMG

- Terex Corp.

- CIFA S.p.A.

- Putzmeister

- Sinotruk Hong Kong

- Tata Motors

- Aimix Group

- Altrad Belle

- Multiquip Inc.

- BHS-Sonthofen

- Speedcrafts Ltd.

- Crown Construction Equip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Mega-Infrastructure Spending (2026-2031)

- 4.2.2 Rapid Adoption of Self-Loading and Volumetric Mixers on Remote Sites

- 4.2.3 Electrification of On-Road Mixer Fleets Amid CO2 Regulations

- 4.2.4 Job-Site Digitalization (IoT, Telematics and Predictive Maintenance)

- 4.2.5 Growth of Rental and "Equipment-As-a-Service" Business Models

- 4.2.6 Integration of Advanced Safety and Automation Technologies

- 4.3 Market Restraints

- 4.3.1 Steel and Component Price Volatility Squeezing OEM Margins

- 4.3.2 Grid-Power Scarcity Limiting Uptake of Full-Electric Mixers in Emerging Markets

- 4.3.3 Tightening Global Noise-Emission Limits For Diesel Drum Trucks

- 4.3.4 High Initial Investment And Maintenance Costs Restricting Market Growth

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power - Suppliers

- 4.7.2 Bargaining Power - Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Drum Mixers

- 5.1.2 Pan Mixers

- 5.1.3 Planetary Mixers

- 5.1.4 Twin-Shaft Mixers

- 5.2 By Capacity

- 5.2.1 Below 2 m3

- 5.2.2 2 - 10 m3

- 5.2.3 Above 10 m3

- 5.3 By Application

- 5.3.1 Residential Construction

- 5.3.2 Commercial Construction

- 5.3.3 Infrastructure Development

- 5.3.4 Roads and Bridges

- 5.3.5 Others

- 5.4 By Model Type

- 5.4.1 Portable Mixers

- 5.4.2 Stationary Mixers

- 5.5 By Drive Type

- 5.5.1 Internal-Combustion Engine (ICE)

- 5.5.2 Electric

- 5.6 By Operating Mode

- 5.6.1 Manual

- 5.6.2 Semi-Automatic

- 5.6.3 Fully-Automatic

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Turkey

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Company Profiles

- 6.1.1 Liebherr Group

- 6.1.2 SANY Group

- 6.1.3 Zoomlion Heavy Industry Science & Technology Co. Ltd

- 6.1.4 Schwing Stetter Group

- 6.1.5 Shantui Construction Machinery Co. Ltd.

- 6.1.6 AB Volvo

- 6.1.7 KYB Corporation

- 6.1.8 Caterpillar Inc.

- 6.1.9 XCMG

- 6.1.10 Terex Corp.

- 6.1.11 CIFA S.p.A.

- 6.1.12 Putzmeister

- 6.1.13 Sinotruk Hong Kong

- 6.1.14 Tata Motors

- 6.1.15 Aimix Group

- 6.1.16 Altrad Belle

- 6.1.17 Multiquip Inc.

- 6.1.18 BHS-Sonthofen

- 6.1.19 Speedcrafts Ltd.

- 6.1.20 Crown Construction Equip.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment