|

시장보고서

상품코드

2043884

미국의 탄산칼슘 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

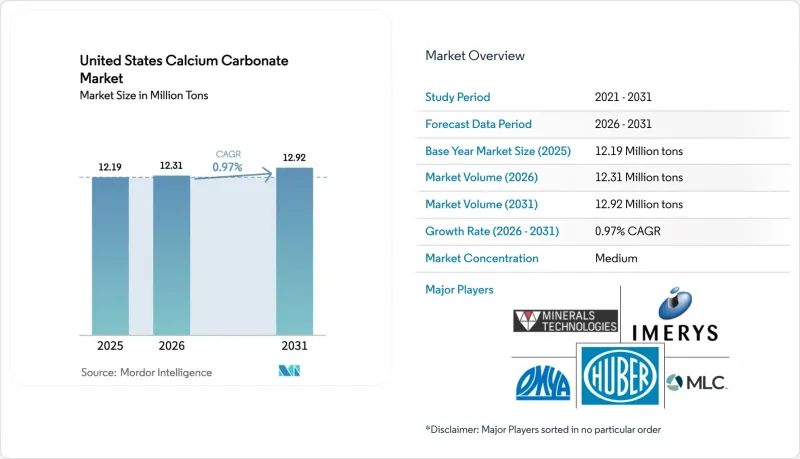

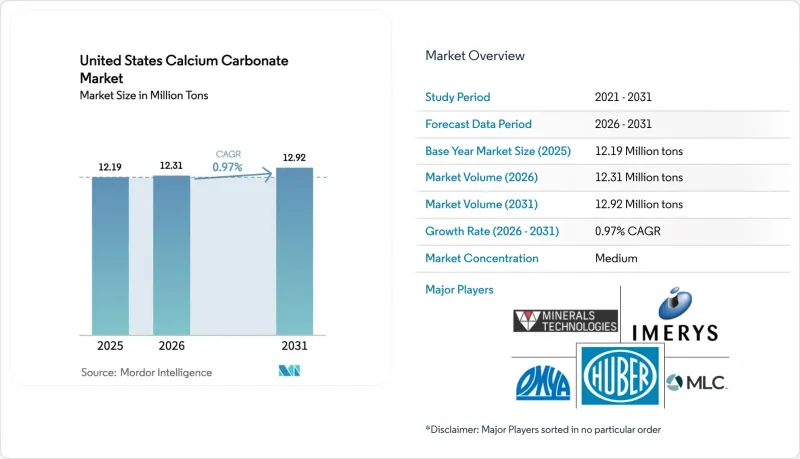

미국의 탄산칼슘 시장 규모는 2025년 1,219만 톤으로 평가되었습니다. 2026년에는 1,231만 톤으로 확대되어 2026년부터 2031년에 걸쳐 CAGR 0.97%를 나타내, 2031년까지 1,292만 톤에 이를 것으로 예측됩니다.

최근 물량 기준의 성장은 완만하지만, 가치 창출 측면에서는 탄소 포집 유래 침전 탄산칼슘(PCC)과 초미세 특수 등급으로 뚜렷한 변화를 보이고 있으며, 모두 높은 가격대에서 거래되고 있습니다. 분쇄된 탄산칼슘(GCC)은 여전히 대량 소비되는 콘크리트 및 골재 시장을 독점하고 있습니다. 그러나 제지 공장에 설치된 온사이트 PCC 생산시설과 새롭게 등장한 CCU(이산화탄소 이용) 시설이 운송에 따른 배출량을 줄이면서 수익의 원천을 확대되고 있습니다. 연방정부의 '인프라 투자 및 고용법(IIJA)'에 따른 인프라 프로젝트가 석회석 공급망을 압박하고 있으며, 가공업체들은 고성능 PCC 등급으로 전환해야 하는 상황에 처해 있습니다. 페인트 및 플라스틱 분야에서는 이산화티타늄과 폴리머의 구조적 비용 상승을 상쇄하기 위해 탄산칼슘의 배합량을 늘리고 있으며, 이는 수요 회복력을 강화하고 있습니다. 또한, 흡입성 결정질 실리카에 대한 규제 당국의 감시가 강화됨에 따라 채석장의 분진 억제에 대한 투자가 증가하고 있으며, 이는 분진 없는 합성 PCC에 경쟁 우위를 가져다주고 있습니다.

미국의 탄산칼슘 시장 동향 및 인사이트

페인트 및 코팅에 대한 수요 증가

배합 제조업체들은 고공행진하는 이산화티타늄 가격에 대응하기 위해 페인트 및 코팅제에서 탄산칼슘의 충진제 비율을 높이고 있습니다. 이러한 움직임은 페인트 및 코팅이 업계에서 가장 빠르게 성장하는 시장으로 부상함에 따라 이루어지고 있습니다. IIJA(인플레이션 억제 및 고용법)의 배분 금액의 대부분은 고속도로 신탁 기금에 사용되며, 이로 인해 교량, 고가도로, 공항 시설의 보호 코팅에 대한 수요가 증가하고 있습니다. 각 공급업체들은 고성능 건축용 도료의 까다로운 유변학 목표를 달성하기 위해 2미크론 이하의 분쇄 능력을 강화하고 스테아르산으로 표면 개질에 투자하고 있습니다. 초미세 등급 및 표면처리 등급은 분산성을 높이고 점도를 감소시켜 도막의 강도를 떨어뜨리지 않고도 필러의 배합량을 늘릴 수 있습니다. 특히, 이러한 대체 경향은 밸류티어 배합에서 두드러지게 나타나고 있으며, 필러의 배합량을 늘림으로써 원재료 비용 절감으로 이어지고 있습니다.

제지 및 포장 산업의 성장

수십년동안 PCC 위성의 통합으로 제지 산업은 여전히 가장 큰 소비 분야이며, 현장 PCC는 일반 시트 용지의 상당 부분을 차지합니다. 위스콘신 주에 위치한 돔탈의 네코사 공장은 2024년 가동을 시작한 새틀라이트에서 공급을 받고 있으며, 이 지역에서의 공동입지 전략을 통해 연간 이산화탄소 배출량 감소와 트럭 운송 거리의 대폭적인 감소에 성공하였습니다. 그래픽 용지는 감소 추세인 반면, 골판지 상자의 인쇄적합성을 높이는 탄산칼슘 코팅에 힘입어 컨테이너 보드와 EC용 포장재는 증가하고 있습니다. 전 세계에 다수의 위성 공장을 보유하고 있는 Minerals Technologies는 신흥 시장인 아시아태평양에 더 많은 자본을 투입하고 있으며, 이는 북미 시장이 성숙기에 접어들었음을 시사합니다. 그러나 국내 제지업체들은 고휘도 특수포장재 수주경쟁에서 승리하기 위해 PCC의 입자크기 조절을 강화하여 안정적인 수요를 확보하고 있습니다.

활석, 카올린 및 합성 필러와의 경쟁

우수한 내열성과 치수 안정성으로 인해 탈크는 폴리프로필렌 자동차 부품에서 선호되는 선택이 되었습니다. 한편, 카올린은 높은 백색도로 인해 종이용 코팅의 틈새 시장에서 선호되고 있습니다. 또한, 침전 실리카 및 알루미나 필러는 고광택 플라스틱 및 내스크래치성 코팅에서 그 존재감을 높이고 있습니다. 배합 설계자들은 강성과 내충격성을 높이기 위해 새로운 플라스틱 배합에 활석과 탄산칼슘을 혼합하는 경우가 증가하고 있습니다. 코팅 분야에서는 합성 실리카계 매트제가 프리미엄 나뭇결 마감에서 탄산칼슘에 도전하고 있지만, 비용적인 측면을 고려하면 그 보급은 제한적입니다. 지역별 공급망이 중요한 역할을 하고 있습니다. 탈크는 주로 몬태나와 텍사스에서 조달되는 반면, 탄산칼슘은 미국 전역에서 구할 수 있기 때문에 많은 대량 생산 응용 분야에서 운송 비용 측면에서 우위를 점하고 있습니다.

부문 분석

2025년, 분쇄 탄산칼슘(GCC)이 전체 시장의 75.69%를 차지하며 시장을 장악했습니다. 예를 들어, 미시간의 포트 칼사이트(Port Calcite)는 호수 화물선을 통해 연간 수백만 톤을 운송하고 있으며, 중서부 지역의 시멘트 및 골재 부문 고객에게 낮은 단가를 제공합니다. 한편, 침강 탄산칼슘(PCC) 시장 점유율은 작지만 생산량은 증가 추세에 있으며, 2026년부터 2031년까지 예측 기간 동안 CAGR 2.26%로 성장하고 있습니다. 이러한 성장은 제지 공장 인근의 위성 공장의 출현과 다양한 CCU 프로젝트에 의해 촉진되고 있습니다. 기반은 작지만, 미국 PCC 시장은 꾸준한 상승세를 보이고 있습니다. CarbonFree의 Gary Works 프로젝트는 CO2를 회수할 뿐만 아니라 이를 식품 등급의 고품질 PCC로 판매합니다. 이 전략은 45Q 인센티브와 일치하며, CCU의 변혁적 잠재력을 강조하고 있습니다. Fortera와 Graymont의 ReAct 파트너십은 시멘트 클링커의 일부 대체재가 될 수 있는 바테라이트 PCC를 도입하여 친환경 콘크리트에 대한 수요 증가에 대응하고 있습니다. 하지만, 공급망에는 문제가 있습니다. CO2의 회수, 정제, 액화 과정은 설비투자를 증가시키는 요인이 됩니다. 다행히도, 연방정부의 보조금과 주정부의 캡 앤 트레이드 제도를 통한 크레딧이 채굴된 GCC와의 경쟁 조건을 평준화하는 데 도움이 되고 있습니다.

미세한 입자 크기, 고순도, 형태 맞춤화로 유명한 상업적 규모의 PCC는 범용 GCC보다 높은 가격에 거래되고 있습니다. 이 때문에 식품, 의약품, 고광택 페인트 등의 분야에서 수요가 매우 증가하고 있습니다. 한편, 초미세 GCC를 생산하는 개선된 분쇄 회로는 특히 무광택 건축용 도료에서 GCC의 평균 단가를 향상시키고 있습니다. 디지털 인쇄 용지 및 저 VOC 수성 도료 분야에서는 하이브리드 필러 시스템이 등장하고 있습니다. 여기서 초미세 GCC는 부피를 제공하고 PCC는 불투명도와 백색도를 향상시킵니다. GCC는 수량적 우위를 유지할 것으로 예상되지만, PCC의 뚜렷한 장점과 CCU(탄산칼슘 이용)에 따른 혜택이 미국의 탄산칼슘 시장에서 기존 가격 대비 성능의 격차를 메울 것으로 예측됩니다.

"미국의 탄산칼슘 시장 보고서"는 유형(미분쇄 탄산칼슘 및 침전 탄산칼슘) 및 최종 이용 산업(종이, 플라스틱, 접착제 및 실란트, 페인트 및 코팅, 기타 최종 이용 산업)별로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The United States Calcium Carbonate Market size is expected to grow from 12.19 million tons in 2025 to 12.31 million tons in 2026 and is forecast to reach 12.92 million tons by 2031 at 0.97% CAGR over 2026-2031.

Recent growth in volume terms has been modest, but there is a notable shift in value creation towards carbon-capture-derived precipitated calcium carbonate (PCC) and ultrafine specialty grades, both commanding premium pricing. Ground calcium carbonate (GCC) continues to dominate high-tonnage concrete and aggregate outlets. However, on-site PCC satellites at paper mills, along with emerging CCU facilities, are expanding the profit pool while cutting down transport emissions. Infrastructure projects, bolstered by the federal Infrastructure Investment and Jobs Act (IIJA), are tightening limestone supply chains, nudging converters towards higher-performance PCC grades. In the paints and plastics sector, formulators have increased calcium carbonate loadings to offset the structurally elevated costs of titanium dioxide and polymers, thus strengthening demand resilience. Moreover, heightened regulatory scrutiny on respirable crystalline silica is driving dust-suppression investments at quarries, giving a competitive edge to dust-free synthetic PCC.

United States Calcium Carbonate Market Trends and Insights

Rising Demand for Paints and Coatings

Formulators are increasing calcium carbonate extender ratios in paints and coatings to counteract persistently high titanium dioxide prices. This move comes as paints and coatings emerge as the fastest-growing outlet in the industry. A significant portion of the IIJA's allocation is directed to the Highway Trust Fund, boosting demand for protective coatings on bridges, overpasses, and airport facilities. Suppliers are ramping up sub-2 micron grinding capacity and investing in stearic-acid surface modification to achieve stringent rheology targets in high-performance architectural paints. Ultrafine and surface-treated grades enhance dispersion and reduce viscosity, allowing for greater filler loading without compromising film integrity. Notably, this substitution trend is pronounced in value-tier formulations, where increased extender levels lead to reduced raw-material costs.

Growth in the Paper and Packaging Industry

Thanks to decades of integrating PCC satellites, paper remains the dominant consumer, with on-site PCC constituting a substantial portion of a typical sheet. Domtar's Nekoosa Mill in Wisconsin, fed by a satellite launched in 2024, has successfully reduced carbon emissions annually and avoided significant trucking miles through its co-location strategy. While graphic paper has seen a decline, containerboard and e-commerce packaging are on the rise, bolstered by calcium carbonate coatings that enhance printability on corrugated boxes. Minerals Technologies, with numerous satellites globally, is channeling more capital into emerging Asia-Pacific, hinting at a maturing North American base. Yet, domestic mills are enhancing PCC particle-size control to compete for high-brightness specialty packaging orders, ensuring steady demand.

Competition from Talc, Kaolin, and Synthetic Fillers

Thanks to its superior heat resistance and dimensional stability, talc has become the preferred choice for polypropylene automotive parts. Kaolin, with its brightness advantage, is preferred in paper-coating niches. Meanwhile, precipitated silica and alumina fillers are gaining traction in high-gloss plastics and scratch-resistant coatings. Formulators are increasingly blending talc with calcium carbonate in new plastic recipes to enhance stiffness and impact properties. In the coatings sector, while synthetic silica matting agents challenge calcium carbonate in premium wood finishes, cost considerations limit their widespread adoption. Regional supply chains play a pivotal role: talc is mainly sourced from Montana and Texas, while calcium carbonate's nationwide availability offers a freight advantage in numerous high-volume applications.

Other drivers and restraints analyzed in the detailed report include:

- Plastics Industry Adoption of CaCO3 Fillers

- United States Infrastructure Spending (IIJA) Boosting GCC Demand

- Stricter United States Quarrying and Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Ground Calcium Carbonate (GCC) dominated the market, accounting for 75.69% of the total volume. For example, Michigan's Port Calcite ships millions of tons annually via lake freighters, achieving low unit costs for clients in the Midwest cement and aggregate sectors. While Precipitated Calcium Carbonate (PCC) holds a smaller market share, its output is on the rise, growing at a 2.26% CAGR through the forecast period of 2026-2031. This growth is fueled by the emergence of satellite plants near paper mills and various CCU projects. Even though starting from a smaller base, the U.S. market for PCC is on a steady upward trajectory. CarbonFree's Gary Works project is not only capturing CO2 but also marketing it as premium food-grade PCC. This strategy aligns with 45Q incentives and highlights CCU's transformative potential. Fortera and Graymont's ReAct partnership is introducing vaterite PCC, which can serve as a partial substitute for cement clinker, addressing the increasing demand for green concrete. However, the supply chain faces hurdles: the processes of capturing, purifying, and liquefying CO2 elevate capital expenditures. Fortunately, federal grants and state cap-and-trade credits are helping to level the playing field with mined GCC.

Commercial-scale PCC, known for its finer particle size, elevated purity, and customizable morphology, commands a premium over commodity GCC. This makes it highly desirable in sectors such as food, pharmaceuticals, and high-gloss coatings. Meanwhile, upgraded grinding circuits producing ultrafine GCC are enhancing GCC's average unit value, especially in matte architectural coatings. In the realm of digital-print papers and low-VOC water-based paints, hybrid filler systems are emerging. Here, ultrafine GCC provides volume, while PCC contributes opacity or brightness. While GCC is likely to retain its volume leadership, the distinct advantages of PCC and the benefits from CCU are set to bridge the historical price-to-performance gap in the U.S. calcium carbonate market.

The United States Calcium Carbonate Market Report is Segmented by Type (Ground Calcium Carbonate and Precipitated Calcium Carbonate), and End-User Industry (Paper, Plastic, Adhesive and Sealant, Paints and Coatings, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Blue Mountain Minerals

- Carmeuse

- Cerne Calcium Company

- Chememan Public Company Limited.

- CIMBAR RESOURCES, INC.

- Columbia River Carbonates

- GLC Minerals LLC

- Graymont

- ILC Resources

- Imerys

- J.M. Huber Corporation

- Lhoist

- Minerals Technologies Inc.

- Mississippi Lime Company

- Newpark Resources Inc.

- Omya AG

- Sibelco

- The Cary Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rising demand from paints and coatings

- 4.1.2 Growth in paper and packaging industry

- 4.1.3 Plastics industry adoption of CaCO3 fillers

- 4.1.4 United States infrastructure spending (IIJA) boosting GCC demand

- 4.1.5 On-site PCC produced via carbon-capture utilization

- 4.2 Market Restraints

- 4.2.1 Health hazards from respirable CaCO3 dust

- 4.2.2 Competition from talc, kaolin and synthetic fillers

- 4.2.3 Stricter United States quarrying and emission regulations

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

- 4.5 Mine Locations

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Ground Calcium Carbonate

- 5.1.2 Precipitated Calcium Carbonate

- 5.2 By End-user Industry

- 5.2.1 Paper

- 5.2.2 Plastic

- 5.2.3 Adhesive and Sealant

- 5.2.4 Paints and Coatings

- 5.2.5 Other End-User Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Blue Mountain Minerals

- 6.4.2 Carmeuse

- 6.4.3 Cerne Calcium Company

- 6.4.4 Chememan Public Company Limited.

- 6.4.5 CIMBAR RESOURCES, INC.

- 6.4.6 Columbia River Carbonates

- 6.4.7 GLC Minerals LLC

- 6.4.8 Graymont

- 6.4.9 ILC Resources

- 6.4.10 Imerys

- 6.4.11 J.M. Huber Corporation

- 6.4.12 Lhoist

- 6.4.13 Minerals Technologies Inc.

- 6.4.14 Mississippi Lime Company

- 6.4.15 Newpark Resources Inc.

- 6.4.16 Omya AG

- 6.4.17 Sibelco

- 6.4.18 The Cary Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment