|

시장보고서

상품코드

2043886

미국의 프로판 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Propane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

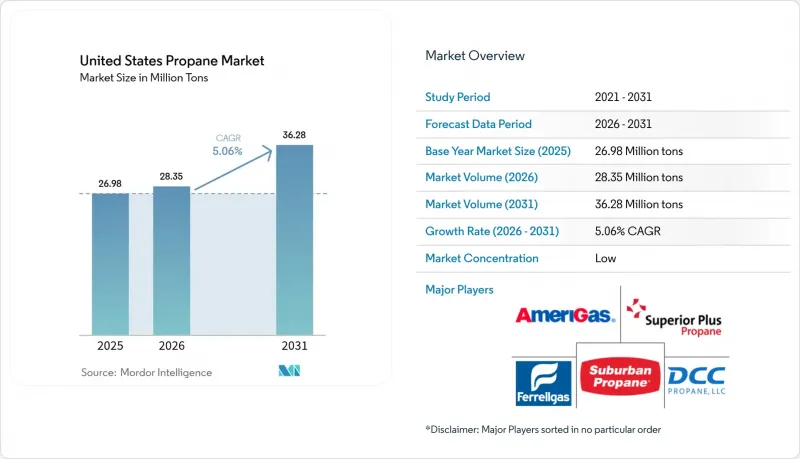

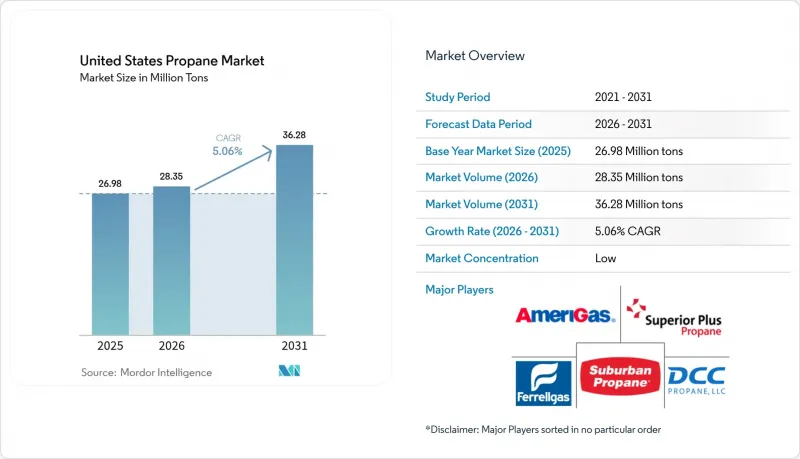

미국의 프로판 시장 규모는 2025년 2,698만 톤으로 평가되었습니다. 2026년 2,835만 톤으로부터, 2031년까지 3,628만 톤으로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.06%를 나타낼 전망입니다.

프로판 탈수소(PDH) 설비의 증설과 비상용 전원의 견조한 도입을 배경으로 차량 연료 전환이 탄력을 받고 있습니다. 이러한 추세에 따라 기존에는 날씨에 좌우되던 주거용 수요에서 수송 및 석유화학 용도로 수요의 무게 중심이 이동하고 있습니다. 2025년까지 천연가스 처리가 전체 수요의 대부분을 차지했습니다. 그러나 재생가능 프로판도 상당한 진전을 보이고 있습니다. 이러한 성장은 주로 캘리포니아주의 저탄소 연료 기준(LCFS) 크레딧에 의한 것으로, 이는 조달 경제의 구조를 완전히 바꾸어 놓았습니다. 스쿨버스의 연료 전환과 라스트마일 배송의 확대를 배경으로 자동차 연료에 대한 수요가 증가하고 있습니다. 이러한 전환을 통해 더 엄격한 NOx 배출 규제를 준수하면서도 디젤 연료에 비해 연료비를 현저히 절감할 수 있습니다. 멕시코만 지역의 PDH 시설에 대한 투자는 원료에 대한 구조적 수요를 창출하고 계절적 난방 수요 변동에 따른 영향을 완화하고 있습니다. 한편, IoT를 활용한 '서비스형 프로판(Propane-as-a-Service)' 모델이 유통 방식을 혁신하고 있습니다. 이러한 모델은 판매자의 배송 횟수를 줄이고 고객 유지율을 향상시킴으로써 대형 소매업체가 세분화되기 쉬운 시장에서 확고한 지위를 유지할 수 있게 해줍니다.

미국의 프로판 시장 동향과 인사이트

디젤 규제 강화에 따라, 차량들의 오토가스로의 전환이 가속화되고 있습니다.

각 학군은 '클린 스쿨 버스 프로그램'의 보조금을 활용하여 디젤 차량 교체를 추진하고 있습니다. 디젤보다 저렴한 비용으로 프로판을 확보할 수 있기 때문에 단 몇년만에 투자 회수가 가능합니다. 프로판 직분사 엔진은 압도적인 마력으로 디젤과 동등한 토크를 발휘할 뿐만 아니라 NOx 배출량을 크게 줄입니다. 블루버드의 7.3리터 플랫폼과 커민스의 B6.7 프로판 엔진은 이 기술을 클래스 6-7 배송용 차량으로 확장하여 수십만 대 규모 시장을 목표로 하고 있습니다. 차량 운영자는 연료비를 크게 절감하고 있으며, 텔레매틱스 데이터를 통해 연간 운행 주기에서 우수한 주행거리를 달성하는 안정적인 성능을 확인할 수 있습니다. 대도시 지역에서 저공해 구역의 도입이 진행됨에 따라 배터리 전기 시스템에 비해 초기 투자가 적은 프로판은 전환이 가속화되고 있으며, 이러한 추세는 2026년부터 2031년의 예측 기간 동안 지속될 것으로 예측됩니다.

석유화학 PDH의 생산능력 증설로 원료 수요 확고히 뒷받침할 것

Enterprise Products Partners의 PDH 2 공장은 하루에 대량의 프로판을 처리하여 폴리머 등급프로파일렌을 생산하고 있습니다. 2028년까지 LyondellBasell의 채널뷰 확장을 통해 이 생산 능력은 더욱 강화될 예정입니다. 현재 PDH 플랜트가 석유화학용 프로판 소비량의 상당 부분을 차지하고 있기 때문에 그 수요는 정유공장 가동률과 분리되어 있습니다. 한편, 자본비용이 낮은 신형 유동접촉 탈수소(FCDh) 플랜트 설계는 ESG 파이낸싱의 어려움에도 불구하고 생산능력 확대를 주도하고 있습니다. 향후 2026년부터 2031년까지의 예측 기간 동안 견조한 석유화학 수요가 미국의 프로판 시장을 견인할 것으로 예측됩니다.

가격 변동으로 유통업체 마진 압박

2024년에는 따뜻한 날씨와 기록적인 NGL 생산량으로 인해 몬트 벨뷰의 현물 가격이 크게 하락하여 고정 가격 계약 보유자에게 어려움을 겪었습니다. 연중 수출이 급증하고, 아시아 지역의 매력적인 프리미엄을 배경으로 배럴당 공급이 해외로 전환되었습니다. 멕시코만 연안과 지역 허브 간의 베이시스 리스크로 인해 헤지가 불완전해지는 경우가 빈번하게 발생했습니다. 그 결과 Suburban Propane은 판매량은 증가했지만, 회계연도 갤런당 매출 총이익률은 감소했습니다.

부문 분석

2025년, 천연가스 처리가 공급 구조를 지배하여 78.72%의 큰 점유율을 차지했습니다. 이는 주로 몬트 벨뷰(Mont Bellevue)의 분별 활동과 파미안 분지(Permian Basin)의 부생가스의 견조한 생산량에 힘입은 결과입니다. 이러한 처리 추세는 정유사의 제품별 공급이 감소하는 가운데서도 미국의 프로판 시장을 강화시키고 있습니다. 재생가능 프로판은 현재 전체 공급량에서 차지하는 비중은 미미하지만, 2026-2031년의 예측 기간 동안 CAGR 9.95%의 괄목할만한 성장세를 보이고 있습니다. 이 급증은 주로 LCFS 크레딧에 의한 것으로, 캘리포니아-오레곤 지역의 초기 도입자들의 관심을 끌며 수익성 높은 틈새 시장을 개척하고 있습니다. 이처럼 변화하는 미국의 프로판 시장에서 전통적인 NGL(천연가스 액화천연가스) 추출은 상품 수요를 충족시키는 반면, 선구적인 저탄소 이니셔티브는 신용을 중시하는 구매자를 끌어들이고 있습니다.

인수합병의 움직임은 인프라의 가치가 높아지고 있음을 여실히 보여주고 있습니다. ONEOK의 Magellan 인수는 강력한 분별 능력을 가진 두 개의 대형 기업을 통합하는 것이었습니다. 수출의 유연성을 높이기 위해 엔터프라이즈사는 저장 동굴을 계획적으로 확장하고 있습니다. ESG에 대한 엄격한 감시에도 불구하고, 생산업체들은 PDH(프로파일렌 탈수소) 및 수출 시장의 안정적인 수요에 힘입어 가공 프로젝트에 대한 낙관적인 전망을 유지하고 있습니다. 재생에너지의 선구자인 네스테와 오베론은 콤팩트한 시설을 건설하고 있습니다. 기존 재생 디젤 및 DME(디메틸에테르) 생산 라인을 활용하여 저탄소 공급을 확대하기 위한 전략적, 모듈식 접근 방식을 구현하고 있습니다.

"미국의 프로판 시장 보고서는 공급원(천연가스 처리, 원유 정제, 재생에너지), 용도(난방/급탕, 요리, 자동차 연료, 화학 원료, 발전, 기타 용도), 최종 사용자 산업(주거, 상업, 산업, 운송, 발전, 기타 최종 사용자 산업)별로 분류하여 분석했습니다. 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The United States Propane Market size is projected to expand from 26.98 million tons in 2025 and 28.35 million tons in 2026 to 36.28 million tons by 2031, registering a CAGR of 5.06% between 2026 to 2031.

Fleet conversions are gaining momentum, driven by expanding propane dehydrogenation (PDH) capacities and robust standby-power deployments. These developments are shifting volumes away from a traditionally weather-dependent residential base and toward transportation and petrochemical applications. By 2025, natural-gas processing accounted for the majority of the total volume. However, renewable propane has been making significant progress. This growth is largely attributed to California's Low Carbon Fuel Standard (LCFS) credits, which have transformed the economics of sourcing. The demand for motor fuel has been rising, driven by conversions in school buses and last-mile deliveries. These transitions are resulting in notable savings in fuel costs compared to diesel, all while adhering to stricter NOx emissions limits. Investments in PDH facilities along the Gulf Coast have created a structural pull for feedstock, providing insulation from seasonal heating fluctuations. On another front, IoT-enabled "Propane-as-a-Service" models are revolutionizing the distribution landscape. By reducing distributor truck rolls and boosting customer retention, these models are empowering large retailers to maintain their foothold in an otherwise fragmented market.

United States Propane Market Trends and Insights

Autogas Fleet Conversions Accelerate as Diesel Rules Tighten

School districts are utilizing Clean School Bus Program grants to replace diesel units. By securing propane at a cost lower than diesel, they achieve paybacks in just a few years. Propane direct-injection engines, with their impressive horsepower, not only replicate diesel torque but also significantly reduce NOx emissions. Blue Bird's 7.3-liter platform and Cummins' B6.7 Propane are advancing this technology into Class 6-7 delivery fleets, targeting a market of hundreds of thousands of vehicles. Fleet operators are experiencing substantial fuel savings, and telematics confirm steady performance with annual duty cycles achieving impressive mileage. As more metropolitan areas adopt low-emission zones, the lower capital requirement of propane - compared to battery-electric systems - is accelerating conversions, a trend projected to persist during the forecast period of 2026-2031

Petrochemical PDH Capacity Additions Lock In Feedstock Demand

Enterprise Products Partners' PDH 2, which processes a substantial daily volume of propane, produces polymer-grade propylene. By 2028, LyondellBasell's Channelview expansion will add to this capacity. With PDH units now commanding a significant portion of petrochemical propane consumption, their demand has become decoupled from refinery operating rates. Meanwhile, newer fluid catalytic dehydrogenation (FCDh) designs, which come with lower capital costs, are driving capacity expansions, despite hurdles in ESG financing. Looking ahead, robust petrochemical demand during the forecast period of 2026-2031 is expected to bolster the United States propane market.

Price Volatility Compresses Distributor Margins

In 2024, warm weather and record NGL output caused a significant drop in Mont Belvieu spot prices, posing challenges for holders of fixed-price contracts. Throughout the year, exports surged, with barrels being redirected offshore due to attractive premiums in Asia. The basis risk between the Gulf and regional hubs often resulted in imperfect hedges. As a result, Suburban Propane experienced a decline in its fiscal-year gross margin per gallon, even with increased volumes.

Other drivers and restraints analyzed in the detailed report include:

- Stand-by Generator Installations Rise with Grid-Reliability Investments

- Propane-as-a-Service Subscription Models Boost Margins

- Rail and Pipeline Bottlenecks Elevate Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, natural-gas processing dominated the supply landscape, commanding a substantial 78.72% share. This was largely driven by fractionation activities at Mont Belvieu and robust outputs from the Permian's associated gas. Such processing dynamics fortify the U.S. propane market, even as contributions from refinery coproducts diminish. Although renewable propane currently holds a modest slice of the supply pie, it is on an impressive growth trajectory, boasting a 9.95% CAGR during the forecast period of 2026-2031. This surge is largely attributed to LCFS credits, carving out a lucrative niche that has piqued the interest of early adopters in the California-Oregon region. In this evolving U.S. propane landscape, traditional NGL extraction aligns with commodity demands, while pioneering low-carbon initiatives draw in credit-centric buyers.

Mergers and acquisitions underscore the escalating value of infrastructure: ONEOK's takeover of Magellan unified two powerhouses with substantial fractionation capabilities. In a bid to bolster export flexibility, Enterprise is methodically expanding its storage caverns. Even amidst ESG scrutiny, producers maintain an optimistic outlook on processing projects, buoyed by consistent demand from PDH and export markets. Renewable trailblazers, Neste and Oberon, are establishing compact facilities. By harnessing existing renewable-diesel or DME trains, they are exemplifying a strategic, modular approach to scaling low-carbon supplies.

The United States Propane Market Report is Segmented by Source (Natural Gas Processing, Crude Oil Refining, and Renewable), Application (Space and Water Heating, Cooking, Motor Fuel, Chemical Feedstock, Power Generation, and Other Applications), and End-User Industry (Residential, Commercial, Industrial, Transportation, Power Generation, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AmeriGas Propane, Inc.

- Blossman Gas

- CHS Inc.

- DCC Propane

- Energy Transfer LP

- Ferrellgas

- GROWMARK Inc.

- MFA Oil Company

- NGL Energy Partners LP

- Paraco

- Pinnacle

- Suburban Propane

- Superior Plus Propane

- ThompsonGas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Autogas fleet conversions (school buses/delivery/municipal)

- 4.2.2 Petrochemical PDH capacity additions

- 4.2.3 Stand-by generator installations for grid resiliency

- 4.2.4 Propane-as-a-Service subscription models (IoT tank monitoring)

- 4.2.5 Off-grid microgrids for rural broadband towers

- 4.3 Market Restraints

- 4.3.1 Price volatility tied to NGL and crude markets

- 4.3.2 Rail/pipeline bottlenecks in key PADDs

- 4.3.3 ESG-driven divestment limiting upstream capex

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Natural Gas Processing

- 5.1.2 Crude Oil Refining

- 5.1.3 Renewable Propane (Bio-Propane)

- 5.2 By Application

- 5.2.1 Space and Water Heating

- 5.2.2 Cooking

- 5.2.3 Motor Fuel

- 5.2.4 Chemical Feedstock

- 5.2.5 Power Generation

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Transportation

- 5.3.5 Power Generation

- 5.3.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AmeriGas Propane, Inc.

- 6.4.2 Blossman Gas

- 6.4.3 CHS Inc.

- 6.4.4 DCC Propane

- 6.4.5 Energy Transfer LP

- 6.4.6 Ferrellgas

- 6.4.7 GROWMARK Inc.

- 6.4.8 MFA Oil Company

- 6.4.9 NGL Energy Partners LP

- 6.4.10 Paraco

- 6.4.11 Pinnacle

- 6.4.12 Suburban Propane

- 6.4.13 Superior Plus Propane

- 6.4.14 ThompsonGas

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment