|

시장보고서

상품코드

2043887

적층 부스바 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Laminated Busbar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

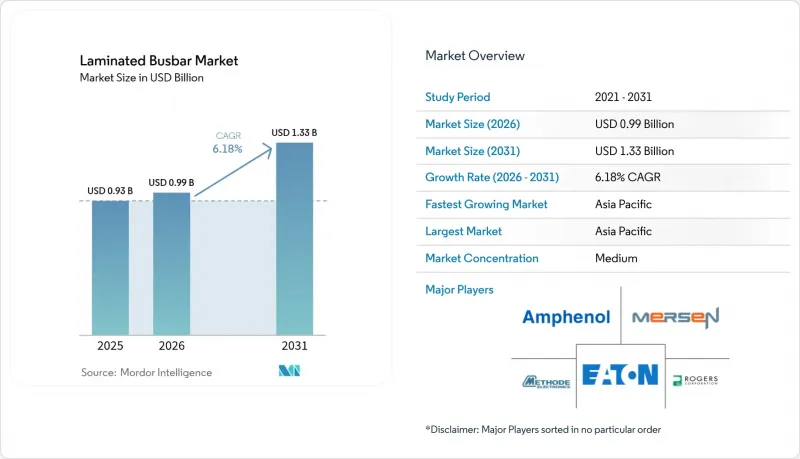

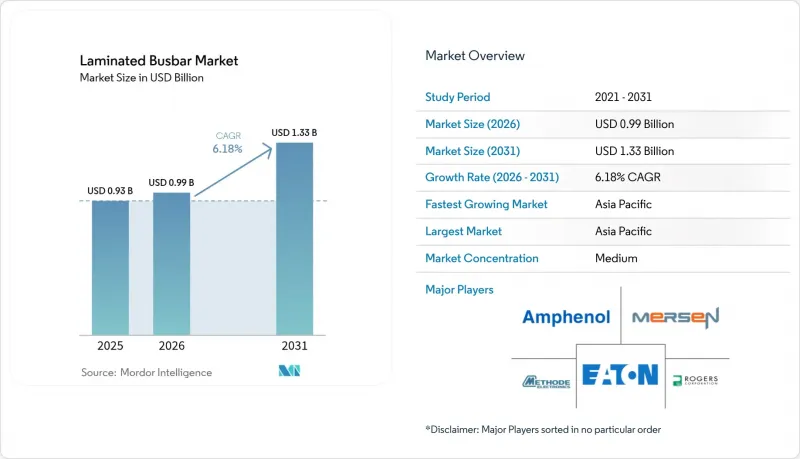

2026년 적층 부스바 시장 규모는 9억 8,747만 달러로 추정됩니다. 2025년 9억 3,000만 달러에서 성장하여 2031년에는 13억 3,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 6.18%를 나타낼 것으로 예상됩니다.

이러한 성장의 원동력은 전기 운송 장비, 재생 에너지용 인버터, 고밀도 데이터센터의 전원 백플레인 등 저인덕턴스, 고열 효율의 컴팩트한 배전 어셈블리를 필요로 하는 분야가 주도하고 있습니다. 성능이 매우 중요한 시스템에서는 구리가 여전히 주요 도체로 사용되지만, 무게가 중요한 응용 분야에서는 알루미늄과 하이브리드 금속의 조합이 주목을 받고 있습니다. 원자재 공급의 안정성과 광대역 갭 파워 모듈의 지속적인 발전은 전통적인 바 및 케이블 하네스보다 적층 구조를 우선시하는 새로운 설계 요구 사항을 뒷받침합니다. 구리 가격 변동에 따른 가격 압력에 대해서는 제조 생산성 향상과 안전성과 공간 절약성 향상에 대해 최종 사용자가 더 높은 가격을 지불할 의향이 높아진 것이 그 영향을 일부 상쇄하고 있습니다.

세계의 적층 부스바 시장 동향 및 인사이트

EV 및 HEV의 보급이 소형 전원 솔루션을 주도하고 있습니다.

자동차 제조업체들은 배터리 팩의 설치 면적을 줄이고 열 성능을 향상시키기 위해 적층형 부스바의 채택을 가속화하고 있습니다. 테슬라의 구조용 배터리와 BYD의 블레이드 형태는 적층 도체가 높은 전류 밀도를 유지하면서 조립의 복잡성을 40%까지 줄일 수 있다는 것을 입증했습니다.(1) 냉간 클래드 공법으로 제조된 알루미늄-구리 하이브리드 소재는 경량화와 전도성을 겸비하고 있으며, 초음파 용접과 은 코팅을 통해 알루미늄의 산화 문제를 해결하고 있습니다. 400V-800V 시스템으로 전환하는 차량 플랫폼에서는 안전 마진을 유지하면서 변화하는 배터리 화학적 특성에 대응할 수 있는 유연한 부스바 형상이 요구되고 있습니다. 그 결과, 공급업체 기반이 확대되고, 소재 전문 기업 및 Tier 1 인티그레이터들이 장기 공급 계약을 따내기 위해 경쟁하면서 적층형 부스바 시장이 활성화되고 있습니다.

재생에너지용 인버터 도입 확대는 그리드 통합을 촉진합니다.

태양광 및 풍력 발전 OEM 업체들은 저인덕턴스 및 고전류 인버터 단에 적층형 부스바를 지정하고 있습니다. SiC 및 GaN 스위치는 현재 50kHz 이상의 주파수에서 작동하며, 적층 구조로 인해 부동 인덕턴스를 최대 90%까지 줄일 수 있어 변환 효율이 향상되고, 축전 설비와 결합된 자산에서 양방향 전력 흐름을 가능하게 합니다.(2) 표준화된 인터페이스를 통해 에너지 저장 모듈의 교체를 간소화하고, 내장된 센서로 예측 유지보수를 가능하게 함으로써 대규모 발전소의 인버터 다운타임을 방지하고 적층형 부스바 시장을 더욱 확대할 수 있습니다.

변동하는 구리 및 알루미늄 가격

2024년 7월, 구리 가격은 파운드당 6.20달러에 이르렀고, 원자재 비용이 원가의 최대 70%를 차지함에 따라 부품 공급업체들은 가격표를 최대 45% 인상했습니다. 다년간의 인버터 및 송전망 계약으로 인해 비용 전가 능력이 제한되어 수익률이 압박을 받고 있습니다. 하이브리드 시스템이 점유율을 확대하는 가운데, 알루미늄 가격의 변동으로 인해 불확실성이 더욱 커지고 있습니다. 일부 OEM 업체들은 장기 공급 계약을 통해 리스크를 헤지하거나, 전도성을 잃지 않고 리스크를 줄일 수 있는 구리 피복 알루미늄 도체를 채택하는 것을 고려하고 있습니다.

부문 분석

2025년 구리는 독보적인 전도성과 성숙한 가공 공정에 힘입어 적층 부스바 시장 점유율의 71.05%를 차지했습니다. 이러한 장점은 저항 손실과 온도 상승을 허용하지 않는 고출력 인버터와 배터리 팩에 의해 뒷받침됩니다. 그러나 자동차 제조업체들이 밀도를 희생하여 무게를 줄이고 원자재 비용을 40% 절감할 수 있게 되면서 알루미늄 제품 시장은 CAGR 7.85%로 확대될 것으로 예측됩니다. Samuel Taylor와 동종업계의 냉간 클래드 바이메탈 스트립은 전류 경로와 기계적 무결성을 유지하는 이음매 없는 알루미늄-구리 접합부를 구현합니다. 그 결과, 사양 설계 엔지니어들은 800V 구동용 인버터 및 충전 모듈에 하이브리드 소재의 채택을 점점 더 많이 승인하고 있으며, 부품표의 표준을 재구성하고 있습니다.

알루미늄의 채택으로 절연 연구소는 융점이 낮은 도체에 대응하기 위해 유전체 두께를 재검토해야 하는 반면, 은 플래시 도금이나 니켈 도금은 접합면의 수명을 연장할 수 있습니다. 무게에 최적화된 레일 설계는 장거리 EV의 배터리 팩의 질량을 줄이고, 추가 kW시 또는 적재량을 가능하게 합니다. 적층 부스바 산업을 대상으로 하는 공급업체들은 대규모 생산 로트에서 일관된 클래딩의 무결성을 보장하기 위해 초음파 용접 라인과 자동 품질 관리에 투자하고 있습니다.

에폭시 분체 코팅은 강력한 기계적 보호와 부품당 저렴한 비용으로 인해 2025년 매출의 37.45%를 차지했으며, 배전반 및 FA 캐비닛의 기본 선택이 되었습니다. 그러나 폴리에스테르 및 폴리이미드 필름은 적층이 얇아짐에 따라 인덕턴스가 감소하고 열전도 경로가 개선되어 CAGR 7.55%로 보급이 진행되고 있습니다. 특수 필름은 SiC 트랙션 모듈에서 흔히 볼 수 있는 급격한 온도 변화에 견딜 수 있으며, 175°C 이상의 접합부 온도에서도 균열 없이 작동할 수 있습니다.

필름 라미네이트는 2mm 미만의 두께를 가진 부스바를 가능하게 하며, 좁은 배터리 팩의 캐비티를 따라 뱀처럼 배치됩니다. 내열성 섬유 보강재와 세라믹 필러는 유연성을 유지하면서 절연 파괴 전압을 향상시킵니다. 또한, 환경, 건강 및 안전(EHS) 팀은 새로운 무용제 필름 접착제가 제조 과정에서 휘발성 유기 화합물(VOC) 배출을 줄여 제품 수명을 희생하지 않고 기업의 지속가능성 목표 달성을 촉진하고 있다고 지적합니다.

"적층 부스바 시장 보고서는 전도성 재료(구리, 알루미늄, 하이브리드), 절연 재료(에폭시 분체 코팅, 폴리에스테르 등), 부스바 구성(다층, 고층, 플렉스/박형 부스바), 정격 전압(저전압 등), 용도(신재생에너지 등), 최종 사용자(전력회사, 운송장비 제조업체 등) 및 지역(북미, 아시아태평양 등)별로 분류되어 있습니다. 운송 장비 제조업체 등), 그리고 지역(북미, 아시아태평양 등)으로 분류되어 있습니다.

지역별 분석

2025년 아시아태평양은 적층 부스바 시장에서 40.95%의 점유율을 차지하며 시장을 주도했습니다. 중국, 일본, 한국의 수직 통합형 공급망은 리드타임 단축과 비용 절감으로 인해 이 지역은 CAGR 7.2%로 확대될 것으로 예측됩니다. 이 지역의 적층형 부스바 시장 규모는 배터리 팩 생산 확대에 따른 다년 계약을 확보한 대규모 EV 생산 라인의 수혜를 받고 있습니다. 또한, 인도에서는 재생에너지용 인버터 도입이 가속화되고 있으며, 이는 이 지역의 적층 생산 능력에 대한 수요를 더욱 증가시키고 있습니다.

북미는 2위를 차지했습니다. 이는 하이퍼스케일 데이터센터 리노베이션과 야심찬 자동차 전동화 일정에 힘입은 것입니다. 테슬라의 구조용 배터리 프로그램만으로도 맞춤형 도체 레이아웃에 대한 수요가 급증하고 있으며, 클라우드 캠퍼스에서 48V 랙으로의 전환은 사전 설계된 백플레인 키트에 대한 안정적인 수주를 보장하고 있습니다. 연방 정부의 인센티브는 핵심 부품 제조의 현지화를 장려하여 미국 내 라미네이트 투자에 박차를 가하고 있습니다.

유럽에서는 엄격한 환경 지침과 산업 자동화로 인해 꾸준한 보급이 유지되고 있습니다. 풍력발전 OEM 업체들은 해상 컨버터 스테이션에서 SiC 파워 모듈과 결합된 부스바에 의존하고 있으며, 독일 공작기계 제조업체들은 캐비닛의 설치 면적을 줄이기 위해 공장용 패널을 적층 기판으로 개조하고 있습니다. 지역 공급업체들은 저탄소 구리 조달과 '생산에서 폐기까지' 재활용 프로그램을 통해 차별화를 꾀하고 있으며, 이는 EU의 지속가능성 목표에 부합합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29Laminated Busbar market size in 2026 is estimated at USD 987.47 million, growing from 2025 value of USD 0.93 billion with 2031 projections showing USD 1.33 billion, growing at 6.18% CAGR over 2026-2031.

Momentum comes from electrified transportation, renewable energy inverters, and high-density data center power backplanes, all of which demand compact power distribution assemblies with low inductance and high thermal efficiency. Copper remains the baseline conductor for performance-critical systems, while aluminum and hybrid metal combinations build traction in weight-sensitive applications. Supply security for raw materials and continuing advances in wide-bandgap power modules underpin new design requirements that favor laminated architectures over conventional bar or cable harnesses. Pricing pressure from volatile copper costs is partially offset by manufacturing productivity gains and the growing willingness of end users to pay a premium for enhanced safety and space savings.

Global Laminated Busbar Market Trends and Insights

EV & HEV Proliferation Drives Compact Power Solutions

Automakers are accelerating the adoption of laminated busbars to reduce battery-pack footprints and improve thermal performance. Tesla's structural battery and BYD's blade format demonstrate how laminated conductors reduce assembly complexity by 40% while maintaining high current density.[1] Aluminum-copper hybrids produced via cold-cladding now combine weight savings with conductivity, and ultrasonic welding, along with silver coatings, resolve aluminum oxidation hurdles. Vehicle platforms shifting to 400 V-800 V systems require flexible busbar geometries that accommodate changing cell chemistries without compromising safety margins. The cascading effect is a broadened supply base, with materials specialists and tier-one integrators vying for long-term supply awards, boosting the laminated busbar market.

Renewable-Energy Inverter Roll-outs Expand Grid Integration

Solar and wind OEMs specify laminated busbars for low-inductance, high-current inverter stages. SiC and GaN switches now operate well past 50 kHz, and laminated geometries cut stray inductance by up to 90%, improving conversion efficiency and enabling bidirectional power flow in storage-combined assets.[2] Standardized interfaces simplify the swapping of energy-storage modules, while embedded sensors enable predictive maintenance that prevents inverter downtime in utility-scale parks, further expanding the laminated busbar market.

Volatile Copper & Aluminum Prices

Copper reached USD 6.20 per pound in July 2024, prompting component suppliers to increase their price lists by up to 45%, as raw materials account for up to 70% of the cost. Multi-year inverter or grid contracts limit pass-through ability, eroding margins. Aluminum swings add another layer of uncertainty just as hybrids gain share. Some OEMs hedge their bets with long-term supply agreements or explore copper-clad aluminum conductors that reduce exposure without compromising conductivity.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Power-Backplane Demand Spike

- Industrial Electrification & Automation Surge

- Heat-Dissipation & Delamination Beyond 1 kV

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper captured 71.05% of the laminated busbars market share in 2025, driven by its unmatched conductivity and mature processing routes. This dominance is anchored by high-power inverters and battery packs that cannot compromise on resistive losses or heat rise. However, aluminum sections are expected to accelerate at an 7.85% CAGR as vehicle OEMs trade density for weight savings and achieve a 40% reduction in raw-material costs. Cold-clad bimetal strip from Samuel Taylor and similar suppliers enables jointless aluminum-copper interfaces that maintain current paths and mechanical integrity. As a result, specification engineers increasingly approve hybrids for 800 V traction inverters and charging modules, reshaping bill-of-materials norms.

Aluminum adoption forces insulation labs to rethink dielectric thickness for lower melting-point conductors, while silver-flash or nickel-plate coatings extend mating-surface life. Weight-optimized rail designs trim pack mass in long-range EVs, unlocking extra kilowatt-hours or payload. Suppliers targeting the laminated busbars industry invest in ultrasonic welding lines and automated quality control to guarantee consistent clad integrity across large production batches.

Epoxy powder coating accounted for 37.45% of the revenue in 2025 by combining robust mechanical protection with low per-part costs, making it the default choice for switchgear and factory automation cabinets. Yet polyester and polyimide films are gaining traction at a 7.55% CAGR because thinner stacks translate to lower inductance and better thermal pathways. Specialty films withstand the rapid temperature swings commonly seen in SiC traction modules, supporting junction temperatures exceeding 175°C without cracking.

Film laminates enable busbars under 2 mm thick that snake through cramped battery-pack cavities. Heat-resistant fiber reinforcements and ceramic fillers raise breakdown voltage while maintaining flexibility. Environmental, health, and safety teams also note that newer solvent-free film adhesives lower volatile organic compound emissions in production, advancing corporate sustainability targets without sacrificing product lifespan.

The Laminated Busbar Market Report is Segmented by Conducting Material (Copper, Aluminum, and Hybrid), Insulation Material (Epoxy Powder Coating, Polyester, and More), Busbar Configuration (Multi-Layer, High-Layer, and Flex/Thin Busbars), Voltage Rating (Low Voltage, and More), Application (Renewable Energy, and More), End-User (Power Utilities, Transportation OEMs, and More), and Geography (North America, Asia-Pacific, and More).

Geography Analysis

The Asia-Pacific region dominated the laminated busbars market in 2025, with a 40.95% share, and is expected to expand at a 7.2% CAGR as vertically integrated supply chains in China, Japan, and South Korea compress lead times and reduce costs. The laminated busbars market size in the region benefits from large-volume EV production lines that secure multiyear busbar contracts tied to battery-pack ramps. India accelerates renewable-energy inverter deployment, adding further pull for regional lamination capacity.

North America ranked second, driven by hyperscale data-center retrofits and ambitious automotive electrification timelines. Tesla's structural battery programs alone create recurring demand spikes for custom conductor layouts, while 48V rack conversions in cloud campuses secure steady orders for pre-engineered backplane kits. Federal incentives to localize critical-component manufacturing add momentum to US-based lamination investments.

Europe relies on stringent environmental directives and industry automation to maintain steady adoption. Wind-energy OEMs rely on busbars that pair with SiC power modules in offshore converter stations, whereas German machine-tool makers retrofit factory panels with laminated boards to shrink cabinet footprints. Regional suppliers differentiate through low-carbon copper sourcing and cradle-to-grave recycling programs, resonating with EU sustainability goals.

- Eaton Corporation plc

- Rogers Corporation

- Mersen SA

- Methode Electronics Inc.

- Amphenol Corporation

- Molex LLC

- Sun.King Power Electronics Group Ltd

- Zhuzhou CRRC Times Electric Co., Ltd

- Storm Power Components

- Segue Electronics Inc.

- EMS Industrial & Service Company

- Ryoden Kasei Co., Ltd

- Shanghai Eagtop Electronic Technology Co., Ltd

- Suzhou West Deane Machinery Inc.

- Raychem RPG Private Limited

- Zhejiang RHI Electric Co., Ltd

- Electronic Systems Packaging LLC

- Idealec SAS

- Advanced Energy Industries, Inc.

- Delta Electronics, Inc.

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Littelfuse Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV & HEV proliferation

- 4.2.2 Renewable energy inverter roll-outs

- 4.2.3 Data-center power-backplane demand spike

- 4.2.4 Industrial electrification & automation surge

- 4.2.5 SiC/GaN-based high-voltage modules adoption

- 4.2.6 Modular eVTOL battery pack architectures

- 4.3 Market Restraints

- 4.3.1 Volatile copper & aluminum prices

- 4.3.2 Low-cost conventional busbars as substitutes

- 4.3.3 Heat-dissipation & delamination beyond 1 kV

- 4.3.4 Aerospace qualification/documentation burden

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Conducting Material

- 5.1.1 Copper

- 5.1.2 Aluminum

- 5.1.3 Hybrid (Cu-Al composite)

- 5.2 By Insulation Material

- 5.2.1 Epoxy Powder Coating

- 5.2.2 Polyvinyl Fluoride Film

- 5.2.3 Polyester

- 5.2.4 Heat-Resistant Fiber

- 5.2.5 Polyimide/Kapton

- 5.2.6 Others

- 5.3 By Busbar Configuration

- 5.3.1 Multi-layer (3 to 5 layers)

- 5.3.2 High-layer (More Than 5 layers)

- 5.3.3 Flex/Thin busbars

- 5.4 By Voltage Rating

- 5.4.1 Low Voltage (Below 1 kV)

- 5.4.2 Medium Voltage (1 to 35 kV)

- 5.4.3 High Voltage (Above 35 kV)

- 5.5 By Application

- 5.5.1 Electric and Hybrid Vehicles

- 5.5.2 Renewable Energy (Solar, Wind, ESS)

- 5.5.3 Data Centers and Cloud Infrastructure

- 5.5.4 Industrial Drives and Machinery

- 5.5.5 Rail and Mass Transit

- 5.5.6 Aerospace and eVTOL

- 5.6 By End-User

- 5.6.1 Power Utilities

- 5.6.2 Industrial OEMs

- 5.6.3 Transportation OEMs

- 5.6.4 Residential and Commercial Construction

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germnay

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 ASEAN Countries

- 5.7.3.7 Rest of Asia Pacific

- 5.7.4 South America

- 5.7.4.1 Argentina

- 5.7.4.2 Brazil

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Eaton Corporation plc

- 6.4.2 Rogers Corporation

- 6.4.3 Mersen SA

- 6.4.4 Methode Electronics Inc.

- 6.4.5 Amphenol Corporation

- 6.4.6 Molex LLC

- 6.4.7 Sun.King Power Electronics Group Ltd

- 6.4.8 Zhuzhou CRRC Times Electric Co., Ltd

- 6.4.9 Storm Power Components

- 6.4.10 Segue Electronics Inc.

- 6.4.11 EMS Industrial & Service Company

- 6.4.12 Ryoden Kasei Co., Ltd

- 6.4.13 Shanghai Eagtop Electronic Technology Co., Ltd

- 6.4.14 Suzhou West Deane Machinery Inc.

- 6.4.15 Raychem RPG Private Limited

- 6.4.16 Zhejiang RHI Electric Co., Ltd

- 6.4.17 Electronic Systems Packaging LLC

- 6.4.18 Idealec SAS

- 6.4.19 Advanced Energy Industries, Inc.

- 6.4.20 Delta Electronics, Inc.

- 6.4.21 Siemens AG

- 6.4.22 ABB Ltd

- 6.4.23 Schneider Electric SE

- 6.4.24 Littelfuse Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment