|

시장보고서

상품코드

2043888

유럽의 방위 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

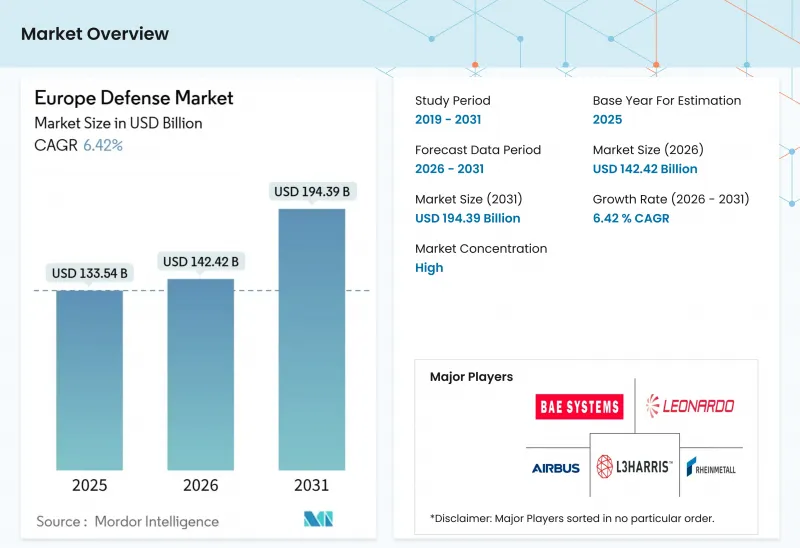

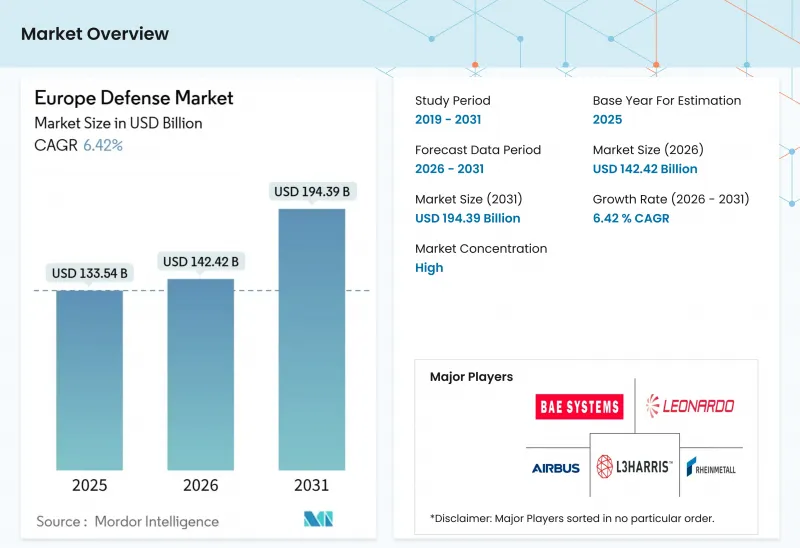

유럽의 방위 시장 규모는 2025년 1,335억 4,000만 달러로 평가되었습니다. 2026년 1,424억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.42%를 나타내, 2031년까지 1,943억 9,000만 달러에 이를 것으로 예측됩니다.

NATO의 방위비 지출 증가와 지속적인 확대 노력은 육, 공, 해, 우주 프로그램에 걸친 다년간의 조달 계획과 생산 능력에 대한 투자를 촉진하여 유럽 방위 시장의 구조적 성장을 강화하고 있습니다. 러시아의 2024년 국방예산은 1,490억 달러로 GDP의 7.1%에 달했습니다. 이에 따라 최전방 및 최전선에 인접한 국가들의 무기 생산, 통합방공, 해군의 억지력에 대한 관심이 높아지고 있습니다. 각국 정부는 유럽산 부품 채택과 동맹국 간 상호 운용 가능한 시스템을 우선시하는 공통 조달 프레임워크와 현지 산업화 규칙을 활용하여 회복탄력성(resilience)을 향상시키고 있습니다. 또한, 유럽 방위 시장에서는 소프트웨어와 데이터의 통합이 전장에서의 우위를 창출하고 기존 대기업을 보완하는 신규 시장 진출기업에게 기회를 제공하는 네트워크 중심 개념으로의 전환을 볼 수 있습니다.

유럽의 방위 시장 동향과 인사이트

NATO의 방위비 지출 기준, 각국의 예산 조정 가속화

동맹국 정부들은 방위비 배분을 GDP 대비 산출식에 고정시킴으로써 연도별 변동성을 억제하고, 유럽 방위 시장에서 산업계가 다년간의 생산능력 확대를 계획할 수 있도록 하고 있습니다. NATO 회원국들은 수년간의 2% 가이드라인을 넘어 더 높은 수준의 지속 가능한 지출로 나아가고 있으며, 모든 동맹국들은 2025년에 이어 2026년에도 즉각적인 대응 태세와 비축을 재구축하는 것을 우선순위로 삼고 있습니다. 영국은 2027년까지 GDP 대비 2.5%를 달성하겠다고 공언하고 있으며, 차기 의회에서는 3%를 달성하겠다는 의지를 보이고 있습니다. 이에 따라 항공전력, 육상 시스템, 해상방어에 대한 수요 전망은 더욱 강화되고 있습니다. 스웨덴은 NATO 가입 첫 해에 2.0%의 기준을 달성하여 유럽 전체가 영토 방어와 억지력으로 전환하는 데 힘을 보탰다. 2026년 1월 15일부터 시행되는 독일의 새로운 '계획 및 조달 가속화법'은 조달 프로세스를 효율화하고, 유럽 방위 시장에서 규모의 경제를 지원하며, 상호 운용 가능한 기성품(기성품) 유럽산 솔루션에 우선순위를 부여하도록 설계되었습니다. 이러한 조치가 정착됨에 따라 예산의 자동 배분은 유럽 방위 시장 수요 변동에 지나치게 영향을 받지 않고 탄약, 방공 및 C4ISR(지휘, 통제, 통신, 컴퓨터, 정보, 감시 및 정찰) 능력을 확장할 수 있는 예측가능성을 제공합니다.

EU 방위기금의 인센티브로 국경 간 R&D 및 역량 강화 프로그램 지원 강화

EU의 제도는 회원국과 산업계를 연결하고, 유럽 방위 시장의 연구개발, 초기 조달에서 위험을 공유하며, 더 큰 규모의 국경을 초월한 팀을 구성하고 있습니다. 유럽의 방위산업 프로그램(EDIP)에는 '유럽 제품 우선' 원칙이 포함되어 있으며, 공통 조달에서 비EU산 제품의 비율을 35%로 제한하고, 각국이 수요를 집약하는 경우 최대 25%의 EU 공동 자금 지원을 허용하고 있습니다. 이를 통해 중견 공급업체와 듀얼유즈 분야의 혁신가들의 참여를 촉진할 수 있습니다. EDF와 EDIP는 최소 3개국의 3개 사업체가 협력할 수 있는 인센티브를 창출하고, 센서, AI, UAS(무인항공기 시스템) 분야에서 프라임 계약자와 소프트웨어 중심 공급업체 간의 기술 이전을 가속화하고 있습니다. 2025년 10월에 발표된 유럽연합 집행위원회의 '국방 준비 로드맵'은 2027년 이후 예산 프레임워크에서 국방 및 우주 분야를 확대하기 위한 경로를 제시하며, 유럽 방위 시장에 대한 지속적인 제도적 지원을 표명하고 있습니다. 이러한 구조가 성숙해짐에 따라 공통 표준과 공동 물류로 인해 단위 비용 절감과 주요 제품 라인의 분절화 해소가 진행될 것으로 예측됩니다. 이 프레임워크는 공급업체가 각국의 요구사항과 유럽 공동 사양을 모두 충족하는 모듈식 설계 및 디지털 엔지니어링에 투자하도록 장려합니다.

에너지 전환 우선순위와의 경쟁으로 인한 예산 제약으로 인해

회원국들은 다년간의 재군비 추진과 에너지 전환에 따른 자금 수요의 균형을 맞추기 위해 노력하고 있으며, 유럽 방위 시장에서는 예산의 절충이 계속해서 초점이 되고 있습니다. 'REPowerEU' 계획은 2027년까지 막대한 추가 민관 투자를 요구하고 있으며, 탄소 집약적 투입물의 컴플라이언스 비용이 중공업의 생산 경제성에 지속적으로 영향을 미치고 있습니다. 유럽연합 집행위원회의 예측에 따르면, 이탈리아의 2026년 국방 예산은 313억 유로(368억 3,000만 달러)로 GDP의 약 1.2%에 해당하며, 이는 남유럽 국가들의 재정적 제약이 얼마나 큰지 잘 보여줍니다. EU의 재정 규정은 유연성을 높이기 위해 개정되었지만, 각국의 적자 시정 절차로 인해 동맹의 목표 수준까지 지출을 늘릴 수 있는 속도는 여전히 제한되어 있습니다. 정부가 특별 기금이나 조달을 위한 신속화 조치를 마련하더라도 유럽 방위 시장의 산업 생산량을 결정하는 중요한 변수는 여전히 실행력입니다. 중기적으로, 이미 빠듯한 예산 속에서 에너지 전환의 우선순위를 압박하지 않으면서도 안정적인 국방 관련 현금 흐름을 확보하는 것이 속도 배분의 과제입니다.

부문 분석

2025년 육군은 유럽 방위 시장 점유율의 42.67%를 차지했습니다. 이는 영토 방어, 통합 방공 및 미사일 방어, 기계화 부대에 대한 강조가 다시 강화된 것을 반영합니다. 이 점유율은 유럽 육군 전체가 탄약과 예비 부품의 비축을 늘리고 대응 태세를 강화하는 방향으로 전환하는 것과 일치합니다. 해군은 대잠전, 수상 전투함, 해양 영역 인식을 우선시하는 발트해 및 북대서양 이니셔티브에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 7.67%로 가장 빠르게 확대될 것으로 예측됩니다. 또한, 영역 간 통합으로 인해 유럽 방위 시장에서 해군 자산과 통합 화력 네트워크를 연결하는 해상 ISR 및 지휘통제 노드에 대한 수요가 증가하고 있습니다. 2025년 12월 콘스버그가 독일과 노르웨이의 212CD형 잠수함에 전투 시스템 요소와 항법 시스템을 공급하는 계약을 체결한 것은 수중 능력과 업계 파트너십의 모멘텀을 보여줍니다.

각 공군에서는 센서, 전자전, 항공 경계 임무의 업그레이드가 계속되고 있으며, 차세대 전투 항공 계획에서 주권적 데이터 파이프라인과 통합 이펙터가 강조되고 있습니다. '다이나믹 프론트 25(Dynamic Front 25)'와 같은 훈련은 대규모 연합군의 화력 조정 및 병참을 검증하고, 유럽 방위 시장에서 상호 운용 가능한 무선, 데이터 링크 및 소프트웨어 정의 능력의 조달을 촉진하고 있습니다. 해군의 현대화 목표는 검증된 시스템 통합 능력을 갖추고 납기 내 납품이 가능한 조선소에 주목하고 있으며, 이러한 요인으로 인해 확실한 실행력을 갖춘 업체에게 발주가 집중되고 있습니다. NATO 내 상호운용성은 표준화된 규격에 부합하는 탄약 및 통신 장비의 구매를 촉진하고 있으며, 이는 유럽 방위 시장에서 유지보수 위험을 줄이고 배치를 가속화하고 있습니다. 육군의 지속적인 점유율과 해군의 성장 추세는 육상 회랑과 해상 요충지에서 억지력을 지원하는 포트폴리오의 재조정을 강조하고 있습니다.

2025년 유럽 방위 시장에서 차량 부문은 48.85%를 차지했으며, 주력 전차 갱신, 보병 전투차 조달, 자주포 프로그램 등이 이를 뒷받침했습니다. 다층 방공 시스템 및 통합 화력 시스템에 대한 주문은 계속해서 지상 전투 시스템을 보완하고 있으며, 유럽 방위 시장 전체에서 공급업체는 센서와 이펙터를 디지털 지휘 네트워크에 통합하고 있습니다. 드론 군단, UAS(무인항공기 시스템), 회전식 이펙터가 전술적 우위를 재구축하고 표적 포착 주기를 단축하는 가운데, 무인 시스템은 CAGR 7.12%로 가장 빠르게 성장할 것으로 예측됩니다. 독일이 여단급 부대를 위해 AI를 활용한 정찰 처리 시스템을 도입한 것은 자율성과 소프트웨어가 대규모 항공 위협에 대한 대응을 포함하여 작전 속도와 생존성을 어떻게 향상시킬 수 있는지를 잘 보여줍니다. 스카이레인저(Skyranger)와 같은 이동식 대공포의 주문도 유럽 방위 시장에서 신속하게 배치할 수 있고 대규모로 유지할 수 있는 물리적 대 UAS 솔루션의 필요성을 반영하고 있습니다.

탄약 및 미사일 생산은 다년간의 자금 조달의 확실성과 공장 확장으로 가속화되고 있으며, 억지력과 동맹국 지원을 위한 전략적 두께를 강화하고 있습니다. MBDA의 수주량은 2021년 이전 수준과 비교하여 2024년과 2025년에 급증하여 유럽의 방위 시장에서 다층 방공에 대한 수요와 장거리 정밀 화력에 대한 모멘텀을 보여주었습니다. 또한, 데이터 융합과 표적 선택 자동화가 우위를 결정하는 멀티 도메인 작전으로 전술이 전환됨에 따라 소프트웨어 중심의 C4ISR, 전자전(EW) 및 훈련 솔루션의 점유율이 확대되고 있습니다. 유인 시스템과 무인 시스템의 균형을 맞추기 위한 영국의 '포스 믹스(Force Mix)' 구상은 재사용 가능한 플랫폼과 소모성 이펙터를 우선시하고 있으며, 이러한 전환은 모듈성과 대량 생산을 촉진하는 것입니다. 이를 종합하면, 차량, 미사일, 자율 기술의 조합은 유럽 방위 시장에서 반복적인 업그레이드, 신속한 프로토타이핑, 플러그 앤 플레이 아키텍처를 강조하는 사이클을 강조하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe Europe defense market size is expected to grow from USD 133.54 billion in 2025 to USD 142.42 billion in 2026 and is forecasted to reach USD 194.39 billion by 2031 at a 6.42% CAGR over 2026-2031.

Expanding NATO commitments to higher, sustained defense outlays are pushing multi-year procurement pipelines and capacity investments across land, air, maritime, and space programs, reinforcing structural growth in the Europe defense market. Russia's 2024 defense budget reached USD 149 billion, equal to 7.1% of GDP, which sharpened focus on munitions production, integrated air defense, and naval deterrence in frontline and near-frontline countries. Governments are elevating resilience through common procurement frameworks and local industrialization rules that favor European content and interoperable systems across alliances. The European defense market is also seeing a shift toward network-centric concepts, where software and data integration drive battlefield advantage and create opportunities for new entrants to complement legacy primes.

Europe Defense Market Trends and Insights

NATO Defense Spending Threshold Accelerates National Budget Alignments

Allied governments are anchoring defense allocations to GDP formulas that reduce annual volatility and enable industry to plan multi-year capacity expansions in the Europe defense market. NATO members signaled a path to higher, sustained outlays beyond the longstanding 2% guidance, and all Allies continued to prioritize readiness and stockpile rebuilding in 2026 after a notable step-up in 2025. The UK has committed to reaching 2.5% of GDP by 2027, with an ambition to reach 3% in the next Parliament, which tightens the demand outlook for air power, land systems, and maritime protection. Sweden met the 2.0% benchmark in its first year of NATO membership, reinforcing the broader European pivot to territorial defense and deterrence. Germany's new Act on Accelerated Planning and Procurement, effective January 15, 2026, is designed to streamline acquisitions and give preference to interoperable, off-the-shelf European solutions that support scale efficiencies in the Europe defense market. As these measures take hold, budget automaticity is creating predictability for contractors to expand ammunition, air-defense, and C4ISR capacity without overexposure to stop-start cycles in the Europe defense market.

EU Defense Fund Incentives Boost Cross-Border R&D and Capability Programs

EU instruments are bringing together Member States and industry into larger, cross-border teams that share risk across research, development, and early procurement in the Europe defense market. The European Defence Industry Programme embeds a "Buy European" presumption that caps non-EU content at 35% on common procurements and permits up to 25% EU co-funding when nations aggregate demand, which lifts participation by mid-tier suppliers and dual-use innovators. EDF and EDIP create incentives for at least three entities from three countries to collaborate, accelerating technology transfer between primes and software-centric suppliers across sensors, AI, and counter-UAS. The Commission's Defence Readiness Roadmap, published in October 2025, outlined a pathway to scale defense and space within the post-2027 budget framework, signaling durable institutional support for the Europe defense market. As these mechanisms mature, common standards and pooled logistics are likely to compress unit costs and reduce fragmentation in key product lines. This architecture encourages suppliers to invest in modular designs and digital engineering that meet both national requirements and joint European specifications.

Budget Constraints Due to Competing Energy Transition Priorities

Member States are balancing a multi-year rearmament push with the financing demands of the energy transition, keeping budget trade-offs in focus in the Europe defense market. REPowerEU requires significant additional public and private investment through 2027, and compliance costs for carbon-intensive inputs continue to influence production economics for heavy industry. Italy's 2026 defense allocation stands at EUR 31.3 billion (USD 36.83 billion), around 1.2% of GDP, according to European Commission projections, underscoring fiscal constraints in Southern Europe. EU fiscal rules have been adapted to improve flexibility, but national deficit procedures still limit the speed at which some countries can lift spending to alliance targets. Where governments have created special funds or procurement fast-tracks, execution remains the key variable that determines industrial throughput in the Europe defense market. Over the medium term, the pacing challenge is to lock in stable defense cash flows without crowding out energy transition priorities in already tight budgets.

Other drivers and restraints analyzed in the detailed report include:

- Russia-Ukraine Conflict Intensifies Defense Preparedness and Threat Awareness

- Adoption of Multi-Domain Operations Reshapes European Force Planning

- Supply Chain Disruptions in Energetic Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Army held 42.67% of the Europe defense market share in 2025, reflecting the renewed emphasis on territorial defense, integrated air and missile defense, and mechanized formations. This share aligns with the shift toward higher readiness levels and deeper munitions and spares stocks across European land forces. The Navy is projected to expand the fastest at 7.67% CAGR through 2031, supported by Baltic and North Atlantic initiatives that prioritize anti-submarine warfare, surface combatants, and maritime domain awareness. Cross-domain integration is also lifting demand for maritime ISR and command-and-control nodes that connect naval assets with joint fires networks in the Europe defense market. Kongsberg's December 2025 agreements to provide combat-system elements and navigation systems for German and Norwegian 212CD submarines illustrate momentum in undersea capabilities and industry partnerships.

Across air forces, upgrades continue on sensors, electronic warfare, and air policing, while planning for next-generation combat air emphasizes sovereign data pipelines and joint effectors. Exercises such as Dynamic Front 25 validate coalition fire coordination and logistics at scale, reinforcing procurement of interoperable radios, data links, and software-defined capabilities in the Europe defense market. Naval modernization goals are drawing attention to shipyards able to deliver on time with proven systems integration, a factor that is consolidating orders with vendors demonstrating reliable execution. Interoperability within NATO is driving purchases of munitions and communications that meet standardized standards, reducing sustainment risk and accelerating fielding in the Europe defense market. The Army's enduring share and the Navy's growth profile underscore a portfolio rebalancing that supports deterrence across land corridors and maritime chokepoints.

Vehicles captured 48.85% of the European defense market in 2025, underpinned by main battle tank recapitalization, infantry fighting vehicle procurement, and self-propelled artillery programs. Orders for layered air defense and integrated firepower continue to complement ground combat systems, with suppliers integrating sensors and effectors into digital command networks across the European defense market. Unmanned systems are forecast to grow the fastest, at a 7.12% CAGR, as drone swarms, counter-UAS, and loitering effectors reshape the tactical edge and compress the targeting cycle. Germany's rollout of AI-enabled reconnaissance processing for brigade-level formations highlights how autonomy and software lift operational tempo and survivability, including against massed aerial threats. Orders for mobile air-defense cannons such as Skyranger also reflect the urgency of kinetic counter-UAS solutions that can be fielded fast and sustained at scale in the Europe defense market.

Munitions and missile production are accelerating with multi-year funding visibility and factory expansions, reinforcing strategic depth for deterrence and allied support. MBDA's intake surged in 2024 and 2025 versus pre-2021 levels, signaling multi-layer air-defense demand and long-range precision fires momentum in the Europe defense market. Software-centric C4ISR, EW, and training solutions are also gaining share as doctrine moves toward multi-domain operations where data fusion and targeting automation define advantage. The United Kingdom's force-mix concept, which balances crewed and uncrewed systems, prioritizes reusable platforms and consumable effectors, a shift that favors modularity and high-volume production. Taken together, the mix of vehicles, missiles, and autonomy underscores a cycle favoring iterative upgrades, rapid prototyping, and plug-and-play architectures in the Europe defense market.

The Europe Defense Market Report is Segmented by Armed Forces (Air Force, Army, and Navy), Type (Personnel Training and Protection, Vehicles, Weapons and Ammunition, Unmanned Systems, and More), Domain (Land, Air, Naval, and More), Procurement Nature (Indigenous Production and Foreign Procurement), and Geography (United Kingdom, Germany, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Airbus SE

- BAE Systems plc

- Leonardo S.p.A.

- Thales Group

- Rheinmetall AG

- Saab AB

- KNDS N.V.

- Dassault Aviation S.A.

- MBDA

- Rolls-Royce Holdings plc

- HENSOLDT AG

- Diehl Stiftung & Co. KG (Diehl Group)

- Kongsberg Gruppen ASA

- Elbit Systems Ltd.

- L3Harris Technologies, Inc.

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

- United Aircraft Corporation (UAC)

- Ukroboronprom

- thyssenkrupp AG

- General Atomics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NATO defense spending threshold accelerates national budget alignments

- 4.2.2 EU defense fund incentives boost cross-border R&D and capability programs

- 4.2.3 Russia-Ukraine conflict intensifies defense preparedness and threat awareness

- 4.2.4 Adoption of multi-domain operations reshapes European force planning

- 4.2.5 Rapid prototyping pathways (EDIDP, ASAP)

- 4.2.6 Sovereign missile defense development gains traction through initiatives like Sky Shield

- 4.3 Market Restraints

- 4.3.1 Budget constraints due to competing energy transition priorities

- 4.3.2 Supply chain disruptions in energetic materials

- 4.3.3 Inconsistent export licensing policies across EU member states

- 4.3.4 Limited availability of skilled labor for systems integration

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Armed Forces

- 5.1.1 Air Force

- 5.1.2 Army

- 5.1.3 Navy

- 5.2 By Type

- 5.2.1 Personnel Training and Protection

- 5.2.2 C4ISR and Electronic Warfare

- 5.2.3 Vehicles

- 5.2.4 Weapons and Ammunition

- 5.2.5 Unmanned Systems

- 5.2.6 Space and Cyber Systems

- 5.3 By Domain

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Cyber and Electromagnetic Spectrum

- 5.4 By Procurement Nature

- 5.4.1 Indigenous Production

- 5.4.2 Foreign Procurement

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Sweden

- 5.5.7 Poland

- 5.5.8 Netherlands

- 5.5.9 Norway

- 5.5.10 Russia

- 5.5.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 BAE Systems plc

- 6.4.3 Leonardo S.p.A.

- 6.4.4 Thales Group

- 6.4.5 Rheinmetall AG

- 6.4.6 Saab AB

- 6.4.7 KNDS N.V.

- 6.4.8 Dassault Aviation S.A.

- 6.4.9 MBDA

- 6.4.10 Rolls-Royce Holdings plc

- 6.4.11 HENSOLDT AG

- 6.4.12 Diehl Stiftung & Co. KG (Diehl Group)

- 6.4.13 Kongsberg Gruppen ASA

- 6.4.14 Elbit Systems Ltd.

- 6.4.15 L3Harris Technologies, Inc.

- 6.4.16 RTX Corporation

- 6.4.17 Lockheed Martin Corporation

- 6.4.18 Northrop Grumman Corporation

- 6.4.19 General Dynamics Corporation

- 6.4.20 United Aircraft Corporation (UAC)

- 6.4.21 Ukroboronprom

- 6.4.22 thyssenkrupp AG

- 6.4.23 General Atomics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment