|

시장보고서

상품코드

2043889

공항 보안 검색 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Airport Security Screening Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

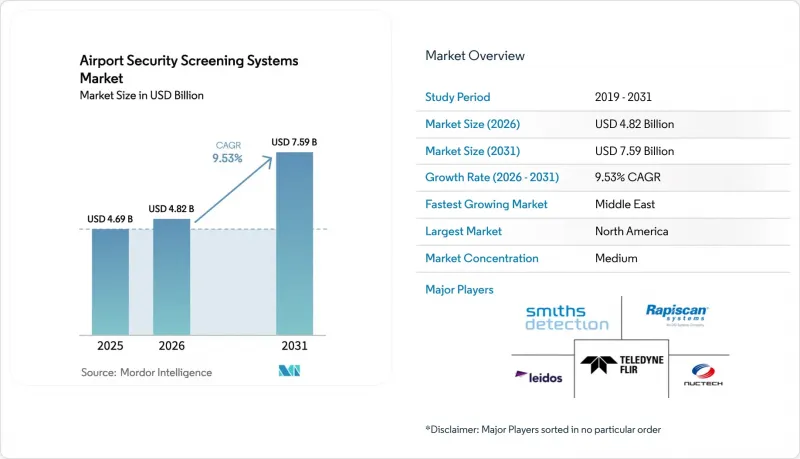

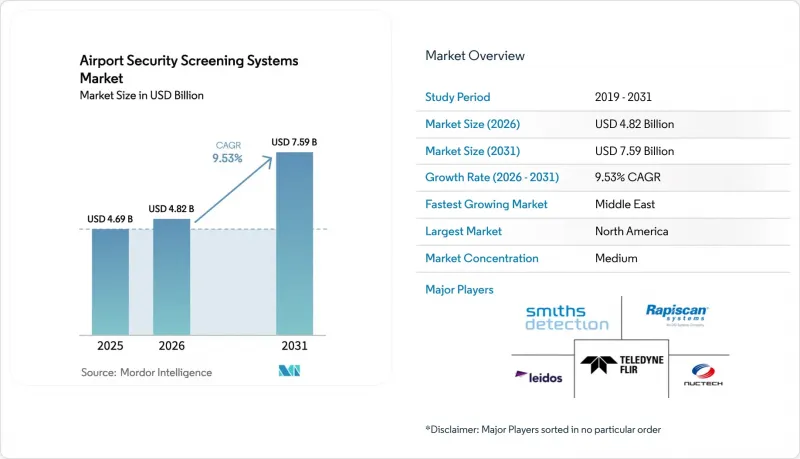

공항 보안 검색 시스템 시장 규모는 2025년 46억 9,000만 달러로 평가되었습니다. 2026년 48억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 9.53%를 나타내, 2031년에는 75억 9,000만 달러에 이를 것으로 예측됩니다.

공항에서는 제한된 부지 확장과 장기화되는 항공기 인도 지연 속에서 사상 최대 여객 수를 처리하고 있어, 시장은 사후 대응형 검색대 운영에서 예측형 및 AI를 활용한 스크리닝으로 전환하고 있습니다. 현재 처리 능력의 최적화는 수작업으로 수하물을 꺼내지 않아도 되고 재검사를 줄일 수 있는 컴퓨터 단층촬영(CT) 스캐너와 자동 레인 등을 중심으로 이루어지고 있으며, 대규모 기존 시설 전체에 대한 소프트웨어 중심의 업그레이드 필요성이 높아지고 있습니다. 미국과 유럽의 규제 요건으로 인해 CT 도입과 생체인증을 통한 신원 확인이 조달 로드맵에 포함되면서 북미와 유럽에서 단기적으로 수요가 집중되는 한편, 개방형 아키텍처 표준에 기반한 소프트웨어의 상호운용성이 가속화되고 있습니다. 생산 제약으로 인해 신규 하드웨어 도입 속도가 조절되는 가운데, 벤더의 전략은 지속적인 소프트웨어 및 유지보수 수익에 점점 더 많은 비중을 두고 있습니다.

세계의 공항 보안 검색 시스템 시장 동향과 인사이트

코로나19 이후 회복세에 따른 전 세계 항공 여객 수 급증

2025년 연간 총 수요(여객 킬로미터(RPK) 기준)는 2024년 대비 5.3% 증가했습니다. 총 공급 능력(가용 좌석 킬로미터(ASK) 기준)은 2025년 5.2% 증가했습니다. IATA의 데이터에 따르면, 수요 모멘텀은 지역에 따라 다르며 아시아태평양이 주도하는 반면 북미는 완만한 추세를 보이고 있으며, 이는 스크리닝 능력의 도입 우선순위를 형성하고 있습니다. 공항에서는 CT(컴퓨터 단층촬영)를 이용한 수하물 스캔과 자동 레인 도입으로 전자기기와 액체류 반출을 불필요하게 함으로써 수속 절차를 줄이고 레인 처리 능력을 안정화시키고 있습니다. 터미널의 확장이 지연되는 경우, 운영사는 알고리즘 개선과 원격 분석 센터를 활용하여 물리적 공간을 늘리지 않고도 유효 용량을 향상시키고 있습니다. 그 결과, 피크 부하 시 의사결정을 효율화하는 CT, 신원인증, 그리고 오픈 아키텍처 소프트웨어에 대한 지속적인 투자가 이루어지고 있습니다.

증가하는 테러 위협과 규제 요건

미국의 규정 개정으로 인해 항공화물 검사에 대한 기술적 요구 사항이 더욱 엄격해졌습니다. 최신 ACSTL(항공화물 검사 기술기준)에서는 CT 기반 EDS(전자검출시스템) 기준이 강화되어 기존의 시각적 영상장비의 폐지 시기가 설정되어 있습니다. 유럽에서는 2025년 10월부터 출입국 관리 시스템이 가동되기 시작했습니다. 2026년 4월까지 EU 역외 국적자 전원을 대상으로 전면 도입될 예정이며, 국경에서의 생체 인식 등록이 의무화되어 키오스크 단말기 및 데이터 보안 대책에 대한 투자가 증가하고 있습니다. EES의 워크플로우에는 승객의 흐름에 신원 확인이 내장되어 있으며, 이로 인해 심사대와 국경 관리 시스템 사이에 검문소를 통합할 필요성이 높아지고 있습니다. 미국에서는 최종 규칙에 따라 공항, 항구, 육로 국경 검문소에서 출국하는 외국인의 생체정보 수집이 확대되었고, 이에 따라 관련 인프라의 설치 범위가 터미널 내로 확대되었습니다. 이러한 조치는 "프라이버시 바이 디자인"의 요구 사항에 따라 EDS, CT 및 생체 인식의 통합에 대한 지속적인 수요 패턴을 창출하고 있습니다.

고가의 설비 투자 및 장기간의 조달 주기

풀 사이즈 CT 장비는 이전 세대의 듀얼 뷰 시스템보다 고가이며, 자본 계획에 제약이 있는 공항의 경우 초기 예산 부담이 증가합니다. 많은 운영자들은 수명을 연장하고 전체 교체를 미루기 위해 리노베이션 키트나 알고리즘 업그레이드로 대응하고 있으며, 단기적인 지출을 소프트웨어와 유지보수로 전환하고 있습니다. 다년간의 물류 계약은 대규모 항공기군에 대한 가동률 향상과 라이프사이클 지원의 필요성을 강조하고 있으며, 이는 도입 일정을 더욱 복잡하게 만들고 있습니다. 유럽에서는 여러 공항을 대상으로 한 프로그램에서 레인 개조 및 직원 인증이 단계적으로 진행되어 CT 도입이 수년에 걸쳐 단계적으로 이루어지고 있습니다. 이러한 요인으로 인해 규제상의 기한이 설정되어 있는 경우에도 조달 주기 및 설치 기간이 길어지고 있습니다.

부문 분석

수하물 및 위탁 수하물 검사는 2025년 매출의 62.36%를 차지했으며, 인라인 EDS 의무화 및 전자 수하물 검사 프로그램에 대한 다년간의 자금 지원으로 뒷받침되었습니다. 이 하위 부문은 토목 공사와 차선 통합이 현대화 속도를 좌우하는 지하 시설과 인라인 컨베이어에서 안정적인 업데이트 주기를 반영합니다. 공항에서는 기존 장비의 감지율을 높이고 오경보를 줄이는 알고리즘 업그레이드를 선호하고 있으며, 이를 통해 도입된 자산의 투자수익률을 향상시키고 있습니다. 여객 검사는 기술 혁신 측면에서 빠르게 발전하고 있으며, CT 수하물 스캐너와 자동 검사 레인을 통해 수작업으로 수하물을 꺼내는 과정을 없애고 시간당 처리 능력을 향상시키고 있습니다. 비접촉식 신원확인 프로그램은 신분증 인증 및 위험도 기반 선별과 결합하여 체크포인트의 효율성을 더욱 높이고 있습니다.

화물 및 차량 검사는 2031년까지 10.67%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되는 가장 높은 하위 부문으로, 전자상거래를 통한 소포 증가와 방사성 물질 식별 및 폭발물 미량 검출을 우선시하는 세관 프로그램에 힘입어 성장세를 보이고 있습니다. 미국 내 화물 검사 및 국제 도입의 경우, 턴키 계약에 기반한 포털 시스템 및 통합 트레이서 유닛을 통해 처리 용량이 확대되고 있습니다. 생산 능력의 제약으로 인해 검문소용 CT의 도입이 둔화되고 있는 가운데, 소프트웨어의 이식성과 개방형 인터페이스로 인해 각 레인 및 화물 시설 전체에 최고급 분석 기술이 보급되고 있습니다. 네트워크 전체에서 원격 판정을 조정하는 공항은 인력 배치의 효율성과 의사결정의 일관성을 확보할 수 있어 중앙집중형 해결실의 편의성을 높일 수 있습니다.

엑스레이 및 듀얼 뷰 시스템은 기존 설비의 관성 및 컨베이어와의 호환성으로 인해 2025년에도 38.67%의 점유율을 유지하였으나, 계획 기간 동안 많은 장비에서 부품의 노후화가 우려되는 상황입니다. OEM 업체들은 기존 터널형 검사기에 듀얼 에너지 분석 및 AI 기반 감지 기능을 추가하는 모듈식 키트를 통해 장비의 수명을 연장하고 있으며, 이는 CT로의 전환을 위한 비용 효율적인 교량 역할을 하고 있습니다. 유럽 검문소에서 CT의 도입이 진행되고 데이터 보호 대책이 통일됨에 따라 대규모 허브 공항의 수하물 검사에서 2차원 방식은 단계적으로 폐지될 것입니다. 듀얼 뷰 방식은 처리 능력과 비용 측면에서 여전히 높은 이점이 있는 특정 2차 검사 레인 및 대형 수하물 레인에서 계속 유용하게 사용될 수 있습니다.

컴퓨터 단층촬영(CT)은 여러 조달 프로그램으로 인해 베이직, 미드, 풀 사이즈 체크포인트 장비의 수가 증가하고, 자동 검출을 위한 소프트웨어 인증이 추진됨에 따라 CAGR 11.25%를 나타낼 것으로 예측됩니다. 각국의 자본 계획에는 생산상의 제약이 강조되고 있으며, 납품 규모가 확대되는 가운데 시스템을 계속 가동하기 위한 유지관리 비용이 할당되어 있습니다. mm파 AIT는 오경보를 줄이고 신체검사 프로세스를 효율화하는 알고리즘의 업데이트로 신체검사에서 여전히 필수적인 존재입니다. 생체 인식 게이트와 신분증 인증 시스템이 신원 확인을 대신하면서 현대화된 검사 레인에서 금속 감지기와 수동 신분증 확인의 역할은 줄어들고 있습니다.

지역별 분석

북미는 2025년 매출의 40.77%를 차지했습니다. 이는 TSA의 예산 배분으로 인해 검문소 수하물 검사, CT, 신분증 인증 프로그램 및 장기 유지관리 계약이 지원되었기 때문입니다. 여객수 회복이 세계 평균을 밑돌면서 일부 소규모 공항에서는 업그레이드의 시급성이 떨어졌지만, 대규모 허브 공항에서는 인력 부족을 보완하기 위해 생체 인식 전자 게이트와 자동 레인 도입이 진행되었습니다. 조달 및 유지보수 프로그램에서는 다양한 장비군의 가용성을 보장하기 위해 가동률, 사이버 보안, 예측 유지보수에 중점을 두었습니다. 이 지역의 태도는 미래 지향적인 투자를 보장하기 위해 소프트웨어 중심의 개선과 개방형 아키텍처 준수를 강화하는 것입니다.

유럽에서는 비EU 여행객의 생체 인식 등록을 의무화하고 데이터 보호 대책을 도입의 핵심으로 삼는 '쉥겐 출입국 관리 시스템'의 도입을 추진하는 동시에 CT 도입에 박차를 가하고 있습니다. 회원국은 다년간의 예산을 투입하여 주요 허브 공항의 차선 전환을 추진하고, 얼굴 인식 시스템 및 데이터 저장 관행에 대한 '프라이버시 바이 디자인' 요건을 통일했습니다. 개별 공항 프로젝트에서는 CT 도입, 자동 트레이 반납 시스템, 금지 물품 감지를 위한 소프트웨어 인증 AI 모듈이 결합되었습니다. 국가마다 일정은 달랐지만, 주요 허브 공항에서는 투자가 활성화된 반면, 일부 지방 공항에서는 자금 조달을 기다리며 시스템 업데이트를 연기했습니다.

중동은 2031년까지 11.87%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 이는 허브공항이 턴키 계약에 따라 CT(컴퓨터 단층촬영)를 활용한 수하물 검사 및 통합 화물 솔루션에 투자하고 있기 때문입니다. 지역 산업 정책에는 보안 검사 장비의 현지 조립, 공급망 탄력성 강화, 애프터 서비스 지원 등이 포함됩니다. 아시아태평양의 모멘텀은 DICOS 호환 데이터 교환을 활용하여 각국의 시스템을 가로지르는 원격 수하물 검사를 도입하는 허브 공항 프로젝트를 통해 환승 시간을 단축하고 중앙 집중식 심사 모델을 확대하는 데 힘입어 더욱 탄력을 받고 있습니다. 남미와 아프리카의 경우, 평균 이상의 승객 수 증가는 드물고, 예산의 제약으로 인해 개조 전략과 원격 검문소용 휴대용 추적기 감지 장비가 선호되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The airport security screening systems market size is expected to grow from USD 4.69 billion in 2025 to USD 4.82 billion in 2026 and is forecasted to reach USD 7.59 billion by 2031 at a 9.53% CAGR over 2026-2031.

The market is shifting from reactive checkpoint operations to predictive and AI-augmented screening, as airports manage record passenger volumes with limited footprint expansion and prolonged aircraft delivery backlogs. Throughput optimization now centers on computed tomography (CT) scanners and automated lanes that eliminate manual divestment and reduce re-screening, strengthening the case for software-driven upgrades across large installed bases. Regulatory mandates in the United States and Europe hardwire CT adoption and biometric identity checks into procurement roadmaps, which concentrate near-term demand in North America and Europe while accelerating software interoperability under open-architecture standards. Vendor strategies increasingly emphasize recurring software and sustainment revenues as production constraints modulate the pace of new hardware installations.

Global Airport Security Screening Systems Market Trends and Insights

Surging Global Air-Passenger Traffic Post-COVID Recovery

Total full-year demand in 2025, measured in revenue passenger kilometers (RPKs), increased by 5.3% compared to 2024. Total capacity, measured in available seat kilometers (ASK), grew by 5.2% in 2025. IATA shows demand momentum, with regional variation: Asia-Pacific leads, while North America trends slower, shaping deployment priorities for screening capacity. Airports are using CT-based carry-on scanning and automated lanes to eliminate the need to divest electronics and liquids, reducing handling steps and stabilizing lane throughput. Where terminal expansion lags, operators lean on algorithmic enhancements and remote analysis centers to lift effective capacity without physical space increases. The net effect supports sustained investment in CT, credential authentication, and open-architecture software that streamlines decisions under peak loads.

Heightened Terrorism Threat and Regulatory Mandates

Regulatory updates in the US tightened technology qualification for air-cargo screening, with the latest ACSTL versions advancing CT-based EDS standards and scheduling sunset dates for legacy visual image devices. In Europe, the Entry/Exit System went live in October 2025. It will be fully deployed by April 2026 for all non-EU nationals, mandating biometric enrollment at external borders and increasing investments in kiosks and data security controls. The EES workflow embeds identity checks into the passenger flow, which raises the case for integrating checkpoints between screening lanes and border-control systems. In the US, a final rule expanded biometric collection for departing aliens across airports, seaports, and land crossings, thereby extending the relevant infrastructure footprint into terminals. These measures set sustained demand patterns for EDS, CT, and biometric integration under privacy-by-design mandates.

High Capex and Long Procurement Cycles

Full-size CT units cost more than earlier-generation dual-view systems, which elevates upfront budgets for airports with constrained capital plans. Many operators respond with retrofit kits and algorithm upgrades that extend the useful life and defer full replacements, shifting near-term spending to software and sustainment. Multi-year logistics contracts underscore the need for higher uptime and lifecycle support for large fleets, which further complicates deployment calendars. In Europe, multi-airport programs phase CT adoption over several years as lane conversions and staff certifications proceed in waves. These factors lengthen procurement cycles and space installation windows even where regulatory deadlines are in place.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Transition from 2D X-ray to CT Scanners in US and EU Airports

- Adoption of AI-Powered Automated Threat Recognition

- Privacy and Health Concerns Over Advanced Imaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Baggage and hold-luggage screening accounted for 62.36% of 2025 revenues, underpinned by inline EDS mandates and multi-year funding for the Electronic Baggage Screening Program. This subsegment reflects a stable replacement cycle in basements and inline conveyors, where civil works and lane integration pace modernization. Airports favor algorithmic upgrades that increase detection and reduce false alarms on existing machines, which raises the return on installed assets. Passenger screening is advancing rapidly in terms of innovation, as CT carry-on scanners and automated screening lanes increase hourly throughput while eliminating manual divestment steps. Touchless identity programs further streamline checkpoints when combined with credential authentication and risk-based screening.

Cargo and vehicle screening is the fastest subsegment with a 10.67% CAGR through 2031, supported by e-commerce parcel growth and customs programs that prioritize radiation identification and explosives trace detection. US cargo-screening and international deployments add capacity through portal systems and integrated trace units under turnkey contracts. As production limits slow checkpoint CT rollouts, software portability and open interfaces enable best-of-breed analytics to spread across lanes and cargo facilities. Airports that coordinate remote adjudication across networks gain staffing leverage and decision-making consistency, thereby increasing the appeal of centralized resolution rooms.

X-ray and dual-view systems retained a 38.67% share in 2025 due to installed-base inertia and conveyor compatibility, yet many units face parts obsolescence over the plan period. OEMs extend life through modular kits that add dual-energy analysis and AI-based detection to legacy tunnels, which provides a cost-effective bridge to CT. As European checkpoints phase in CT and align data safeguards, the 2-D approach sunsets in carry-on applications at large hubs. Dual-view retains utility in specific secondary or oversize lanes where throughput and cost profiles remain favorable.

Computed tomography (CT) is projected to grow at a 11.25% CAGR as multi-award programs expand the number of base-, mid-, and full-size checkpoint units and drive software certification for automated detection. National capital plans highlight production constraints and allocate spending for sustainment to keep systems operational as deliveries scale. Millimeter-wave AIT remains critical for on-person screening with algorithm updates that reduce false alarms and streamline the pat-down process. As biometric e-gates and credential authentication systems take over identity checks, metal detectors and manual ID verification play reduced roles inside modernized lanes.

The Airport Security Screening Systems Market Report is Segmented by Screening Type (Passenger Screening, and More), Technology (X-Ray Screening Systems, Computed Tomography, and More), Installation (New and Upgrade), Airport Size (Large, Medium, and Small), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.77% of 2025 revenues, as TSA appropriations supported checkpoint property screening, CT, and credential authentication programs, as well as a long-term sustainment contract. Passenger traffic recovery trailed global averages, compressing upgrade urgency at some smaller airports, while large hubs advanced biometric e-gates and automated lanes to offset staffing pressure. Procurement and sustainment programs maintained focus on uptime, cybersecurity, and predictive maintenance to ensure availability across a diverse fleet. The region's posture reinforces software-centric improvements and open-architecture compliance to future-proof investments.

Europe accelerated CT adoption while implementing the Schengen Entry/Exit System, which requires biometric enrollment for non-EU travelers and places data-protection controls at the core of deployments. Member states moved on lane conversions at large hubs with multi-year budgets and aligned privacy-by-design requirements for facial recognition systems and storage practices. Individual airport projects combined CT installations, automated tray return systems, and software-certified AI modules for prohibited-item detection. National timelines varied, but investment intensity rose at primary hubs while some regional airports deferred conversions pending funding.

The Middle East is set to be the fastest-growing region, with a 11.87% CAGR through 2031, as hubs invest in CT-based carry-on screening and integrated cargo solutions under turnkey contracts. Regional industrial policy includes local assembly of security screening equipment, strengthening supply resilience, and after-sales support. Asia-Pacific momentum is reinforced by hub projects that implement remote baggage screening across sovereign systems using DICOS-compliant data exchange, reducing connection times and extending centralized adjudication models. South America and Africa rarely experience above-average traffic growth, and budget constraints favor retrofit strategies and portable trace detection for remote checkpoints.

- Smiths Detection Group Ltd.

- Rapiscan Systems, Inc. (OSI Systems, Inc.)

- Leidos, Inc.

- Nuctech Company Limited

- Teledyne FLIR LLC

- Autoclear LLC

- Costruzioni Elettroniche Industriali Automatismi S.p.A.

- Chemring Group PLC

- Garrett Electronics Inc.

- Analogic Corporation

- Rohde & Schwarz GmbH & Co. KG

- ICTS Europe S.A

- Vanderlande Industries B.V.

- Westminster Group Plc

- VMI Security

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global air-passenger traffic post-COVID recovery

- 4.2.2 Heightened terrorism threat and regulatory mandates (e.g., TSA ACSTL updates)

- 4.2.3 Mandatory transition from 2D X-ray to CT scanners in US and EU airports

- 4.2.4 Adoption of AI-powered automated threat recognition to cut queue times

- 4.2.5 Shift to contact-less biometric screening for hygiene and throughput gains

- 4.2.6 Demand for centralized remote image analysis to optimise screener staffing

- 4.3 Market Restraints

- 4.3.1 High capex and long procurement cycles for CT and MMW equipment

- 4.3.2 Privacy and health concerns over advanced imaging/biometric data storage

- 4.3.3 Semiconductor and detector-grade crystal supply constraints delaying roll-outs

- 4.3.4 Labor-union push-back against job loss from full-automation of lanes

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Screening Type

- 5.1.1 Passenger Screening

- 5.1.2 Baggage and Hold-Luggage Screening

- 5.1.3 Cargo and Vehicle Screening

- 5.2 By Technology

- 5.2.1 X-Ray Screening Systems

- 5.2.2 Computed Tomography (CT)

- 5.2.3 Millimeter-Wave and Advanced Imaging Technology (AIT)

- 5.2.4 Metal Detectors

- 5.2.5 Explosives Trace Detection (ETD)

- 5.2.6 Biometric Screening

- 5.3 By Installation

- 5.3.1 New Installation

- 5.3.2 Upgrade

- 5.4 By Airport Size

- 5.4.1 Large (Greater than 30 million passengers per annum)

- 5.4.2 Medium (10 to 29 million passengers per annum)

- 5.4.3 Small (Less than 10 million passengers per annum)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smiths Detection Group Ltd.

- 6.4.2 Rapiscan Systems, Inc. (OSI Systems, Inc.)

- 6.4.3 Leidos, Inc.

- 6.4.4 Nuctech Company Limited

- 6.4.5 Teledyne FLIR LLC

- 6.4.6 Autoclear LLC

- 6.4.7 Costruzioni Elettroniche Industriali Automatismi S.p.A.

- 6.4.8 Chemring Group PLC

- 6.4.9 Garrett Electronics Inc.

- 6.4.10 Analogic Corporation

- 6.4.11 Rohde & Schwarz GmbH & Co. KG

- 6.4.12 ICTS Europe S.A

- 6.4.13 Vanderlande Industries B.V.

- 6.4.14 Westminster Group Plc

- 6.4.15 VMI Security

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment