|

시장보고서

상품코드

2043891

아시아태평양의 인슈어테크 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Insurtech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

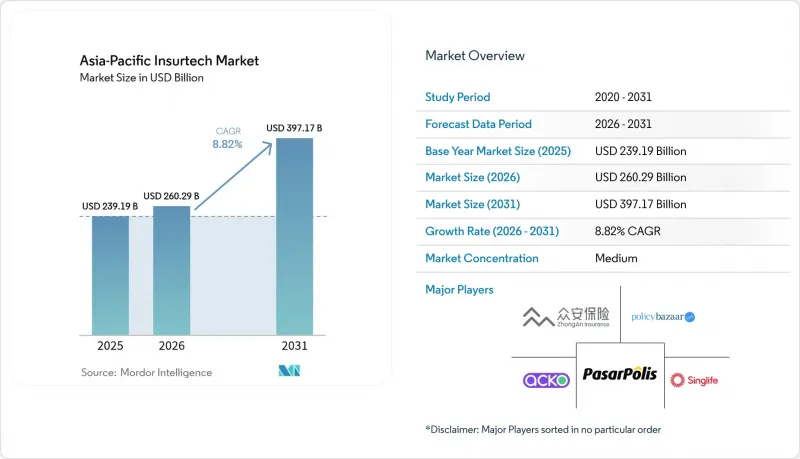

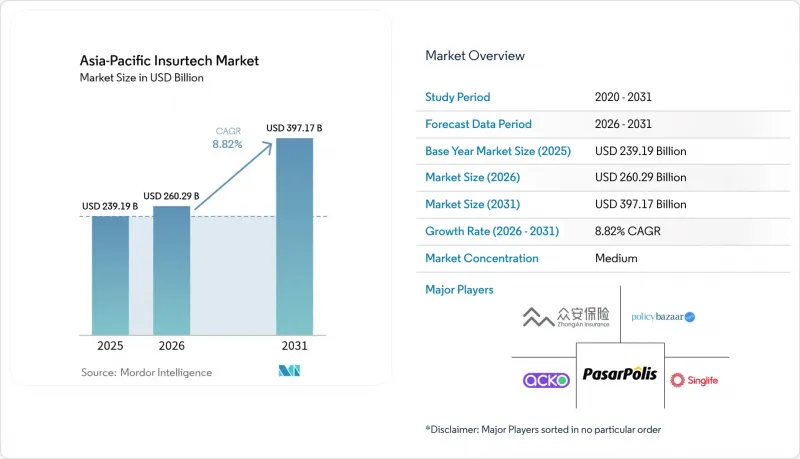

아시아태평양의 인슈어테크 시장 규모는 2025년 2,391억 9,000만 달러로 평가되었습니다. 2026년 2,602억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 8.82%를 나타내, 2031년에는 3,971억 7,000만 달러에 이를 것으로 예측됩니다.

이러한 성장의 배경에는 스마트폰을 중심으로 한 판매 채널의 경제성, 규제 샌드박스의 가속화, 그리고 인수 정확도 향상과 보험금 지급 자동화를 가능하게 하는 고급 분석 기술의 활용이 있습니다. 임베디드 보험 생태계는 그동안 도달할 수 없었던 개인고객과 중소기업(SME)을 확실하게 확보하는 한편, 아세안 역내 국경 간 규제 조화로 인해 여러 시장에 대응하는 플랫폼의 진입장벽이 낮아지고 있습니다. 모바일을 통한 고객 확보 비용 감소, 특수 위험에 대한 인식 증가, 파라메트릭 보험 솔루션에 대한 새로운 자본의 유입은 아시아태평양의 인슈어테크 시장의 상승 여력을 더욱 강화시키고 있습니다. AI를 활용한 인수 심사가 기존의 손해율 우위를 약화시키고, 기존 기업들이 핀테크 기업과의 전략적 제휴를 추진함에 따라 경쟁 환경은 여전히 유동적입니다.

아시아태평양의 인슈어테크 시장 동향과 인사이트

임베디드 보험 생태계의 부상

임베디드 플랫폼은 일상적인 구매 프로세스 내에 보험을 내장하여 사용자가 호스트 앱을 떠나지 않고도 보험을 구매할 수 있도록 합니다. 이 원활한 흐름은 대리점을 통한 마찰을 없애고, 고객 확보 비용을 최대 40%까지 절감할 수 있습니다. 이러한 비용 절감은 대규모 배치에서 단위당 수익성을 향상시킵니다. 앤트그룹과 알리바바의 제휴는 전자상거래, 여행, 지갑 거래에서 보험료를 창출하는 이 모델의 확장성을 보여주고 있습니다. 싱가포르의 명확한 API 가이드라인을 통해 비보험사도 기존 핀테크 라이선스에 따라 상품을 판매할 수 있어 컴플라이언스 부담을 낮출 수 있습니다. 여러 접점에서의 참여도 향상은 행동 데이터를 언더라이팅 부서에 피드백하여 가격 설정의 정확도를 높이고 손해율을 낮출 수 있습니다. 이러한 네트워크 효과로 인해 임베디드 보험은 아시아태평양의 인슈어테크 시장의 구조적 성장 동력으로 자리매김하고 있습니다.

아시아태평양의 사이버 위험 노출 급증

디지털 전환으로 의료, 금융, 제조 등 공격 대상 영역이 확대되면서 사이버 보험에 대한 수요가 급증하고 있습니다. 싱가포르의 2024년 AI 모델 리스크 관리 규정은 금융회사에 강력한 관리 체계의 증명을 요구하고 있으며, 이에 따라 구매자는 컴플라이언스를 문서화한 보험 계약을 요구하고 있습니다. 인슈어테크 기업들은 이에 대응해 다운타임 분수 등 지표에 따라 자동으로 보험금이 지급되는 파라메트릭형 사이버 보험 상품을 출시해 장기간에 걸친 조사를 피하고 있습니다. 실시간 가격 책정 엔진은 위협 인텔리전스 피드와 취약점 스캔을 통합하여, 인수 담당자가 각 고객의 보안 태세에 맞게 보험료를 책정할 수 있도록 지원합니다. 하이퍼스케일 제공업체들이 지역 거점을 확장함에 따라 클라우드 집중화 리스크가 증가하면서 맞춤형 보험 계약에 대한 수요가 급증하고 있습니다. 이러한 요인들이 복합적으로 작용하여 사이버 보험의 보급률은 증가하고 있지만, 민첩한 신규 진출기업에게는 충분한 보호의 공백이 남아있습니다.

관할권별 데이터 프라이버시 규정의 파편화 현상

아시아태평양의 규제 당국은 각각 고유한 동의, 저장 및 전송 관련 규정을 적용하고 있으며, 인슈어테크 기업들은 각 시장마다 별도의 데이터 스택을 구축해야 합니다. 컴플라이언스 팀은 싱가포르의 PDPA, 인도의 디지털 개인정보 보호법, 중국의 사이버 보안법을 숙지해야 하며, 그 결과 단일 시장을 대상으로 하는 동종업계에 비해 25-35% 더 높은 비용을 부담하고 있습니다. 이러한 분절은 파트너와의 실시간 데이터 공유가 거주지 규정에 저촉될 수 있기 때문에 임베디드 보험의 확산을 지연시키고 있습니다. 한 관할권의 가장 엄격한 요건이 모든 공유 데이터에 적용될 경우, 재보험사는 국경을 초월한 리스크 풀링에 어려움을 겪을 수 있습니다. 정부가 단기간의 통지를 통해 조항을 강화하거나 완화하는 등 지속적인 변화로 인해 불확실성이 더욱 커지고 있습니다. 이로 인한 복잡성은 제품 개발에서 자본을 분산시켜 아시아태평양의 인슈어테크 시장의 지역적 확장을 제약하고 있습니다.

부문 분석

손해보험은 2025년 보험료의 40.62%를 차지하며 아시아태평양의 인슈어테크 시장 점유율의 가장 큰 비중을 차지했습니다. 안정적인 보험금 청구 패턴, 다년간의 규제에 대한 숙련도, 그리고 고도로 디지털화된 자동차 보험 및 가정 보험이 이러한 우위를 뒷받침하고 있습니다. 그러나 가격 경쟁의 심화 및 대형 재해로 인한 손실이 인수 마진을 압박하고 있어 성장세가 둔화되고 있습니다. 반면, 특수보험 분야는 CAGR 9.86%로 성장하고 있으며, 사이버 보험, 반려동물 보험, 여행자 보험이 기업 및 소비자 부문에서 인지도가 높아짐에 따라 아시아태평양의 인슈어테크 시장 규모에 대한 기여도가 매년 증가하고 있습니다. 필리핀과 피지에서의 파라메트릭 사이클론 보험 시범 사업은 신속한 지급이 가능한 상품이 오랜 기간 동안 보장 공백을 메우고 다국적 기부자 자금을 유치할 수 있다는 것을 보여주며, 특수 보험사에게 사회적 의미와 수익성 높은 규모를 모두 가져다주었습니다. 사회적 의미와 수익성을 모두 가져왔습니다.

랜섬웨어로 인한 비용 증가에 따라 사이버보험은 여전히 전문 분야로 주목받고 있지만, 보험계리상의 얇은 이익이 재보험 부보 기준금액을 높게 유지하여 단기적인 보급을 억제하고 있습니다. 인슈어테크 기업들은 위협 인텔리전스 피드, 엔드포인트 텔레메트리, 클라우드 서비스 가동률 지표를 융합하여 보안이 잘 갖춰진 기업에는 보험료를 낮게 책정하는 동적 인수 모델을 구축하여 데이터 부족을 해소하고 있습니다. 반려동물 보험도 비슷한 데이터 기반의 궤적을 밟고 있으며, 원격진료 서비스를 통해 지속적인 행동 정보를 제공함으로써 가격 책정의 정확성을 높이고 있습니다. 해상 및 내륙 운송 보험은 위성 화물 추적을 통해 항해 중단 시 파라메트릭 보험금을 자동으로 지급하여 수출업체의 번거로운 보험금 청구 절차를 간소화합니다. 이러한 혁신이 결합되어 평균 보험료 성장률이 시장 기준선을 크게 상회하면서 스페셜티 라인은 아시아태평양의 인슈어테크 시장에서 장기적으로 주요한 가치 창출 엔진으로 자리매김하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 백만 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Asia-Pacific Insurtech Market size is expected to grow from USD 239.19 billion in 2025 to USD 260.29 billion in 2026 and is forecast to reach USD 397.17 billion by 2031 at 8.82% CAGR over 2026-2031.

This resilient growth is rooted in smartphone-first distribution economics, regulatory sandbox acceleration, and the use of advanced analytics that enhance underwriting precision and claims automation. Embedded-insurance ecosystems now secure previously unreachable retail and SME customers, while cross-border regulatory harmonization inside ASEAN lowers entry barriers for multi-market platforms. Falling mobile-acquisition costs, a surge in specialty-risk awareness, and fresh capital flowing into parametric solutions further reinforce the upside for the Asia-Pacific insurtech market. Competitive dynamics remain fluid as AI-enabled underwriting erodes traditional loss-ratio advantages and encourages incumbents to form strategic alliances with fintechs.

Asia-Pacific Insurtech Market Trends and Insights

Rise of Embedded-Insurance Ecosystems

Embedded platforms place cover inside everyday purchase journeys, letting users buy protection without leaving the host app. This seamless flow removes agent friction and cuts acquisition costs by up to 40%, a saving that improves unit economics at scale. Ant Group's partnership with Alibaba shows the model's reach as premiums emerge from e-commerce, travel, and wallet transactions. Singapore's clear API guidelines allow non-insurers to distribute products under existing fintech licenses, keeping compliance overhead low. Higher engagement across multiple touchpoints feeds behavioral data back to underwriters, raising pricing accuracy and lowering loss ratios. These network effects reinforce adoption, positioning embedded insurance as a structural growth engine for the Asia-Pacific insurtech market.

Sharp Increase in Asia-Pacific Cyber-Risk Exposure

Digital transformation widens attack surfaces across health care, finance, and manufacturing, driving urgent demand for cyber cover. Singapore's 2024 AI Model Risk Management rules compel financial firms to prove robust controls, pushing buyers toward policies that document compliance. Insurtechs respond with parametric cyber products that pay automatically on metrics like downtime minutes, avoiding long investigations. Real-time pricing engines ingest threat-intel feeds and vulnerability scans, letting underwriters match premiums to each client's security posture. Cloud concentration risk grows as hyperscale providers expand regional centers, adding urgency for bespoke policies. Together, these forces raise cyber insurance penetration yet leave ample protection gaps for agile entrants.

Persistent Data-Privacy Fragmentation by Jurisdiction

APAC regulators each impose unique consent, storage, and transfer rules, forcing insurtechs to build separate data stacks for every market. Compliance teams must master Singapore's PDPA, India's Digital Personal Data Protection Act, and China's Cybersecurity Law, driving costs 25-35% higher than single-market peers. Fragmentation slows embedded-insurance rollouts because real-time data sharing with partners may breach residency rules. Reinsurers struggle to pool risks across borders when one jurisdiction's strictest requirement governs all shared data. Ongoing changes add further uncertainty as governments tighten or relax clauses with short notice. The resulting complexity diverts capital from product development and constrains the Asia-Pacific insurtech market's regional scaling.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone-First Customer Acquisition Costs Falling

- Sandbox-Style Regulatory Fast-Tracks Across Asia-Pacific

- Thin Actuarial Loss Histories for New-Risk Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Property & Casualty retained 40.62% of 2025 premiums, giving it the largest slice of the Asia-Pacific insurtech market share. Stable claim patterns, long-standing regulatory familiarity, and highly digitized motor and household lines underpin this dominance, yet growth momentum is slowing as pricing competition intensifies and catastrophe losses pressure underwriting margins. Specialty Lines, in contrast, are expanding at a 9.86% CAGR, lifting their contribution to the Asia-Pacific insurtech market size year after year as cyber, pet, and travel covers gain recognition across corporate and consumer segments. Parametric cyclone pilots in the Philippines and Fiji illustrate how rapid-payout products can fill long-standing protection gaps and attract multilateral donor funding, giving specialty carriers both social relevance and profitable scale.

Cyber insurance remains the specialty headline as ransomware costs rise, yet actuarial thinness keeps reinsurance attachment points high, tempering near-term penetration. Insurtechs mitigate data scarcity by fusing threat-intelligence feeds, endpoint telemetry, and cloud-service uptime metrics into dynamic underwriting models that reward strong security hygiene with lower premiums. Pet insurance follows a similar data-rich trajectory as tele-vet usage supplies continuous behavioral information that sharpens pricing. Marine and inland transit lines leverage satellite cargo tracking to trigger parametric payouts for voyage disruptions, cutting claims friction for exporters. Together, these innovations lift average premium growth well above the market baseline, positioning Specialty Lines as the primary long-run value engine of the Asia-Pacific insurtech market.

The Asia-Pacific Insurtech Market Report is Segmented by Product Line (Life Insurance, Health Insurance, Property & Casualty, Specialty Lines), Distribution Channel (Direct-To-Consumer Digital, Aggregators/Marketplaces, and More), End User (Retail/Individual, SME/Commercial, and More), and Geography (India, China, Japan, Australia, South Korea, South-East Asia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ZhongAn

- Policybazaar

- Acko

- PasarPolis

- Singlife

- OneDegree

- CXA Group

- Waterdrop

- Koala

- CoverGo

- Bolttech

- Shift Technology

- CarDekho (Insurance arm)

- Turtlemint

- Tokio Marine & Nichido (Digital Lab)

- Ping An OneConnect

- Munich Re Digital Partners

- FWD Group

- Sompo Himaraya

- NTUC Income (Income Insurance)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of embedded-insurance ecosystems

- 4.2.2 Sharp increase in Asia-Pacific cyber-risk exposure

- 4.2.3 Smartphone-first customer acquisition costs falling

- 4.2.4 Sandbox-style regulatory fast-tracks across Asia-Pacific

- 4.2.5 Advanced analytics/Gen-AI driving underwriting accuracy

- 4.2.6 Climate-linked parametric products gaining traction

- 4.3 Market Restraints

- 4.3.1 Persistent data-privacy fragmentation by jurisdiction

- 4.3.2 Thin actuarial loss histories for new-risk products

- 4.3.3 Profit-pool concentration in incumbents limits exits

- 4.3.4 Rising reinsurance pricing & capacity constraints

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product Line (Insurance Type)

- 5.1.1 Life Insurance

- 5.1.2 Health Insurance

- 5.1.3 Property & Casualty (Motor, Home, Commercial, Liability)

- 5.1.4 Specialty Lines (Cyber, Pet, Marine, Travel)

- 5.2 By Distribution Channel

- 5.2.1 Direct-to-Consumer (Digital)

- 5.2.2 Aggregators / Marketplaces

- 5.2.3 Digital Brokers / MGAs

- 5.2.4 Embedded Insurance Platforms

- 5.2.5 Traditional Agents / Brokers (digitally enabled)

- 5.2.6 Bancassurance (digitally enabled)

- 5.2.7 Other Channels

- 5.3 By End User

- 5.3.1 Retail / Individual

- 5.3.2 SME / Commercial

- 5.3.3 Large Enterprise / Corporate

- 5.3.4 Government / Public Sector

- 5.4 By Country

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South-East Asia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ZhongAn

- 6.4.2 Policybazaar

- 6.4.3 Acko

- 6.4.4 PasarPolis

- 6.4.5 Singlife

- 6.4.6 OneDegree

- 6.4.7 CXA Group

- 6.4.8 Waterdrop

- 6.4.9 Koala

- 6.4.10 CoverGo

- 6.4.11 Bolttech

- 6.4.12 Shift Technology

- 6.4.13 CarDekho (Insurance arm)

- 6.4.14 Turtlemint

- 6.4.15 Tokio Marine & Nichido (Digital Lab)

- 6.4.16 Ping An OneConnect

- 6.4.17 Munich Re Digital Partners

- 6.4.18 FWD Group

- 6.4.19 Sompo Himaraya

- 6.4.20 NTUC Income (Income Insurance)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border expansion patterns and market consolidation trends

- 7.2 Emerging technology applications and regulatory changes