|

시장보고서

상품코드

2043909

북미의 소프트 시설 관리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Soft Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

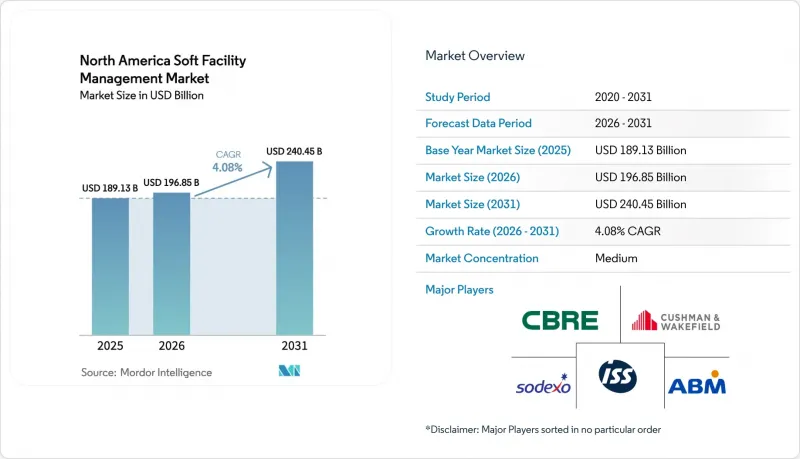

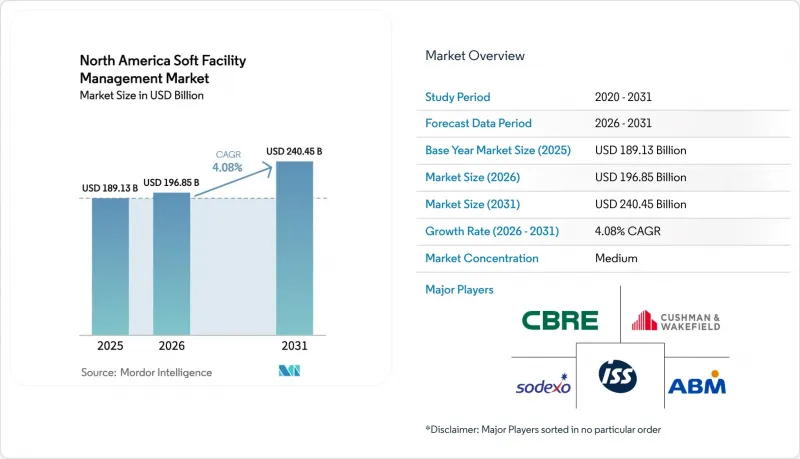

북미의 소프트 시설 관리 시장 규모는 2025년에 1,891억 3,000만 달러로 평가되었습니다. 2026년 1,968억 5,000만 달러에서 2031년까지 2,404억 5,000만 달러에 이를 것으로 예상되며, 예측 기간 CAGR은 4.08%를 나타낼 전망입니다.

(2026-2031년), 이는 노동집약적인 서비스와 디지털 관리를 결합할 수 있는 벤더에게 꾸준한 성장 여지가 있음을 보여줍니다.

하이브리드 근무 체제, 대형 프로젝트 완료, 웰빙 중심의 리노베이션 프로그램 등이 계약 수요를 촉진하는 한편, 비용 상승에 대한 우려로 인해 사내 팀에서 아웃소싱 및 성과급 계약으로의 전환이 가속화되고 있습니다. 현재 구매자는 시간당 인건비가 아닌 IoT 대시보드를 통해 확인된 '청소 가능한 평방피트당 총 비용'을 기준으로 제안서를 평가했습니다. 로봇 기술과 AI를 통한 작업지시 최적화를 통해 노동시간을 두 자릿수 단축할 수 있다는 것을 입증할 수 있는 통합업체가 다년간의 기업 계약을 따내고 있습니다. 일반 임금 규정, PFAS 금지, 사이버 보안 지침과 관련된 규제가 복잡해짐에 따라, 전담 컴플라이언스 담당자를 두고 소송 위험으로부터 고객을 보호할 수 있는 공급업체가 계속해서 유리한 위치를 점하고 있습니다.

북미의 소프트 시설 관리 시장 동향과 인사이트

북미 메가 건설 프로젝트의 성장

10억 달러가 넘는 대형 건설 프로젝트에서는 소프트 서비스 동원이 중요한 경로에 포함되어 입주 전 수익이 보장됩니다. 그 예로 고디 하우 국제대교와 게이트웨이 허드슨 터널을 들 수 있습니다. 이들 모두 인도 몇 달 전에 청소와 경비 통합 입찰을 실시하여 기존의 판매 주기를 단축했습니다. 이러한 계약의 조기 발주로 인해 벤더는 채용, 장비 임대, 안전 교육을 빠르게 확대해야 하지만, 5년 이상 예측 가능한 현금 흐름을 확보할 수 있습니다. 비주택 프로젝트 수주잔고 지표는 2025년 초 9.2개월로 2019년 이후 최고치를 기록해 향후 파이프라인이 견고하다는 것을 보여주었습니다. 유해물질 취급 자격이나 밀폐공간 작업 경험이 있는 시공사들은 주택 부동산의 경기변동에 영향을 덜 받는 분야인 지하철과 교량 자산에서 우대받고 있습니다. 중기적으로는 2026년부터 2028년까지 예정된 대규모 완공으로 설비투자가 지속적인 서비스 수익으로 전환되어 지역 평균을 상회하는 성장을 뒷받침할 것입니다.

상업용 부동산 전반의 아웃소싱 트렌드

기업 부동산 소유주나 임차인들은 가동률 변동에 따라 유연하게 대응할 수 있는 변동비 계약을 우선시하고, 비 핵심 업무인 청소나 경비 인력을 지속적으로 감축하고 있습니다. 통합 계약은 현재 아웃소싱 지출의 약 5분의 1을 차지하고 있으며, 2020년의 15%에서 증가하여 도입 속도가 눈에 띄게 빨라지고 있습니다. 포트폴리오 통합을 통해 송장 대조가 간소화되고, 조달 담당자의 인력이 줄어들고, 환승의 문턱이 낮아집니다. 이것이 바로 컨시어지 서비스를 제공하는 빌딩에서 입주자 유지율이 8%나 개선된 이유입니다. 이러한 추세는 어메니티 경쟁이 치열한 A급 타워에서 가장 두드러지게 나타나고 있으며, 교외의 건물주들조차도 임대계약 갱신에 따른 순영업이익을 보호하기 위해 성과연동형 가격 책정을 시도하고 있습니다.

청소업무 종사자의 인건비 상승과 높은 이직률

2019년부터 2025년까지 청소 노동자의 평균 임금은 19.1% 상승하여 전체 임금 인플레이션을 상회하며, 6-10%의 순이익률로 운영되는 계약업체들의 수익률을 압박했습니다. 뉴욕이나 샌프란시스코와 같은 고비용 도시 지역에서는 이직률이 75%를 넘어서는 것으로 보고되고 있으며, 각 기업은 대체 인력 1명을 채용할 때마다 1,200-1,800달러의 도입 비용을 부담해야 합니다. 현재 많은 입찰 업체들은 예상치 못한 임금 상승에 대비하기 위해 소비자 물가지수에 1퍼센트 포인트를 더한 연례 가격 조정 조항을 계약서에 포함시키고 있습니다. 로봇 기술은 효과적이지만, 막대한 설비투자와 유지보수 프로그램이 필요하기 때문에 이용률이 투자를 정당화할 수 있는 대규모 거점에만 도입이 제한적입니다. 인력 부족은 서비스 수준 준수를 위협하고 벤더에게 금전적 처벌과 계약 해지의 위험을 초래하기 때문에 인력 확보가 가장 시급한 성장의 걸림돌로 작용하고 있습니다.

부문 분석

보안 및 사무 지원 서비스는 2031년까지 연평균 5.76% 성장할 것으로 예상되며, 이는 북미 전체 소프트 시설 관리 시장의 평균을 상회하는 수치입니다. 이러한 수요는 원활한 출입 통제, 방문자 심사, 컨시어지 데스크가 통합된 워크플레이스 경험 앱에 통합된 하이브리드 워크모델에 의해 주도되고 있습니다. 청소 서비스는 2025년 매출의 38.89%를 차지하는 핵심 분야이지만, 모션 센서와 최적화된 순회 경로로 인해 화장실 한 곳당 근무 시간이 줄어들면서 성장 속도는 둔화되고 있습니다. 기업들이 물리적 보안과 사이버 보안의 융합을 중시하는 인재를 채용함에 따라, 보안 업무와 관련된 북미의 소프트 시설 관리 시장 규모는 2031년까지 100억 달러 규모에 달할 것으로 예측됩니다.

건물주들은 경비, 수하물 처리, 작업 공간 예약을 하나의 리셉션 기능으로 통합하는 경향이 증가하고 있으며, 이로 인해 평방피트당 서비스 요금이 상승하고 있습니다. 기업 캠퍼스에서 케이터링은 팬데믹 이전의 중요성을 되찾고 있으며, 2025년에는 급식 지원 프로그램을 통해 현장 출근률이 최대 18% 포인트까지 상승했습니다. 조경, 해충 방제, 폐기물 관리는 여전히 분산되어 있지만, 컴플라이언스 및 보고를 간소화하는 종합적인 마스터 계약으로 통합되고 있습니다. 리셉션, 우편실, 보안을 통합한 계약은 벤더에게 이벤트 관리 및 비상 대응 교육을 업셀링할 수 있는 입구이자 고객으로부터의 매출 점유율을 확대할 수 있는 기회이기도 합니다.

2025년에는 아웃소싱 계약이 시장 지출의 65.44%를 차지했고 CAGR 5.23%를 나타냈으며, 고정 인건비를 변동비로 전환하려는 의지가 강조되고 있습니다. 이 분야에서 통합 시설 관리 계약이 가장 빠르게 성장하고 있으며, 이는 조달 부서가 벤더 목록을 줄이고 서비스 제공에 실시간 분석을 도입하려는 의지를 반영하고 있습니다. 반면, 사내 프로그램은 34.56%를 차지하며, 대부분 보안 허가 요건이나 감염 방지 프로토콜에 묶여 있는 분야에 국한되어 있습니다.

북미의 소프트 시설 관리 시장에서 통합형 패키지의 점유율이 급증할 것으로 예측됩니다. 이는 조달팀이 계약에 성과 대시보드를 통합하여 거의 실시간으로 공급업체에 대한 제재와 보상을 할 수 있기 때문입니다. 단일 서비스 계약은 조정상의 마찰이 약간의 가격 할인을 능가하게 되면서 지지를 잃어가고 있습니다. 번들형과 비번들형 패키지는 아웃소싱을 시도하는 중견기업에게 가교 역할을 하고 있습니다. 많은 경우, 파일럿 단계에서 비용 절감 효과가 입증되면 완전히 통합된 계약으로 갱신하는 경우가 많습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe North America Soft Facility Management Market size was valued at USD 189.13 billion in 2025 and is estimated to grow from USD 196.85 billion in 2026 to reach USD 240.45 billion by 2031, at a CAGR of 4.08% during the forecast period (2026-2031), illustrating steady headroom for vendors that can pair labor-intensive services with digital oversight.

Hybrid work schedules, mega-project completions, and wellness-oriented retrofit programs are reinforcing contract demand, while cost-inflation concerns are accelerating the pivot from in-house teams to outsourced, performance-priced agreements. Buyers now judge proposals on total cost per cleanable square foot, verified through Internet of Things dashboards, rather than on hourly labor rates. Integrators able to prove double-digit reductions in labor hours through robotics or AI work-order routing are winning multi-year enterprise deals. Regulatory complexity linked to prevailing-wage rules, PFAS bans, and cybersecurity directives continues to favor suppliers with dedicated compliance staff and the ability to de-risk clients from litigation exposure.

North America Soft Facility Management Market Trends and Insights

Growth of Mega Construction Projects in North America

Mega builds valued above USD 1 billion are embedding soft-service mobilization into the critical path, guaranteeing revenue before occupancy. Examples include the Gordie Howe International Bridge and the Gateway Hudson Tunnel, both of which executed integrated cleaning and security bids months ahead of handover, shortening traditional sales cycles. Early award of these contracts forces vendors to scale recruitment, equipment leasing, and safety training rapidly but locks in predictable cash flows for 5-plus years. The backlog indicator for non-residential projects hit 9.2 months in early 2025, the highest since 2019, signaling a robust future pipeline. Contractors with hazardous-material certifications and confined-space experience are favored for underground rail and bridge assets, segments less vulnerable to residential real-estate cycles. Over the medium term, substantial completions scheduled between 2026 and 2028 will convert capex into recurring service revenue, supporting above-average regional growth.

Rising Outsourcing Trend Across Commercial Real Estate

Corporate landlords and occupiers continue divesting non-core janitorial and security staff in favor of variable-cost contracts that flex with fluctuating occupancy. Integrated contracts now account for roughly one-fifth of outsourced spend, up from 15% in 2020, highlighting the speed of adoption. Portfolio consolidation simplifies invoice reconciliation, trims procurement headcount, and raises switching barriers, which explains why tenant-retention rates improved eight percentage points in buildings offering concierge-style services. The trend is strongest in Class A towers where amenity arms races intensify, but even suburban landlords are experimenting with performance pricing to defend net operating income as leases roll.

Rising Labor Costs and High Employee Turnover in the Janitorial Workforce

Median janitorial wages rose 19.1% from 2019 to 2025, outpacing overall wage inflation and squeezing margins for contractors operating on 6-10% net profits. High-cost metros like New York and San Francisco report turnover exceeding 75%, forcing agencies to spend USD 1,200-1,800 in onboarding costs per replacement. Many bidders now insert annual price-escalator clauses pegged to the consumer price index plus one percentage point to hedge unexpected wage hikes. Robotics helps but requires hefty capital outlays and maintenance programs, limiting penetration to large footprints where utilization justifies investment. Staffing strain can jeopardize service-level compliance, exposing vendors to financial penalties and contract termination, making labor availability the most immediate brake on growth.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Healthcare Infrastructure Investment

- Adoption of Integrated Facility Management Platforms

- PFAS Chemical Regulations Restricting Cleaning Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and office support services are set to expand at 5.76% annually through 2031, exceeding the overall North America soft facility management market average. Demand is fueled by hybrid work models that require frictionless access control, visitor vetting, and concierge desks woven into workplace-experience apps. Cleaning, still the backbone at 38.89% of 2025 revenue, faces slower expansion as motion sensors and optimized routing cut labor-minutes per restroom. The North America soft facility management market size attached to security roles is slated to reach double-digit billions by 2031 as enterprises prioritize physical-cyber convergence hiring.

Landlords increasingly combine guard posts, package handling, and workspace reservations into a single reception function, boosting per-square-foot service fees. Catering resumes its pre-pandemic importance on corporate campuses, where subsidized food programs lifted on-site attendance by up to 18 percentage points in 2025. Landscaping, pest control, and waste management remain fragmented but are being wrapped into bundled master agreements that simplify compliance and reporting. Integrated reception, mailroom, and security contracts also provide a gateway for vendors to upsell event management and emergency preparedness training, deepening wallet share.

Outsourced arrangements captured 65.44% of market spending in 2025 and are projected to rise at a 5.23% CAGR, emphasizing the appetite to convert fixed payrolls into variable costs. Within this pool, integrated facility management contracts are the fastest-moving slice, a reflection of procurement's determination to cut vendor lists and insert real-time analytics into service delivery. In contrast, in-house programs cling to 34.56%, largely in sectors bound by security-clearance mandates or infection-control protocols.

North America soft facility management market share for integrated packages is poised to jump as procurement teams embed performance dashboards into contracts, letting them sanction or reward suppliers in near real time. Single-service deals are losing favor because coordination friction now outweighs marginal price discounts. Bundled but non-integrated packages serve as a bridge for mid-size enterprises experimenting with outsourcing; many flow into fully integrated renewals after pilot phases validate savings.

The North America Soft Facility Management Market Report is Segmented by Service Type (Cleaning, Security and Office Support, Catering, and More), Offering Type (In-House, and Outsourced), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CBRE Group Inc.

- Sodexo Inc.

- ISS A/S

- ABM Industries Inc.

- Cushman & Wakefield Plc

- Aramark Corporation

- Jones Lang LaSalle Incorporated

- GDI Integrated Facility Services Inc.

- Guardian Service Industries Inc.

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Calico Building Services Inc.

- CleanNet USA Inc.

- ServiceMaster Clean

- Compass Group PLC

- Pritchard Industries Inc.

- Coverall North America Inc.

- Vanguard Cleaning Systems Inc.

- Flagship Facility Services

- Jani-King International Inc.

- Shine Facility Services

- Cintas Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of Mega Construction Projects in North America

- 4.2.2 Rising Outsourcing Trend Across Commercial Real Estate

- 4.2.3 Increasing Healthcare Infrastructure Investment

- 4.2.4 Adoption of Integrated Facility Management Platforms

- 4.2.5 Demand for WELL and Fitwel Certified Workspaces Driving Specialized Soft Services

- 4.2.6 Proliferation of Tenant Experience Apps Enhancing Housekeeping Service Demand

- 4.3 Market Restraints

- 4.3.1 Rising Labor Costs and High Employee Turnover in Janitorial Workforce

- 4.3.2 Heightened Cybersecurity Risks for FM Data Platforms

- 4.3.3 PFAS Chemical Regulations Restricting Cleaning Formulations

- 4.3.4 Insurance Premium Inflation for On-site Service Contractors

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Cleaning

- 5.1.2 Security and Office Support

- 5.1.3 Catering

- 5.1.4 Other Soft Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single-service FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM (IFM)

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Commercial (IT/Telecom, Retail, Warehouses)

- 5.4.2 Hospitality (Hotels, Restaurants)

- 5.4.3 Institutional and Public Infrastructure

- 5.4.4 Healthcare

- 5.4.5 Industrial and Process

- 5.4.6 Residential and Leisure

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Sodexo Inc.

- 6.4.3 ISS A/S

- 6.4.4 ABM Industries Inc.

- 6.4.5 Cushman & Wakefield Plc

- 6.4.6 Aramark Corporation

- 6.4.7 Jones Lang LaSalle Incorporated

- 6.4.8 GDI Integrated Facility Services Inc.

- 6.4.9 Guardian Service Industries Inc.

- 6.4.10 Emeric Facility Services

- 6.4.11 SMI Facility Services

- 6.4.12 AHI Facility Services Inc.

- 6.4.13 Calico Building Services Inc.

- 6.4.14 CleanNet USA Inc.

- 6.4.15 ServiceMaster Clean

- 6.4.16 Compass Group PLC

- 6.4.17 Pritchard Industries Inc.

- 6.4.18 Coverall North America Inc.

- 6.4.19 Vanguard Cleaning Systems Inc.

- 6.4.20 Flagship Facility Services

- 6.4.21 Jani-King International Inc.

- 6.4.22 Shine Facility Services

- 6.4.23 Cintas Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment