|

시장보고서

상품코드

2043914

미국의 파사드 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)US Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

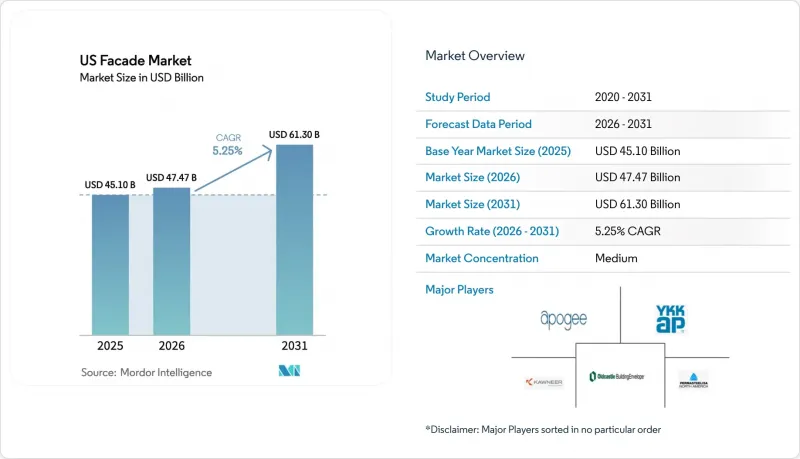

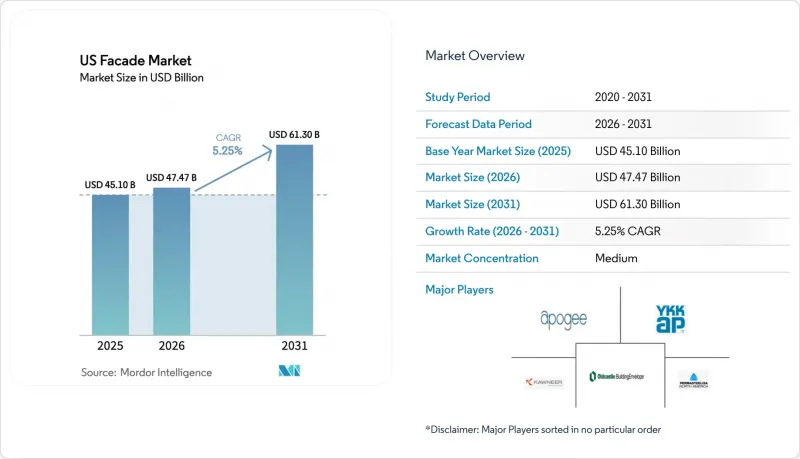

미국의 파사드 시장 규모는 2025년에 451억 달러로 평가되었습니다. 2026년 474억 7,000만 달러에서 2031년까지 613억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 5.25%를 나타낼 전망입니다.

이러한 확장을 촉진하는 세 가지 구조적 변화로는 팬데믹으로 인해 지연된 비주택 건설의 회복, 더욱 강화된 2024년판 국제 에너지 절약 표준(IECC) 및 ASHRAE 90.1-2022 건축 외피 표준의 미국 전역 도입, 그리고 특수한 방폭 및 고단열 조립 구조가 필요한 하이퍼스케일 데이터센터에 대한 투자 증가를 들 수 있습니다. 이러한 요인들이 복합적으로 작용하여 고성능 커튼월, 통기성 레인스크린 클래딩, 저탄소 알루미늄 프레임에 대한 수요가 증가하고 있습니다. 지역별로는 2025년 미국의 파사드 시장의 35.32%를 남부가 차지했지만, 캘리포니아주의 '바이 클린법'과 내진 규제에 힘입어 서부는 2031년까지 연평균 복합 성장률(CAGR) 5.46%로 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 2025년에는 오피스 빌딩의 현대화 및 데이터센터 캠퍼스 건설로 인해 현장 인력을 25-30% 절감할 수 있는 유닛화 시스템 수주가 가속화되어 상업용 최종 사용자가 전체 수요의 67.65%를 차지할 것으로 예측됩니다.

미국의 파사드 시장 동향 및 인사이트

비주택 건설의 회복으로 첨단 파사드 시스템에 대한 수요 증가

2025년 내내 설계 수주액은 견조한 흐름을 보였으며, AIA 지수는 평균 51.2를 기록했습니다. 이는 선벨트 지역의 주요 도시권에서 오피스 빌딩 및 복합용도 프로젝트의 지속적인 파이프라인이 형성될 것임을 시사합니다. 개발업체들은 시공기간을 최대 30%까지 단축할 수 있는 유닛화 커튼월 공법을 선호하고 있으며, 숙련공이 부족한 상황에서 인건비 절감에 기여하고 있습니다. 현재 A+등급의 건물은 LEED 플래티넘 또는 WELL 인증을 획득하는 것이 일반화되어 있으며, 이를 위해 파사드의 U값 0.30 미만, 가시광선 투과율 40% 이상을 요구하고 있습니다. 대표적인 예가 텍사스 어빙에 위치한 110만 평방피트 규모의 파이오니어 내추럴 리소스 본사 건물입니다. 이 건물은 가시광선 투과율(VLT) 44%, 일사 열획득률(SHGC) 0.26을 실현하는 빌라콘(Viracon) 유리를 채택한 3,000장의 고성능 커튼월로 덮여 있습니다. 이러한 프로젝트와 함께 단열 프레임, Low-E 단열 유리, 견고한 앵커 시스템 주문이 증가하고 있습니다. 에너지 기준이 강화됨에 따라 개발업체들이 자산의 미래성을 확보하기 위해 경쟁하는 가운데, 이러한 추세는 2027년까지 지속될 것으로 예측됩니다.

IECC 및 ASHRAE 90.1의 건축 외피 기준 강화로 고성능 파사드 채택 촉진

2024년판 IECC에서는 추운 지역의 커튼월 U값 상한이 0.36-0.40으로 강화된 반면, ASHRAE 90.1-2022에서는 허용 공기 누출량이 25% 감소했습니다. 이를 위해 삼중 유리 단열 유리 유닛, 연속 기밀층 및 고급 개스킷이 필요하며, 이로 인해 조립 비용이 12-15% 상승합니다. 그러나 캘리포니아, 뉴욕, 매사추세츠의 주정부 공사 프로그램에서는 기준치보다 20% 이상 성능이 우수한 파사드에 대해 평방피트당 8-12달러의 리베이트를 지급하고 있으며, 이를 통해 투자 회수 기간을 9년 미만으로 단축하고 있습니다. Old Castle Building Envelope의 'Series 3000 XT' 스토어 프론트는 기준치보다 훨씬 낮은 U값 0.20을 달성하여 제조업체가 프리미엄 고성능 제품으로의 사업 전환을 추진하고 있음을 보여주고 있습니다. 2026년 초까지 38개 주에서 2024년판 IECC를 채택함으로써 전국 통일 기준이 확립되어 첨단 외피 기술의 보급이 가속화되고 있습니다.

알루미늄 및 유리 가격 변동으로 파사드 시스템 프로젝트 비용 증가

2025년 초, 중국 제련소의 생산 제한으로 알루미늄 현물 가격이 전년 대비 30.5% 상승했고, 미국의 수입 금속에 대한 25% 관세 부과로 인해 알루미늄 현물 가격이 더욱 상승했습니다. 천연가스 가격의 급등으로 플로트 유리 제조업체는 15%의 비용 증가에 직면했고, 초대형 단열유리(IGU) 계약 가격이 급등했습니다. 파사드 시공업체는 수익률이 200-300bp 하락하여 고정가격 계약 재협상을 해야 했고, 중층 오피스 빌딩과 공동주택의 일부 착공이 늦어졌습니다. YKK AP America는 수요의 80%에 대해 저탄소 알루미늄 제련소와 장기 계약을 체결하여 원재료 가격을 안정화시킴으로써 리스크를 줄였지만, 일시적인 시장 하락 국면을 활용할 수 있는 능력은 제한적이었습니다. Apogee와 같이 자체적으로 유리 제조 및 마감 공정을 보유한 수직 통합형 대기업은 지역 독립 기업보다 가격 변동에 대한 저항력이 강해 경쟁 격차를 확대했습니다.

부문 분석

통기성 레인스크린 공법은 2025년 미국의 파사드 시장 점유율의 50.48%를 차지했고, 2031년까지 연평균 5.01%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예상되며, 해안 기후의 습도 관리를 우선순위로 삼고 있는 건축 규제 당국에 힘입어 2031년까지 성장할 것으로 예측됩니다. 이 설계는 수증기를 배출하는 0.75-1.5인치의 구멍을 만들어 결로 위험을 장벽벽에 비해 최대 50%까지 줄일 수 있습니다. 동해안을 포함한 IECC 기후대 4A-5A에서는 바람과 비의 영향으로 기존의 밀폐형 파사드가 문제가 되기 때문에 이 공법의 채택이 가속화되고 있습니다. 보험사는 통풍구 설치가 입증된 경우 보험료를 5-10% 할인해주고 있어 소유주에게 경제적 동기를 부여하고 있습니다.

건조한 남서부 지역에서는 낮은 습도로 인해 고장 발생률이 최소화되고 성능보다 비용 효율성이 우선시되기 때문에 비통풍식 시스템이 여전히 주류를 이루고 있습니다. 배수구 내부에 연속 단열재를 통합한 킹스팬의 '쿼드코어(QuadCore)' 패널과 같은 하이브리드 제품은 각 카테고리의 경계를 모호하게 만들어 설계자가 에너지 효율과 방습이라는 두 가지 목표를 모두 달성할 수 있게 해줍니다. 투자자들이 탄력적이고 저탄소적인 자산을 찾는 가운데, 통기성 설계는 가장 건조한 지역을 제외한 모든 지역에서 표준 사양이 될 것으로 예상되며, 미국의 파사드 시장 전체에서 꾸준히 확대될 것으로 예측됩니다.

2025년 기준, 커튼월은 고층 건축에서 확고한 입지를 바탕으로 미국 파사드 시장 규모의 52.40%를 차지했습니다. 그러나 2031년까지 연평균 복합 성장률(CAGR) 5.08%로 가장 빠르게 성장할 것으로 예상되는 분야는 레인스크린 클래딩입니다. 이는 세입자에게 미치는 영향을 최소화하기 위해 경량 오버클래딩을 선호하는 리노베이션 프로젝트의 물결에 편승한 것입니다. 구조층과 방수층을 분리하여 열교를 60-70% 줄일 수 있으며, U값 성능에 대한 엄격한 IECC 2024의 목표를 충족시킬 수 있습니다.

캘리포니아의 "몬테벨로 게이트웨이"와 같은 고층 오피스 타워는 여전히 파노라마 유리 외관을 실현하기 위해 맞춤형 커튼월에 의존하고 있습니다. 그러나 노후화된 B급 건물에서는 레인스크린이 실용적인 개보수 수단이 될 수 있으며, 덱스톨(Dextall)과 같은 지역 기업들은 현장의 노동력을 30% 절감할 수 있는 조립식 키트를 제공합니다. 미래에는 개폐식 통풍구와 배수구를 커튼월 프레임에 통합한 하이브리드 시스템이 경쟁 우위를 점할 수 있지만, 현재로서는 레인스크린이 미국의 파사드 시장에서 구조적 성장 우위를 누리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The US Facade Market size is projected to be USD 45.10 billion in 2025, USD 47.47 billion in 2026, and reach USD 61.30 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

Three structural shifts propel this expansion, including the rebound in non-residential construction after pandemic-era delays, the nationwide roll-out of stricter 2024 International Energy Conservation Code (IECC) and ASHRAE 90.1-2022 building-envelope standards, and a wave of hyperscale data-center investments requiring specialized blast-resistant and thermally efficient assemblies.Together, these forces boost demand for high-performance curtain walls, ventilated rainscreen cladding, and low-carbon aluminum framing. At the regional level, the South accounted for 35.32% of the US facade market in 2025, while the West is projected to be the fastest-growing region at 5.46% CAGR through 2031, aided by California's Buy Clean Act and seismic mandates. Commercial end-users dominated with 67.65% of demand in 2025 as office-tower modernizations and data-center campuses accelerated orders for unitized systems that cut on-site labor by 25-30%.

US Facade Market Trends and Insights

Rebound in Non-Residential Construction Increases Demand for Advanced Facade Systems

Design billings strengthened throughout 2025, with the AIA Index averaging 51.2, foreshadowing a sustained pipeline of office towers and mixed-use projects across Sunbelt metros. Developers favor unitized curtain-wall assemblies that cut installation time by up to 30%, helping contain labor costs amid skilled-trade shortages. Class A+ buildings now routinely target LEED Platinum or WELL certification, which encourages facade U-factors below 0.30 and visible-light transmittance above 40%. A marquee example is the 1.1 million-sq-ft Pioneer Natural Resources headquarters in Irving, Texas, clad with 3,000 high-performance curtain-wall units featuring Viracon glass that delivers 44% VLT and 0.26 SHGC. Taken together, these projects amplify orders for thermally broken framing, low-e insulated glass, and robust anchorage systems. The trend is expected to continue through 2027 as developers race to future-proof assets against tightening energy benchmarks.

Stricter IECC and ASHRAE 90.1 Building-Envelope Codes Drive High-Performance Facade Adoption

The 2024 IECC tightened curtain-wall U-factor limits to 0.36-0.40 in colder zones, while ASHRAE 90.1-2022 cut allowable air leakage by 25%. Compliance now demands triple-glazed IGUs, continuous air barriers, and advanced gaskets that raise assembly costs by 12-15%. Yet state utility programs in California, New York, and Massachusetts rebate USD 8-12 per sq ft for facades that outperform code by 20%, shrinking payback periods to less than nine years. Oldcastle BuildingEnvelope's Series 3000 XT storefront achieves U-factors of 0.20, well below code, highlighting how fabricators are repositioning toward premium, high-performance products. As 38 states had adopted the 2024 IECC by early 2026, a uniform national baseline now accelerates widespread adoption of advanced envelope technologies.

Volatility in Aluminum and Glass Prices Raises Facade System Project Costs

Aluminum spot prices climbed 30.5% year-over-year in early 2025 due to curtailments in Chinese smelting, while a 25% U.S. tariff on imported metals added further strain. Float-glass producers faced 15% cost hikes as natural-gas prices spiked, sending contract prices for oversized IGUs sharply higher. Facade contractors lost 200-300 basis points of margin and renegotiated fixed-price deals, delaying some mid-rise office and multifamily starts. YKK AP America mitigated risk by signing long-term deals with low-carbon aluminum smelters for 80% of its demand, stabilizing input pricing yet limiting its ability to exploit short-lived market dips. Vertically integrated majors such as Apogee, with in-house glass and finishing, weathered volatility better than regional independents, widening competitive gaps.

Other drivers and restraints analyzed in the detailed report include:

- Aging Commercial Building Stock Triggers Large-Scale Facade Retrofit and Modernization Projects

- Rising Demand for High-Performance Glazing Improves Building Energy-Efficiency Outcomes

- Shortage of Certified Facade Installers Delays Project Execution and Increases Labor Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ventilated rainscreen assemblies captured 50.48% of the US facade market share in 2025 and are projected to expand at a 5.01% CAGR through 2031 as code bodies prioritize moisture management in coastal climates. The design introduces a 0.75-1.5-inch cavity that drains vapor, cutting condensation risk by up to 50% relative to barrier walls. Adoption accelerates in IECC Climate Zones 4A-5A, covering the Eastern seaboard, where wind-driven rain challenges traditional sealed facades. Insurance carriers offer 5-10% premium discounts when ventilated cavities are documented, reinforcing financial motivation for owners.

Non-ventilated systems remain dominant in the arid Southwest, where low humidity keeps failure rates minimal, and cost efficiency trumps performance. Hybrid products, such as Kingspan's QuadCore panels that integrate continuous insulation inside a drained cavity, blur the lines between categories and allow designers to meet both energy and moisture objectives. As investors demand resilient and low-carbon assets, ventilated designs are expected to become the baseline specification in all but the driest regions, ensuring their steady ascent within the broader US facade market.

Curtain walls accounted for 52.40% of the US facade market size in 2025, owing to their stronghold in high-rise construction. However, rainscreen cladding is projected to grow fastest at 5.08% CAGR to 2031, riding a wave of retrofit projects that favor lightweight over-cladding with minimal tenant disruption. Decoupling of structural and weatherproofing layers reduces thermal bridging by 60-70%, meeting stringent IECC 2024 targets for U-factor performance.

High-rise office towers, such as Montebello Gateway in California, still depend on custom curtain walls to achieve panoramic glass facades. Yet for aging Class B stock, rainscreens offer a practical upgrade path, and regional players like Dextall provide prefabricated kits that slash on-site labor by 30%. Looking ahead, hybrid systems that merge operable vents and drainage cavities into curtain-wall frames could neutralize the competitive gap, but for now, rainscreens enjoy a structural growth advantage in the US facade market.

The US Facade Market Report is Segmented by Type (Ventilated, Non-Ventilated, and Others), by Facade System Type (Rainscreen Cladding, Curtain-Wall Systems, and Others), by Material (Glass, Metal, Plastics and Fibers, and More), by Installation (New Construction, Renovation & Retrofit), by End-User (Commercial, and More), and by Region (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Apogee Enterprises Inc.

- Oldcastle BuildingEnvelope

- YKK AP America

- Kawneer North America

- Permasteelisa North America

- Enclos Corp

- Walters & Wolf

- Benson Industries

- EFCO Corporation

- CENTRIA

- Kingspan Insulated Panels US

- Sto Corp.

- Clark Pacific

- C.R. Laurence (U.S. Aluminum)

- National Enclosure Company

- GlassFab Tempering Services

- Technical Glass Products

- PPG Architectural Coatings

- Guardian Glass North America

- Schuco USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rebound in non-residential construction increases demand for advanced facade systems

- 4.2.2 Stricter IECC and ASHRAE 90.1 building envelope codes drive high-performance facade adoption

- 4.2.3 Aging commercial building stock triggers large-scale facade retrofit and modernization projects

- 4.2.4 Rising demand for high-performance glazing improves building energy efficiency outcomes

- 4.2.5 Expansion of hyperscale data centers increases investment in specialized facade structures

- 4.2.6 FEMA resilience grants encourage installation of hurricane-rated and disaster-resistant facades

- 4.3 Market Restraints

- 4.3.1 Volatility in aluminum and glass prices raises facade system project costs

- 4.3.2 Shortage of certified facade installers delays project execution and increases labor costs

- 4.3.3 Insurance exclusions for combustible cladding under NFPA 285 limit material choices

- 4.3.4 City-level embodied carbon regulations such as Buy Clean policies increase compliance costs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing Analysis

- 4.8 Consumer Behavior Analysis

- 4.9 Sustainability Trends

- 4.10 Porter's Five Forces

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Others

- 5.2 By Facade System Type

- 5.2.1 Rainscreen Cladding

- 5.2.2 Curtain-Wall Systems

- 5.2.3 Others

- 5.3 By Material

- 5.3.1 Glass

- 5.3.2 Metal

- 5.3.3 Plastic & Fibres

- 5.3.4 Stone

- 5.3.5 Others

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation & Retrofit

- 5.5 By End-User

- 5.5.1 Commercial

- 5.5.2 Residential

- 5.5.3 Others

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.3.1 Apogee Enterprises Inc.

- 6.3.2 Oldcastle BuildingEnvelope

- 6.3.3 YKK AP America

- 6.3.4 Kawneer North America

- 6.3.5 Permasteelisa North America

- 6.3.6 Enclos Corp

- 6.3.7 Walters & Wolf

- 6.3.8 Benson Industries

- 6.3.9 EFCO Corporation

- 6.3.10 CENTRIA

- 6.3.11 Kingspan Insulated Panels US

- 6.3.12 Sto Corp.

- 6.3.13 Clark Pacific

- 6.3.14 C.R. Laurence (U.S. Aluminum)

- 6.3.15 National Enclosure Company

- 6.3.16 GlassFab Tempering Services

- 6.3.17 Technical Glass Products

- 6.3.18 PPG Architectural Coatings

- 6.3.19 Guardian Glass North America

- 6.3.20 Schuco USA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment