|

시장보고서

상품코드

2043920

제약 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

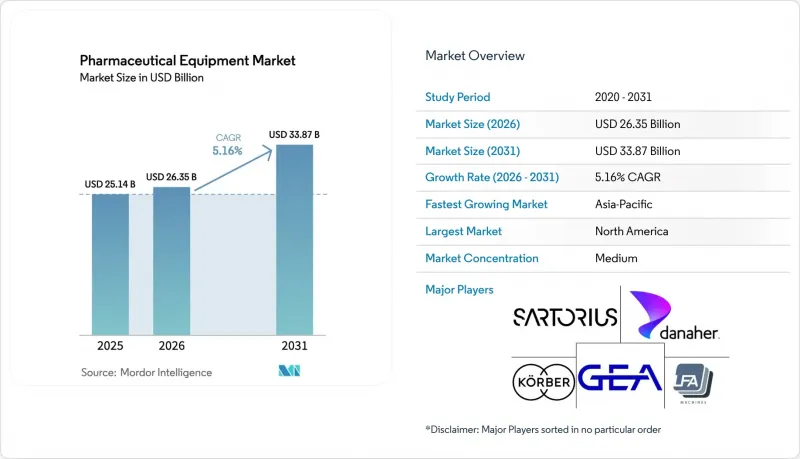

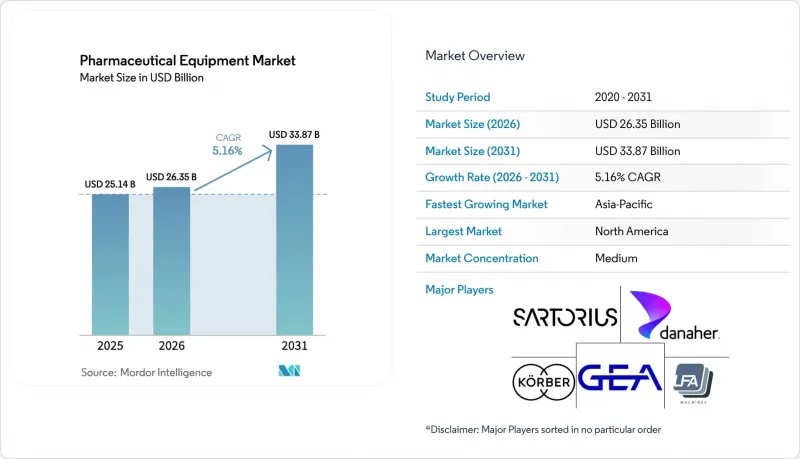

제약 장비 시장 규모는 2025년 259억 3,000만 달러로 평가되었습니다. 2026년 271억 달러로 확대되어 2031년까지 337억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 4.51%를 나타낼 전망입니다.

수요는 바이오 의약품으로 이동하고 있으며, 현재 전임상 및 임상 제조 공정의 62%를 차지하고 있습니다. 이를 통해 공급업체는 모놀리식 스테인리스 스틸 설비를 모듈식 일회용 어셈블리로 대체하여 검증 기간을 18개월에서 6개월 이내로 단축할 수 있게 되었습니다. 위탁 개발 및 제조 기관(CDMO)은 구매력을 강화하고 있으며, 2024년에는 전 세계 바이오리액터 용량의 28%를 소비했고 2028년에는 38%를 차지할 것으로 예상되며, 연속 흐름 생산 스키드에 대한 투자를 가속화하고 있습니다. 규제 변경으로 인해 업그레이드 주기가 가속화되고 있습니다. 유럽의약품청(EMA)의 Annex 1 개정으로 유럽 내 약 1,200여 곳의 충전 및 마감 라인에 아이솔레이터 또는 제한적 접근 차단 시스템(RABS) 도입이 의무화됨에 따라 수년간의 개보수 수요가 축적되어 왔습니다. 한편, 미국 식품의약국(FDA)은 첨단 제조기술을 도입하는 신청서를 우선 심사하고 있으며, 이로 인해 시판 승인까지의 기간이 6-9개월 단축되어 설비투자가 가속화되고 있습니다.

세계의 제약 장비 시장 동향과 인사이트

늘어나는 바이오의약품 생산량

2024년에는 바이오의약품이 파이프라인 제조 공정의 85%를 차지했으며, 이에 따라 전 세계 바이오리액터 설치 용량은 2028년까지 670만 리터에서 890만 리터로 확대될 것으로 전망됩니다. 바이러스 벡터 생산 라인의 제약이 가장 심하고, 설비 리드타임이 18-24개월에 달하고, 유전자 치료제 시장 출시가 제한되고 있습니다. 신제품 파이프라인은 업스트림 공정과 충전 및 마무리 공정의 설비 통합을 촉진하고, 배치 간 이송을 40% 줄이고 오염 관리를 간소화합니다.

일회용 기술 도입 가속화

일회용 시스템 시장 규모는 2025년 278억 달러에 달했으며, 현재 상업 생산 배치의 62%에서 도입되어 세척 및 검증에 따른 다운타임을 수백만 달러 절감했습니다. CDMO 업체들은 스테인리스 라인의 45-60일 대비 14일이라는 짧은 캠페인 전환 기간을 높이 평가하고 있으며, 이를 통해 설비 가동률 향상을 실현하고 있습니다. 2024년 발생한 폴리머 필름 공장 화재로 인해 4개월 동안 가방 납품이 중단되어 유럽 전역의 현물 가격이 15% 상승하는 등 공급망 취약성은 여전히 지속되고 있습니다.

부문 분석

GLP-1 작용제 및 단일 클론 항체용 프리필드시린지 및 오토인젝터에 대한 수요 증가를 배경으로 2025년 무균 충전 포장 플랫폼은 제약 기기 시장 점유율의 29.55%를 차지할 것으로 예측됩니다. 규제 당국이 100% 육안 검사 및 실시간 릴리스 검사를 의무화함에 따라 품질 관리 장비 시장은 2031년까지 연평균 4.85% 성장할 것으로 예측됩니다. 업스트림 바이오프로세스 스키드는 포유류 세포 배양 능력이 33% 급증한 혜택을 누리고 있지만, 중국 업체들이 유럽과 미국 가격보다 최대 40% 낮은 가격을 책정하고 있어 수익률이 압박을 받고 있습니다.

공정의 병목현상인 다운스트림 정제 설비는 주요 CDMO의 경우 가동률이 85% 이상이며, 2,000L 배치당 8-12회 크로마토그래피 처리가 필요하고 1회당 4-6시간이 소요됩니다. 직렬화 의무화로 인해 1차 및 2차 포장 라인의 비용은 설치당 150만-250만 달러 증가했으며, Annex 1(부록 1)의 요구사항으로 인해 공조(HVAC)와 주사용수 지출이 증가했습니다. 경구용 고형제 생산이 저비용 기지로 이동함에 따라 동결건조기 및 균질화기 관련 제약 장비 시장 규모는 전체 시장 평균을 밑돌고 있습니다.

지역별 분석

2025년 북미는 제약 제조 장비 시장 매출의 42.52%를 차지했습니다. 이는 310만 리터의 설치 바이오리액터 용량과 최대 9개월의 승인 주기를 단축하는 FDA의 신속한 심사 덕분입니다. BARDA의 투자로 텍사스, 노스캐롤라, 메릴랜드에 신속 배포 모듈이 설치되는 한편, 캐나다의 3.7억 달러 규모의 재생의료 허브는 임상 단계의 생산 능력을 강화하고 있습니다. 멕시코는 40-50%의 인건비 절감을 무기로 미국 기업의 3건의 충진포장 공정 확장을 유치하고 있습니다.

아시아태평양은 중국의 120만 리터 생산능력 증설과 인도의 API 및 바이오의약품에 대한 1,500억 루피의 PLI(생산 연동형 인센티브)가 견인차 역할을 하며 2031년까지 연평균 5.12% 성장할 것으로 예측됩니다. 한국과 싱가포르는 주요 CDMO 클러스터를 보유하고 있으며, 일본은 노동력 부족을 보완하기 위해 자동화를 추진하여 검사 셀에 18대의 협동로봇을 도입하고 있습니다.

유럽은 에너지 비용 상승에 직면하고 있으며, 2024년 독일의 전기 요금이 22% 상승했지만, 그럼에도 불구하고 일회용 부품 혁신의 핵심으로 남아 있으며, 상위 15개 공급업체 중 9개 업체는 독일에 본사를 두고 있습니다. 부속서 1에 따르면, 독일, 영국, 프랑스를 필두로 30억 달러 규모의 설비 교체 붐이 일어나고 있습니다. 남유럽은 규제 승인 절차가 다소 오래 걸리지만, 낮은 인건비를 배경으로 바이오시밀러의 충진 및 포장 허브로 부상하고 있습니다. 중동 및 아프리카와 남미는 규모는 작지만 전략적으로 중요한 지역으로 남아 있습니다. 사우디는 2030년까지 의약품 수입 의존도를 50%로 낮추기 위해 32억 달러를 투자하기로 결정했습니다. 남아공의 Biovac은 mRNA 제제 충전 포장에 있어 Pfizer와의 제휴를 확보하여 아프리카 대륙 최초의 WHO 사전 승인 라인을 구축했습니다. 브라질 국영기업 Biomanguinhos는 2025년 2,000리터 규모의 일회용 원자로를 도입했지만, 품질 관리에 대한 투자 부족으로 수출 준비에 차질을 빚고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The pharmaceutical equipment market size is expected to increase from USD 25.93 billion in 2025 to USD 27.10 billion in 2026 and reach USD 33.79 billion by 2031, growing at a CAGR of 4.51% over 2026-2031.

Demand pivots toward biologics, which now account for 62% of pre-clinical and clinical manufacturing runs, prompting suppliers to replace monolithic stainless-steel installations with modular, single-use assemblies that cut validation timelines from 18 months to under 6 months. Contract development and manufacturing organizations (CDMOs) are consolidating purchasing power; they consumed 28% of global bioreactor capacity in 2024 and are projected to command 38% by 2028, accelerating investment in continuous-flow production skids. Regulatory change intensifies upgrade cycles: the European Medicines Agency's Annex 1 revision obliges isolators or restricted-access barrier systems (RABS) across roughly 1,200 European fill-finish suites, driving a multiyear retrofit backlog. Meanwhile, the U.S. Food and Drug Administration (FDA) fast-tracks applications that deploy advanced manufacturing technologies, shortening commercial approval by 6 to 9 months and accelerating capital spending.

Global Pharmaceutical Equipment Market Trends and Insights

Rising Biologics Manufacturing Volumes

Biologics commanded 85% of pipeline manufacturing runs in 2024, pushing installed global bioreactor volume from 6.7 million L to an expected 8.9 million L by 2028. Viral-vector lines are most constrained, with 18-24-month equipment lead times that limit gene-therapy launches. New product pipelines encourage co-location of upstream and fill-finish assets, trimming batch transfer by 40% and simplifying contamination control.

Accelerated Adoption of Single-Use Technologies

Single-use systems reached USD 27.8 billion in 2025 and are now deployed in 62% of commercial batches, saving users millions in cleaning-validation downtime. CDMOs value the 14-day campaign changeovers versus 45-60 days for stainless-steel lines, unlocking higher asset utilization. Supply-chain fragility persists: a 2024 polymer-film plant fire disrupted bag deliveries for 4 months and raised spot prices by 15% across Europe.

Other drivers and restraints analyzed in the detailed report include:

- Stringent GMP-Driven Equipment Upgrades

- Expansion of Contract Manufacturing Capacity

- High Capital Investment & Long Payback

- Supply-Chain Shortages of Critical Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aseptic fill-finish platforms captured 29.55% of the pharmaceutical equipment market share in 2025 amid the boom in pre-filled syringes and autoinjectors for GLP-1 agonists and monoclonal antibodies. Quality-control instrumentation is forecast to grow 4.85% annually through 2031 as regulators require 100% visual inspection and real-time release testing. Upstream bioprocess skids benefit from a 33% surge in mammalian capacity, yet Chinese vendors undercut Western prices by up to 40%, squeezing margins.

Downstream purification assets, a gating step, run at >85% utilization in leading CDMOs, with each 2,000 L batch cycling through 8-12 chromatography passes and consuming 4-6 hours per pass. Serialization mandates raise primary and secondary packaging line costs by USD 1.5-2.5 million per installation, while Annex 1 drives higher HVAC and water-for-injection expenditure. The pharmaceutical equipment market size tied to lyophilizers and homogenizers trails the broader average as oral-solid dose output migrates to lower-cost sites.

The Pharmaceutical Equipment Market Report is Segmented by Equipment Type (Upstream Bioprocess Equipment, Downstream Purification Equipment, and More), Manufacturing Stage (Drug Substance Production, Drug Product Formulation, and More), End User (Pharmaceutical Manufacturing Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 42.52% of the pharmaceutical equipment market revenue in 2025, supported by 3.1 million L of installed bioreactor volume and expedited FDA reviews that shorten approval cycles by up to 9 months. BARDA investments establish rapid-deployment modules in Texas, North Carolina, and Maryland, while Canada's USD 370 million regenerative-medicine hub enhances clinical-stage capacity. Mexico leverages labor savings of 40-50% to attract three U.S. fill-finish expansions.

Asia-Pacific is projected to grow 5.12% CAGR through 2031, spearheaded by China's 1.2 million L capacity boost and India's INR 150 billion PLI incentives for APIs and biologics. South Korea and Singapore host major CDMO clusters, whereas Japan automates to offset labor deficits, implementing 18 collaborative robots across inspection cells.

Europe faces elevated energy costs, with German electricity tariffs up 22% in 2024, yet it remains the innovation nucleus for single-use components, housing 9 of the top 15 suppliers. Annex 1 drives a USD 3 billion retrofit boom, led by Germany, the UK, and France. Southern Europe is emerging as a biosimilar fill-finish hub, driven by lower labor costs, despite slightly longer regulatory timelines. Middle East-Africa and South America remain small but strategically important. Saudi Arabia commits USD 3.2 billion to cut drug import reliance to 50% by 2030. South Africa's Biovac secured Pfizer partnership for mRNA fill-finish, the continent's first WHO-prequalified line. Brazil's state-run Biomanguinhos installed a 2,000 L single-use reactor in 2025, but under-investment in quality control curbs export readiness.

- ACG Worldwide

- Colanar AG

- Danaher (Cytiva & Pall)

- Esco Lifesciences

- GEA Group

- IMA Group

- Korber Pharma

- Merck KGaA (MilliporeSigma)

- Optima Packaging

- Pall

- Romaco Group

- Sartorius

- Shinva Medical

- Stevanato Group

- Syntegon Technology

- Thermo Fisher Scientific

- Tofflon Science & Technology

- Truking Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biologics Manufacturing Volumes

- 4.2.2 Accelerated Adoption of Single-Use Tech

- 4.2.3 Stringent GMP-Driven Equipment Upgrades

- 4.2.4 Expansion of Contract Manufacturing Capacity

- 4.2.5 Shift Toward Continuous Manufacturing Lines

- 4.2.6 Pharma 4.0 Predictive-Maintenance Retrofits

- 4.3 Market Restraints

- 4.3.1 High Capital Investment & Long Payback

- 4.3.2 Supply-Chain Shortages of Critical Components

- 4.3.3 Multi-Jurisdiction Approval Complexity

- 4.3.4 Skilled-Labor Gap in Emerging Markets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Equipment Type

- 5.1.1 Upstream Bioprocess Equipment

- 5.1.2 Downstream Purification Equipment

- 5.1.3 Aseptic Fill-Finish Systems

- 5.1.4 Primary & Secondary Packaging Lines

- 5.1.5 Quality-Control & Inspection Instruments

- 5.1.6 Ancillary Utilities (HVAC, CIP/SIP, etc.)

- 5.1.7 Others

- 5.2 By Manufacturing Stage

- 5.2.1 Drug Substance Production

- 5.2.2 Drug Product Formulation

- 5.2.3 Fill-Finish

- 5.2.4 Final Packaging & Labelling

- 5.2.5 Quality-Control & Release Testing

- 5.3 By End User

- 5.3.1 Pharmaceutical Manufacturing Companies

- 5.3.2 Contract Development & Manufacturing Orgs (CDMOs/CMOs)

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ACG Worldwide

- 6.3.2 Colanar AG

- 6.3.3 Danaher (Cytiva & Pall)

- 6.3.4 Esco Lifesciences

- 6.3.5 GEA Group AG

- 6.3.6 IMA Group

- 6.3.7 Korber Pharma

- 6.3.8 Merck KGaA (MilliporeSigma)

- 6.3.9 Optima Packaging

- 6.3.10 Pall Corporation

- 6.3.11 Romaco Group

- 6.3.12 Sartorius AG

- 6.3.13 Shinva Medical

- 6.3.14 Stevanato Group

- 6.3.15 Syntegon Technology

- 6.3.16 Thermo Fisher Scientific

- 6.3.17 Tofflon Science & Technology

- 6.3.18 Truking Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment