|

시장보고서

상품코드

2043956

상용차 ADAS : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Commercial Vehicle ADAS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

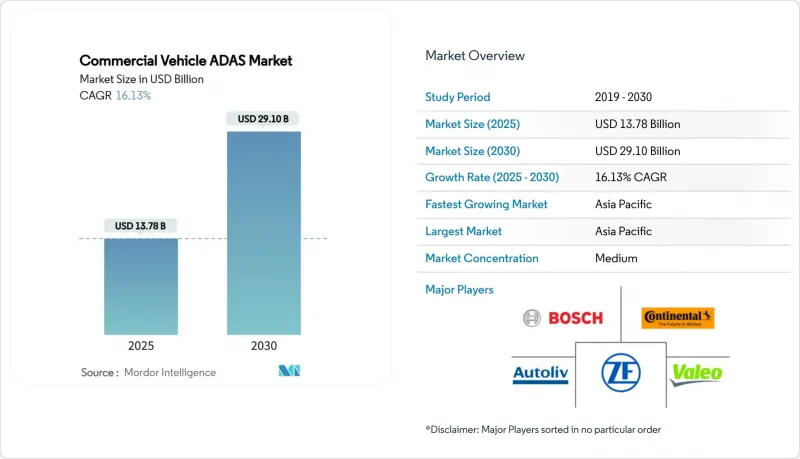

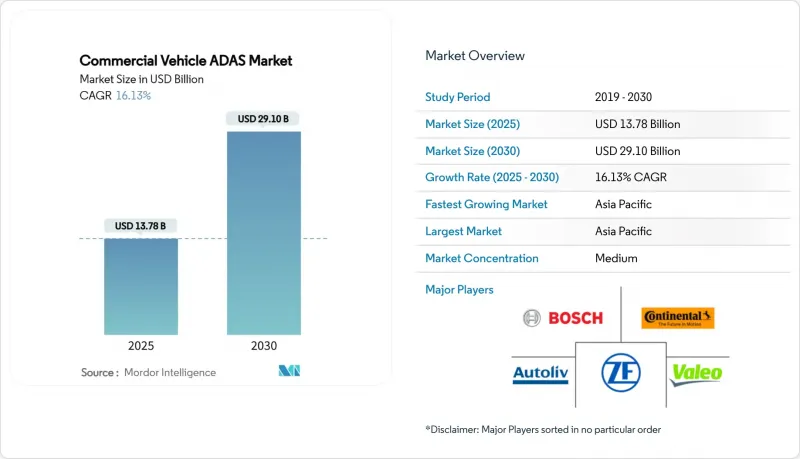

상용차 ADAS 시장 규모는 2025년에 137억 8,000만 달러로 평가되었고 예측 기간(2025-2030년) CAGR 16.13%를 나타내, 2030년에는 291억 달러에 이를 전망입니다.

이러한 성장 궤적은 규제 요건의 일치, 센서 융합 아키텍처의 성숙, 충돌 회피 기술의 뚜렷한 경제적 이점을 반영합니다. 미국 연방교통안전국(FMCSA)의 추정에 따르면, 첨단운전자보조시스템(ADAS)에 1달러를 투자할 때마다 충돌 관련 비용 절감, 운전자 정착, 보험 혜택으로 5.09달러의 수익을 얻을 수 있는 것으로 나타났습니다. 레이더, 카메라, LiDAR의 비용은 2024년 이후 꾸준히 하락하고 있으며, 이를 통해 OEM 업체들은 구매자를 멀리하는 가격 프리미엄을 부과하지 않고도 소형, 중형, 대형 플랫폼에 고급 레벨2 기능을 통합할 수 있게 되었습니다. 동시에 북미와 유럽의 보험사들은 현재 전방충돌경보, 사각지대 감지, 운전자 모니터링 기능을 장착한 차량에 대해 평균 6-12%의 보험료 할인을 적용하고 있습니다. 이는 극도로 낮은 영업이익률 속에서 사업을 영위하는 선단 사업자들에게는 더 큰 인센티브가 될 수 있습니다.

세계의 상용차 ADAS 시장 동향과 인사이트

도로 안전 규제 강화

각 국가와 초국가적 기관은 신형 트럭과 버스에 대한 ADAS의 최소 기준에 대해 합의했습니다. 유럽 연합(EU)의 일반 안전 규정(General Safety Regulation)에 따라 2024년 7월 이후 판매된 모든 신형 상용차에는 첨단 비상 브레이크, 지능형 스피드 어시스트, 운전자 졸음운전 경고장치 장착이 의무화되었습니다. 인도도 2026년부터 버스와 대형 트럭에 대해 유사한 기능을 의무화할 예정으로, 세계 2위의 화물 시장을 세계 베스트 프랙티스 수준으로 끌어올릴 수 있을 것입니다. 미국에서는 FMCSA(연방 자동차 운송 안전국)의 자체 조사 결과를 반영한 자동 긴급 제동 요구사항이 최종 단계에 접어들었습니다. 규칙의 통일은 지역별 기술적 차이를 해소하고, Tier 1 공급업체가 세계 하드웨어 소프트웨어 스택을 개발하여 규모의 경제를 누릴 수 있도록 합니다. 이러한 규제 압력으로 인해 향후 OEM의 라인업에서 ADAS 미탑재 모델은 제외될 것이며, 상용차 ADAS 시장은 선택적 업그레이드가 아닌 표준 안전기능으로 정착될 것입니다.

자율주행/ADAS 스택의 기술적 진보

레벨 2의 경고 지원에서 예측 개입으로의 전환은 센서 융합의 정확성과 AI를 활용한 상황 인식에 달려있습니다. 콘티넨탈의 6세대 레이더는 높은 샘플링 속도로 360도 커버리지를 실현하는 한편, 보쉬와 마이크로소프트는 규칙 기반 알고리즘보다 더 빠르게 위험을 분류하기 위해 생성형 AI를 적용하고 있습니다. LiDAR의 비용은 2019년의 10분의 1로 낮아졌고, 단일 광자 아발란스 다이오드의 기술 발전으로 8mm의 거리 분해능이 실현되어 비나 안개 속에서도 식별 능력이 향상되었습니다. 77GHz 레이더와 결합된 열화상 이미징은 야간에 보행자와 도로변 인프라를 식별하는 데 도움을 줍니다. 이러한 기술의 융합으로 레벨 3 화물 운송 경로의 개발 주기가 단축되고 있으며, Daimler Truck은 2027년까지 미국 고속도로에서 SAE 레벨 4 차량을 출시하는 것을 목표로 하고 있습니다.

ADAS 부품의 높은 초기 비용

센서 가격이 하락하고 있지만, LiDAR의 단가는 여전히 4자릿수이며, 라틴아메리카나 아세안 일부 지역의 개인 사업자가 감당할 수 없는 수준입니다. 레이더, 초음파, 도메인 컨트롤러를 포함한 전체 센서 제품군은 새로운 섀시에 수천 달러의 비용이 추가되어 소규모 차량 소유자에게는 투자 회수 기간이 길어질 수 있습니다. 애프터마켓도 비슷한 문제에 직면해 있습니다. 카메라 보정을 할 수 있을 만큼 넓은 조정 베이를 보유하고 있는 수리 공장은 30%에 불과합니다. Mobileye가 2024년 개보수 설치 부문을 축소하기로 결정한 것은 단기적인 공급량의 한계를 드러냈습니다. 반도체 공급이 정상화되고 규모의 경제가 확대됨에 따라, Tier 2 업체들은 2026년까지 카메라 모듈의 평균 판매 가격이 20% 더 하락하여 가격 장벽이 낮아질 것으로 예상하고 있습니다.

부문 분석

운전 지원 시스템 도입은 차량 사업자가 즉시 수익성이 있다고 판단하는 기능에 집중되어 있습니다. 어댑티브 크루즈 컨트롤(ACC)은 2024년 매출의 24.71%를 차지했으며, 이는 고속도로에서의 정속 주행에서 입증된 연비 개선 효과가 반영된 것입니다. 상용차 ADAS 시장에서 운전자 모니터링 시스템 시장 규모는 CAGR 16.72%로 확대되고 있습니다. 이는 규제 당국이 피로 감지를 중요한 기능으로 정의하고 있기 때문입니다. 1단계 공급업체는 안구 폐쇄 지표, 심박수 변동, 얼굴 랜드마크 추적을 통합하여 차량 내부를 생체 인식 안전지대로 바꾸고 있습니다.

이와 함께 미국 연방 도로교통안전국(FMCSA)의 규칙안이 시속 40마일(약 64km/h)에서 최소 감속률 0.45G를 규정함에 따라 자동긴급제동(AEB) 도입이 가속화되고 있습니다. 또한, Eurospec 규격이 우회전 시 자전거 이용자 보호 검사를 도입하면서 사각지대 감지 기능이 보급되었습니다. 전방 충돌 경고는 여전히 기본적인 기능이지만, 야간 투시 오버레이 기능을 갖춘 멀티모달 융합 시스템에 통합되고 있습니다.

2024년 상용차 ADAS 시장에서 48.17%의 매출 점유율을 차지한 레이더는 여전히 충돌 감소의 핵심 기술입니다. 단거리 모듈 1개당 50달러 이하의 가격대와 우천 시에도 검증된 성능으로 그 필수성은 흔들림이 없습니다. 그러나 LiDAR는 단가가 350달러 이하로 떨어지고 해상도가 1도당 200라인까지 향상되면서 2030년까지 연평균 복합 성장률(CAGR) 16.57%를 나타낼 것으로 예측됩니다. 한국과학기술연구원은 지터 56피코초의 단일 광자 아발란스 다이오드를 개발하여 도시 매핑의 정확도를 10센티미터 이하로 높였습니다.

센서퓨전의 전략은 중복성에서 상호보완성으로 전환하고 있습니다. 마그나(Magna)의 열-레이더 하이브리드 시스템은 감지 거리를 최대 200m까지 확장하여 레이더만 사용하는 시스템에 비해 오감지를 50% 감소시킵니다. 도메인 제어 유닛은 초당 10기가비트 이더넷 스트림을 관리하며, 충돌 회피 알고리즘에 대한 확정적인 지연을 보장합니다.

지역별 분석

아시아태평양은 2024년 전 세계 상용차 ADAS 시장 매출의 38.73%를 차지했으며 2030년까지 연평균 16.24%의 연평균 복합 성장률(CAGR)로 선두를 유지할 것으로 예측됩니다. 중국의 급속한 전동화는 신형 승용차의 레벨2 도입과 맞물려 트럭용 ADAS의 비용을 절감하는 공통공급망을 형성하고 있습니다. 광둥성과 저장성의 상업용 차량은 보험 보조금에 힘입어 전방충돌경보장치를 표준 장비로 도입하고 있습니다. 그러나 지역의 도로 표지판 불일치 및 혼잡한 교통 상황으로 인해 다양한 데이터 세트로 훈련된 AI 모델이 요구되고 있습니다.

북미는 성숙하면서도 계속 확장되고 있는 시장입니다. 미국 도로교통안전국(NHTSA)에서 심의 중인 자동 긴급 제동 관련 규정은 이미 대부분의 장거리 운송 차량에서 채택하고 있는 사실상의 표준을 공식화할 것으로 보입니다. 보험사의 텔레다이애그노스틱(원격 진단)은 충돌 회피 사례를 통해 보험금 청구 비용을 30% 절감하는 피드백 루프를 만들어내고, 그 이익을 사업자에게 환원하고 있습니다. 캐나다는 미국의 규정을 따르고 있으며, 국경 간 화물 운송 통로가 규격의 통일을 촉진하고 있습니다. 유럽에서는 2024년 7월부터 ADAS가 의무화되면서 ADAS가 필수 기능으로 자리 잡게 됩니다. 유럽은 운전자 모니터링 분야에서도 선도적인 역할을 하고 있으며, 2026년에는 카메라 기반 피로 감지가 의무화될 예정입니다. 스칸디나비아 국가에서는 겨울철 환경에서 트랙 플래토닝의 검사 운용이 이루어지고 있으며, 눈과 진흙 속에서 센서 퓨전의 내성을 검증하고 있습니다. 동유럽에서는 차량의 노후화로 인해 도입이 늦어지고 있지만, EU의 'Connecting Europe Facility'에 의한 개조에 대한 보조금이 이 격차를 메우는 것을 목표로 하고 있습니다.

남미와 중동에서는 아직 도입 초기 단계에 있습니다. 브라질의 '국가 도로 안전 계획'은 차선 이탈 경보를 권장하고 있지만, 법적 구속력이 있는 도입 시한은 정해져 있지 않습니다. 수소 트럭 도입을 검토 중인 걸프협력회의(GCC) 회원국 차량은 사막의 눈부심에 대응하기 위해 카메라 미러 시스템도 평가했습니다. 각 신흥 지역에서 상용차 ADAS 산업은 높은 수입 관세와 제한된 캘리브레이션 인프라라는 이중 장벽에 직면해 있지만, 센서 비용의 하락으로 2030년까지 점진적으로 시장에 침투할 것으로 예측됩니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Commercial Vehicle ADAS Market size is estimated at USD 13.78 billion in 2025, and is expected to reach USD 29.10 billion by 2030, at a CAGR of 16.13% during the forecast period (2025-2030).

This trajectory reflects the alignment of regulatory mandates, maturing sensor fusion architectures, and the clear economic case for crash-avoidance technology. The Federal Motor Carrier Safety Administration (FMCSA) estimates that every USD 1 spent on advanced driver-assistance systems returns USD 5.09 in crash-related savings, driver retention, and insurance benefits. Radar, camera, and LiDAR costs have fallen steadily since 2024, allowing OEMs to embed sophisticated Level 2 functionality across light, medium, and heavy platforms without a price premium discouraging buyers. At the same time, insurers in North America and Europe now grant average premium discounts of 6-12% for vehicles equipped with forward-collision warning, blind-spot detection, and driver monitoring-a further incentive for fleets navigating razor-thin operating margins.

Global Commercial Vehicle ADAS Market Trends and Insights

Increasing Road-Safety Regulations

National and supranational bodies have converged on a minimum ADAS baseline for new trucks and buses. The European Union's General Safety Regulation obliges advanced emergency braking, intelligent speed assistance, and driver drowsiness warning for all new commercial vehicles sold after July 2024. India will mandate similar functionality for buses and heavy trucks from 2026, elevating the world's second-largest freight market to global best practice. The United States is finalising an automatic emergency-braking requirement that mirrors the FMCSA's own research findings. Harmonised rules are erasing regional engineering divergence, enabling Tier-1 suppliers to develop global hardware-software stacks and capture economies of scale. Over time this legislative pressure removes non-ADAS variants from OEM line-ups, anchoring the commercial vehicle ADAS market as a default safety attribute rather than a discretionary upgrade.

Technological Advances in Autonomous/ADAS Stacks

The transition from Level 2 warning aids to predictive intervention hinges on sensor fusion accuracy and AI-enabled scene interpretation. Sixth-generation radar from Continental brings 360-degree coverage at elevated sampling rates, while Bosch and Microsoft are applying generative AI to classify hazards faster than rule-based algorithms.LiDAR costs have dropped to one-tenth of 2019 levels, and single-photon avalanche diode breakthroughs now give 8 mm range resolution, extending identification capabilities under rain or fog. Thermal imaging paired with 77 GHz radar helps differentiate pedestrians from roadside infrastructure at night. These converging technologies shorten development cycles for Level 3 freight corridors, with Daimler Truck aiming to field SAE Level 4 rigs on US highways by 2027.

High Initial ADAS Component Cost

Despite falling sensor prices, LiDAR still commands four-figure unit costs that owner-operators in Latin America or parts of ASEAN deem prohibitive. Full sensor suites incorporating radar, ultrasonic, and domain controllers add several thousand dollars to a new chassis, eroding the payback horizon for small fleets. The aftermarket faces comparable hurdles: only 30% of repair shops possess alignment bays large enough for camera calibration. Mobileye's 2024 decision to wind down its retrofit division underscored short-term volume limitations. As silicon supply normalises and economies of scale ramp, Tier-2 vendors expect camera modules to decline another 20% in average selling price by 2026, narrowing the affordability gap.

Other drivers and restraints analyzed in the detailed report include:

- Fleet TCO Optimisation Mandates

- Insurance-Telematics-Linked ADAS Incentives

- Retrofit Complexity for Pre-CAN Vehicles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Driver-assistance installations cluster around functions that fleets deem immediately profitable. Adaptive Cruise Control accounted for 24.71% of 2024 revenue, a reflection of proven fuel-efficiency gains during highway platooning. The commercial vehicle ADAS market size for Driver Monitoring Systems is expanding at a 16.72% CAGR because regulators now define fatigue detection as critical. Tier-1 suppliers integrate eye-closure metrics, heart-rate variability, and facial-landmark tracking, turning the cabin into a biometric safety zone.

In parallel, Automatic Emergency Braking adoption accelerated after draft FMCSA rules outlined a 0.45 g minimum deceleration requirement at 40 mph. Blind-spot detection gained momentum once the Eurospec code introduced right-turn cyclist-protection tests. Forward-collision warning remains foundational but is being subsumed into multi-modal fusion stacks that also host night-vision overlays.

With 48.17% revenue share of commercial vehicle ADAS market in 2024, radar remains the backbone of collision mitigation. Price points below USD 50 per short-range module and proven performance in rain keep it indispensable. However, LiDAR is registering a 16.57% CAGR through 2030 as per-unit costs dip below USD 350 and resolution climbs to 200 lines per degree. The Korea Institute of Science and Technology produced single-photon avalanche diodes with 56-picosecond jitter, raising urban mapping fidelity to sub-decimeter levels.

Sensor fusion strategy has moved from redundancy to complementarity. Magna's thermal-radar hybrid extends detection to 200 meters and cuts false positives by 50% compared with radar-only systems. Domain control units manage 10-gigabit per second Ethernet streams, ensuring deterministic latency for collision-avoidance algorithms.

The Commercial Vehicle ADAS Market Report is Segmented by System (Adaptive Cruise Control, Blind Spot Detection, and More), Sensor (Radar, Lidar, and More), Vehicle Type (Light Commercial Vehicles and Medium and Heavy Commercial Vehicles), Distribution Channel (OEM-Fitment and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 38.73% of global commercial vehicle ADAS market revenue share in 2024 and will maintain pole position at a 16.24% CAGR through 2030. China's rapid electrification overlaps Level-2 penetration in new passenger cars, creating a shared supply chain that lowers ADAS costs for trucks. Commercial fleets in Guangdong and Zhejiang provinces deploy forward-collision warning as standard, encouraged by provincial insurance subsidies. Nonetheless, local road-marking inconsistencies and mixed traffic demand AI models trained on heterogeneous data sets.

North America represents a mature yet still expanding arena. Automatic emergency braking legislation under review at the National Highway Traffic Safety Administration will formalise a de facto standard already adopted by most long-haul fleets. Insurance telediagnostics create a feedback loop where crash-avoidable cases trim claim costs by 30%, internalising the benefit for operators. Canada mirrors US rules, and cross-border freight corridors encourage specification parity. Europe's July 2024 blanket requirement cements ADAS as a non-optional feature. The continent also leads on driver-monitoring, with mandatory camera-based fatigue detection scheduled for 2026. Scandinavia pilots truck platooning in winter conditions, stress-testing sensor fusion under snow and slush. Eastern European adoption lags due to an ageing fleet; retrofit subsidies under the EU's Connecting Europe Facility aim to close the gap.

South America and the Middle East remain nascent. Brazil's National Road Safety Plan endorses lane-departure alarms but lacks binding timelines. Gulf Cooperation Council fleets exploring hydrogen trucks also evaluate camera-mirror systems to tackle desert glare. In each emerging region the commercial vehicle ADAS industry faces twin obstacles of high import tariffs and limited calibration infrastructure, although falling sensor costs promise gradual inroads through 2030.

- Bosch

- Continental

- ZF Friedrichshafen

- Autoliv

- Valeo

- Daimler Truck

- Volvo Group

- MAN Truck & Bus

- Scania AB

- HL Mando

- Harman International

- Applied Intuition

- Imagination Technologies

- Vignal Group

- Gauzy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing road-safety regulations

- 4.2.2 Technological advances in autonomous/ADAS stacks

- 4.2.3 Fleet TCO optimisation mandates

- 4.2.4 Insurance-telematics-linked ADAS incentives

- 4.2.5 EU driver-monitoring mandate post-2026

- 4.2.6 Standardised retrofit kits for legacy fleets

- 4.3 Market Restraints

- 4.3.1 High initial ADAS component cost

- 4.3.2 Retrofit complexity for pre-CAN vehicles

- 4.3.3 Urban radar-spectrum congestion

- 4.3.4 Driver disengagement & skills gap

- 4.4 Value / Supply-Chain Analysis

- 4.5 Supplier Landscape

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By System

- 5.1.1 Adaptive Cruise Control

- 5.1.2 Blind Spot Detection

- 5.1.3 Lane Departure Warning System

- 5.1.4 Automatic Emergency Braking

- 5.1.5 Forward Collision Warning

- 5.1.6 Night Vision System

- 5.1.7 Driver Monitoring

- 5.1.8 Tyre-Pressure Monitoring System

- 5.1.9 Head-Up Display

- 5.1.10 Park Assist System

- 5.1.11 Others

- 5.2 By Sensor

- 5.2.1 Radar

- 5.2.2 LiDAR

- 5.2.3 Ultrasonic

- 5.2.4 Image

- 5.2.5 Others

- 5.3 By Vehicle Type

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Medium and Heavy Commercial Vehicles

- 5.4 By Distribution Channel

- 5.4.1 OEM-Fitment

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bosch

- 6.4.2 Continental

- 6.4.3 ZF Friedrichshafen

- 6.4.4 Autoliv

- 6.4.5 Valeo

- 6.4.6 Daimler Truck

- 6.4.7 Volvo Group

- 6.4.8 MAN Truck & Bus

- 6.4.9 Scania AB

- 6.4.10 HL Mando

- 6.4.11 Harman International

- 6.4.12 Applied Intuition

- 6.4.13 Imagination Technologies

- 6.4.14 Vignal Group

- 6.4.15 Gauzy

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment