|

시장보고서

상품코드

2043959

왕겨재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Rice Husk Ash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

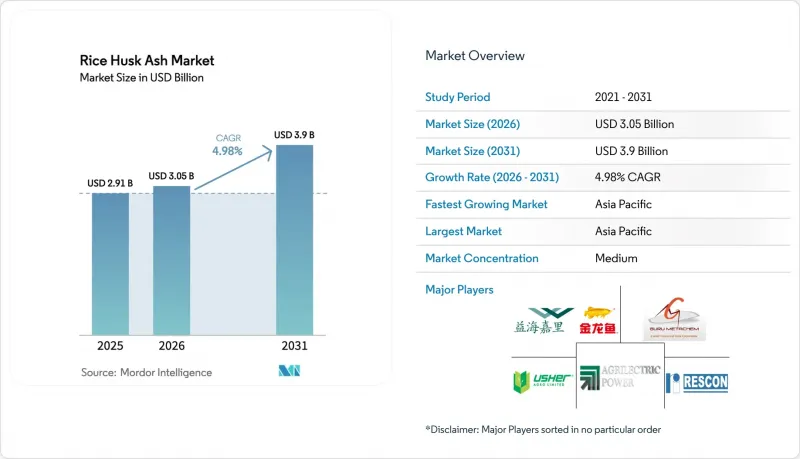

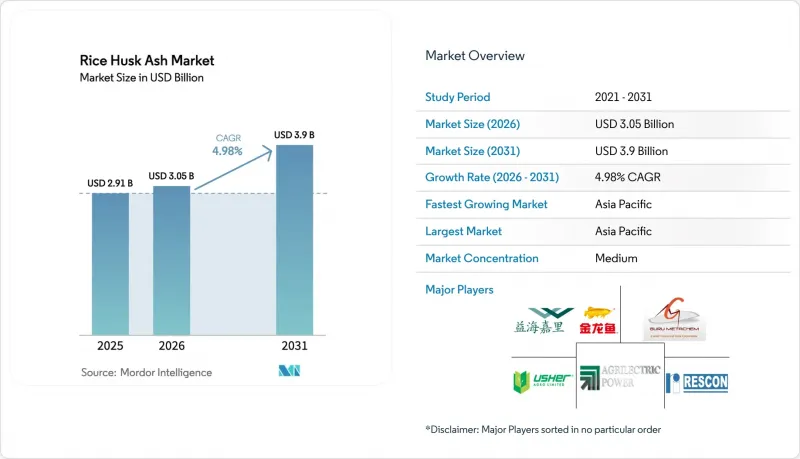

왕겨재 시장 규모는 2025년에 29억 1,000만 달러로 평가되었습니다. 2026년 30억 5,000만 달러에서 2031년까지 39억 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 4.98%를 나타낼 전망입니다.

그린빌딩 의무화, 바이오매스 발전 프로젝트 확대, 첨단 배터리용 초순수 실리카 수요 증가에 힘입어 왕겨재 시장은 저수익 폐기물 관리 부문에서 고부가가치, 사양 중심의 용도로 전환되고 있습니다. 석탄 화력 발전으로 인한 플라이애쉬 공급이 부족해지면서 캘리포니아 주, 유럽 연합(EU), 아시아 일부 지역의 시멘트 제조업체들은 ASTM C618 표준을 준수하는 포졸란을 확보하기 위해 서두르고 있습니다. 한편, 타이어, 내화물, 세라믹 제조업체들은 탄소 함량을 크게 줄이고 기계적 성능을 향상시키는 실리카 함량 90% 이상 등급에 대해 20-40%의 프리미엄을 지불하고 있습니다. 지역 정미업체들은 탄소 잔류량이 4% 이하인 회분을 공급하기 위해 유동층 연소로와 백하우스 필터를 도입하고 있으며, 이를 통해 제3자 품질 인증을 필수로 하는 수출 시장 진출이 가능해졌습니다. 또한, 마그네슘 열환원법의 병행 개발로 하프셀 검사에서 600-2,200 mAh/g의 성능을 발휘하는 다공성 실리콘으로 전환 가능한 배터리 등급 RHA 원료라는 틈새 시장이 빠르게 성장하고 있습니다.

세계의 왕겨재 시장 동향 및 인사이트

SCM 사용을 의무화하는 주류 녹색건축 규제

캘리포니아 주 그린 빌딩 코드, 미국 콘크리트 협회(ACI)의 새로운 성능 기반 탄소 배출 상한선, 곧 발표될 EU 그린딜 조달 지침에 따라 레디믹스트 콘크리트 공급업체들은 포틀랜드 시멘트의 일부를 반응성 시멘트계 재료(SCM)로 대체해야 합니다. SCM)으로 대체해야 합니다. 볏짚 재는 500-700°C에서 연소 시 ASTM C618 클래스 N의 포졸란 기준을 충족합니다. 실험에 따르면, 10-20%의 대체율로 28일 압축강도가 6-25% 향상되고, 콘크리트 1입방미터당 최대 230kg의 이식형 CO2를 줄일 수 있는 것으로 나타났습니다. LEED(Leadership in Energy and Environmental Design) 및 BREEAM(Building Research Establishment Environmental Assessment Methodology) 프레임워크는 현재 바이오 SCM에 대한 추가 크레딧을 부여하고 있으며, 공공 부문 프로젝트 및 유틸리티 사용자 부담 인프라에서 RHA를 풍부하게 포함하는 혼합물에 대한 자금 조달 가능성을 높이고 있습니다. RHA가 풍부한 혼합물의 자금 조달 가능성이 높아지고 있습니다. 캘리포니아, 독일, 싱가포르의 건설업체들은 '천연 포졸란'이 아닌 RHA를 명시적으로 언급하는 입찰 서류를 발행하고 있어 표준화가 가속화되고 있습니다. 이러한 규제와 인센티브를 종합하면 2026-2031년 왕겨재 시장의 CAGR을 약 1.2% 끌어올릴 것으로 예측됩니다.

내화 단열 혼합물의 급속한 보급

내화물 및 철강용 단열재 용도로는 RHA의 열전도율 0.037-0.073 W/m-K의 낮은 열전도율과 1,500°C 이상의 온도에서 안정성을 인정받고 있습니다. 독일 제조업체인 Refratechnik은 RHA를 20% 함유한 발열성 라이저 슬리브를 사용하여 응고 시간을 273초에서 511초로 연장하고, 주조 스크랩을 15% 감소시켰음을 입증했습니다. 현재 일본과 한국의 철강업체들은 12시간 용해 공정에서 용존산소 농도를 ±5ppm 이내로 유지하여 재산화 결함을 감소시키는 탄디쉬용 분말에 RHA를 지정하고 있습니다. 스페인의 한 세라믹 타일 제조업체는 석영을 비정질 RHA 실리카로 대체함으로써 950°C 이하의 소결 온도에서 파단 탄성률이 향상되어 가마의 에너지 소비를 8-12% 절감할 수 있다고 보고했습니다. 내화물용 재의 수익률은 일반 콘크리트용 재보다 30-40% 높으며, 이에 따라 제분업체들은 실리카 순도를 90% 이상으로 높이기 위해 제어 연소 및 후처리에 대한 투자를 촉진하고 있습니다.

RHA 인증에 대한 세계 통일된 기준의 부재

ASTM C618 표준에서는 천연 포졸란에 대해 언급하고 있지만, 왕겨재에 대해서는 규정하지 않아 모든 구매자가 소실감량, 미세도, 강도 및 활성도에 대한 자체 검사를 실시할 수밖에 없는 상황입니다. 유럽의 EN 450-1은 RHA를 완전히 배제하고 있고, 인도의 BIS IS 17225-6은 재의 품질을 정의하지 않아 불신이 생겨 수출 거래에서 거래비용이 10-15% 상승하고 있습니다. 미국 콘크리트 협회(ACI) 표준 323-24는 성능 기반 탄소 배출 상한으로 전환하고 있지만, RHA에 특화된 수용 기준을 규정하지 않아 시장의 불투명성을 조장하고 있습니다. 그 결과, 원래는 확실히 판매할 수 있는 선적물이 제3자 기관의 검사 결과를 기다리는 동안 항만 창고에 머물러 자금 흐름이 지연될 뿐만 아니라 2031년까지의 예상 성장률을 0.6% 낮추고 있습니다.

부문 분석

고순도 재료(SiO2 90% 이상)는 2025년 왕겨재 시장 점유율의 56.67%를 차지하며 CAGR 5.64%를 나타내 저급 재를 압도적으로 능가할 것입니다. 생산자는 쌀 껍질을 500-700°C의 유동층 가마에서 소성 후 산 침출과 공기 분급을 통해 알칼리 금속과 탄소를 제거하여 이 순도를 실현하고 있습니다. 공장도 가격이 톤당 80-150달러인 이 부문은 2배의 프리미엄이 붙지만, 타이어, 내화물, 배터리용 음극재 구매자에게 순도는 양보할 수 없는 요구사항이기 때문에 수요 탄력성이 매우 낮은 상태입니다. 예를 들어, Continental AG는 2025년 ISCC Plus 인증 획득을 위해 석영 유래 실리카를 고순도 RHA 실리카로 대체함으로써 에너지 발자국을 15% 절감할 수 있었다고 밝혔습니다.

90% 이하의 실리카 함량 범주는 절대적인 SiO2 함량보다 반응성과 알칼리성을 중시하는 지역 혼합 시멘트 및 토양 개량제 사용자에게 여전히 중요합니다. 단순 화격자로 및 노천 소성 방식으로 생산되며,(SiO2+Al2O3+Fe2O3)의 합계가 최소 70% 이상이어야 한다는 기준을 충족하기 때문에 납품 가격은 톤당 40-70달러입니다. 방글라데시에서의 농학 검사에서 1헥타르당 1톤의 적용량으로 곡물 수확량이 1헥타르당 5.55톤으로 급증하여 화학비료 수요를 25% 감소시키는 것으로 확인되었습니다.

지역별 분석

아시아태평양은 2025년 43.37%의 점유율로 왕겨재 시장을 장악했으며, 베트남, 태국, 인도, 인도네시아가 전력, 증기, 재를 단일 비즈니스 모델로 수익화하는 통합 정미 및 발전 단지를 확장하고 있어 2031년까지 연평균 복합 성장률(CAGR) 5.25%를 나타낼 것으로 예측됩니다. 태국 아지노모토 공장에서만 연간 6,000만 리터의 디젤 연료를 대체하고, 1만 5,000톤의 고품질 재를 지역 시멘트 가마에 공급하여 식품 가공과 자원 회수의 시너지를 발휘하고 있습니다. 2025년 4월 가동을 시작한 베트남 하우장 공장은 20MW급 터빈과 ISO 인증을 획득한 재 포장라인을 결합하여 지역 내 모범사례가 되고 있습니다.

북미는 규모는 작지만 전략적 움직임이 보입니다. 농업전력파트너는 2025년 초에 고반응성 재를 대상으로 한 연구개발을 위해 미화 10만 달러를 조달하고, 하이록에너지그룹은 2025년 11월에 27MW 규모의 와담에너지 발전소를 인수했습니다. 이는 장기적으로 리스크가 감소된 바이오매스 자산에 대한 투자자들의 의지를 보여줍니다. 캘리포니아 주 그린 빌딩 코드에 따라 유틸리티에서 ASTM 표준을 준수하는 포졸란 사용을 의무화하면서 센트럴 밸리는 시멘트와 내화물 라인 모두에 있어 주요 공급 기지로 변모하고 있습니다.

유럽의 동향은 규제와 밀접하게 얽혀 있습니다. '산업 배출 지침'에 따라 1MW 이상의 발전소에는 백필터 또는 정전 집진기 설치가 의무화되어 있으며, 이는 1MW당 5만-20만 유로의 비용이 소요됩니다. 이탈리아나 스페인의 소규모 가족 경영 기업들은 이 비용을 정당화하기 어려운 상황입니다. 2025년에 설비를 갱신한 독일 제분소는 설비 투자 비용을 충당하기 위해 현재 8-12유로의 프리미엄 가격으로 재를 판매하고 있으며, 그 순도 수준은 종종 아시아 표준을 초과하여 내화물 부문의 골격을 구축하고 있습니다. 남미와 아프리카는 여전히 개발 중입니다. 브라질의 순환경제 관련 법령과 이집트의 혼소 검사, 일관된 보조금 제도가 마련된다면 성장의 계기가 될 수 있지만, 인프라와 기준의 격차가 여전히 국경을 넘나드는 유통을 가로막고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO용 중요 전략적 과제

KTH 26.05.29The Rice Husk Ash Market size is projected to be USD 2.91 billion in 2025, USD 3.05 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 4.98% from 2026 to 2031.

Supported by green-building mandates, larger biomass-power pipelines, and expanding demand for ultra-high-purity silica in advanced batteries, the rice husk ash market is shifting from a low-margin waste-management outlet toward premium, specification-driven applications. Cement producers in California, the European Union (EU), and parts of Asia are rushing to secure ASTM C618-compliant pozzolans as coal-fired fly-ash supplies tighten, while tire, refractory, and ceramic manufacturers are paying 20-40% premiums for Greater than or equal to 90% silica grades that slash embodied carbon and improve mechanical performance. Regional rice-mill operators are installing fluidized-bed combustors and baghouse filters to deliver ash with carbon residues below 4%, enabling entry to export markets that insist on third-party quality certification. Parallel developments in magnesiothermic reduction are opening a niche but fast-growing lane for battery-grade RHA feedstock that can be converted into porous silicon delivering 600-2,200 mAh/g in half-cell testing.

Global Rice Husk Ash Market Trends and Insights

Mainstream Green-Building Regulations Mandating SCMs

California's Green Building Code, the American Concrete Institute's new performance-based carbon ceilings, and forthcoming EU Green Deal procurement guidelines are forcing ready-mix suppliers to swap a portion of Portland cement for reactive supplementary cementitious materials. Rice husk ash meets ASTM C618 Class N pozzolan criteria when combusted at 500-700°C; trials show a 6-25% gain in 28-day compressive strength at 10-20% replacement rates while trimming embodied CO2 by up to 230 kg per cubic meter of concrete. LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method) frameworks now award additional credits for bio-based SCMs, reinforcing bankability for RHA-rich mixes on public-sector projects and utility-ratepayer-funded infrastructure. Builders in California, Germany, and Singapore are issuing bid documents that reference RHA outright rather than "natural pozzolan," accelerating standardization. Taken together, these codes and incentives add an estimated 1.2 percentage-point lift to the 2026-2031 CAGR of the Rice Husk Ash market.

Rapid Adoption in Refractory Insulating Mixes

Refractory and steel-insulation applications value RHA's low thermal conductivity of 0.037-0.073 W/m*K and stability above 1,500°C. German producer Refratechnik showed that exothermic riser sleeves with 20% RHA extended solidification time from 273 s to 511 s, cutting casting scrap by 15%. Steelmakers in Japan and South Korea now specify RHA in tundish powders that hold dissolved oxygen within +-5 ppm over 12-hour heats, mitigating reoxidation defects. Ceramic-tile manufacturers in Spain report modulus-of-rupture gains at sintering temperatures below 950°C when substituting quartz with amorphous RHA silica, a shift that saves 8-12% in kiln energy. Margins on refractory-grade ash stand 30-40% above commodity concrete ash, encouraging mills to invest in controlled combustion and post-treatment that elevate silica purity past 90%.

Lack of Globally Harmonized RHA Certification Norms

ASTM C618 mentions natural pozzolans but stops short of codifying rice husk ash, forcing every buyer to run bespoke loss-on-ignition, fineness, and strength-activity tests. Europe's EN 450-1 omits RHA entirely, while India's BIS IS 17225-6 leaves ash quality undefined, creating distrust that raises transaction costs by 10-15% on export deals. The American Concrete Institute's Code 323-24 moves to performance-based carbon caps but provides no RHA-specific acceptance criteria, perpetuating market opacity. As a result, otherwise bankable shipments are stuck in port warehouses awaiting third-party lab results, delaying cash cycles and shaving 0.6 percentage points off expected growth through 2031.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biomass-Power Co-Generation at Rice Mills

- Government Subsidies for Agro-Waste Valorization

- Competition from Cheaper Fly Ash in Price-Sensitive Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-purity material (greater than or equal to 90% SiO2) captured 56.67% rice husk ash market share in 2025 and is expanding at a 5.64% CAGR, decisively outpacing lower-grade ash. Producers achieve these purities by burning husk in fluidized-bed kilns at 500-700°C, then applying acid leaching and air classification to strip alkali metals and carbon. At ex-works prices of USD 80-150 per ton, the segment commands a 2 times premium yet experiences minimal demand elasticity because buyers in tires, refractories, and battery anodes view purity as non-negotiable. Continental AG, for instance, cited a 15% lower energy footprint when swapping quartz-derived silica for high-purity RHA silica during its ISCC Plus certified roll-out in 2025.

The less than 90% silica category remains important for regional blended-cement and soil-amendment users that value reactivity and alkalinity over absolute SiO2 content. Delivered costs land at USD 40-70 per ton, underpinned by simple grate furnaces or open-air burning that still meet a minimum 70% combined (SiO2 + Al2O3 + Fe2O3) threshold. Agronomic trials in Bangladesh recorded a jump in grain yield to 5.55 tonnes per hectare with a 1-tonne per hectare application rate, cutting chemical fertilizer demand by 25%.

The Rice Husk Ash Market Report is Segmented by Silica Content (Greater Than or Equal To 90% Silica and Less Than 90% Silica), Application (Cement and Concrete Additive, Silica, Ceramics and Refractories, Steel - Insulating Covers, Rubber and Plastics Filler, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the Rice Husk Ash market with 43.37% share in 2025 and is forecast to post a 5.25% CAGR through 2031 as Vietnam, Thailand, India, and Indonesia scale integrated rice-mill-power complexes that monetize electricity, steam, and ash in a single business model. Thailand's Ajinomoto plants alone displace 60 million liters of diesel fuel annually and funnel 15,000 tons of high-grade ash into regional cement kilns, illustrating the synergy between food processing and materials recovery. Vietnam's Hau Giang facility, commissioned in April 2025, serves as a regional blueprint by coupling a 20 MW turbine with ISO-certified ash packaging lines.

North America commands a smaller footing yet showcases strategic moves: Agrilectric Power Partners raised USD 100,000 in early 2025 for research and development aimed at high-reactivity ash, and High Rock Energy Group acquired the 27 MW Wadham Energy plant in November 2025, signaling investor appetite for long-lived, de-risked biomass assets. California's Green Building Code, which now stipulates ASTM-compliant pozzolans in public projects, is turning the Central Valley into a premium supplier corridor for both cement and refractory lines.

Europe's trajectory is intertwined with regulation. The Industrial Emissions Directive forces mills above 1 MW to install baghouses or electrostatic precipitators, a EUR 50,000-200,000 per-MW ticket that smaller, family-owned operations in Italy and Spain struggle to justify. German mills that upgraded in 2025 are now selling ash at an EUR 8-12 premium to cover capex, yet purity levels often exceed Asian benchmarks, giving them a foothold in refractory niches. South America and Africa remain nascent; Brazil's circular-economy statutes and Egypt's co-firing trials could unlock growth once consistent subsidy frameworks are in place, but infrastructure and standards gaps still curtail cross-border flows.

- AC2N THAILAND CO., LTD.

- Agrilectric Power Partners

- Astrra Chemicals

- Enpower Corp.

- Global Recycling

- Guru Metachem Pvt. Ltd.

- JASORIYA RICE MILL

- Ketan Chemicals Corp.

- Rescon

- Rice Husk Ash (Thailand)

- Usher Agro Ltd.

- Yihai Kerry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream green-building regulations mandating SCMs

- 4.2.2 Rapid adoption in refractory insulating mixes

- 4.2.3 Expansion of biomass-power co-generation at rice mills

- 4.2.4 Government subsidies for agro-waste valorisation (India, Thailand)

- 4.2.5 Niche demand for ultra-high-purity RHA in Li-ion battery silicon anodes

- 4.3 Market Restraints

- 4.3.1 Lack of globally harmonised RHA certification norms

- 4.3.2 Competition from cheaper fly-ash in price-sensitive regions

- 4.3.3 Tightening particulate-emission limits for biomass boilers (EU IED)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Silica Content

- 5.1.1 Greater than or equal to 90% Silica

- 5.1.2 Less than 90% Silica

- 5.2 By Application

- 5.2.1 Cement and Concrete Additive

- 5.2.2 Silica

- 5.2.3 Ceramics and Refractories

- 5.2.4 Steel - Insulating Covers

- 5.2.5 Rubber and Plastics Filler

- 5.2.6 Other Applications (Agriculture and Fertilisers, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AC2N THAILAND CO., LTD.

- 6.4.2 Agrilectric Power Partners

- 6.4.3 Astrra Chemicals

- 6.4.4 Enpower Corp.

- 6.4.5 Global Recycling

- 6.4.6 Guru Metachem Pvt. Ltd.

- 6.4.7 JASORIYA RICE MILL

- 6.4.8 Ketan Chemicals Corp.

- 6.4.9 Rescon

- 6.4.10 Rice Husk Ash (Thailand)

- 6.4.11 Usher Agro Ltd.

- 6.4.12 Yihai Kerry

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment