|

시장보고서

상품코드

2043960

액침 냉각액 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Immersion Cooling Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

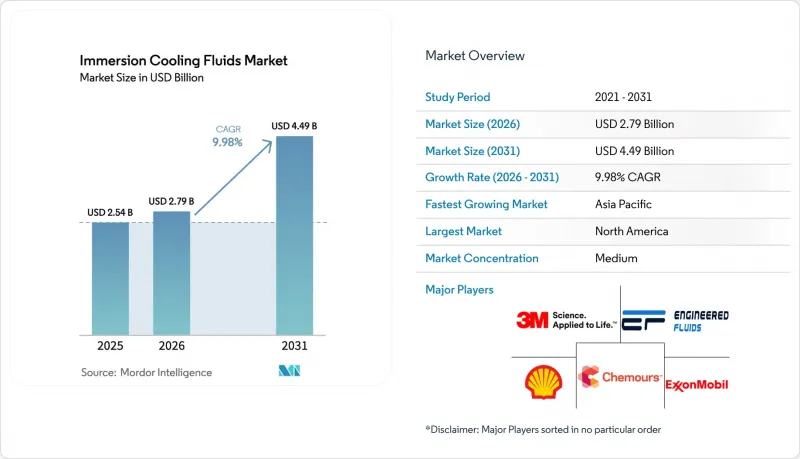

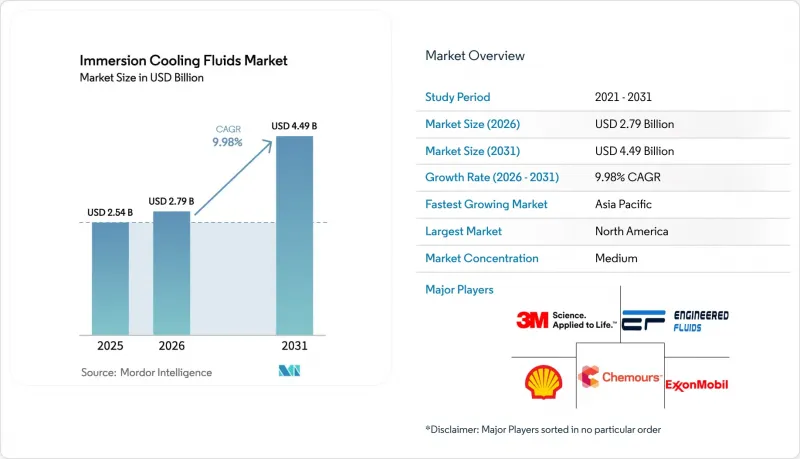

액침 냉각액 시장 규모는 2025년 25억 4,000만 달러로 평가되었습니다. 2026년 27억 9,000만 달러에서 2031년까지 44억 9,000만 달러로 확대되며 2026-2031년까지 연평균 복합 성장률(CAGR)은 9.98%를 나타낼 전망입니다.

30kW 이상의 랙 밀도 증가, 하이퍼스케일 사업자들이 캠퍼스당 400MW 이상의 AI 클러스터로 전환하고, 폐열을 수익화하는 지역난방 프로그램이 데이터센터의 경제성을 재정의하고 있습니다. 북미와 유럽에서 PFAS 화합물 단계적 폐지를 위한 규제 시한이 다가옴에 따라 구매자들이 PFAS가 없는 합성유와 에스테르로 전환하고 있는 가운데, 인텔의 2025년 Shell 및 ExxonMobil 유체 인증은 하이퍼스케일 도입에 있어 주요 장벽을 제거했습니다. 그 결과, 광유에서 리터당 2-5달러의 단상 시스템이 도입 용량의 대부분을 차지했지만, 현재는 PFAS가 없는 불소계 대체품이 가장 빠르게 성장하는 화학계가 되었습니다. 점유율이 12% 이상의 업체가 없어 경쟁은 여전히 치열하지만, 정제 규모와 칩 제조업체의 지지를 겸비한 공급업체가 영향력을 강화하고 있습니다.

세계의 액침 냉각액 시장 동향 및 인사이트

에너지 효율 및 PUE 최적화에 대한 압박감 증가

PUE를 1.15 이하로 유지하려는 사업자에게 랙 밀도가 30kW를 초과하면 공랭식 냉각 방식에서는 큰 페널티가 발생합니다. 단상 침수 냉각은 팬과 냉각기의 부하를 줄여 PUE를 1.05-1.15로 낮추고, 2상 냉각은 1.02-1.08을 달성합니다. 2025년 7월 마이크로소프트가 모든 데이터센터에 직접 수냉을 도입한 것과 콜로보어가 랙당 200kW 용량을 확보하기 위해 9억 2,500만 달러의 자금을 조달한 것은 파일럿 단계에서 표준 엔지니어링으로 전환하는 것을 보여줍니다. Dell'Oro Group의 조사에 따르면, 2025년 수냉식 시장은 전년 대비 85%의 성장을 기록했지만, 수냉식 냉각은 여전히 DTC(Direct-to-Chip)로의 개조가 이루어지지 않았다고 합니다. 유럽데이터센터협회(EDCA)의 조사에 따르면, 2024년 액침냉각 도입률은 5.6%에 불과하며, 전환에 5-10년이 소요될 것으로 예상하고 있습니다. 인텔과 Shell의 검사에서 최대 48%의 에너지 절약, 30%의 CO2 절감, 99%의 물 사용량 감소가 확인되어 기업의 과학에 의한 목표에 부합하는 것으로 나타났습니다.

지속가능성과 탄소 중립 목표가 도입 가속화

지역열 공급 프로그램에서는 공급열 가격이 1MWh당 12-22유로(약 1만2000원)로 책정되어 가스보일러보다 약 50% 저렴하게 공급됩니다. AWS Talart는 2024년 트리니티 칼리지 더블린의 난방 수요의 92%를 공급하여 704톤의 CO2를 절감했습니다. 이는 수익성 높은 열 공급을 입증하는 계기가 되었습니다. 마이크로소프트와 포르탐의 핀란드 계획은 2026년까지 25만 명의 주민들에게 서비스를 제공할 예정입니다. 싱가포르에서는 PUE 1.3 이하와 재생에너지 조달이 의무화되면서 STT GDC의 수냉이 촉진되고 있습니다. 메타의 650억 달러 규모의 AI 시설 건설과 구글의 400억 달러 규모의 텍사스 주 계획은 모두 수냉식을 명시하고 있으며, 코로케이션 사업자에게는 kW당 20-40%의 가격 우위를 가져다 줄 수 있습니다.

PFAS 규제를 둘러싼 재료의 적합성 및 안전성 문제

탄화수소계 냉각제는 특정 엘라스토머를 부식시킬 수 있어 부품별 검증이 필수적입니다. 카길의 FR3는 생분해성이지만, 고온의 고온부위를 발생시켜 수익성이 낮은 설계에서는 수명주기를 단축시킬 수 있습니다. 2상 탱크는 밀폐된 밀봉이 요구됩니다. 미세한 누출은 성능을 현저히 저하시키고, 유체가 가연성일 경우 화재 위험을 증가시킵니다. 장기적인 실제 데이터가 부족하기 때문에 Shell과 ExxonMobil은 2025년에야 비로소 인텔의 테스트를 통과했습니다. 위험회피적인 BFSI(은행, 금융, 보험) 사용자들은 전환을 미루고 있습니다. EU와 미국의 규정이 다르기 때문에 지역별로 혼합이 필요하고, SKU 수와 비용이 증가하고 있습니다.

부문 분석

2025년 인텔이 Shell과 ExxonMobil의 배합액에 대한 지지를 바탕으로 합성 탄화수소는 액침 냉각액 시장에서 37.12%의 점유율을 차지했습니다. Chemours, Solvay, Dow에 의해 PFAS가 없는 하이드로플루오로에테르로 재출시된 불소계 유체는 예측 기간(2026-2031년) 동안 CAGR 10.22%를 나타낼 것으로 예측됩니다. 미네랄 오일은 리터당 2-5달러의 가격대와 6-12개월의 투자 회수 기간으로 인해 암호화폐 채굴자들의 지지를 받고 있습니다. 한편, 천연 에스테르 혼합은 IEC 62770 표준을 준수하지만 발열량이 높아 HPC(고성능 컴퓨팅) 부문에서의 채택이 억제되고 있습니다. 다이나린, 엔지니어링 유체 등 엔지니어링 공급업체는 맞춤형 요구의 격차를 해소하여 높은 수익률을 실현하고 있습니다.

2025년 액침 냉각액 시장 규모에서 단상 시스템은 64.44%를 차지하며 10.36%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. 이는 낮은 자본 비용(기밀 밀봉이 필요 없음), 간단한 유체 관리(증발 제어가 필요 없음), 50-60°C의 입구 온도에 대응하는 지역 열 공급 네트워크와 호환되는 것을 반영합니다. 100kW 이상의 랙에서는 여전히 2상 방식이 필수적이며, Accelsius의 파이프라인과 PUE 1.02-1.08을 달성한 DarkNX의 온타리오주 300MW 캠퍼스가 이를 입증한 사례입니다. 그러나 밀폐 설계의 복잡성과 냉매 관리의 어려움으로 인해 현재로서는 2상 방식의 채택은 틈새 시장에 머물러 있습니다.

지역별 분석

북미는 Meta의 650억 달러 규모의 AI 인프라 구축과 구글의 400억 달러 규모의 텍사스 주 프로젝트가 2025년 매출의 41.18%를 차지하며 시장을 주도했습니다. 아시아태평양은 싱가포르의 그린 데이터센터 규제, 일본 시장 CAGR 9.6%, 인도 200kW 랙 도입에 힘입어 10.45%의 예측 CAGR을 보이고 있습니다. 유럽에서는 폐열의 효율적 활용이 진행되고 있으며, AWS Talart는 2024년 704톤의 CO2를 감축하고, Microsoft와 Fortum은 2026년까지 25만 명의 핀란드인에게 난방을 공급할 계획이며, 이를 통해 사업자의 ROI가 15-25% 향상될 것으로 예상했습니다. 라틴아메리카와 중동은 두 자릿수 성장을 기록했지만, 유해물질 규제와 인력 부족으로 수냉식 서버의 도입 속도가 둔화되고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO용 중요 전략적 과제

KTH 26.05.29The Immersion Cooling Fluids Market size is projected to expand from USD 2.54 billion in 2025 and USD 2.79 billion in 2026 to USD 4.49 billion by 2031, registering a CAGR of 9.98% between 2026 and 2031. Growing rack densities that exceed 30 kilowatts, hyperscale operators' shift toward AI clusters above 400 MW per campus, and district-heating programs that monetize waste heat are redefining data-center economics. Regulatory deadlines phasing out PFAS compounds in North America and Europe are steering buyers toward PFAS-free synthetics and esters, while Intel's 2025 certification of Shell and ExxonMobil fluids removed a key hurdle for hyperscale adoption. As a result, single-phase systems priced at USD 2-5 per liter for mineral oils dominate installed capacity, yet fluorinated alternatives, now PFAS-free, are the fastest-growing chemistry. Competitive intensity remains high because no vendor holds more than 12% share, but suppliers that combine refining scale with chip-maker endorsements are consolidating influence.

Global Immersion Cooling Fluids Market Trends and Insights

Rising Energy-Efficiency and PUE Optimization Pressures

Operators pushing PUE below 1.15 face steep air-cooling penalties once rack densities top 30 kW. Single-phase immersion reduces fan and chiller loads, delivering a PUE of 1.05-1.15, while two-phase achieves 1.02-1.08. Microsoft's fleetwide rollout of direct liquid cooling in July 2025 and Colovore's USD 925 million financing for 200 kW-per-rack capacity mark a shift from pilot to baseline engineering. Dell'Oro Group recorded 85% year-over-year liquid-cooling growth in 2025, although immersion still trails direct-to-chip retrofits. The European Data Centre Association measured only 5.6% immersion adoption in 2024, underscoring a five-to-ten-year conversion window. Intel-Shell tests confirmed up to 48% energy savings, 30% CO2 reduction, and 99% lower water use, aligning with corporate science-based targets.

Sustainability and Carbon-Neutral Targets Accelerate Adoption

District-heating programs price delivered heat at EUR 12-22 per MWh, undercutting gas boilers by roughly 50%. AWS Tallaght supplied 92% of Trinity College Dublin's heating and cut 704 tons of CO2 in 2024, proving revenue-positive heat export. Microsoft-Fortum's Finland scheme will reach 250,000 residents by 2026. Singapore's moratorium lift now mandates PUE less than 1.3 and renewable sourcing, stimulating liquid cooling at STT GDC. Meta's USD 65 billion AI build and Google's USD 40 billion Texas plan both specify liquid cooling, giving colocation operators pricing power premiums of 20-40% per kilowatt.

Material Compatibility and Safety Concerns Amid PFAS Regulation

Hydrocarbon coolants can attack certain elastomers, forcing component-by-component validation. Cargill FR3 is biodegradable but creates hotter spots, potentially shortening lifecycle in tight-margin designs. Two-phase tanks demand hermetic sealing; micro-leaks slash performance and raise fire risk when fluids are flammable. Absent long-term field data, Shell and ExxonMobil only cleared Intel tests in 2025; risk-averse BFSI users defer conversion. Divergent EU and U.S. rules oblige region-specific blends, inflating SKUs and cost.

Other drivers and restraints analyzed in the detailed report include:

- Stricter PFAS-Phase-Out Deadlines Reshape Fluid Chemistries

- Growing Edge-Micro-Data-Centers in Untapped Emerging Markets

- Limited Standards / Inter-Operability Across OEM Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic hydrocarbons captured 37.12% of the Immersion Cooling Fluids market share in 2025, buoyed by Intel's endorsement of Shell and ExxonMobil formulas. Fluorinated fluids, relaunched as PFAS-free hydrofluoroethers by Chemours, Solvay, and DOW, are forecast for a 10.22% CAGR during the forecast period (2026-2031). Mineral oils keep crypto miners loyal thanks to USD 2-5 per-liter pricing and 6-12 month paybacks, while natural-ester blends meet IEC 62770 yet run hotter, curbing HPC uptake. Engineered suppliers such as Dynalene and Engineered Fluids fill customization gaps at premium margins.

Single-phase accounted for 64.44% of the Immersion Cooling Fluids market size in 2025 and should grow at a 10.36% CAGR, reflecting their lower capital cost (no hermetic sealing required), simpler fluid management (no evaporation control), and compatibility with district-heating networks that accept 50-60°C inlet temperatures. Two-phase remains essential for racks above 100 kW, demonstrated by Accelsius pipelines and DarkNX's 300 MW Ontario campus hitting PUE 1.02-1.08. However, hermetic design complexity and refrigerant management keep the two-phase adoption niche today.

The Immersion Cooling Fluids Market Report is Segmented by Fluid Type (Synthetic Hydrocarbon Oils, and More), Cooling Type (Single-Phase Immersion Cooling and More), Application (Data Centers - Hyperscale, and More), End-User Industry (IT and Telecom, BFSI, and Mores), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 41.18% of 2025 revenue owing to Meta's USD 65 billion AI build and Google's USD 40 billion Texas project. Asia-Pacific shows a 10.45% forecast CAGR, catalyzed by Singapore's green-data-center rules, Japan's 9.6% market CAGR, and India's 200 kW-rack deployments. Europe monetizes waste heat, AWS Tallaght cut 704 tons of CO2 in 2024, and Microsoft-Fortum will heat 250,000 Finns by 2026, creating 15-25% better ROI for operators. Latin America and the Middle East record double-digit growth but struggle with hazmat regulations and skills shortages, slowing immersion ramp.

List of Companies Covered in this Report:

- 3M

- AGC Inc.

- Cargill

- Castrol Limited (BP)

- Chevron Oronite

- DOW

- Dynalene Inc.

- Engineered Fluids

- ExxonMobil Corporation

- FUCHS

- Lubrizol

- M&I Materials Ltd

- Shell plc

- Solvay

- The Chemours Company

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising energy-efficiency and PUE optimization pressures

- 4.2.2 Sustainability and carbon-neutral targets accelerate adoption

- 4.2.3 Stricter PFAS-phase-out deadlines reshape fluid chemistries

- 4.2.4 Growing edge-micro-data-centers in untapped emerging markets

- 4.2.5 Heat-to-heat-re-use initiatives driving district-heating integration

- 4.3 Market Restraints

- 4.3.1 Material compatibility and safety concerns amid PFAS regulation

- 4.3.2 Limited standards/inter-operability across OEM ecosystems

- 4.3.3 Volatility in synthetic base-oil supply chain post-3M exit

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fluid Type

- 5.1.1 Synthetic Hydrocarbon Oils

- 5.1.2 Mineral Oils

- 5.1.3 Fluorinated Fluids

- 5.1.4 Esters / Bio-based and Biodegradable Fluids

- 5.1.5 Other Fluid Types

- 5.2 By Cooling Type

- 5.2.1 Single-phase Immersion Cooling

- 5.2.2 Two-phase Immersion Cooling

- 5.3 By Application

- 5.3.1 Data Centers - Hyperscale

- 5.3.2 Data Centers - Colocation

- 5.3.3 Data Centers - Enterprise

- 5.3.4 Crypto-mining/Blockchain

- 5.3.5 HPC and AI Training Clusters

- 5.3.6 Power Electronics and Industrial Computing

- 5.3.7 EV Fast-charging and Battery Thermal Management

- 5.3.8 Other Applications

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Energy and Utilities

- 5.4.5 Automotive and Transportation

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 Singapore

- 5.5.1.5 South Korea

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Cargill

- 6.4.4 Castrol Limited (BP)

- 6.4.5 Chevron Oronite

- 6.4.6 DOW

- 6.4.7 Dynalene Inc.

- 6.4.8 Engineered Fluids

- 6.4.9 ExxonMobil Corporation

- 6.4.10 FUCHS

- 6.4.11 Lubrizol

- 6.4.12 M&I Materials Ltd

- 6.4.13 Shell plc

- 6.4.14 Solvay

- 6.4.15 The Chemours Company

- 6.4.16 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment