|

시장보고서

상품코드

2043961

불용성 유황 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Insoluble Sulfur - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

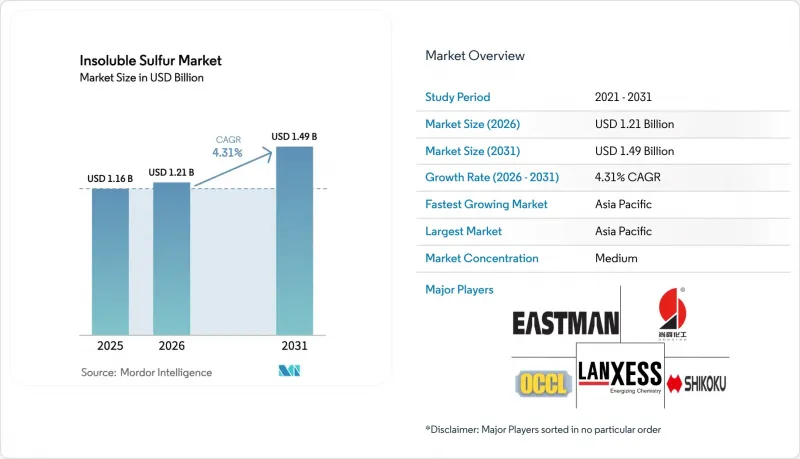

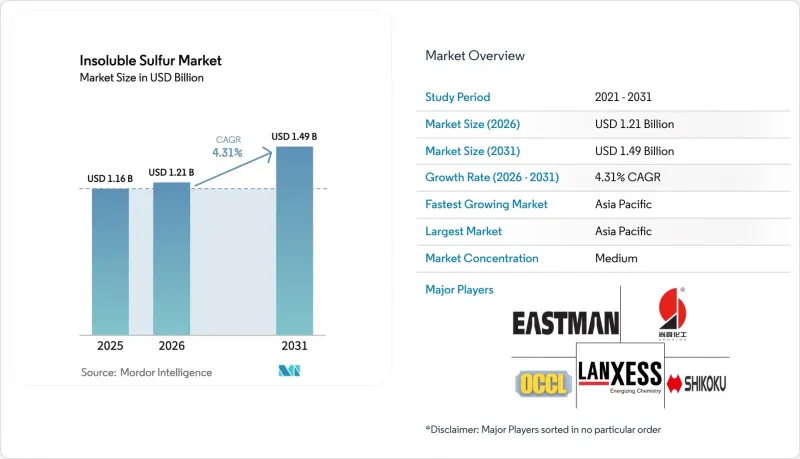

불용성 유황 시장 규모는 2025년 11억 6,000만 달러로 평가되었습니다. 2026년 12억 1,000만 달러로 확대되어 2031년까지 14억 9,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 4.31%를 나타낼 전망입니다.

타이어의 방사형화, 전기자동차(EV) 보급률 증가, 프리미엄 고분산 등급으로의 전환으로 원소유황 가격 상승에 따른 수익률 압박에도 불구하고 수요 회복력이 강화되고 있습니다. 중국의 생산능력 증설과 연속공정 제조의 도입으로 비용 곡선이 재편되고 있는 반면, 유럽과 미국공급업체들은 EV용 타이어를 위한 저탄소 및 고안정성 배합에 집중하고 있습니다. 중견 컴파운더들이 기술 지원과 적시 납품을 요구하면서 대리점 중심의 판매가 확대되고 있으며, 산업용 고무 제품은 광업과 인프라 투자의 수혜를 받고 있습니다. 이황화탄소(CS2) 노출에 대한 규제 당국의 감시와 지속 가능한 원료에 대한 탐색으로 인해 자본 수요는 높은 수준으로 유지될 것이며, 장기적으로 가격 규율이 유지될 것으로 예측됩니다.

세계의 불용성 유황 시장 동향 및 인사이트

전 세계 OEM 및 교체용 타이어 생산 수요 급증

중국에서는 2024년 11억 9,000만 개의 타이어가 생산되어 전년 대비 9.2% 증가했습니다. 한편, 차량 노후화에 따른 주행거리 증가로 교체용 타이어에 대한 수요도 꾸준히 증가하고 있습니다. 태국이 미국 승용차 타이어 수입의 40.38%를 차지하는 등 동남아시아가 타이어 수출에서 주도적인 위치를 차지하고 있기 때문에 이 지역 수요는 견조하게 유지되고 있습니다. 레이디얼 타이어는 바이어스 타이어에 비해 불용성 유황이 약 1.7배 더 많이 필요하기 때문에 타이어의 현대화에 따른 수요 증가가 촉진되고 있습니다. 관세를 피하기 위해 공장을 이전하는 타이어 제조업체로 인해 화학제품 수입이 증가하고 국제 주문이 가속화되고 있습니다. 이러한 구조적 요인과 순환적 요인이 결합하여 불용성 유황 시장 수요를 뒷받침하고 있습니다.

EV 전용 저회전저항 컴파운드로의 전환

EV용 타이어는 더 무거운 하중을 지탱하고 더 긴 항속거리를 실현해야 합니다. 따라서 실리카가 풍부하고 구름 저항이 낮은 화합물에 의존하고 있으며, 불용성 유황은 블룸(표면 미백)을 방지하고 열 안정성을 보장하기 위해 필수적입니다. 이스트만사가 더블코인과 공동 개발한 'Crystex Cure Pro'는 유동성과 분산성을 향상시켜 혼련시간 단축과 가황온도 감소를 가능하게 하여 에너지 절약과 배출가스 감소를 실현합니다. Flexsys에 따르면, Flexsys의 'Cure Pro Malaysia' 등급은 기존 HD-OT20에 비해 제품의 탄소 발자국을 10% 감소시켜 OEM(자동차 제조업체)의 Scope 3 목표 달성을 돕습니다. 2024년 신에너지 자동차 판매 점유율이 41%에 달하는 중국 내 전기차 보급 확대에 따라 2031년까지 프리미엄 불용성 유황 등급 판매량은 두 자릿수 성장이 예상됩니다.

휘발성 원소 유황 및 CS2 가격 동향

러시아가 수출 금지 조치를 연장하고 중동 생산자들이 인도네시아 니켈 프로젝트로 공급을 전환함에 따라 2026년 1월 중국 FOB 황 가격은 톤당 571달러로 2024년 1월 대비 4배 상승했습니다. 유황은 인산 비료 비용의 절반 이상을 차지하기 때문에 비료 수요는 화학 원료 구매자와 직접적으로 경쟁하게 됩니다. 랑세스는 수익률을 유지하기 위해 2026년 3월에 첨가제 가격을 최대 50% 인상했습니다. 장기 유황 계약을 체결하지 않은 생산자들은 수익률 압박과 운전자금 압박에 직면해 있습니다.

부문 분석

일반 오일 충전 등급(OT33/OT10)은 바이어스 타이어 및 교체용 타이어의 비용 우위로 인해 불용성 유황 시장에서 33.47%의 점유율을 차지하고 있습니다. 일반 등급의 불용성 유황 시장 규모는 여전히 가장 크지만, 특히 OEM의 지속가능성 요구 사항으로 인해 제품의 탄소 발자국을 줄여야 하는 분야에서는 프리미엄 등급이 추가 수익률을 얻고 있습니다. 고분산 프리미엄(HD-OT20) 등급은 낮은 구름성과 우수한 열 안정성이 요구되는 EV용 타이어 수요에 힘입어 CAGR 4.58%로 가장 높은 성장률을 기록했습니다. Flexsys의 Crystex HD OT 20은 불용성 유황을 72% 이상 함유하고 있으며, 105°C에서 15분 동안 안정성을 유지합니다. 이스트만의 'Cure Pro' 시리즈는 더 낮은 반죽 속도로 사용할 수 있어 최대 10%의 에너지를 절약할 수 있습니다.

저유분 및 무유분 등급은 고실리카 함유 EV용 컴파운드에서 보급이 진행되고 있습니다. 2025년 출시된 랑세스의 'Aflux SD'는 실리카의 분산성과 습식 그립을 향상시키는 제품입니다. Flexsys의 'XD' 등급은 전체 제조 공정(크레이드 투 게이트)에서 1kg당 1.23톤의 CO2를 배출해 저탄소 타이어의 입지를 강화하고 있습니다. 연속 생산 능력을 갖춘 공급업체는 신속하게 등급을 전환할 수 있어 컴파운더의 다양한 요구 사항을 충족하고 설비 가동률을 최적화할 수 있습니다.

지역별 분석

아시아태평양은 2025년 시장 규모의 56.25%를 차지하며, 중국의 타이어 생산 확대와 EV 보급에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 5.14%를 나타낼 것으로 예측됩니다. 중국 선샤인은 불용성 유황 생산능력을 연간 6만 톤으로 확대했지만, 공급과잉으로 인해 2024년 가동률은 68% 내외에 머물렀습니다. 산동양곡화태가 2022년 연간 4만톤의 생산능력을 증설함에 따라 2024년 중반까지 평균 판매가격이 24% 하락했습니다. 태국의 천연고무 우위와 베트남의 타이어 공장 증가는 이 지역 수요를 촉진하고 있습니다. 인도는 국내 자동차 시장의 성장에 대응하기 위해 생산능력을 확충하고 있지만, 여전히 수입에 의존하고 있어 지역 내 신규 생산업체에 대한 투자 여지가 남아있습니다.

북미에서는 랑세스의 부쉬 파크 확장 공장의 혜택을 누리고 있으며, 2025년 11월에 새로운 가공 촉진제 라인이 가동되었습니다. 현지 생산을 통해 지정학적 긴장 상황에서도 출하 기간 단축과 공급 안정성을 향상시킬 수 있습니다. 플렉스시스(Flexsys)는 Scope 3 배출량 감축을 목표로 국내 OEM 업체에 공급하는 미국 공장을 운영하고 있습니다. 멕시코의 타이어 공장은 미국 자동차 제조업체에 공급하고 있으며, 캐나다는 여전히 주요 유황 수출국입니다. 이 지역의 전기차 보급은 중국에 비해 늦게 시작되었고, 수요 증가는 완만하지만 고부가가치, 저탄소 등급을 밀어붙이고 있습니다.

유럽 시장은 엄격한 환경 기준과 탈탄소화 의무를 반영하고 있습니다. 2024년부터 ISCC PLUS 인증을 획득한 랑세스의 'Vulkanox HS Scopeblue'는 이 지역에서 바이오 원료에 대한 중요성을 입증하고 있습니다. Flexsys의 독일산 HD-OT20은 말레이시아산 대비 18% 낮은 CO2 배출량을 자랑하며, 적극적인 CO2 감축 목표를 가진 유럽연합(EU) OEM 업체들에게 매력적인 제품입니다. 러시아의 황 수출 금지 조치와 에너지 비용 상승으로 수익률이 압박을 받고 있으며, 제조 공정의 업그레이드와 현지 원료 조달 계약이 촉진되고 있습니다. 남미에서는 브라질의 자동차 및 농기계 부문의 성장이 집중되어 있는 반면, 중동 및 아프리카는 광산 관련 고무 제품에 의존하고 있으며 불용성 유황의 대부분을 아시아에서 수입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제8장 CEO을 위한 중요 전략적 과제

KTH 26.05.29The Insoluble Sulfur Market size is expected to increase from USD 1.16 billion in 2025 to USD 1.21 billion in 2026 and reach USD 1.49 billion by 2031, growing at a CAGR of 4.31% over 2026-2031.

Tire radialization, higher electric-vehicle (EV) penetration, and the shift toward premium high-dispersion grades are reinforcing demand resilience despite margin pressure from elemental sulfur cost spikes. Capacity additions in China and the adoption of continuous-process manufacturing are reshaping cost curves, while Western suppliers focus on low-carbon, high-stability formulations to serve EV tires. Distributor-led sales are expanding as mid-tier compounders seek technical support and just-in-time delivery, and industrial rubber goods capitalize on mining and infrastructure spending. Regulatory scrutiny of carbon disulfide (CS2) exposure and the search for sustainable feedstocks will keep capital requirements high and support long-term price discipline.

Global Insoluble Sulfur Market Trends and Insights

Surging Global OEM and Replacement Tire Production Demand

China produced 1.19 billion tire units in 2024, an increase of 9.2% year on year, while replacement demand remained robust because aging vehicle fleets continue to clock higher mileage. Southeast Asia's dominance in tire exports, led by Thailand's 40.38% share of US passenger-tire imports, keeps regional offtake solid. Radial tires need about 1.7 times more insoluble sulfur than bias-ply designs, reinforcing the volume pull from tire modernization. Tire makers relocating plants to circumvent tariffs are boosting chemical imports and accelerating international orders. Combined, these structural and cyclical forces underpin a sustained volume floor for the insoluble sulfur market.

Shift to EV-Specific Low-Rolling-Resistance Compounds

EV tires carry heavier loads and must deliver a longer range. They therefore rely on silica-rich, low-rolling-resistance compounds that demand insoluble sulfur to prevent bloom and ensure thermal stability. Eastman's Crystex Cure Pro, jointly developed with Double Coin, improves flow and dispersion, enabling shorter mixing times and lower cure temperatures, which saves energy and reduces emissions. Flexsys reports that its Cure Pro Malaysia grade has a 10% lower product carbon footprint than conventional HD-OT20, supporting OEM (original equipment manufacturer) scope-3 targets. Growing EV adoption in China, where new-energy vehicles reached a 41% sales share in 2024, positions premium insoluble sulfur grades for double-digit volume growth through 2031.

Volatile Elemental Sulfur and CS2 Pricing

China's FOB sulfur price hit USD 571 per ton in January 2026, quadrupling from January 2024, after Russia extended its export ban and Middle Eastern producers diverted tonnage to Indonesian nickel projects. Sulfur makes up over half of phosphate-fertilizer costs, so fertilizer demand competes directly with chemical feedstock buyers. LANXESS raised additive prices by up to 50% in March 2026 to preserve margins. Producers without long-term sulfur contracts face margin squeeze and working-capital strain.

Other drivers and restraints analyzed in the detailed report include:

- Continuous-Process IS Manufacturing Boosts Capacity and Consistency

- Rise of Green High-Dispersion, Low-Oil Grades for Sustainability

- Tightening Occupational-Exposure Limits for Dust and CS2

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular Oil-Filled Grades (OT33/OT10) hold 33.47% of the Insoluble Sulfur market share owing to cost advantages for bias-ply and replacement tires. The insoluble sulfur market size for regular grades remains the largest, yet premium grades capture incremental margin, especially where OEM sustainability mandates push for lower product carbon footprints. High-Dispersion Premium (HD-OT20) grades captured the fastest growth at a 4.58% CAGR, supported by EV tire needs for low bloom and superior thermal stability. Flexsys's Crystex HD OT 20 specifies more than or equal to 72% insoluble sulfur and maintains stability at 105°C for 15 minutes. Eastman's Cure Pro variant allows lower mixing speeds and saves up to 10% energy.

Low-oil and no-oil grades are gaining traction in high-silica EV compounds. LANXESS's Aflux SD, launched in 2025, improves silica dispersion and wet grip. Flexsys's XD grade posts cradle-to-gate emissions near 1.23 tons CO2 equivalent per kilogram, reinforcing its positioning in low-carbon tires. Suppliers with continuous-process capability can switch between grades quickly, meeting diverse compounder requirements and optimizing asset utilization.

The Insoluble Sulfur Market Report is Segmented by Product Grade (High-Dispersion Premium, Regular Oil-Filled Grades, and Low-Oil/No-Oil Grades), Distribution Channel (Direct To Tire/Rubber Manufacturers and More), Application (Tires, Industrial Rubber Goods, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 56.25% of the 2025 value and will post a 5.14% CAGR to 2031, driven by China's tire expansion and EV adoption. China Sunsine raised insoluble sulfur capacity to 60,000 tons per annum, but oversupply kept utilization near 68% in 2024. Shandong Yanggu Huatai's 40,000 tons per annum addition in 2022 depressed average selling prices by 24% through mid-2024. Thailand's natural-rubber supremacy and Vietnam's rising tire plants fortify regional offtake. India is adding capacity to meet domestic auto growth, yet it relies on imports, offering investment headroom for new regional producers.

North America benefits from LANXESS's Bushy Park expansion, which brought new processing-promoter lines online in November 2025. Local production cuts shipment times and enhances security amid geopolitical tension. Flexsys operates US plants that feed domestic OEMs pursuing lower scope-3 emissions. Mexican tire plants serve US automakers, and Canada remains a key sulfur exporter. Regional EV uptake is slower than in China, moderating demand growth but supporting higher-value, low-carbon grades.

Europe's market reflects strict environmental norms and decarbonization mandates. LANXESS's Vulkanox HS Scopeblue, ISCC PLUS-certified since 2024, evidences regional emphasis on bio-based inputs. Flexsys's German HD-OT20 emits 18% less CO2 than its Malaysian counterpart, appealing to European Union (EU) OEMs with aggressive CO2 targets. Russian sulfur export bans and higher energy costs squeeze margins, encouraging process upgrades and local feedstock contracts. South America's growth clusters in Brazil's auto and agricultural equipment sectors, while Middle East and Africa depend on mining-related rubber goods, importing most insoluble sulfur from Asia.

- Chaoyang Mingyu Chemical Co., Ltd.

- Chemiplas Rubber Chemicals

- China Petrochemical Corp.

- China Sunsine Chemical Holdings

- Eastman Chemical Company

- Flexsys

- Henan Kailun Chemical Co., Ltd.

- Honeywell International Inc.

- Jiangxi Hengxingyuan Chemical Co., Ltd.

- KISHO Corporation Co., Ltd.

- Lanxess AG

- Nantong Haotai Chemical Products Co., Ltd.

- Ningxia Xinlong Chemical Industry Co., Ltd.

- OCCL Limited

- SHIKOKU CHEMICALS CORPORATION

- Taizhou Huangyan Donghai Chemical Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global OEM and replacement tire production demand

- 4.2.2 Shift to EV-specific low-rolling-resistance compounds

- 4.2.3 Continuous-process IS manufacturing boosts capacity and consistency

- 4.2.4 Rise of "green" high-dispersion, low-oil IS grades for sustainability

- 4.2.5 Industrial rubber goods capacity additions in mining and construction

- 4.3 Market Restraints

- 4.3.1 Volatile elemental sulfur and CS2 feedstock pricing

- 4.3.2 Tightening occupational-exposure limits for dust and CS2

- 4.3.3 Emerging peroxide/other non-sulfur cure systems in specialty elastomers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Grade

- 5.1.1 High-Dispersion Premium (HD-OT20)

- 5.1.2 Regular Oil-Filled Grades (OT33/OT10)

- 5.1.3 Low-Oil/No-Oil Grades

- 5.2 By Distribution Channel

- 5.2.1 Direct to Tire/Rubber Manufacturers

- 5.2.2 Specialty Chemical Distributors

- 5.3 By Application

- 5.3.1 Tires (Passenger, Commercial, Off-road)

- 5.3.2 Industrial Rubber Goods (Hoses, Belts, Seals)

- 5.3.3 Other Molded and Foamed Rubber Products

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Chaoyang Mingyu Chemical Co., Ltd.

- 6.4.2 Chemiplas Rubber Chemicals

- 6.4.3 China Petrochemical Corp.

- 6.4.4 China Sunsine Chemical Holdings

- 6.4.5 Eastman Chemical Company

- 6.4.6 Flexsys

- 6.4.7 Henan Kailun Chemical Co., Ltd.

- 6.4.8 Honeywell International Inc.

- 6.4.9 Jiangxi Hengxingyuan Chemical Co., Ltd.

- 6.4.10 KISHO Corporation Co., Ltd.

- 6.4.11 Lanxess AG

- 6.4.12 Nantong Haotai Chemical Products Co., Ltd.

- 6.4.13 Ningxia Xinlong Chemical Industry Co., Ltd.

- 6.4.14 OCCL Limited

- 6.4.15 SHIKOKU CHEMICALS CORPORATION

- 6.4.16 Taizhou Huangyan Donghai Chemical Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment