|

시장보고서

상품코드

2043975

남미의 사이버 보안 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)South America Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

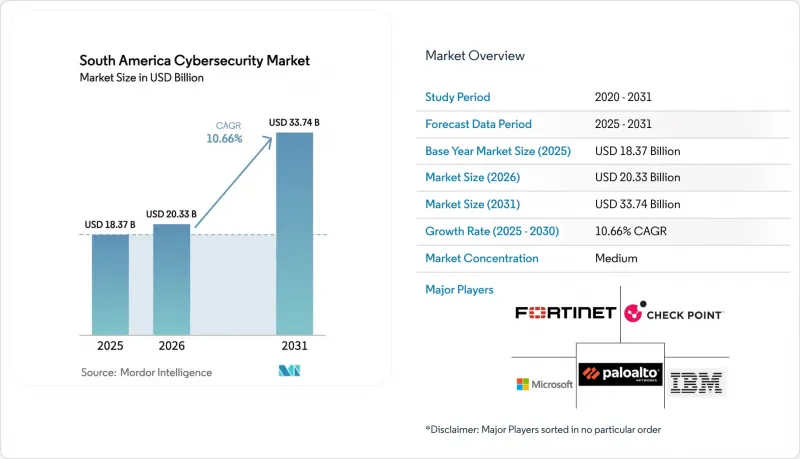

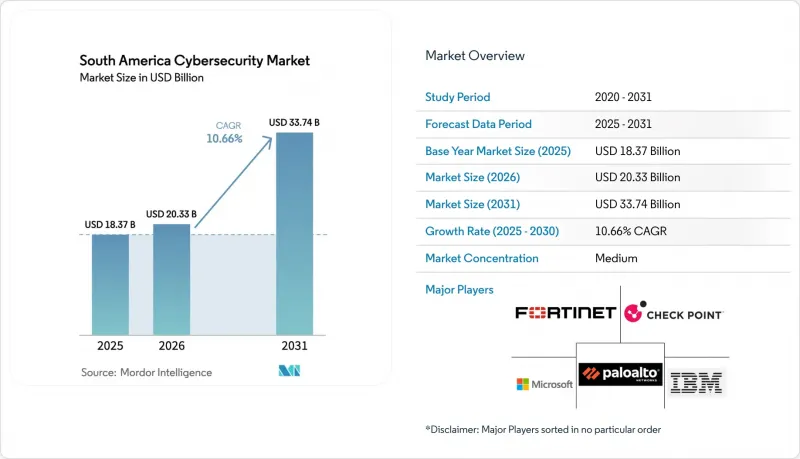

남미의 사이버 보안 시장 규모는 2025년에 183억 7,000만 달러로 평가되었습니다. 2026년 203억 3,000만 달러에서 2031년까지 337억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 10.66%를 나타낼 전망입니다.

서비스형 랜섬웨어(RaaS, ransomware-as-a-service) 키트의 급증, 규제 대상 산업에서의 제로 트러스트 확산, 중소기업(SME)의 클라우드 전환으로 인해 지출은 기본적인 방화벽을 넘어 통합 감지 및 대응 플랫폼으로 이동하고 있습니다. 브라질의 결의안 538호로 인해 지속적인 모니터링이 모범 사례에서 라이선스 조건으로 바뀌면서 관리형 보안 운영 센터(SOC)의 용량에 대한 수요가 급증하고 있습니다. 특히 아르헨티나의 통화 변동으로 인해 구매자는 달러로 표시된 구독 가격을 선택하는 경향이 있습니다. 한편, 상파울루와 산티아고의 하이퍼스케일러에 대한 투자로 인해 규제 대상 워크로드의 지연에 대한 우려는 줄어들고 있습니다. 또한, 제조 기업들이 원격 유지보수를 위해 OT(Operational Technology) 네트워크를 개방함에 따라 기존 IT 툴이 제공하지 못하는 프로토콜 기반 위협 분석에 대한 수요가 증가하고 있습니다.

남미의 사이버 보안 시장 동향 및 인사이트

RaaS(Ransomware-as-a-Service) 생태계 확대

기성품 암호화 페이로드를 판매하는 제휴 프로그램으로 인해 공격자의 기술적 장벽이 낮아지면서 남미의 사이버 보안 시장의 지출은 엔드포인트 감지, 불변의 백업 및 사고 대응을 위한 정액제 계약으로 이동하고 있습니다. Dragos의 기록에 따르면, 2025년 1-3분기 동안 이 지역의 산업 제어 시스템에 대한 랜섬웨어 공격은 147건이 발생하여 전년 동기 대비 34% 증가하였습니다. 그중 62%가 브라질에서 발생한 사례입니다. Windows Server 2012를 운영하는 의료기관이 가장 큰 피해를 입었고, 주정부는 예산의 제약에도 불구하고 암호자산을 통한 지불을 승인할 수 밖에 없었습니다. 암호화 전에 데이터를 탈취하는 이중 강탈 수법으로 인해 기업들은 데이터 유출 방지 및 포렌식 대책을 강화하게 되었습니다. 이사회는 현재 경계선 침해를 가정한 모의훈련을 요구하고 있으며, 이에 따라 1시간 이내 봉쇄를 서비스수준협약(SLA)에 포함시킨 관리형 감지 및 대응(MDR) 서비스 도입이 진행되고 있습니다. 지급액이 증가함에 따라 보험사들은 인수 기준을 강화하고 보험료를 인상하는 한편, 예방적 보안 도구에 대한 투자수익률(ROI)을 강조하는 움직임을 보이고 있습니다.

규제 대상 산업에서의 제로 트러스트 도입 확대

2025년 12월 브라질의 결의안 538호로 은행에 지속적인 인증과 마이크로세분화을 의무화하면서 제로 트러스트 프레임워크는 개념에서 컴플라이언스 의무로 전환되었습니다. 칠레의 구리 생산업체도 랜섬웨어로 인해 감시 제어 및 데이터 수집 시스템이 중단되어 수백만 달러 규모의 생산 손실이 발생하자 유사한 접근 방식을 도입했습니다. 접근을 허용하기 전에 기기의 상태와 지리적 위치를 평가하는 아이덴티티 플랫폼이 정적인 인증 정보 확인을 대체하고 있습니다. 도입은 자산 인벤토리에서 시작하여 동-서부 트래픽 모니터링으로 마무리되지만, 사내 아키텍트가 부족하기 때문에 많은 기업이 이 과정을 관리형 보안 제공업체에 위탁하고 있습니다. 브라질의 LGPD와 칠레의 프레임워크 법률을 준수하는 정책 템플릿을 제공하는 벤더는 감사 기간을 단축하고 클라우드 워크로드 보호에 대한 교차판매를 촉진하고 있습니다.

국가별로 분절된 데이터 보호 규정

브라질의 LGPD는 72시간 내 침해 공개와 데이터 보호 책임자 설치를 의무화하고 있지만, 칠레의 새로운 법은 유럽의 통지 기간을 반영하는 반면, 페루는 여전히 10일의 유예기간을 허용하고 있습니다. 다국적 기업들은 서로 다른 동의 규칙과 국경 간 전송 금지 조치에 대응해야 하고, 그 결과 위협 사냥에 투입해야 할 예산을 압박하는 데이터 거주 요건을 회피할 수밖에 없는 상황에 처해 있습니다. EU의 충분성 인증 제도에 상응하는 남미만의 프레임워크가 없기 때문에 기업들은 국가마다 다른 암호화 게이트웨이를 도입해야 하고, 도구와 감사 비용이 증가하고 있습니다. 또한, 이러한 난립된 상황은 지역적 SOC의 중앙집중화를 방해하고 있습니다. 개인 데이터가 포함된 경고는 상관관계 분석을 위해 국경을 넘어 전송할 수 있는 것은 아니기 때문입니다. 이러한 비효율성으로 인해, 더 넓은 시장에서 컴플라이언스 대응 비용을 분산시킬 수 없는 현지 벤더들은 불리한 상황에 처하게 됩니다.

부문 분석

2026년부터 2031년까지 서비스 시장은 CAGR 11.18%로 확대될 것이며, 은행, 병원, 광산 기업들이 인력 부족을 보충하기 위해 24시간 365일 모니터링 업무를 아웃소싱하면서 남미 전체 사이버 보안 시장 성장률을 상회할 것으로 예측됩니다. 2025년에는 솔루션이 남미의 사이버 보안 시장 점유율의 61.76%를 차지했지만, 구매자는 경보 조정 및 위협 사냥을 수행하는 전문 지식이 없으면 어플라이언스가 작동하지 않는다는 사실을 깨달았습니다. 결의안 538과 같은 규제 요인으로 인해 중견은행들은 실시간 사고 대응 능력을 입증해야 했고, 사내 SOC를 구축하는 것보다 MDR(Managed Detection and Response) 계약을 체결하는 것이 컴플라이언스를 달성하는 지름길로 여겨지게 되었습니다. 하이브리드 아키텍처의 확산으로 클라우드 보안 및 ID 관리 제품군이 솔루션 지출을 주도한 반면, 범용 네트워크 방화벽은 다기능 플랫폼에 점유율을 빼앗겼습니다.

기업이 제로 트러스트로 전환할 때 전문 서비스를 통한 평가, 통합 및 전환은 여전히 필수적입니다. LGPD(브라질 일반 데이터 보호법), 칠레의 프레임워크 법 및 산업별 규제 요건을 통합 관리 매트릭스에 반영할 수 있는 컨설턴트에 대한 수요가 증가하고 있습니다. 현재 매니지드 서비스는 GRC 대시보드, 위협 인텔리전스 피드, 자동화된 봉쇄 기능을 묶어 사용자 단위로 중소기업에 엔터프라이즈급 성과를 제공합니다. 템페스트 시큐리티 인텔리전스(Tempest Security Intelligence)와 같이 포르투갈어와 스페인어를 구사하는 SOC 분석가를 보유한 통합업체는 주로 영어로만 센터를 운영하는 국제적인 기업들과 차별화를 꾀하고 있습니다.

클라우드 도입은 2031년까지 연평균 복합 성장률(CAGR) 11.24%를 나타내며 2025년 53.43%를 차지했던 On-Premise 환경의 비중을 꾸준히 줄여나가고 있습니다. 전환점은 하이퍼스케일러가 상파울루와 산티아고에 데이터 거주 요건을 충족하고 실시간 결제를 위한 지연을 크게 줄인 상파울루와 산티아고 구역을 개설한 것입니다. 인플레이션 경제에서는 월별 청구로 현금 흐름을 유지하고 환율 변동 위험을 헤지할 수 있기 때문에 종량제가 선호되고 있습니다. 남미의 사이버 보안 시장에서 클라우드 툴의 규모가 확대되고 있으며, 중소기업들이 설비 투자 없이 웹 네이티브 방화벽, 워크로드 보호, 보안 액세스 엣지 구성 요소를 도입하고 있기 때문입니다.

On-Premise 환경은 주권 및 레거시 시스템 간의 상호 의존성으로 인해 물리적 제어가 요구되는 코어뱅킹, 의료기록, 국방 분야에서는 여전히 자리를 잡고 있습니다. 그러나 이러한 분야에서도 Microsoft Defender for Cloud와 같은 통합 콘솔을 통해 물리 머신과 가상 머신에 걸쳐 공통된 정책이 적용되고 있습니다. 통신사들은 현재 SASE 게이트웨이를 도시 지역 네트워크에 배치하여 인라인 위협 검사와 결합된 탄력적인 대역폭을 제공합니다. 섀도우 IT가 감소함에 따라 정책 적용의 핵심은 지점 라우터에서 ID 중심의 오버레이로 이동하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe South America cybersecurity market size was valued at USD 18.37 billion in 2025 and estimated to grow from USD 20.33 billion in 2026 to reach USD 33.74 billion by 2031, at a CAGR of 10.66% during the forecast period (2026-2031).

A surge in ransomware-as-a-service kits, wider zero-trust adoption across regulated industries, and cloud migration by small and medium enterprises (SMEs) are pushing spending beyond basic firewalls toward integrated detection and response platforms. Brazil's Resolution 538 has turned continuous monitoring from a best practice into a licensing condition for banks, causing a run on managed security operations center (SOC) capacity. Currency volatility, especially in Argentina, is steering buyers toward subscription pricing denominated in USD, while hyperscaler investments in Sao Paulo and Santiago reduce latency concerns for regulated workloads. As industrial firms expose operational technology (OT) networks for remote maintenance, demand is rising for protocol-aware threat analytics that traditional IT tools cannot deliver.

South America Cybersecurity Market Trends and Insights

Rising Ransomware-as-a-Service Ecosystem

Affiliate programs selling ready-made encryption payloads have cut the skill threshold for attackers, shifting South America cybersecurity market spending toward endpoint detection, immutable backup, and incident response retainers. Dragos logged 147 ransomware incidents against regional industrial control systems during the first three quarters of 2025, a 34% year-over-year increase, with Brazil accounting for 62% of cases. Healthcare institutions running Windows Server 2012 were hit hardest, forcing provincial governments to authorize cryptocurrency payments despite budget constraints. Double-extortion tactics stealing data before encryption nudged enterprises to elevate data loss prevention and forensics. Boards now request tabletop exercises that assume perimeter compromise, prompting uptake of managed detection and response services with one-hour containment service-level agreements. As payouts inflate, insurers tighten underwriting, raising premiums and amplifying return-on-investment narratives for proactive security tooling.

Proliferation of Zero-Trust Adoption by Regulated Industries

Zero-trust frameworks moved from concept to compliance obligation once Brazil's Resolution 538 mandated continuous authentication and micro-segmentation for banks in December 2025. Chile's copper producers replicated the approach after ransomware halted supervisory control and data acquisition systems, costing millions in lost output. Identity platforms that score device posture and geolocation before granting access are replacing static credential checks. Implementation starts with asset inventory and ends with east-west traffic monitoring, a path that most firms outsource to managed security providers due to scarce in-house architects. Vendors offering policy templates mapped to Brazil's LGPD and Chile's Framework Law shorten audits and encourage cross-sell into cloud workload protection.

Fragmented Data-Protection Regulations Across Countries

Brazil's LGPD obliges 72-hour breach disclosure and data-protection officers, Chile's new law mirrors European notice periods, yet Peru still allows 10 business days. Multinationals juggle divergent consent rules and cross-border transfer bans, forcing data-residency workarounds that drain budgets earmarked for threat hunting. Without a South American equivalent of the EU's adequacy regime, firms deploy country-specific encryption gateways, multiplying tooling and audit costs. The patchwork also deters regional SOC centralization because alerts containing personal data cannot always cross borders for correlation. This inefficiency disadvantages local vendors that cannot amortize compliance engineering over wider markets.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Cloud Migration Among South American SMEs

- Government Cybersecurity Capacity-Building Programs in Brazil and Chile

- Acute Cybersecurity Skills Shortage in Spanish and Portuguese Talent Pools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services expanded at an 11.18% CAGR from 2026-2031, eclipsing the broader South America cybersecurity market rate as banks, hospitals, and miners outsourced 24/7 monitoring to offset staffing gaps. Although solutions controlled a 61.76% slice of South America cybersecurity market share in 2025, buyers realized that appliances are inert without expertise to tune alerts and run threat hunts. Regulatory triggers like Resolution 538 forced mid-tier banks to prove real-time incident response, making managed detection and response contracts a faster path to compliance than building internal SOCs. Cloud security and identity suites led solution spending thanks to hybrid architectures, while commodity network firewalls ceded ground to multifunction platforms.

Professional services assessment, integration, migration remain essential when enterprises pivot to zero trust. Demand rises for consultants who map LGPD, Chile's Framework Law, and sector mandates into unified control matrices. Managed services now bundle GRC dashboards, threat intel feeds, and automated containment, delivering enterprise-grade outcomes to SMEs on a per-user basis. Integrators with Portuguese and Spanish SOC analysts, such as Tempest Security Intelligence, differentiate against global players that primarily staff English-only centers.

Cloud deployments are tracking an 11.24% CAGR through 2031, steadily shrinking the on-premises majority that stood at 53.43% in 2025. The tipping point came as hyperscalers opened Sao Paulo and Santiago zones, satisfying data residency clauses and slicing latency for real-time payments. Consumption pricing resonates in inflationary economies because monthly invoices preserve cash flow and hedge currency swings. South America cybersecurity market size for cloud tools grows as SMEs procure web-native firewalls, workload protection, and secure access edge components without capital outlays.

On-premises estates persist in core banking, health records, and defense environments where sovereignty and legacy system interdependence demand physical control. Yet even here, unified consoles like Microsoft Defender for Cloud enforce common policies across physical and virtual machines. Telcos now position SASE gateways inside their metropolitan networks, offering elastic bandwidth married with inline threat inspection. As shadow IT declines, the locus of policy enforcement moves from branch routers to identity-centric overlays.

The South America Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (On-Premises, and Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-Commerce, Energy and Utilities, and More), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems, Inc.

- International Business Machines Corporation

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Microsoft Corporation

- Broadcom Inc. (Symantec Enterprise Division)

- CrowdStrike Holdings, Inc.

- Zscaler, Inc.

- Sophos Group plc

- Kaspersky Lab JSC

- McAfee Corp.

- Proofpoint, Inc.

- Dell Technologies Inc.

- Huawei Technologies Co., Ltd.

- BAE Systems plc

- Prosegur Compania de Seguridad, S.A. (Cipher)

- Tempest Security Intelligence S.A.

- VaultOne, Inc.

- Modulo Security LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to cloud-native architectures

- 4.2.2 Exploding ransomware-as-a-service economy

- 4.2.3 Mandatory data-protection laws (LGPD, Chile Law 21.459)

- 4.2.4 OT/ICS security spend for critical infrastructure

- 4.2.5 AI-powered zero-trust network access roll-out

- 4.2.6 Nearshoring of global MSSP delivery centres

- 4.3 Market Restraints

- 4.3.1 Shortage of cyber-talent and high salary inflation

- 4.3.2 Fragmented, country-specific compliance regimes

- 4.3.3 FX volatility limiting cap-ex for SMEs

- 4.3.4 Grey-market hardware inflows undermining standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Other End-User Verticals

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Peru

- 5.5.4 Chile

- 5.5.5 Colombia

- 5.5.6 Ecuador

- 5.5.7 Venezuela

- 5.5.8 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 International Business Machines Corporation

- 6.4.3 Palo Alto Networks, Inc.

- 6.4.4 Fortinet, Inc.

- 6.4.5 Check Point Software Technologies Ltd.

- 6.4.6 Trend Micro Incorporated

- 6.4.7 Microsoft Corporation

- 6.4.8 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.9 CrowdStrike Holdings, Inc.

- 6.4.10 Zscaler, Inc.

- 6.4.11 Sophos Group plc

- 6.4.12 Kaspersky Lab JSC

- 6.4.13 McAfee Corp.

- 6.4.14 Proofpoint, Inc.

- 6.4.15 Dell Technologies Inc.

- 6.4.16 Huawei Technologies Co., Ltd.

- 6.4.17 BAE Systems plc

- 6.4.18 Prosegur Compania de Seguridad, S.A. (Cipher)

- 6.4.19 Tempest Security Intelligence S.A.

- 6.4.20 VaultOne, Inc.

- 6.4.21 Modulo Security LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment