|

시장보고서

상품코드

2043987

남미의 핀테크 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)South America Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

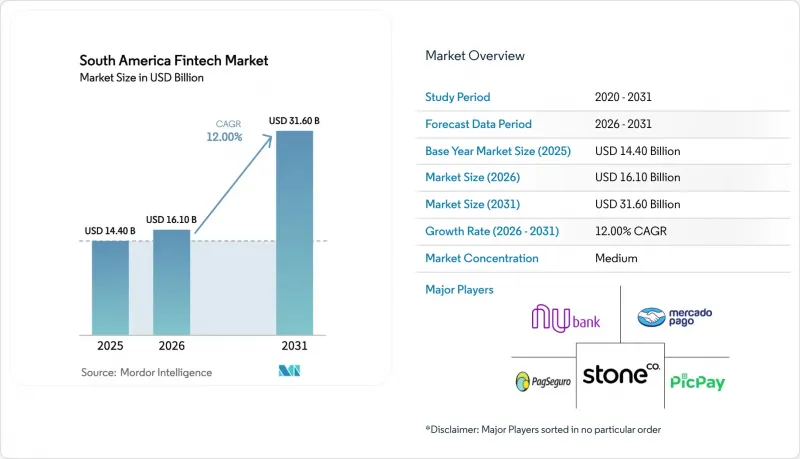

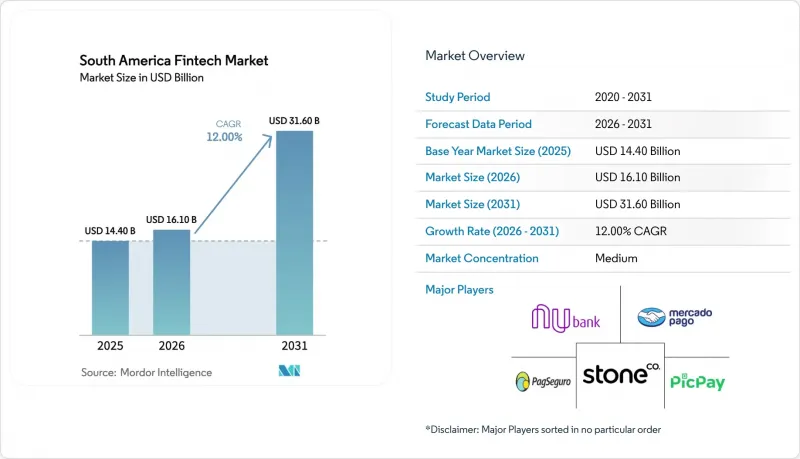

남미의 핀테크 시장 규모는 2025년 144억 달러로 평가되었습니다. 2026년 161억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 12%를 나타내, 2031년에는 316억 달러에 이를 것으로 예측됩니다.

디지털 결제가 45.0%의 점유율로 시장을 주도하는 가운데, 소비자 신용과 중소기업 대출이 지속적으로 확대되는 가운데, 디지털 대출은 CAGR 21.3%로 가장 빠른 성장이 예상됩니다. 2025년에는 개인 사용자가 68.6%를 차지하고, 모바일 애플리케이션이 인터페이스와의 상호작용의 74.7%를 차지하는 등 신규 고객 확보 및 참여에 있어 모바일 중심의 경로가 확립되고 있음을 알 수 있습니다. 특히 브라질과 아르헨티나는 인터체인지 수수료 상한 규제, 금리 상승, 환율 관리로 인해 수수료율과 결제 수익성이 압박을 받는 등 단기적인 역풍이 지속되고 있습니다. 네오뱅크와 임베디드 금융 플랫폼이 신용, 보험, 투자 상품을 교차 판매하면서 경쟁이 심화되고 있으며, Nubank가 1억 2,700만 명의 고객을, Mercado Pago가 7,200만 명의 월간 활성 사용자를 보유하고 있는 것이 그 한 예입니다. 한 예입니다.

남미의 핀테크 시장 동향과 인사이트

RTP의 규모 확대와 기능 강화가 거래량 증가를 견인합니다.

실시간 결제는 현재 남미의 핀테크 시장 전반의 거래 성장을 뒷받침하는 축이 되고 있으며, 그 선두에는 브라질의 Pix가 있습니다. 성인층에서 거의 모든 연령층에 보급되면서 2024년에는 634억 건의 거래를 처리했습니다. Pix의 24시간 365일 이용 가능성과 빠른 결제 처리로 인해 2024년 말까지 등록 사용자 수가 163만 명으로 급증했습니다. 한편, '픽스 오토매틱(Pix Automatico)'과 비접촉식 탭 결제와 같은 새로운 기능은 구독 및 POS 결제의 사용처를 확대했습니다. 페루의 상호 운용 가능한 결제 인프라는 Yape와 PLIN을 핵심으로 하고 있으며, 도시 지역 소매점 및 마이크로 커머스 가맹점에서의 사용을 촉진하고 있습니다. Pix와 인근 시장을 연결하는 초기 크로스보더 파일럿 사업을 통해 남미의 핀테크 시장의 송금 및 EC 회랑의 결제 기간이 단축되고 환율 스프레드가 축소되고 있습니다. Mercado Pago는 월 7,200만 명의 활성 사용자들에게 즉각적인 송금을 가능하게 하는 대규모 생태계를 통해 플랫폼의 보급을 촉진하고 있으며, StoneCo는 2025년 초 MSME(중소영세기업) 고객의 픽스 거래가 전년 대비 95% 증가했다고 보고했습니다. 규제 측면의 명확화가 사업 확장을 뒷받침하고 있습니다. 여기에는 브라질의 상호운용성 의무화, 2026년 중반을 목표로 하는 칠레와 콜롬비아의 즉시 결제 이니셔티브, APP(용도) 사기 보고 증가에 따라 강화된 KYC(신원확인) 및 생체인증 확인이 포함됩니다.

개방형 금융의 데이터 마이그레이션성, 신용과 자문의 문을 열다.

브라질의 오픈 파이낸스 시스템은 4,300만 명 이상의 활성 사용자들의 동의를 기록했으며, 주당 15억 건 이상의 API 호출을 처리하여 거래량 측면에서 세계 최대 규모의 이니셔티브 중 하나로 자리매김했습니다. 중앙은행 지침에 따라 대상 금융기관은 거래, 신용, 투자 분야의 데이터를 공유해야 하며, 이를 통해 제3자는 검증된 계좌 정보 및 급여 흐름을 활용하여 무담보 대출, 급여 연동 대출 및 담보 대출의 가격을 책정할 수 있습니다. Nubank의 담보 대출 포트폴리오는 2025년에 전년 대비 133% 증가했습니다. 이는 소득 및 계좌 데이터에 대한 동의에 기반한 접근을 통해 신용 심사 및 회수 실적이 강화된 것이 기여하고 있습니다. 칠레 금융시장위원회(CMF)는 2024년 7월 일반규정 제514호를 발표하며 2026년 7월까지 표준화된 API 도입을 의무화했습니다. 또한, 콜롬비아는 2025년 6월에 시행령안을 발표하여 적용 범위를 은행업에서 보험 및 연금 분야로 확대했습니다. 아르헨티나의 2025년 행정령 제353호는 아르헨티나 중앙은행(BCRA)의 감독 하에 동의에 기반한 데이터 공유를 통한 오픈 파이낸스 제도를 공식화하여, 남미의 핀테크 시장에서 다상품 금융 자문에 대한 장벽을 더욱 낮추었습니다. 이러한 모멘텀이 있는 반면, 데이터 분야 표준의 차이와 아직 개발 중인 국경 간 상호운용성은 소규모 사업자에게는 통합 비용과 복잡성을 증가시키고 있습니다.

높은 고객 확보 비용과 낮은 금융 이해도 : 구조적 성장의 장애물

높은 고객 확보 비용과 함께 남미 여러 시장에서 여전히 낮은 금융 문해력이 핀테크의 확장성을 제약하는 요인으로 작용하고 있습니다. 디지털화의 급속한 확산에도 불구하고, 소비자 온보딩을 위해서는 여전히 많은 마케팅 비용, 오프라인 신원 확인, 그리고 교육 중심의 참여가 필요합니다. 이로 인해 특히 은행 서비스를 충분히 이용할 수 없는 지역이나 농촌 지역에서 고객 획득 단가(CAC)의 평균 비용이 상승하고, 평생가치(LTV)의 경제성이 떨어지고 있습니다. 이러한 도전은 구조적이고 장기적인 과제이며, 핀테크 기업은 전환율과 고객 유지율을 높이기 위해 금융 교육, 대행사 지원을 통한 온보딩, 데이터 기반 개인화에 대한 투자를 해야 합니다.

부문 분석

2025년, 디지털 결제는 남미의 핀테크 시장 점유율의 45.1%를 차지했습니다. 이는 브라질의 Pix, 아르헨티나의 Transferencias 3.0과 같은 결제 인프라가 뒷받침하고 있으며, 이는 소비자와 가맹점 모두의 결제 비용을 절감하고 있습니다. 부문별로는 디지털 대출이 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 21.3%를 나타낼 것으로 예측되며, 오픈 파이낸스 데이터와 임베디드 신용 채널을 통해 신용 이력이 부족한 계층에 대한 신용 심사가 확대됨에 따라 남미의 핀테크 시장의 남미의 핀테크 시장의 가속화가 두드러지고 있습니다. 현재 대출기관은 동의한 은행 데이터와 마켓플레이스 및 물류 이력을 결합하여 소비자 및 MSMB(중소기업) 대출자의 상환 행동을 평가하고 있으며, 이를 통해 승인 시간을 단축하고 그동안 서비스를 받지 못했던 계층의 승인율을 높이고 있습니다. Nubank의 담보 대출 포트폴리오는 2025년에 전년 대비 133% 증가했습니다. 이는 검증된 급여 이체 및 계좌의 자금 흐름에 대한 접근을 통해 대출의 질과 회수력이 강화되었기 때문입니다. 마르카 리브레의 핀테크 부문은 마켓플레이스의 거래 데이터와 배송 접점을 활용하여 리볼빙 잔액, 연체율, 가격 책정을 최적화하고, 2025년 3분기까지 신용 발행액을 110억 달러까지 확대했습니다.

투자 및 보험 관련 분야의 모멘텀이 개인 및 MSME(중소영세기업) 사용자를 위한 보다 종합적인 서비스 제안을 뒷받침하고 있습니다. 메르카도 파고의 운용자산 잔액은 매력적인 벤치마크 연동 수익률을 가진 머니마켓상품을 일상적인 지갑 경험에 통합한 결과, 2025년 3분기에 전년 동기 대비 2배 증가한 미화 15.1억 달러에 달했습니다. 네오뱅크와 결제 플랫폼은 중소기업을 위한 타겟팅된 보험 상품을 도입하고, 온보딩과 체크아웃 흐름에 보상 옵션을 포함시킴으로써 시간이 지남에 따라 부수율을 높이고 있습니다. 금융회사들이 대규모 대출 사업에 진출함에 따라 데이터 보호 및 AML(자금세탁방지) 관련 컴플라이언스 기준은 고정비용을 증가시키고, 견고한 지배구조와 자본력을 갖춘 기업을 우대하는 결과를 초래하여 남미의 핀테크 시장의 통합 움직임이 강화되고 있습니다. 전반적으로 남미의 핀테크 산업은 단일 결제 서비스에서 다각화된 금융 서비스로의 전환을 지속하고 있으며, 동의한 데이터가 신용 심사 및 채권 추심을 지원하는 가운데 신용 중심의 수익화가 다음 성장 단계를 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The South America Fintech Market size is expected to grow from USD 14.40 billion in 2025 to USD 16.10 billion in 2026 and is forecast to reach USD 31.60 billion by 2031 at 12% CAGR over 2026-2031.

Digital payments led activity with a 45.0% share, while digital lending is set to expand at the fastest pace, with a 21.3% CAGR, as consumer credit and SME financing continue to scale. Retail users drove 68.6% of usage in 2025, and mobile applications accounted for 74.7% of interface interactions, underscoring a mobile-centric pathway for onboarding and engagement. Short-term headwinds persist from interchange caps, elevated interest rates, and FX controls that compress take rates and settlement economics, particularly in Brazil and Argentina. Competitive intensity is high as neobanks and embedded-finance platforms cross-sell credit, insurance, and investment products, illustrated by Nubank's 127 million customers and Mercado Pago's 72 million monthly active users across the region.

South America Fintech Market Trends and Insights

RTP Scale-Up and Features Propel Volume Growth

Real-time payments now anchor transaction growth across the South America fintech market, led by Brazil's Pix, which handled 63.4 billion transactions in 2024 as adoption approaches ubiquity among adults. Pix's 24/7 availability and rapid settlement underpinned a surge to 163 million registered users by late 2024, while new features such as Pix Automatico and contactless tap-to-pay expanded use cases for subscriptions and point-of-sale payments. Peru's interoperable rails, anchored by Yape and PLIN, support merchant acceptance in urban retail and micro-commerce. Early cross-border pilots linking Pix with neighboring markets are shortening settlement windows and reducing FX spreads for remittance and e-commerce corridors in the South America fintech market. Platform adoption has been reinforced by large ecosystems, with Mercado Pago enabling instant disbursements to its 72 million monthly active users and StoneCo reporting a 95% year-over-year increase in Pix transactions among MSMB clients in early 2025. Regulatory clarity supports scale, including Brazil's interoperability mandates and ongoing instant payment initiatives in Chile and Colombia for mid-2026 timelines, as well as enhanced KYC and biometric checks in response to elevated APP fraud reports.

Open Finance Data Portability Unlocks Credit and Advisory

Brazil's open finance system records more than 43 million active user consents and processes over 1.5 billion API calls weekly, placing it among the largest initiatives globally by transaction volume. Central bank directives require data sharing across transactional, credit, and investment domains for qualifying institutions, enabling third parties to price unsecured, payroll-linked, and secured credit using verified account and salary flows. Nubank's secured-lending portfolio rose 133% year over year in 2025, assisted by consented access to income and account data that tightened underwriting and collection performance. Chile's CMF issued General Rule No. 514 in July 2024 to require standardized APIs by July 2026, and Colombia published a draft decree in June 2025 to extend coverage beyond banking into insurance and pensions. Argentina's Executive Decree No. 353 of 2025 formalized an open finance system with BCRA oversight and consent-based data sharing, further lowering barriers to multi-product financial advice in the South America fintech market. Despite momentum, differing data field standards and nascent cross-border interoperability raise integration costs and complexity for smaller providers.

High Customer Acquisition Costs and Low Financial Literacy as Structural Growth Barriers

High customer acquisition costs, coupled with persistently low financial literacy across several South American markets, continue to constrain fintech scalability. Despite rapid digital adoption, consumer onboarding still requires significant marketing spend, offline verification, and education-driven engagement. This raises blended CAC and depresses lifetime value economics, particularly in underbanked and rural segments. The challenge is structural and long-duration, pushing fintechs to invest in financial education, agent-assisted onboarding, and data-led personalization to improve conversion and retention.

Other drivers and restraints analyzed in the detailed report include:

- Embedded Finance in E-Commerce and Super Apps

- Dollar-Linked Savings and Stablecoin Adoption

- FX Controls, Settlement Frictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments captured 45.1% of the South American fintech market share in 2025, underpinned by rails such as Brazil's Pix and Argentina's Transferencias 3.0, which have lowered acceptance costs for consumers and merchants. Within the segment mix, digital lending is forecast to expand at a 21.3% CAGR between 2026 and 2031, highlighting acceleration in the South American fintech market as thin-file underwriting scales through open-finance data and embedded-credit channels. Lenders now combine consented bank data with marketplace and logistics histories to assess repayment behaviour for consumer and MSMB borrowers, compressing approval times while lifting acceptance rates for previously underserved cohorts. Nubank's secured-lending portfolio grew 133% year over year in 2025, aided by access to verified salary deposits and account flows that strengthened origination quality and collections. Mercado Libre's fintech arm scaled credit issuance to USD 11 billion by Q3 2025, using marketplace transaction data and delivery touchpoints to calibrate revolving balances, delinquency, and pricing.

Momentum in investment and insurance adjacencies has supported a more complete proposition for retail and MSMB users. Mercado Pago's assets under management doubled year over year to USD 15.1 billion in Q3 2025 as money-market products were bundled into daily-wallet experiences with attractive benchmark-linked yields. Neobanks and payments platforms have introduced targeted protection products for small businesses, embedding coverage options into onboarding and checkout flows to increase attach rates over time. As providers expand into lending at scale, compliance standards linked to data protection and AML have increased fixed costs and favoured players with robust governance and capital, reinforcing consolidation dynamics in the South American fintech market. On balance, the South America fintech industry continues to shift from single-product payments toward multi-product financial services, with credit-led monetization driving the next leg of growth, where consented data support underwriting and collections.

The South America Fintech Market Report is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, Neobanking), End-User (Retail, Businesses), User Interface (Mobile Applications, Web/Browser, POS/IoT Devices), and Geography (Brazil, Peru, Chile, Argentina, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nubank (Nu Holdings)

- Mercado Pago (Mercado Libre)

- PagSeguro (PagBank)

- StoneCo

- PicPay

- Inter&Co (Banco Inter)

- EBANX

- dLocal

- Uala

- C6 Bank

- Creditas

- Neon

- XP Inc.

- BTG Pactual (digital platforms)

- Getnet Brasil (Santander)

- Prisma Medios de Pago (Argentina)

- Naranja X (Argentina)

- Brubank (Argentina)

- MACH (Banco de Chile)

- Khipu (Chile)

- FPay (Falabella)

- Transbank (Chile)

- Yape (Peru)

- Plin (Peru)

- RecargaPay (Brazil)

- SumUp (Brazil)

- Dock (Brazil)

- Pismo (Brazil)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RTP scale-up and features

- 4.2.2 Open finance data portability

- 4.2.3 Embedded finance in platforms

- 4.2.4 SoftPOS and low-cost acceptance

- 4.2.5 Dollar-linked savings via fintech

- 4.2.6 Tokenized deposits and CBDC

- 4.3 Market Restraints

- 4.3.1 High Customer Acquisition Costs and Low Financial Literacy

- 4.3.2 Fee caps squeeze economics

- 4.3.3 APP fraud on instant rails

- 4.3.4 FX controls, settlement frictions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Real-time payments infrastructure status

- 4.8 Merchant acceptance & QR interoperability landscape

- 4.9 Cash-in/Cash-out (CICO) and agent network coverage

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Peru

- 5.4.3 Chile

- 5.4.4 Argentina

- 5.4.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Nubank (Nu Holdings)

- 6.4.2 Mercado Pago (Mercado Libre)

- 6.4.3 PagSeguro (PagBank)

- 6.4.4 StoneCo

- 6.4.5 PicPay

- 6.4.6 Inter&Co (Banco Inter)

- 6.4.7 EBANX

- 6.4.8 dLocal

- 6.4.9 Uala

- 6.4.10 C6 Bank

- 6.4.11 Creditas

- 6.4.12 Neon

- 6.4.13 XP Inc.

- 6.4.14 BTG Pactual (digital platforms)

- 6.4.15 Getnet Brasil (Santander)

- 6.4.16 Prisma Medios de Pago (Argentina)

- 6.4.17 Naranja X (Argentina)

- 6.4.18 Brubank (Argentina)

- 6.4.19 MACH (Banco de Chile)

- 6.4.20 Khipu (Chile)

- 6.4.21 FPay (Falabella)

- 6.4.22 Transbank (Chile)

- 6.4.23 Yape (Peru)

- 6.4.24 Plin (Peru)

- 6.4.25 RecargaPay (Brazil)

- 6.4.26 SumUp (Brazil)

- 6.4.27 Dock (Brazil)

- 6.4.28 Pismo (Brazil)

7 Market Opportunities & Future Outlook

- 7.1 Cross-border instant-payment corridors (e.g., Pix-enabled international flows and merchant-of-record use cases)

- 7.2 SME embedded finance for B2B trade (real-time FX, invoice financing, supply-chain payments)