|

시장보고서

상품코드

2043989

남미의 섬유 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)South America Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

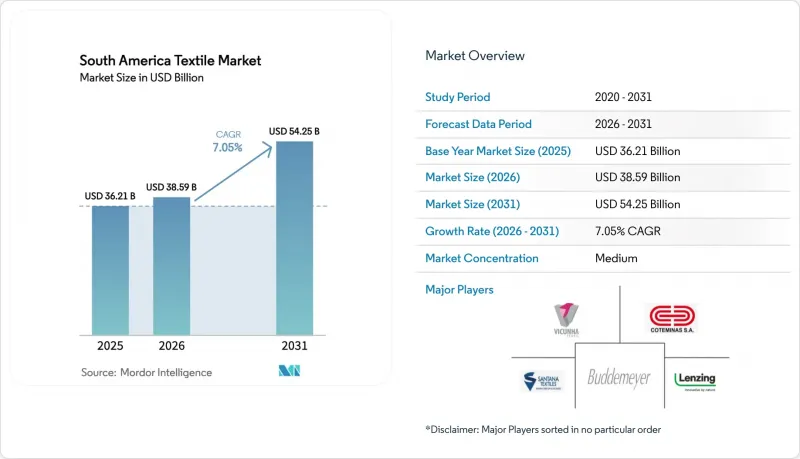

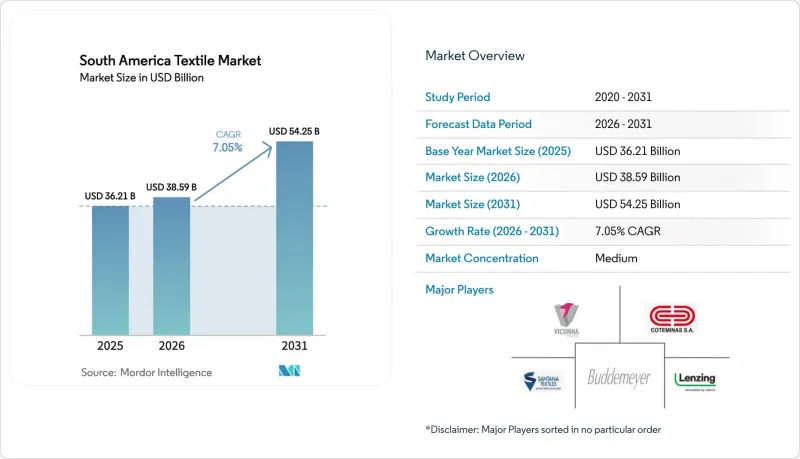

남미의 섬유 시장 규모는 2025년 362억 1,000만 달러로 평가되었습니다. 2026년 385억 9,000만 달러에서 2031년까지 542억 5,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.05%를 나타낼 전망입니다.

브라질과 아르헨티나의 의류 수요의 수혜는 현재 지오섬유, 위생용 부직포, 재생 폴리에스터 섬유의 구조적 성장과 함께 패션 분야를 넘어서는 수익 기반 확대로 이어지고 있습니다. 유럽의 순환경제 기준 강화로 인해 추적 가능한 공급망과 '디지털 제품 여권' 시범사업에 대한 투자가 가속화되고 있으며, 기준을 준수하는 수출업체는 EU에 관세 없이 접근할 수 있게 되었습니다. 렌징과 인드라마의 외국인 직접투자는 지역 내 원자재 확보, 재활용 인프라 강화, 다국적 기업의 면화 가격 변동으로부터 보호해주는 역할을 하고 있습니다. 동시에 상파울루의 비공식 허브는 디자인에서 매장까지의 주기를 14일 이내로 단축하고 있으며, 정규 방적 공장은 주문형 생산을 채택하거나 점유율 하락을 초래할 위험을 감수해야 하는 선택을 해야 합니다. 에너지 가격 변동, 특히 2025년에 예정된 브라질의 전기 요금 12% 인상은 염색 및 마감 부문의 이익률에 계속 압력을 가하고 있습니다.

남미의 섬유 시장 동향 및 인사이트

지역 모빌리티 인프라에 테크니컬 섬유을 보급하는 것

브라질의 2024-2030년 인프라 계획에 따르면, 교통망 정비에 560억 달러가 할당되어 있으며, 그중 많은 부분이 ASTM 표준에 부합하는 부직포 지오섬유을 필요로 합니다. 아르헨티나 바카 무에르타 셰일 프로젝트에서 고강도 폴리에스테르 원단에 대한 수요는 환경 규제 강화를 반영하여 2025년 19% 증가하였습니다. 페루의 광업 부문에서는 현재 꼬리 댐의 보강용 직물이 사양서에 명시되어 있으며, 리마의 유통업체를 통해 유럽 공급업체가 진출하고 있습니다. 브라질의 ABNT NBR 12553과 같은 기술 표준이 시행됨에 따라 조달은 인증된 현지 제조업체로 전환되고 있습니다. 이전에는 감독체계가 느슨하여 규격 미달 수입품이 적합품보다 가격면에서 낮은 경우가 있었기 때문에 일관성 있는 검사가 여전히 매우 중요합니다.

패스트 패션의 사이클과 주문형 제조

상파울루의 브라스 지구와 부에노스아이레스의 라살라 시장에 있는 비공식 클러스터는 2주 안에 소셜 미디어의 트렌드를 완성품으로 만들어냅니다. 마이크로팩토리는 재단, 봉제, 마무리를 한 곳에서 통합하고 도매업체를 거치지 않고 인스타그램, 카카오톡을 통해 판매합니다. 2025년까지 이러한 비공식 사업은 브라질 국내 의류 생산량의 38%를 차지했으며, 그 규모를 실감할 수 있습니다. 정규 공장은 디지털 인쇄와 최소 주문량을 50벌까지 낮춘 모듈식 생산 라인으로 대응하고 있지만, 추적성을 훼손하지 않고 동등한 기동성을 갖추기 위해 여전히 고군분투하고 있습니다. EU 바이어들이 노동 기준의 검증을 요구함에 따라 속도와 규정 준수 사이의 긴장이 높아질 것이며, 비정규 업체들은 합법화를 추진하거나 수출 경로를 축소해야할 것입니다.

에너지 및 원자재 가격 변동

2025년 브라질의 전기 요금이 12% 상승하면서 에너지 집약적인 염색 및 스텐트 가공 사업의 수익률에 대한 압박이 더욱 커졌습니다. 아르헨티나에서는 차코 지역의 가뭄으로 인해 2024년 면화 가격이 18% 급등하여 공장들은 비싼 가격에 수입을 해야만 했습니다. 폴리에스터 원가는 원유 가격 변동이 60일 늦게 반영되기 때문에 고정 가격 의류 계약을 맺은 공장은 위험에 노출되어 있습니다. Indorama의 상파울루 rPET 시설과 같이 재활용 사업을 수직적으로 통합한 생산자는 버진 수지 가격 변동에 대한 헤지를 수행합니다. 이러한 완충기능이 없는 기업은 설비투자를 미루고 있으며, 구매자가 가격 안정성이 높은 공급업체를 선호함에 따라 설비 노후화 위험에 직면하고 있습니다.

부문 분석

남미 섬유 시장에서 패션-의류 부문의 점유율은 55.55%로 여전히 지배적이지만, 재량지출 둔화와 중고품 수입 증가로 인해 성장 속도가 둔화되고 있습니다. 산업 및 테크니컬 섬유 부문은 CAGR 6.15%로 성장하고 있으며, 다른 어떤 용도보다 빠른 속도로 성장하고 있습니다. 수요의 원천은 브라질의 560억 달러 규모의 교통 인프라 개보수를 위한 토목용 지오텍 스타일과 페루의 광업 부문을 위한 여과용 직물입니다. 의류 기업들은 여전히 관세를 피하기 위해 아르헨티나에 니어쇼어링에 투자하고 있지만, 석유, 가스, 건설용 기능성 원단이 조달 예산에서 점점 더 큰 비중을 차지하고 있습니다.

테크니컬 섬유 생산자들은 ASTM 및 ABNT 인증을 의무화하는 공공 조달에 기대를 걸고 있으며, 자체 시험소를 보유한 제조업체가 유리합니다. Ober와 같은 현지 대기업은 ISO 9001 시스템을 도입한 반면, 신규 진출기업은 독일의 전문 기업 HUESKER와 제휴하여 턴키 방식의 침식 방지 솔루션을 제공합니다. 성공의 열쇠는 EU 바이어들이 중요시하는 지속가능성 기준에 부합하는 재생 폴리에스테르 지오그리드의 빠른 상용화에 있습니다. 이에 대해 의류업체들은 높은 가격 책정을 정당화하기 위해 QR코드를 통한 추적 기능을 내장하여 대응하고 있으며, 두 부문이 공존하면서도 기술 플랫폼은 수렴해 나갈 것임을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측(금액 기준 : 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe South America Textile Market size is projected to expand from USD 36.21 billion in 2025 and USD 38.59 billion in 2026 to USD 54.25 billion by 2031, registering a CAGR of 7.05% between 2026 to 2031.

Benefits from apparel demand in Brazil and Argentina now overlap with structural gains in geotextiles, hygiene nonwovens, and recycled-polyester fiber, broadening the revenue base beyond fashion. Higher European circular-economy standards accelerated investment in traceable supply chains and Digital Product Passport pilots, positioning compliant exporters for tariff-free access to the EU. Foreign direct investment from Lenzing and Indorama secures regional feedstock, strengthens recycling infrastructure, and shields multinationals from cotton-price swings. At the same time, Sao Paulo's informal hubs cut design-to-shelf cycles to under 14 days, forcing formal mills to adopt on-demand manufacturing or risk erosion of their share. Energy-price volatility, especially Brazil's 12% electricity hike in 2025, continues to pressure dyeing and finishing margins.

South America Textile Market Trends and Insights

Uptake of Technical Textiles in Regional Mobility & Infrastructure

Brazil's 2024-2030 infrastructure plan earmarks USD 56 billion for transport upgrades, many of which require nonwoven geotextiles that meet ASTM standards. Demand for high-tenacity polyester fabrics in Argentina's Vaca Muerta shale projects rose 19% in 2025, reflecting stricter environmental protocols. Peru's mining sector is now specifying tailings-dam reinforcement fabrics, attracting European suppliers through Lima distributors. Enforcement of engineering standards, such as Brazil's ABNT NBR 12553, tilts procurement toward certified local producers. Consistent inspection remains critical, as lax oversight previously let substandard imports undercut compliant products.

Fast-Fashion Cycles and On-Demand Manufacturing

Informal clusters in Sao Paulo's Bras district and Buenos Aires' La Salada market turn social-media trends into finished garments within two weeks. Micro-factories combine cutting, sewing, and finishing on a single site, bypassing wholesalers and selling on Instagram or WhatsApp. By 2025, these informal operations produced 38% of Brazil's domestic apparel volume, underscoring their scale. Formal mills answer with digital printing and modular lines that trim minimum orders to 50 units, yet still struggle to match the agility without compromising traceability. Tension between speed and compliance will rise as EU buyers demand verified labor standards, pushing informal players either toward legalization or toward shrinking export avenues.

Volatile Energy and Raw-Material Prices

A 12% rise in Brazilian electricity tariffs during 2025 deepened margin pressure for energy-intensive dyeing and stentering operations. Cotton prices in Argentina spiked 18% in 2024 after the Chaco droughts, forcing mills to import at a premium. Polyester costs mirror crude-oil swings with a 60-day lag, leaving mills exposed under fixed-price apparel contracts. Producers with vertically integrated recycling, such as Indorama's Sao Paulo rPET facility, hedge against volatility in virgin resin prices. Firms lacking such buffers delay capex, risking obsolescence as buyers gravitate toward price-stable suppliers.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce and Social-Commerce Compressing Design-to-Shelf Time

- Mandatory EU-27 Separate Textile-Waste Collection (2025)

- High Capex for Advanced Recycling / Sorting Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The South America textile market share of Fashion & Apparel remains dominant at 55.55% yet slowing discretionary spend and mounting second-hand imports temper its pace. The industrial/Technical Textiles segment is advancing at a 6.15% CAGR, faster than any other application. Demand originates from civil-engineering geotextiles for Brazil's USD 56 billion transport overhaul and filtration fabrics keyed to Peru's mining sector. Apparel houses still invest in near-shoring to Argentina to avoid tariffs, but performance fabrics for oil, gas, and construction now capture a growing share of procurement budgets.

Technical textile producers bank on public procurement that mandates ASTM and ABNT certification, favouring mills with in-house labs. Local champions like Ober add ISO 9001 systems, while newcomers partner with German specialist HUESKER to deliver turnkey erosion-control solutions. Success hinges on the rapid commercialization of recycled-polyester geogrids that align with EU buyers' sustainability scorecards. Apparel mills counter by embedding QR-coded traceability to justify higher price points, signalling that both segments will coexist but with converging technology platforms.

The South America Textile Market Report is Segmented by Application (Fashion & Apparel, Industrial/Technical, and More), by Raw Material (Natural Fibers, Synthetic Fibers, Recycled Fibers, Specialty High-Performance Fibers), by Process/Technology (Woven, Knitted, Non-Woven, 3D Weaving & Spacer Fabrics), and by Geography (Brazil, Argentina, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vicunha Textil

- Coteminas S.A.

- Santana Textiles Group

- Buddemeyer S.A.

- Springs Global

- Lenzing AG

- Freudenberg Performance Materials

- Indorama Ventures (PET Brazil)

- Ahlstrom-Munksjo

- Beaulieu Technical Textiles

- HUESKER Synthetic GmbH

- TWE Group

- PFNonwovens

- DuPont de Nemours

- Berry Global Group

- Toray Industries

- Schoeller Textil AG

- Borgers SE & Co. KG

- Kaltex Textiles

- Albini Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fast-fashion cycles & on-demand manufacturing

- 4.2.2 Mandatory EU-27 separate textile-waste collection (2025)

- 4.2.3 E-commerce & social-commerce compressing design-to-shelf time

- 4.2.4 Uptake of technical textiles in regional mobility & infrastructure

- 4.2.5 Surging investor interest in low-impact South-American natural fibres

- 4.2.6 Blockchain-enabled "Digital Product Passport" pilots in MERCOSUR

- 4.3 Market Restraints

- 4.3.1 Volatile energy & raw-material prices

- 4.3.2 High capex for advanced recycling / sorting capacity

- 4.3.3 Skilled-labour shortages (dyeing, finishing, automation)

- 4.3.4 SME fragmentation vs. new ESG / due-diligence compliance

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geopolitics on Textile Market

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Application

- 5.1.1 Fashion & Apparel

- 5.1.2 Industrial/Technical Textiles

- 5.1.3 Household & Home Textiles

- 5.1.4 Medical & Healthcare Textiles

- 5.1.5 Automotive & Transport Textiles

- 5.1.6 Others (Protective, Sports Textiles, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibers

- 5.2.1.1 Cotton

- 5.2.1.2 Wool

- 5.2.1.3 Silk

- 5.2.2 Synthetic Fibers

- 5.2.2.1 Polyester

- 5.2.2.2 Nylon

- 5.2.2.3 Rayon / Viscose

- 5.2.2.4 Acrylic

- 5.2.2.5 Polypropylene

- 5.2.3 Recycled Fibers

- 5.2.4 Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- 5.2.1 Natural Fibers

- 5.3 By Process / Technology

- 5.3.1 Woven

- 5.3.2 Knitted

- 5.3.3 Non-woven

- 5.3.3.1 Spunlaid (Spunbond / Melt-blown)

- 5.3.3.2 Dry-laid Hydro-entangled

- 5.3.3.3 Wet-Laid

- 5.3.3.4 Needle-punched

- 5.3.4 3-D Weaving & Spacer Fabrics

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Peru

- 5.4.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Vicunha Textil

- 6.4.2 Coteminas S.A.

- 6.4.3 Santana Textiles Group

- 6.4.4 Buddemeyer S.A.

- 6.4.5 Springs Global

- 6.4.6 Lenzing AG

- 6.4.7 Freudenberg Performance Materials

- 6.4.8 Indorama Ventures (PET Brazil)

- 6.4.9 Ahlstrom-Munksjo

- 6.4.10 Beaulieu Technical Textiles

- 6.4.11 HUESKER Synthetic GmbH

- 6.4.12 TWE Group

- 6.4.13 PFNonwovens

- 6.4.14 DuPont de Nemours

- 6.4.15 Berry Global Group

- 6.4.16 Toray Industries

- 6.4.17 Schoeller Textil AG

- 6.4.18 Borgers SE & Co. KG

- 6.4.19 Kaltex Textiles

- 6.4.20 Albini Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment