|

시장보고서

상품코드

2044005

자동차용 반도체 실리콘 웨이퍼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Semiconductor Silicon Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

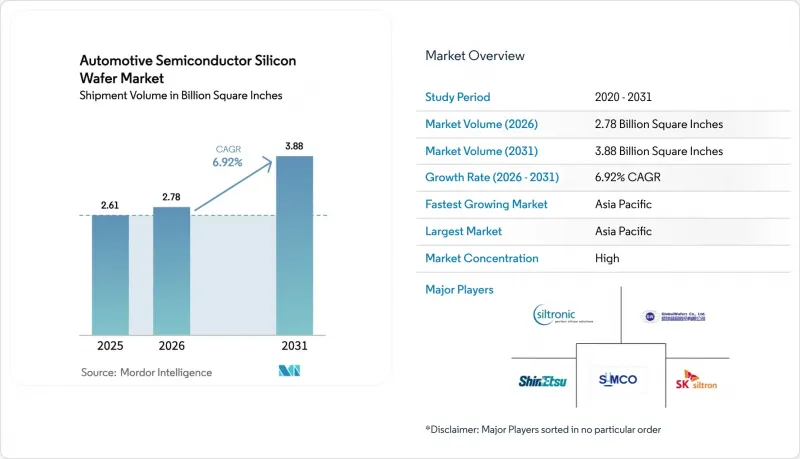

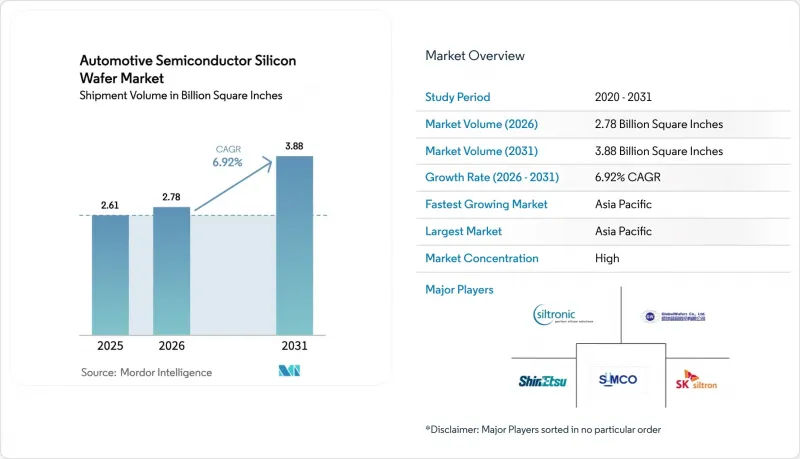

자동차용 반도체 실리콘 웨이퍼 시장 규모는 2025년 26억 1,000만 평방인치로 평가되었습니다. 2026년에는 27억 8,000만 평방인치로 확대되어 2031년까지 38억 8,000만 평방인치에 이를 것으로 예상되며 2026-2031년에 걸쳐 CAGR 6.92%를 나타낼 전망입니다.

이러한 확장은 승용차의 급속한 전기화, 800V 배터리 팩으로의 전환, 소프트웨어 정의 차량 컴퓨팅 영역의 부상으로 인해 주도되고 있습니다. 200mm 기판의 와이드 밴드갭 SiC 에피택셜 웨이퍼가 증가분의 대부분을 차지하고 있지만, 여전히 프라임 연마 실리콘의 출하량이 가장 많은 것으로 나타났습니다. 미국, 유럽, 한국, 인도 등의 정책적 인센티브로 팹의 투자 회수 기간은 단축되고 있지만, 지속적인 기판 부족과 자동차 등급 인증 주기가 길어지고 있는 것이 단기적인 생산량을 억제하고 있습니다. 수직 통합과 300mm로의 전환에 따른 경쟁적인 움직임이 비용 곡선을 재구성하고 있으며, 이는 자동차용 반도체 실리콘 웨이퍼 시장의 향후 궤도를 결정하게 될 것입니다.

세계의 자동차용 반도체 실리콘 웨이퍼 시장 동향 및 인사이트

전기차 보급 확대와 800V 차량 플랫폼으로의 전환

800V 배터리 팩을 장착한 전기차 모델에는 1,200V 정격의 SiC MOSFET이 필요하며, 이를 위해서는 200mm 에피택셜 웨이퍼의 기판면 전위 밀도가 매우 낮아야 합니다. 현대자동차의 '아이오닉 5', 기아자동차의 'EV6'와 같은 신차 출시에 따라 Porsche, Audi, General Motors도 2026년형에 대한 유사한 로드맵을 수립하고 있습니다. Infineon의 크림 공장의 생산 능력 증설과 STMicroelectronics가 체결한 장기 웨이퍼 공급 계약은 생산량 증가에 앞서 재료를 확보하기 위한 경쟁에 대해 잘 보여주고 있습니다. 이러한 구조적 수요로 인해 리드타임이 12개월 이상 소요되고 있어 안정적인 기판 확보가 얼마나 중요한지 강조하고 있습니다.

800V 충전 인프라의 신속한 정비

초급속 충전에 대한 공공 및 민간 투자는 2025년 120억 달러를 넘어섰으며, 유럽의 AFIR 규정에 따라 2027년까지 주요 간선도로를 따라 60km마다 400kW의 충전기를 설치하도록 의무화되어 있습니다. 800V 자동차용 충전기 1대당 150mm-200mm 웨이퍼에 형성된 6-8개의 SiC MOSFET이 내장되어 있어, 충전기 도입 가속화는 웨이퍼 수요 증가와 직결됩니다. 중국 내 도입량은 이미 전 세계 800V 충전스탠드의 60% 이상을 차지하며 아시아태평양의 우위를 점하고 있습니다. 소이테크의 Power-SOI 기판은 PCB 면적이 한정된 게이트 드라이버 소켓 시장에서 채택이 확대되고 있습니다. OBC의 설계 주기가 인프라 구축보다 약 18개월 정도 늦기 때문에 본격적인 수요 증가는 2027-2028년 사이에 나타날 것으로 보입니다.

200mm 기판 공급 부족

2025년 세계 생산능력은 200mm SiC 웨이퍼 기준 120만 장에 불과했지만, 자동차 수요는 2028년까지 200만 장을 넘어설 것으로 예측됩니다. PVT 리액터 1기당 비용이 최대 800만 달러에 달하고, 인증에 18-24개월이 소요되기 때문에 공급 상황의 획기적인 개선은 늦어질 것으로 예측됩니다. 울프스피드의 사일러시티 공장 증설은 2027년까지 지속되는 반면, 유럽과 북미 OEM 업체들은 여전히 아시아로부터의 수입에 크게 의존하고 있습니다. 이러한 공급 부족으로 인해 이중 소싱이 불가피하고 설계 주기가 길어지면서 단기적으로 이 부문의 CAGR을 1.2% 낮추는 요인으로 작용할 것으로 보입니다.

부문 분석

200mm 웨이퍼는 2025년 자동차용 반도체 실리콘 웨이퍼 시장의 56.48%를 차지했으며, SiC 파워디스크리트, 게이트 드라이버, PMIC에 여전히 필수적입니다. 감가상각이 완료된 성숙한 노드 라인은 여전히 매력적인 영업 이익률을 유지하고 있으며, 트랙션 MOSFET의 다이 사이즈는 200mm 웨이퍼의 경제성에 적합합니다. 그러나 Texas Instruments, TSMC, GlobalWafers가 MCU 및 혼합 신호 IC를 더 큰 웨이퍼로 전환하고 다이당 비용을 20% 이상 절감함에 따라 300mm 생산 능력은 CAGR 7.45%로 증가하고 있습니다. Wolfspeed의 300mm SiC 샘플은 1cm2 이하의 결함 밀도를 달성하여 기술적 타당성을 입증하고 2028년 이후 파워 디바이스의 대량 공급을 위한 길을 보여주고 있습니다.

자동차용 반도체 실리콘 웨이퍼 시장은 양극화될 것으로 예측됩니다. 인증 장벽이 제거되면 300mm가 컴퓨팅 및 혼합 신호 부문을 지배하는 반면, 결정 성장 기술이 따라잡기 전까지는 SiC 부문에서 200mm가 계속 사용될 것으로 예측됩니다. 150mm 이하의 형태는 구식 팹의 폐지에 따라 축소 추세가 지속되고 있지만, 사이리스터 및 커스텀 아날로그용 수요는 일부 남아 있습니다. 소이테크는 배터리 관리 수요에 대응하기 위해 Power-SOI를 300mm로 전환하고 있으며, 이는 전동화 프로그램에서 보다 엄격한 비용 구조가 요구되고 있음을 보여줍니다.

"자동차용 반도체 실리콘 웨이퍼 시장 보고서"는 웨이퍼 직경(150mm 이하, 200mm, 300mm), 반도체 디바이스 유형(로직, 메모리, 아날로그, 디스크리트, 기타), 웨이퍼 유형(프라임 폴리싱, 에피택셜, SOI, 특수 실리콘), 지역(북미, 유럽, 아시아태평양, 남미, 중동, 아프리카, 아시아태평양) 유럽, 아시아태평양, 남미, 중동 및 아프리카), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)으로 분류됩니다. 시장 예측은 수량(평방인치) 기준으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 자동차용 반도체 실리콘 웨이퍼 시장에서 84.19%의 점유율을 차지하며 CAGR 7.59%를 나타낼 것으로 예측됩니다. 대만은 6nm 이하 생산능력에서 상당한 점유율을 차지하고 있으며, 성숙 노드 자동차 웨이퍼의 40% 이상을 차지하고 있지만, 중국은 SiC 결정 성장, 에피택시, 디바이스 제조 공장의 통합을 추진하고 있습니다. 한국의 700조원(5,250억 달러) 규모의 전략으로 10개의 신규 시설과 화합물 반도체 라인이 추가되어 지역 기반이 강화되고 있습니다. 일본의 기판 대기업인 Shin-Etsu Chemical과 SUMCO 등이 300mm 프라임 연마 웨이퍼와 SiC 에피택시 웨이퍼 공급을 주도하고 있으며, 인도 정부가 지원하는 12인치 라인은 2026년월5만장 생산 체제를 구축할 예정입니다.

북미는 2025년 출하량 점유율은 작았지만, 'CHIPS법'의 인센티브에 따라 GlobalWafers의 300mm 공장과 Wolfspeed의 SiC 메가팹이 자금을 지원받아 2028년까지 연간 100만장 이상의 200mm 웨이퍼를 추가 생산할 것으로 예측됩니다. 추가 생산될 것으로 예측됩니다. 그러나 현지화 추진에도 불구하고 미국의 경차 생산량이 연간 1,500만 대를 넘어선 가운데, 많은 모듈은 여전히 아시아산 기판에 의존하고 있습니다. 유럽은 상당한 점유율을 차지하고 있으며, Infineon, STMicroelectronics, 세계 웨이버스의 생산능력 확장에 사용된 IPCEI-ME/CT의 자금 지원의 혜택을 받고 있지만, 프라임 연마 웨이퍼 수요의 70% 이상을 수입에 의존하고 있습니다.

남미와 더불어 중동 및 아프리카는 생태계의 깊이가 제한적이고 자본의 장벽으로 인해 생산량은 여전히 낮은 수준에 머물러 있습니다. 공급망 리스크를 줄이기 위해 자동차 제조업체들은 현재 여러 지역공급처를 공동으로 인증하고 있지만, 자동차 등급의 18-24개월 주기로 인해 실질적인 다변화는 2027년 후반까지 지연될 것으로 예측됩니다. 2024년 하반기부터 시작된 재고 조정은 2026년 초에 바닥을 친 것으로 보이며, 새로운 장기 공급 계약에 따라 웨이퍼 주문은 회복세를 보이고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The automotive semiconductor silicon wafer market size is expected to increase from 2.61 Billion Square Inches in 2025 to 2.78 billion Square Inches in 2026 and reach 3.88 Billion Square Inches by 2031, growing at a CAGR of 6.92% over 2026-2031.

The expansion is powered by the rapid electrification of passenger vehicles, the migration to 800-volt battery packs, and the rise of software-defined vehicle compute domains. Wide-bandgap SiC epitaxial wafers on 200 mm substrates are absorbing much of the incremental volume, even as prime-polished silicon continues to ship the most pieces. Policy incentives in the United States, Europe, South Korea, and India are shortening fab paybacks, while ongoing substrate shortages and long automotive-grade qualification cycles moderate near-term output. Competitive moves toward vertical integration and 300 mm migration are reshaping cost curves and will decide the future trajectory of the automotive semiconductor silicon wafer market.

Global Automotive Semiconductor Silicon Wafer Market Trends and Insights

Rising EV Penetration And Shift Toward 800V Vehicle Platforms

Electric models built on 800-volt packs need SiC MOSFETs rated at 1,200 V, which in turn require 200 mm epitaxial wafers with extremely low basal-plane dislocation densities. Launches such as Hyundai's Ioniq 5 and Kia's EV6 have triggered similar roadmaps from Porsche, Audi, and General Motors for model-year 2026 designs. Capacity additions at Infineon's Kulim facility and long-term wafer supply agreements signed by STMicroelectronics underscore the race to lock in material ahead of volume hikes. The structural pull tightens lead times beyond 12 months and underscores the importance of secure substrate access.

Rapid Build-Out Of 800V Charging Infrastructure

Public and private spending on ultra-fast charging surpassed USD 12 billion in 2025, and Europe's AFIR rule mandates 400 kW chargers every 60 km on core corridors by 2027. Each 800 V on-board charger integrates six to eight SiC MOSFETs grown on 150 mm- to 200-mm wafers, so faster charger rollouts translate directly into increased wafer demand. Chinese deployments already account for more than 60% of global 800 V posts, reinforcing Asia-Pacific's dominance. Soitec's Power-SOI substrates are winning gate-driver sockets where PCB area is tight. Because OBC design cycles lag infrastructure by roughly 18 months, the full volume effect will surface between 2027 and 2028.

Limited Availability Of 200 mm Substrates

Global capacity reached only 1.2 million 200 mm SiC wafers in 2025, yet automotive demand will surpass 2 million units before 2028. Each PVT reactor costs up to USD 8 million and needs 18-24 months to qualify, delaying meaningful relief. Wolfspeed's Siler City expansion runs through 2027, while European and North American OEMs still rely heavily on Asian imports. The shortage forces dual-sourcing and stretches design cycles, trimming 1.2 percentage points off the sector CAGR in the near term.

Other drivers and restraints analyzed in the detailed report include:

- High-Temperature, High-Frequency Performance Advantages Over Si

- Government Incentives For Wide-Band-Gap Fabs

- Packaging-Induced Thermo-Mechanical Stress

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 200 mm tranche held 56.48% automotive semiconductor silicon wafer market share in 2025 and remains indispensable for SiC power discretes, gate drivers, and PMICs. Mature-node lines already depreciated keep operating margins attractive, and the die sizes of traction MOSFETs fit 200 mm economics well. However, 300 mm capacity is climbing at a 7.45% CAGR because Texas Instruments, TSMC, and GlobalWafers are shifting MCUs and mixed-signal ICs onto larger wafers, driving 20%-plus cost reductions per die. Wolfspeed's 300 mm SiC samples delivered sub-1 cm-2 defect densities, proving technical feasibility and pointing toward high-volume power-device supply after 2028.

The automotive semiconductor silicon wafer market is likely to bifurcate, 300 mm will dominate compute and mixed-signal content once qualification barriers fall, while 200 mm persists in SiC until crystal growth catches up. Up-to-150 mm formats continue sliding as legacy fabs retire, although they retain pockets of demand for thyristors and custom analog. Soitec is migrating Power-SOI to 300 mm to meet demand for battery management, highlighting the need for tighter cost structures in electrification programs.

The Automotive Semiconductor Silicon Wafer Market Report is Segmented by Wafer Diameter (Up To 150 Mm, 200 Mm, and 300 Mm), Semiconductor Device Type (Logic, Memory, Analog, Discrete, and Other Types), Wafer Type (Prime Polished, Epitaxial, SOI, and Specialty Silicon), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific held 84.19% automotive semiconductor silicon wafer market share in 2025 and is expanding at 7.59% CAGR. Taiwan accounts for a considerable share of sub-6 nm capacity and more than 40% of mature-node automotive wafer starts, while China continues to integrate SiC crystal growth, epitaxy, and device fabs. South Korea's 700 trillion KRW (USD 525 billion) strategy adds 10 new facilities and compound-semiconductor lines, reinforcing regional depth. Japan's substrate majors, including Shin-Etsu and SUMCO, anchor 300 mm prime polished and SiC epitaxial supply, and India's state-backed 12-inch line will bring 50,000 wafers per month online in 2026.

North America controlled a small share of shipments in 2025, but CHIPS Act incentives fund GlobalWafers' 300 mm plant and Wolfspeed's SiC megafab, together adding more than one million 200 mm-equivalent wafers annually by 2028. The localization push, however, still leaves many modules reliant on Asian substrates, as U.S. light-vehicle output surpasses 15 million units yearly. Europe holds a considerable share and benefits from IPCEI-ME/CT funding for capacity at Infineon, STMicroelectronics, and GlobalWafers, yet imports cover over 70% of prime polished demand.

South America plus Middle East and Africa together remain low due to limited ecosystem depth and capital barriers. To mitigate supply-chain risk, automakers now co-qualify multiple geographic sources even though the 18-to-24-month automotive-grade cycle delays meaningful diversification until late 2027. Inventory corrections that began in late-2024 appear to have bottomed by early-2026, and wafer call-offs are rebounding under new long-term supply agreements.

- Shin-Etsu Chemical Co., Ltd.

- SUMCO Corporation

- Siltronic AG

- GlobalWafers Co., Ltd.

- SK Siltron Co., Ltd.

- Soitec S.A.

- Okmetic Oy

- Wafer Works Corp.

- Topsil Semiconductor Materials A/S

- Shanghai Simgui Technology Co., Ltd.

- MEMC Electronic Materials, Inc.

- Infineon Technologies AG

- ON Semiconductor Corp.

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Renesas Electronics Corp.

- Texas Instruments Inc.

- X-FAB Silicon Foundries SE

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Technology Analysis

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Market Drivers

- 4.6.1 Rising EV Penetration and Shift Toward 800-V Vehicle Platforms

- 4.6.2 Rapid Build-Out of 800 V Charging Infrastructure

- 4.6.3 High-Temperature, High-Frequency Performance Advantages Over Si

- 4.6.4 Government Incentives for Wide-Band-Gap Fabs

- 4.6.5 Emergence of Vertically-Integrated SiC Supply Chains in China

- 4.6.6 Novel 200 mm Bulk-Growth Breakthroughs Lowering Defect Density

- 4.7 Market Restraints

- 4.7.1 Limited Availability of 200 mm Substrates

- 4.7.2 Packaging-Induced Thermo-Mechanical Stress

- 4.7.3 Capital-Intensive Crystal-Growth Equipment

- 4.7.4 Recycling Challenges for SiC Kerf Waste

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 Up to 150 mm

- 5.1.2 200 mm

- 5.1.3 300 mm

- 5.2 By Semiconductor Device Type

- 5.2.1 Logic

- 5.2.2 Memory

- 5.2.3 Analog

- 5.2.4 Discrete

- 5.2.5 Other Semiconductor Device Types

- 5.3 By Wafer Type

- 5.3.1 Prime Polished

- 5.3.2 Epitaxial

- 5.3.3 Silicon-on-Insulator (SOI)

- 5.3.4 Specialty Silicon (High-Resistivity, Power, Sensor-Grade)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Taiwan

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Shin-Etsu Chemical Co., Ltd.

- 6.4.2 SUMCO Corporation

- 6.4.3 Siltronic AG

- 6.4.4 GlobalWafers Co., Ltd.

- 6.4.5 SK Siltron Co., Ltd.

- 6.4.6 Soitec S.A.

- 6.4.7 Okmetic Oy

- 6.4.8 Wafer Works Corp.

- 6.4.9 Topsil Semiconductor Materials A/S

- 6.4.10 Shanghai Simgui Technology Co., Ltd.

- 6.4.11 MEMC Electronic Materials, Inc.

- 6.4.12 Infineon Technologies AG

- 6.4.13 ON Semiconductor Corp.

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 NXP Semiconductors N.V.

- 6.4.16 Renesas Electronics Corp.

- 6.4.17 Texas Instruments Inc.

- 6.4.18 X-FAB Silicon Foundries SE

- 6.4.19 Wolfspeed, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment